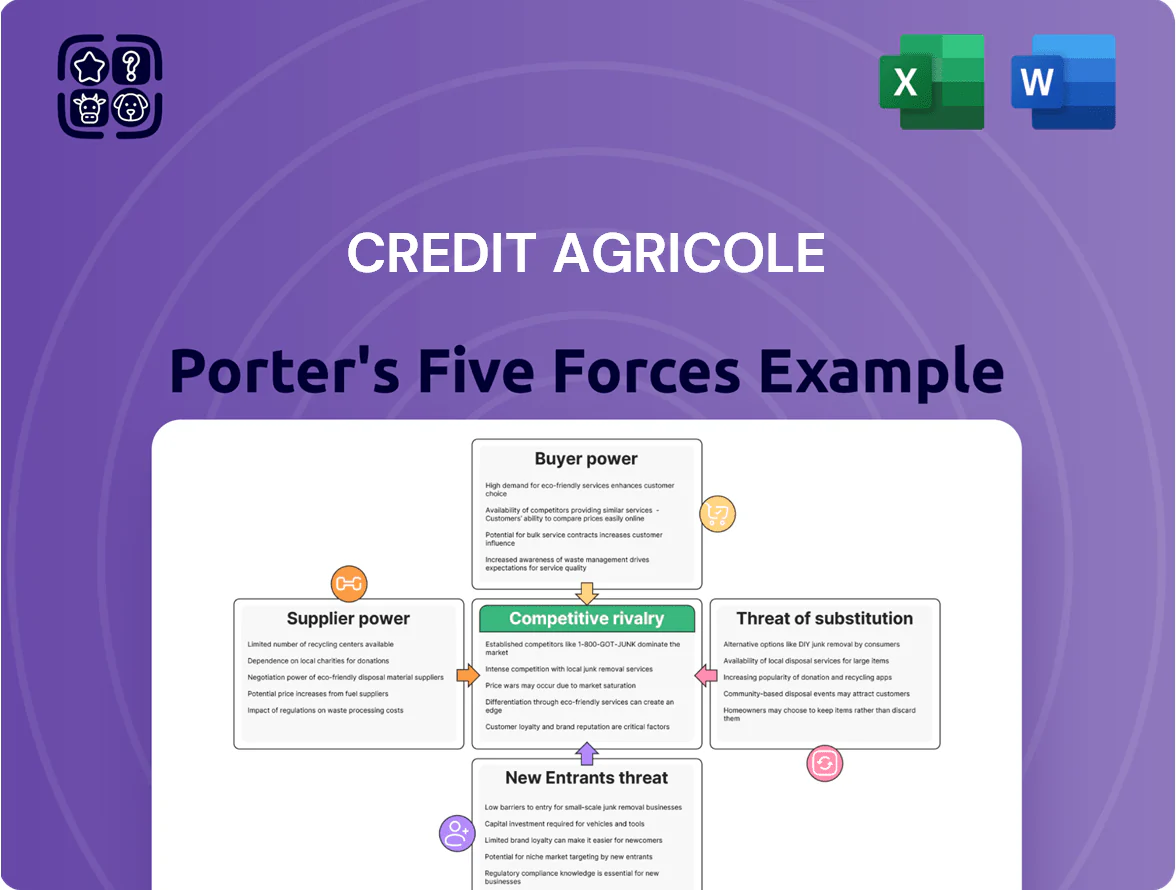

Credit Agricole Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Credit Agricole faces moderate buyer power, regulatory pressures, and rising fintech competition that reshape its margins and growth pathways; supplier power and substitution risks remain manageable but evolving with digitalization. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Credit Agricole’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Influence of Central Bank Monetary Policy

The European Central Bank (ECB) is Crédit Agricole’s main liquidity supplier and sets its base funding cost; ECB deposit rate at 4.00% and main refinancing rate at 4.25% (Dec 2025) directly shape the group’s borrowing cost and net interest margin.

Dependence on Global Tech Infrastructure Providers

Competition for Specialized Financial and Tech Talent

The global shortage of data scientists and risk specialists tightened in 2024, with LinkedIn reporting 65% year-on-year rises in demand for AI and risk roles; these specialists act as suppliers of human capital who can demand 20–50% higher pay and hybrid flexibility. Crédit Agricole must outbid banks and FAANG firms to meet its 2025 targets, where hiring costs could rise EBITDA-adjusted wage pressure by ~0.5–1.2 percentage points.

Bargaining Strength of Retail Depositors

Individual retail depositors supply the cooperative capital base crucial for Credit Agricole’s lending; one depositor has little sway, but mass shifts can strain liquidity.

In 2025, instant digital transfers and higher-yield alternatives raised collective leverage; French household deposits fell 0.8% y/y in Q4 2024, boosting sensitivity to outflows.

- Retail deposits = core funding for CA Group

- Single depositor power: minimal

- Collective shifts: can force higher rates or asset sales

- 2024–25 data: France household deposits -0.8% y/y Q4 2024

- Digital transfers increase outflow speed

Strategic Partnerships with Third-Party Fintechs

Crédit Agricole integrates niche fintechs to boost offerings; by 2024 it had 120+ partnerships across payments, agritech and wealthtech, raising digital revenue share by ~9% year-over-year.

These providers wield supplier power via patented IP and unique APIs, making switching costly and risky for customer retention.

Keeping ties is critical: fintech-enabled features cut churn and time-to-market—losing them risks falling behind faster digital rivals.

- 120+ fintech partners (2024)

- Digital revenue up ~9% YoY (2024)

- High switching costs due to proprietary IP

- Partnerships reduce churn and speed product launch

Suppliers tighten margins: ECB rates, cloud & GPU concentration, fintech churn

Suppliers exert medium-high power: ECB rates (deposit 4.00%, refi 4.25% as of Dec 2025) set core funding cost; cloud vendors (AWS/Azure/GCP >60% share in 2024) and GPU vendors concentrate tech supply; retail deposit outflows (France household deposits -0.8% y/y Q4 2024) and 120+ fintech partners raise switching costs and wage pressure (AI/risk hiring up 65% in 2024).

| Supplier | Key stat |

|---|---|

| ECB rates | Deposit 4.00% / Refi 4.25% (Dec 2025) |

| Cloud | AWS/Azure/GCP >60% (2024) |

| Retail deposits | France -0.8% y/y Q4 2024 |

| Fintech partners | 120+ (2024) |

What is included in the product

Tailored Porter's Five Forces for Crédit Agricole: concise assessment of competitive rivalry, buyer/supplier power, entry barriers, and substitution threats, highlighting disruptive forces, regulatory and market dynamics that shape the bank’s pricing power and strategic positioning.

A concise Porter's Five Forces snapshot for Crédit Agricole—quickly gauge competitive pressures and regulatory risks to steer strategy and investment decisions.

Customers Bargaining Power

Low Switching Costs in Digital Retail Banking

Retail customers in 2025 face EU-mandated simplified account switching (PSD2-era updates), raising their bargaining power; 38% of EU consumers say switching banking providers is easier now (Eurostat 2024). Mobile app proliferation—> 85% smartphone banking uptake in France (2024 Banque de France)—lets users compare fees and move primary relationships with low friction. Crédit Agricole must cut fees and upgrade UX to retain clients, or risk churn above industry avg 12%.

High Transparency through Comparison Platforms

The ubiquity of digital comparison tools lets retail and corporate clients compare Crédit Agricole rates and insurance premiums in real time; 72% of French consumers used comparison sites for banking in 2024, per Médiamétrie. This transparency cuts information asymmetry and lets customers demand pricing matching top market offers, pressuring margins. As a result, Crédit Agricole must justify pricing with better service or brand trust to retain business.

Negotiating Leverage of Large Corporate Clients

Corporate and investment banking clients hold strong negotiating leverage over Crédit Agricole because the top 100 corporate clients generated roughly 22% of group revenues in 2024, concentrating revenue risk. These clients use multiple banking partners and can move mandates quickly—global borrowers shifted an estimated €45bn of syndicated loan volume among banks in 2024—so price and service differences matter. Retention therefore demands bespoke capital-structure solutions, tailored M&A advice, and competitive credit pricing often near market swap+ spreds. Losing one major client can cut earnings materially, so CA must match peers on fees and risk appetite.

Rising Demand for ESG-Compliant Products

By end-2025, about 60% of EU institutional investors and 48% of retail investors say ESG guides allocations, boosting customer leverage over banks’ product mixes.

Clients pick lenders with net-zero targets and green product ranges, so Crédit Agricole risks share loss to ESG-focused banks if it lags on green bonds, sustainability-linked loans, and transition finance.

- 60% EU institutions favor ESG (2025 survey)

- 48% retail investors prioritize ESG (2025)

- Crédit Agricole must expand green bonds, SLLs, and transition finance

Growth of Sophisticated Wealth Management Clients

- HNWIs control ~55% global wealth (Capgemini 2024)

- Demand for lower fees ↑; average private-banking fee decline ~10–20% since 2019

- Value-add: tax, estate, direct co-invest, ESG

Cut fees, boost UX & green products—retain customers as switching and ESG tilt rises

Customers’ bargaining power is high: 38% find switching easier (Eurostat 2024), 85% smartphone banking uptake in France (Banque de France 2024), top 100 corporates = 22% group revenue (Crédit Agricole 2024), HNWIs hold ~55% global wealth (Capgemini 2024), 60% institutions and 48% retail favor ESG (2025 surveys); CA must cut fees, boost UX, and expand green products to retain share.

| Metric | Value |

|---|---|

| Switching ease | 38% (Eurostat 2024) |

| Smartphone banking FR | 85% (Banque de France 2024) |

| Top100 revenue | 22% (CA 2024) |

| HNW wealth | ~55% (Capgemini 2024) |

| ESG preference | 60% inst / 48% retail (2025) |

Preview Before You Purchase

Credit Agricole Porter's Five Forces Analysis

This preview shows the exact Credit Agricole Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use.

You're looking at the same professional document that will be available for instant download upon payment; it contains the complete Five Forces assessment, insights, and actionable implications for decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Credit Agricole faces moderate buyer power, regulatory pressures, and rising fintech competition that reshape its margins and growth pathways; supplier power and substitution risks remain manageable but evolving with digitalization. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Credit Agricole’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Influence of Central Bank Monetary Policy

The European Central Bank (ECB) is Crédit Agricole’s main liquidity supplier and sets its base funding cost; ECB deposit rate at 4.00% and main refinancing rate at 4.25% (Dec 2025) directly shape the group’s borrowing cost and net interest margin.

Dependence on Global Tech Infrastructure Providers

Competition for Specialized Financial and Tech Talent

The global shortage of data scientists and risk specialists tightened in 2024, with LinkedIn reporting 65% year-on-year rises in demand for AI and risk roles; these specialists act as suppliers of human capital who can demand 20–50% higher pay and hybrid flexibility. Crédit Agricole must outbid banks and FAANG firms to meet its 2025 targets, where hiring costs could rise EBITDA-adjusted wage pressure by ~0.5–1.2 percentage points.

Bargaining Strength of Retail Depositors

Individual retail depositors supply the cooperative capital base crucial for Credit Agricole’s lending; one depositor has little sway, but mass shifts can strain liquidity.

In 2025, instant digital transfers and higher-yield alternatives raised collective leverage; French household deposits fell 0.8% y/y in Q4 2024, boosting sensitivity to outflows.

- Retail deposits = core funding for CA Group

- Single depositor power: minimal

- Collective shifts: can force higher rates or asset sales

- 2024–25 data: France household deposits -0.8% y/y Q4 2024

- Digital transfers increase outflow speed

Strategic Partnerships with Third-Party Fintechs

Crédit Agricole integrates niche fintechs to boost offerings; by 2024 it had 120+ partnerships across payments, agritech and wealthtech, raising digital revenue share by ~9% year-over-year.

These providers wield supplier power via patented IP and unique APIs, making switching costly and risky for customer retention.

Keeping ties is critical: fintech-enabled features cut churn and time-to-market—losing them risks falling behind faster digital rivals.

- 120+ fintech partners (2024)

- Digital revenue up ~9% YoY (2024)

- High switching costs due to proprietary IP

- Partnerships reduce churn and speed product launch

Suppliers tighten margins: ECB rates, cloud & GPU concentration, fintech churn

Suppliers exert medium-high power: ECB rates (deposit 4.00%, refi 4.25% as of Dec 2025) set core funding cost; cloud vendors (AWS/Azure/GCP >60% share in 2024) and GPU vendors concentrate tech supply; retail deposit outflows (France household deposits -0.8% y/y Q4 2024) and 120+ fintech partners raise switching costs and wage pressure (AI/risk hiring up 65% in 2024).

| Supplier | Key stat |

|---|---|

| ECB rates | Deposit 4.00% / Refi 4.25% (Dec 2025) |

| Cloud | AWS/Azure/GCP >60% (2024) |

| Retail deposits | France -0.8% y/y Q4 2024 |

| Fintech partners | 120+ (2024) |

What is included in the product

Tailored Porter's Five Forces for Crédit Agricole: concise assessment of competitive rivalry, buyer/supplier power, entry barriers, and substitution threats, highlighting disruptive forces, regulatory and market dynamics that shape the bank’s pricing power and strategic positioning.

A concise Porter's Five Forces snapshot for Crédit Agricole—quickly gauge competitive pressures and regulatory risks to steer strategy and investment decisions.

Customers Bargaining Power

Low Switching Costs in Digital Retail Banking

Retail customers in 2025 face EU-mandated simplified account switching (PSD2-era updates), raising their bargaining power; 38% of EU consumers say switching banking providers is easier now (Eurostat 2024). Mobile app proliferation—> 85% smartphone banking uptake in France (2024 Banque de France)—lets users compare fees and move primary relationships with low friction. Crédit Agricole must cut fees and upgrade UX to retain clients, or risk churn above industry avg 12%.

High Transparency through Comparison Platforms

The ubiquity of digital comparison tools lets retail and corporate clients compare Crédit Agricole rates and insurance premiums in real time; 72% of French consumers used comparison sites for banking in 2024, per Médiamétrie. This transparency cuts information asymmetry and lets customers demand pricing matching top market offers, pressuring margins. As a result, Crédit Agricole must justify pricing with better service or brand trust to retain business.

Negotiating Leverage of Large Corporate Clients

Corporate and investment banking clients hold strong negotiating leverage over Crédit Agricole because the top 100 corporate clients generated roughly 22% of group revenues in 2024, concentrating revenue risk. These clients use multiple banking partners and can move mandates quickly—global borrowers shifted an estimated €45bn of syndicated loan volume among banks in 2024—so price and service differences matter. Retention therefore demands bespoke capital-structure solutions, tailored M&A advice, and competitive credit pricing often near market swap+ spreds. Losing one major client can cut earnings materially, so CA must match peers on fees and risk appetite.

Rising Demand for ESG-Compliant Products

By end-2025, about 60% of EU institutional investors and 48% of retail investors say ESG guides allocations, boosting customer leverage over banks’ product mixes.

Clients pick lenders with net-zero targets and green product ranges, so Crédit Agricole risks share loss to ESG-focused banks if it lags on green bonds, sustainability-linked loans, and transition finance.

- 60% EU institutions favor ESG (2025 survey)

- 48% retail investors prioritize ESG (2025)

- Crédit Agricole must expand green bonds, SLLs, and transition finance

Growth of Sophisticated Wealth Management Clients

- HNWIs control ~55% global wealth (Capgemini 2024)

- Demand for lower fees ↑; average private-banking fee decline ~10–20% since 2019

- Value-add: tax, estate, direct co-invest, ESG

Cut fees, boost UX & green products—retain customers as switching and ESG tilt rises

Customers’ bargaining power is high: 38% find switching easier (Eurostat 2024), 85% smartphone banking uptake in France (Banque de France 2024), top 100 corporates = 22% group revenue (Crédit Agricole 2024), HNWIs hold ~55% global wealth (Capgemini 2024), 60% institutions and 48% retail favor ESG (2025 surveys); CA must cut fees, boost UX, and expand green products to retain share.

| Metric | Value |

|---|---|

| Switching ease | 38% (Eurostat 2024) |

| Smartphone banking FR | 85% (Banque de France 2024) |

| Top100 revenue | 22% (CA 2024) |

| HNW wealth | ~55% (Capgemini 2024) |

| ESG preference | 60% inst / 48% retail (2025) |

Preview Before You Purchase

Credit Agricole Porter's Five Forces Analysis

This preview shows the exact Credit Agricole Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use.

You're looking at the same professional document that will be available for instant download upon payment; it contains the complete Five Forces assessment, insights, and actionable implications for decision-making.