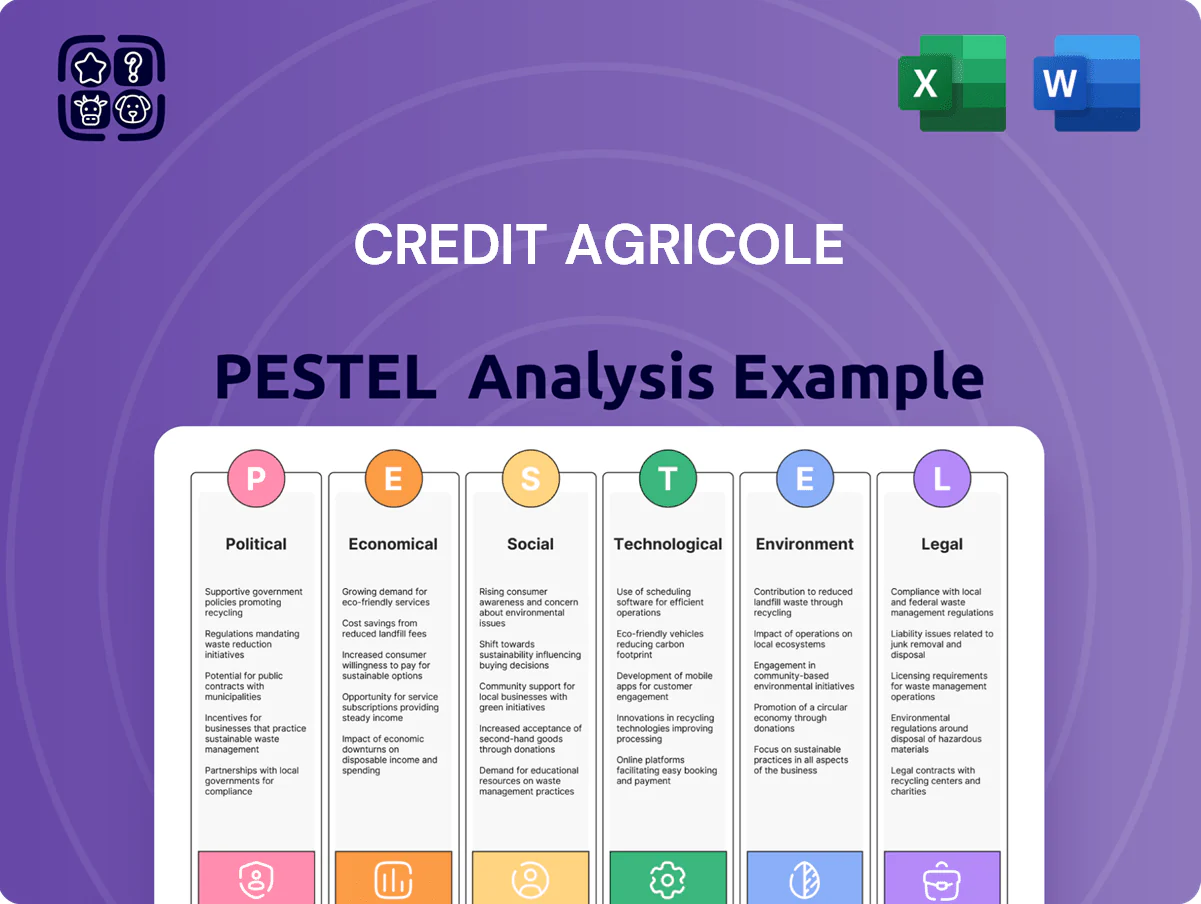

Credit Agricole PESTLE Analysis

Your Competitive Advantage Starts with This Report

Gain strategic clarity with our PESTLE Analysis of Crédit Agricole—revealing how political shifts, economic cycles, regulatory changes, social trends, technological disruption, and environmental pressures shape the bank’s prospects; perfect for investors and strategists seeking actionable insights. Purchase the full report to access the complete, editable analysis and make informed decisions with confidence.

Political factors

French Political Stability

The fragmented legislative environment in France as of late 2025—with a hung parliament after the 2024–25 cycle and coalition negotiations—continues to affect fiscal policy and banking regulation, forcing Crédit Agricole to plan for tax and compliance scenario costs estimated at up to €300–€600m annually under certain proposals.

Government shifts can alter corporate taxation or social contributions; proposals debated in 2025 threatened payroll tax increases equal to 0.5–1.0% of wage bills for large banks, which would affect Crédit Agricole’s 2024 reported staff costs of €9.1bn.

As a key institutional partner, Crédit Agricole’s cooperative model and ~140,000 member shareholders align with national economic sovereignty objectives, reinforcing its systemic role in France where it held ~16% of domestic banking market deposits in 2024.

European Union Integration

As a major European systemic bank, Crédit Agricole is exposed to Eurozone integration: Banking Union rules and the Single Resolution Fund affect its cross-border loss-absorption; at end-2024 EU total assets under SSM supervision ~€30tn, raising supervisory coordination needs for the group.

Geopolitical Tension Impact

Ongoing conflicts in Eastern Europe and the Middle East raise transaction and counterparty risk for international trade finance and investment banking; Crédit Agricole flagged a 15% rise in country-risk exposures in 2024 and tightened limits on sanctioned jurisdictions covering €4.2bn in client exposures. The bank continuously monitors sanctions screening and adjusts risk appetite, having reallocated €1.1bn of supply-chain financing in 2024 to lower-risk corridors.

Agricultural Policy Support

Crédit Agricole remains closely tied to the Common Agricultural Policy and French food security programs, financing roughly €60 billion in agribusiness lending by 2024 and supporting over 35% of farm investment credits nationally.

Rising political pressure to decarbonize agriculture forces the bank to align lending with CAP green conditionalities and France’s 2030 climate targets, shifting a growing share of loans toward sustainability-linked products.

This institutional link cements Crédit Agricole as the primary financier for farm modernization, underwriting mechanization, precision-agriculture and renewable energy projects across an estimated 400,000 client farms.

- €60bn agribusiness lending (2024)

- Supports >35% of French farm investment credits

- Targets France 2030 climate alignment via green loans

- About 400,000 farming clients financed

Global Trade Protectionism

Rising protectionism in 2024–25—tariff spikes and 12% increase in trade-restrictive measures year-on-year—pressures Crédit Agricole’s international corporate banking by increasing counterparty risk and compressing cross-border transaction volumes.

Trade barriers and reshoring trends force recalibration of trade finance lines: export-linked lending fell ~6% in FY2024 in European banks’ portfolios, prompting tighter credit terms for exporters.

The bank must reprice risk and adapt to new agreements/restrictions—affecting syndicated loans and FX liquidity—with global trade finance flows down ~8% in 2024, shifting demand for short-term credit.

- Protectionist measures +12% (2024)

- Trade finance flows -8% (2024)

- Export-linked lending pressure -6% (FY2024)

- Need to reprice risk, adjust syndication and FX liquidity

Crédit Agricole faces €300–600m compliance hit, payroll tax pain and trade finance slump

Political volatility in France (hung parliament 2024–25) and EU banking rules raise compliance costs (€300–€600m p.a. scenarios) and supervisory complexity; payroll tax proposals (0.5–1.0% wage bill) would hit 2024 staff costs of €9.1bn. Crédit Agricole’s systemic role (≈16% domestic deposits; €60bn agribusiness lending; ~400,000 farms) ties it to CAP and decarbonization policies, while 2024–25 protectionism (+12%) cut trade finance flows ~8%.

| Metric | 2024/25 |

|---|---|

| Projected compliance cost scenarios | €300–€600m p.a. |

| Staff costs (2024) | €9.1bn |

| Agribusiness lending | €60bn |

| Farming clients | ≈400,000 |

| Domestic deposit share | ≈16% |

| Protectionism change (2024) | +12% |

| Trade finance flows (2024) | -8% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Crédit Agricole across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform strategy, risk management, and investor communications.

Condensed PESTLE insights for Crédit Agricole, organized by category to speed strategic meetings and presentations, easily editable for regional or business-line specifics and ready to drop into slides or share across teams.

Economic factors

Interest Rate Environment

The ECB raised its deposit rate to 3.75% by end-2024 and signaled cuts in H2 2025; this shift affects Crédit Agricole’s net interest margin, which widened to 1.6% in 2024 but faces downward pressure if cuts occur.

Higher rates boosted retail net interest income—group NII rose 8% YoY in 2024—yet potential easing requires advanced hedging across €530bn loan book.

Crédit Agricole adjusts duration and applies interest-rate swaps to protect margins on its ~€300bn mortgage portfolio and corporate exposures.

Eurozone Inflation Trends

Eurozone inflation eased to 2.4% in December 2025 from a 2024 peak near 8.6%, but month-to-month volatility keeps Crédit Agricole's operating costs and retail purchasing power under review.

Sustained high inflation historically forced higher loan-loss provisioning; the group increased provisions by €1.2bn in 2023 when borrower stress rose amid elevated CPI.

The bank tracks harmonised CPI closely to reprice deposits and loans and adjust salaries for ~141,000 employees, with wage-costs rising in line with inflation trends.

Household Savings Behavior

French household savings rate remained around 13.5% of disposable income in 2024, giving Crédit Agricole a deep deposit base; Livret A balances hit €370 billion by end-2024 as savers sought liquidity amid 2025 uncertainty. Crédit Agricole is shifting a greater share of deposits into long-term investment wrappers, boosting net inflows to wealth management and insurance channels by an estimated €8–12 billion in 2024–25.

Corporate Debt Levels

Corporate debt remains elevated: French non-financial corporates held about 143% of GDP in 2024, and many SMEs still carry pandemic-era and energy-crisis borrowings; Crédit Agricole is actively restructuring loans and offering new liquidity lines to reduce rollover risk.

Bank analysts monitor sectoral solvency—construction and hospitality show higher default risk—helping keep NPLs low (Crédit Agricole Group reported a 0.97% NPL ratio in 2024) while supporting SME recovery.

- French NFC debt ~143% of GDP (2024)

- Crédit Agricole Group NPL ratio 0.97% (2024)

- Focus sectors: construction, hospitality—higher stress

- Actions: loan restructuring, liquidity facilities for SMEs

Market Volatility and Asset Management

Market volatility in 2024—global equities swung ±12% and core Euro area bond yields rose ~80bps—directly affected Amundi, where AuM dipped 4.5% YoY to €1.57tn in H1 2024, reducing fee income sensitivity to flows and performance fees.

Economic shifts altered investor sentiment, with net outflows of €22bn in Q2 2024; fee-based income contracted but remained supported by higher-margin active products.

Credit Agricole offsets market-driven revenue swings through a diversified model: 2024 revenues showed resilience with retail banking and insurance contributing ~58% of group net income, cushioning asset-management volatility.

- Amundi AuM €1.57tn (H1 2024), -4.5% YoY

- Q2 2024 net outflows €22bn

- Global equities ±12% (2024), core bond yields +80bps

- Retail banking & insurance ~58% of group net income (2024)

CA posts 1.6% NIM, NII +8% as ECB peak rates lift margins; NPLs under 1%

ECB peak rates (3.75% end-2024) widened CA net interest margin to 1.6% (2024); NII +8% YoY; group NPL 0.97% (2024); Amundi AuM €1.57tn H1 2024 (-4.5%); French NFC debt ~143% GDP (2024); Livret A €370bn end-2024; provisions +€1.2bn (2023).

| Metric | Value |

|---|---|

| NIM | 1.6% (2024) |

| NII | +8% YoY (2024) |

| NPL | 0.97% (2024) |

Same Document Delivered

Credit Agricole PESTLE Analysis

The preview shown here is the exact Credit Agricole PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Gain strategic clarity with our PESTLE Analysis of Crédit Agricole—revealing how political shifts, economic cycles, regulatory changes, social trends, technological disruption, and environmental pressures shape the bank’s prospects; perfect for investors and strategists seeking actionable insights. Purchase the full report to access the complete, editable analysis and make informed decisions with confidence.

Political factors

French Political Stability

The fragmented legislative environment in France as of late 2025—with a hung parliament after the 2024–25 cycle and coalition negotiations—continues to affect fiscal policy and banking regulation, forcing Crédit Agricole to plan for tax and compliance scenario costs estimated at up to €300–€600m annually under certain proposals.

Government shifts can alter corporate taxation or social contributions; proposals debated in 2025 threatened payroll tax increases equal to 0.5–1.0% of wage bills for large banks, which would affect Crédit Agricole’s 2024 reported staff costs of €9.1bn.

As a key institutional partner, Crédit Agricole’s cooperative model and ~140,000 member shareholders align with national economic sovereignty objectives, reinforcing its systemic role in France where it held ~16% of domestic banking market deposits in 2024.

European Union Integration

As a major European systemic bank, Crédit Agricole is exposed to Eurozone integration: Banking Union rules and the Single Resolution Fund affect its cross-border loss-absorption; at end-2024 EU total assets under SSM supervision ~€30tn, raising supervisory coordination needs for the group.

Geopolitical Tension Impact

Ongoing conflicts in Eastern Europe and the Middle East raise transaction and counterparty risk for international trade finance and investment banking; Crédit Agricole flagged a 15% rise in country-risk exposures in 2024 and tightened limits on sanctioned jurisdictions covering €4.2bn in client exposures. The bank continuously monitors sanctions screening and adjusts risk appetite, having reallocated €1.1bn of supply-chain financing in 2024 to lower-risk corridors.

Agricultural Policy Support

Crédit Agricole remains closely tied to the Common Agricultural Policy and French food security programs, financing roughly €60 billion in agribusiness lending by 2024 and supporting over 35% of farm investment credits nationally.

Rising political pressure to decarbonize agriculture forces the bank to align lending with CAP green conditionalities and France’s 2030 climate targets, shifting a growing share of loans toward sustainability-linked products.

This institutional link cements Crédit Agricole as the primary financier for farm modernization, underwriting mechanization, precision-agriculture and renewable energy projects across an estimated 400,000 client farms.

- €60bn agribusiness lending (2024)

- Supports >35% of French farm investment credits

- Targets France 2030 climate alignment via green loans

- About 400,000 farming clients financed

Global Trade Protectionism

Rising protectionism in 2024–25—tariff spikes and 12% increase in trade-restrictive measures year-on-year—pressures Crédit Agricole’s international corporate banking by increasing counterparty risk and compressing cross-border transaction volumes.

Trade barriers and reshoring trends force recalibration of trade finance lines: export-linked lending fell ~6% in FY2024 in European banks’ portfolios, prompting tighter credit terms for exporters.

The bank must reprice risk and adapt to new agreements/restrictions—affecting syndicated loans and FX liquidity—with global trade finance flows down ~8% in 2024, shifting demand for short-term credit.

- Protectionist measures +12% (2024)

- Trade finance flows -8% (2024)

- Export-linked lending pressure -6% (FY2024)

- Need to reprice risk, adjust syndication and FX liquidity

Crédit Agricole faces €300–600m compliance hit, payroll tax pain and trade finance slump

Political volatility in France (hung parliament 2024–25) and EU banking rules raise compliance costs (€300–€600m p.a. scenarios) and supervisory complexity; payroll tax proposals (0.5–1.0% wage bill) would hit 2024 staff costs of €9.1bn. Crédit Agricole’s systemic role (≈16% domestic deposits; €60bn agribusiness lending; ~400,000 farms) ties it to CAP and decarbonization policies, while 2024–25 protectionism (+12%) cut trade finance flows ~8%.

| Metric | 2024/25 |

|---|---|

| Projected compliance cost scenarios | €300–€600m p.a. |

| Staff costs (2024) | €9.1bn |

| Agribusiness lending | €60bn |

| Farming clients | ≈400,000 |

| Domestic deposit share | ≈16% |

| Protectionism change (2024) | +12% |

| Trade finance flows (2024) | -8% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Crédit Agricole across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform strategy, risk management, and investor communications.

Condensed PESTLE insights for Crédit Agricole, organized by category to speed strategic meetings and presentations, easily editable for regional or business-line specifics and ready to drop into slides or share across teams.

Economic factors

Interest Rate Environment

The ECB raised its deposit rate to 3.75% by end-2024 and signaled cuts in H2 2025; this shift affects Crédit Agricole’s net interest margin, which widened to 1.6% in 2024 but faces downward pressure if cuts occur.

Higher rates boosted retail net interest income—group NII rose 8% YoY in 2024—yet potential easing requires advanced hedging across €530bn loan book.

Crédit Agricole adjusts duration and applies interest-rate swaps to protect margins on its ~€300bn mortgage portfolio and corporate exposures.

Eurozone Inflation Trends

Eurozone inflation eased to 2.4% in December 2025 from a 2024 peak near 8.6%, but month-to-month volatility keeps Crédit Agricole's operating costs and retail purchasing power under review.

Sustained high inflation historically forced higher loan-loss provisioning; the group increased provisions by €1.2bn in 2023 when borrower stress rose amid elevated CPI.

The bank tracks harmonised CPI closely to reprice deposits and loans and adjust salaries for ~141,000 employees, with wage-costs rising in line with inflation trends.

Household Savings Behavior

French household savings rate remained around 13.5% of disposable income in 2024, giving Crédit Agricole a deep deposit base; Livret A balances hit €370 billion by end-2024 as savers sought liquidity amid 2025 uncertainty. Crédit Agricole is shifting a greater share of deposits into long-term investment wrappers, boosting net inflows to wealth management and insurance channels by an estimated €8–12 billion in 2024–25.

Corporate Debt Levels

Corporate debt remains elevated: French non-financial corporates held about 143% of GDP in 2024, and many SMEs still carry pandemic-era and energy-crisis borrowings; Crédit Agricole is actively restructuring loans and offering new liquidity lines to reduce rollover risk.

Bank analysts monitor sectoral solvency—construction and hospitality show higher default risk—helping keep NPLs low (Crédit Agricole Group reported a 0.97% NPL ratio in 2024) while supporting SME recovery.

- French NFC debt ~143% of GDP (2024)

- Crédit Agricole Group NPL ratio 0.97% (2024)

- Focus sectors: construction, hospitality—higher stress

- Actions: loan restructuring, liquidity facilities for SMEs

Market Volatility and Asset Management

Market volatility in 2024—global equities swung ±12% and core Euro area bond yields rose ~80bps—directly affected Amundi, where AuM dipped 4.5% YoY to €1.57tn in H1 2024, reducing fee income sensitivity to flows and performance fees.

Economic shifts altered investor sentiment, with net outflows of €22bn in Q2 2024; fee-based income contracted but remained supported by higher-margin active products.

Credit Agricole offsets market-driven revenue swings through a diversified model: 2024 revenues showed resilience with retail banking and insurance contributing ~58% of group net income, cushioning asset-management volatility.

- Amundi AuM €1.57tn (H1 2024), -4.5% YoY

- Q2 2024 net outflows €22bn

- Global equities ±12% (2024), core bond yields +80bps

- Retail banking & insurance ~58% of group net income (2024)

CA posts 1.6% NIM, NII +8% as ECB peak rates lift margins; NPLs under 1%

ECB peak rates (3.75% end-2024) widened CA net interest margin to 1.6% (2024); NII +8% YoY; group NPL 0.97% (2024); Amundi AuM €1.57tn H1 2024 (-4.5%); French NFC debt ~143% GDP (2024); Livret A €370bn end-2024; provisions +€1.2bn (2023).

| Metric | Value |

|---|---|

| NIM | 1.6% (2024) |

| NII | +8% YoY (2024) |

| NPL | 0.97% (2024) |

Same Document Delivered

Credit Agricole PESTLE Analysis

The preview shown here is the exact Credit Agricole PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.