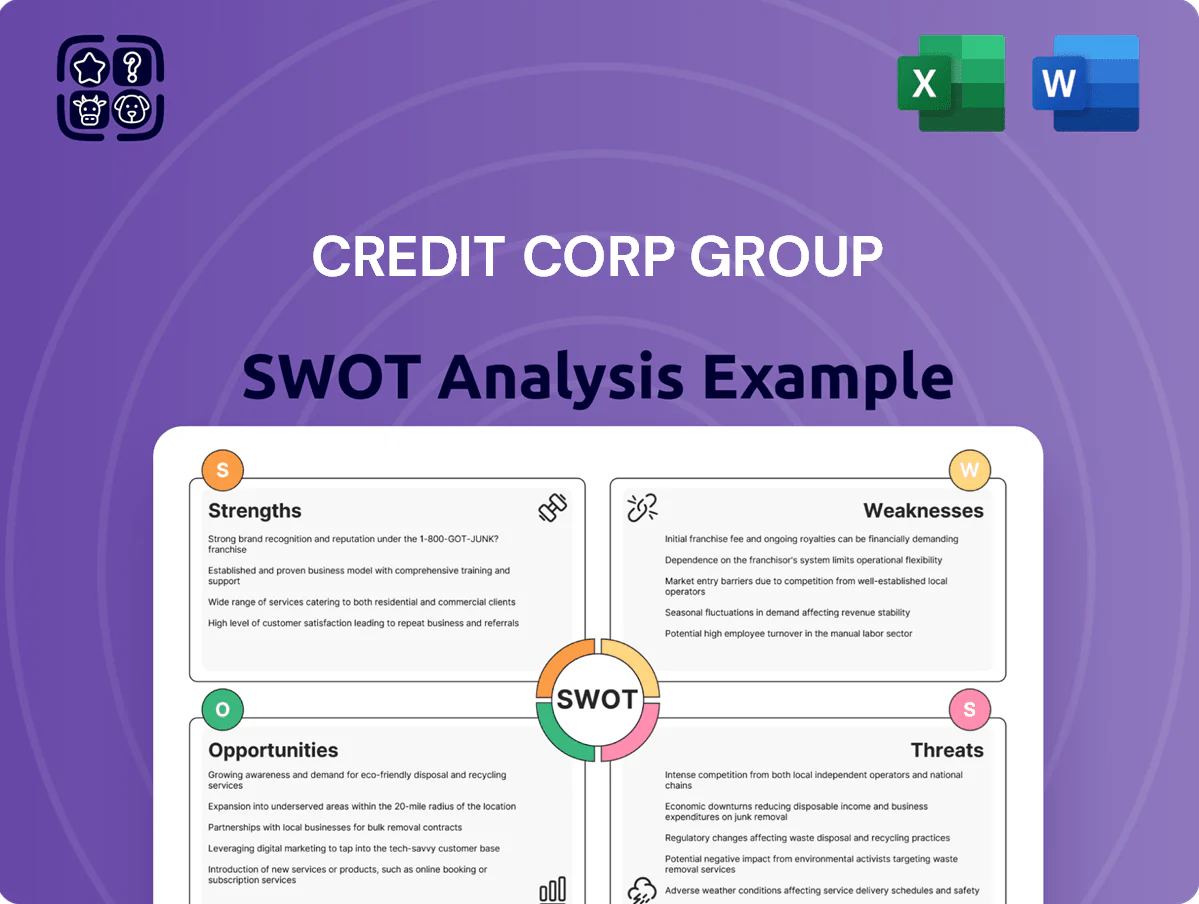

Credit Corp Group SWOT Analysis

Your Strategic Toolkit Starts Here

Credit Corp Group shows resilient receivables management and expanding regional footprint, yet faces regulatory sensitivity and credit-cycle exposure; our full SWOT unpacks these dynamics with financial context and strategic recommendations. Purchase the complete SWOT analysis to access a professionally written, editable report and Excel matrix—ideal for investors, advisors, and strategists seeking actionable, presentation-ready insights.

Strengths

Dominant Market Position in AU/NZ

Credit Corp remains the preeminent debt purchaser in Australia and New Zealand as of late 2025, holding roughly 35–40% market share by volume in AU consumer unsecured portfolios and ~30% in NZ, according to industry filings.

This scale gives Credit Corp superior access to portfolios from the big four banks and major BNPL providers, outbidding smaller rivals that lack comparable capital.

The firm leverages a 20+ year reputation to secure long-term forward-flow agreements—over A$800m committed inventory for FY2026—ensuring steady asset supply.

Data-Driven Pricing Capabilities

Credit Corp Group uses a proprietary database of over 10 million Australian consumer records to price debt portfolios, cutting overpayment risk by an estimated 12% versus sector averages and lifting average recovery rates to ~38% in FY2024; by end-2025 its predictive models added advanced machine learning, improving collection efficiency an estimated 8–10% and shortening days‑to‑collect by ~14 days.

Robust Balance Sheet Management

Credit Corp Group keeps low net debt-to-equity (about 0.15x at FY2025) and generated AUD 210m operating cash flow in FY2025, giving it stronger liquidity than most peers. This conservative balance sheet lets Credit Corp bid competitively for large portfolios despite higher rates, since it can self-fund ~30–40% of acquisitions and avoid volatile capital markets. That lowers funding cost and financial risk when scaling purchases.

Diversified Business Model

- Wallet Wizard: counter‑cyclical revenue

- Reused credit models → lower costs

- ROE ~18% (2025)

- ~22% of group revenue (2025)

- EBITDA margin +120 bps (FY2024–25)

Scalable US Operations

- US receivables under management: ~US$420m (FY2024)

- US share of group cash collections: ~45% (2024)

- Cost-to-collect: ~18–20%

Credit Corp: Dominant AU/NZ debt buyer with strong cash flow, ML‑lifted recoveries

Credit Corp dominates AU/NZ debt purchasing (35–40% AU, ~30% NZ), holds A$800m+ forward-flow FY2026, and had AUD210m operating cash flow with net debt/equity ~0.15x (FY2025); proprietary 10m-record database and ML raised recovery to ~38% (FY2024) and cut collection time ~14 days; Wallet Wizard drove ROE ~18% and 22% of revenue (2025); US RUM ~US$420m (FY2024), cost-to-collect 18–20%.

| Metric | Value |

|---|---|

| AU market share | 35–40% |

| NZ market share | ~30% |

| Forward flow | A$800m+ |

| Op cash flow FY2025 | AUD210m |

| Net D/E FY2025 | ~0.15x |

| Recovery rate FY2024 | ~38% |

| Wallet Wizard revenue | 22% (2025) |

| US RUM FY2024 | US$420m |

| Cost-to-collect | 18–20% |

What is included in the product

Provides a concise SWOT overview of Credit Corp Group, outlining its core strengths, operational weaknesses, market opportunities, and external threats to assess strategic positioning and future growth prospects.

Delivers a concise SWOT matrix for Credit Corp Group to speed executive alignment and decision-making with a clear, visual summary of strengths, weaknesses, opportunities, and threats.

Weaknesses

High Compliance and Regulatory Overhead

The debt-collection sector faces heavy oversight from ASIC and the ACCC, forcing Credit Corp Group to spend roughly A$18–25m annually on compliance systems and training (company filings, FY2024–2025).

Any breach of strict collection rules can trigger fines (up to A$2m+ per contravention) and severed bank partnerships, harming funding lines and revenue streams.

These regulatory overheads compress net margins—Credit Corp’s FY2025 net margin fell to about 11.2%—and are likely to tighten further into 2026.

Dependence on Credit Provider Relationships

The business depends on banks and credit providers selling distressed ledgers instead of handling recoveries internally; in 2024 roughly 60% of Credit Corp Group’s Australian purchases came from the Big Four, exposing concentration risk.

If major lenders shift to in‑house recovery or change disposal strategies, Credit Corp could face a sharp supply crunch—management noted in FY2024 filings that purchased debt volumes fell 12% year‑on‑year when one large seller paused sales.

US Segment Performance Volatility

The US segment shows higher collection volatility versus AU/NZ: 2024 US recovery rates fell to ~18% of book vs 26% in AU/NZ, and quarterly EBITDA margin swung 9–16% in 2023–24. State-level rules (e.g., CA, TX) and varied consumer profiles raise compliance and model risk, increasing operating costs by an estimated 12–15% versus ANZ. Management notes consistent profitability across all US territories remains a work in progress into FY2025.

Sensitivity to Cost of Funding

As a capital‑intensive buyer of distressed debt, Credit Corp Group is highly exposed to higher borrowing costs; its drawn corporate debt was about A$550m at end‑2025, so a 100bp rise in funding spreads can cut IRR on new portfolios by ~1–2 percentage points.

Managing interest‑rate risk through hedges and shorter‑tenor facilities is critical to protect margins and ensure recoveries exceed purchase prices in 2026.

- A$550m drawn debt (FY2025)

- 100bp rise ≈ 1–2pp IRR hit

- Hedge or shorten tenor to protect spreads

Labor Intensive Operational Structure

- 45% of staff tied to collections

- ~32% turnover in 2024

- Recruit/training costs erode EBITDA

- 5–7% productivity dips cut 1–2pp margin

High compliance costs, concentrated supply & debt risk compress margins and IRR

Heavy regulation and compliance costs (A$18–25m p.a.) plus fines (A$2m+ per breach) squeeze margins (FY2025 net margin ~11.2%) and risk bank partner loss; 60% AU purchases from Big Four create supply concentration; US recovery volatility (2024: US 18% vs AU/NZ 26%) and A$550m drawn debt expose IRR to 100bp ≈1–2pp hit; 45% staff in collections and ~32% turnover limit margin upside.

| Metric | Value |

|---|---|

| Compliance spend | A$18–25m |

| FY2025 net margin | 11.2% |

| AU purchases from Big Four | 60% |

| US vs AU/NZ recovery | 18% vs 26% |

| Drawn debt (end‑2025) | A$550m |

| Turnover (2024) | ~32% |

Preview Before You Purchase

Credit Corp Group SWOT Analysis

This is the actual Credit Corp Group SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality and fully editable for your use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

Credit Corp Group shows resilient receivables management and expanding regional footprint, yet faces regulatory sensitivity and credit-cycle exposure; our full SWOT unpacks these dynamics with financial context and strategic recommendations. Purchase the complete SWOT analysis to access a professionally written, editable report and Excel matrix—ideal for investors, advisors, and strategists seeking actionable, presentation-ready insights.

Strengths

Dominant Market Position in AU/NZ

Credit Corp remains the preeminent debt purchaser in Australia and New Zealand as of late 2025, holding roughly 35–40% market share by volume in AU consumer unsecured portfolios and ~30% in NZ, according to industry filings.

This scale gives Credit Corp superior access to portfolios from the big four banks and major BNPL providers, outbidding smaller rivals that lack comparable capital.

The firm leverages a 20+ year reputation to secure long-term forward-flow agreements—over A$800m committed inventory for FY2026—ensuring steady asset supply.

Data-Driven Pricing Capabilities

Credit Corp Group uses a proprietary database of over 10 million Australian consumer records to price debt portfolios, cutting overpayment risk by an estimated 12% versus sector averages and lifting average recovery rates to ~38% in FY2024; by end-2025 its predictive models added advanced machine learning, improving collection efficiency an estimated 8–10% and shortening days‑to‑collect by ~14 days.

Robust Balance Sheet Management

Credit Corp Group keeps low net debt-to-equity (about 0.15x at FY2025) and generated AUD 210m operating cash flow in FY2025, giving it stronger liquidity than most peers. This conservative balance sheet lets Credit Corp bid competitively for large portfolios despite higher rates, since it can self-fund ~30–40% of acquisitions and avoid volatile capital markets. That lowers funding cost and financial risk when scaling purchases.

Diversified Business Model

- Wallet Wizard: counter‑cyclical revenue

- Reused credit models → lower costs

- ROE ~18% (2025)

- ~22% of group revenue (2025)

- EBITDA margin +120 bps (FY2024–25)

Scalable US Operations

- US receivables under management: ~US$420m (FY2024)

- US share of group cash collections: ~45% (2024)

- Cost-to-collect: ~18–20%

Credit Corp: Dominant AU/NZ debt buyer with strong cash flow, ML‑lifted recoveries

Credit Corp dominates AU/NZ debt purchasing (35–40% AU, ~30% NZ), holds A$800m+ forward-flow FY2026, and had AUD210m operating cash flow with net debt/equity ~0.15x (FY2025); proprietary 10m-record database and ML raised recovery to ~38% (FY2024) and cut collection time ~14 days; Wallet Wizard drove ROE ~18% and 22% of revenue (2025); US RUM ~US$420m (FY2024), cost-to-collect 18–20%.

| Metric | Value |

|---|---|

| AU market share | 35–40% |

| NZ market share | ~30% |

| Forward flow | A$800m+ |

| Op cash flow FY2025 | AUD210m |

| Net D/E FY2025 | ~0.15x |

| Recovery rate FY2024 | ~38% |

| Wallet Wizard revenue | 22% (2025) |

| US RUM FY2024 | US$420m |

| Cost-to-collect | 18–20% |

What is included in the product

Provides a concise SWOT overview of Credit Corp Group, outlining its core strengths, operational weaknesses, market opportunities, and external threats to assess strategic positioning and future growth prospects.

Delivers a concise SWOT matrix for Credit Corp Group to speed executive alignment and decision-making with a clear, visual summary of strengths, weaknesses, opportunities, and threats.

Weaknesses

High Compliance and Regulatory Overhead

The debt-collection sector faces heavy oversight from ASIC and the ACCC, forcing Credit Corp Group to spend roughly A$18–25m annually on compliance systems and training (company filings, FY2024–2025).

Any breach of strict collection rules can trigger fines (up to A$2m+ per contravention) and severed bank partnerships, harming funding lines and revenue streams.

These regulatory overheads compress net margins—Credit Corp’s FY2025 net margin fell to about 11.2%—and are likely to tighten further into 2026.

Dependence on Credit Provider Relationships

The business depends on banks and credit providers selling distressed ledgers instead of handling recoveries internally; in 2024 roughly 60% of Credit Corp Group’s Australian purchases came from the Big Four, exposing concentration risk.

If major lenders shift to in‑house recovery or change disposal strategies, Credit Corp could face a sharp supply crunch—management noted in FY2024 filings that purchased debt volumes fell 12% year‑on‑year when one large seller paused sales.

US Segment Performance Volatility

The US segment shows higher collection volatility versus AU/NZ: 2024 US recovery rates fell to ~18% of book vs 26% in AU/NZ, and quarterly EBITDA margin swung 9–16% in 2023–24. State-level rules (e.g., CA, TX) and varied consumer profiles raise compliance and model risk, increasing operating costs by an estimated 12–15% versus ANZ. Management notes consistent profitability across all US territories remains a work in progress into FY2025.

Sensitivity to Cost of Funding

As a capital‑intensive buyer of distressed debt, Credit Corp Group is highly exposed to higher borrowing costs; its drawn corporate debt was about A$550m at end‑2025, so a 100bp rise in funding spreads can cut IRR on new portfolios by ~1–2 percentage points.

Managing interest‑rate risk through hedges and shorter‑tenor facilities is critical to protect margins and ensure recoveries exceed purchase prices in 2026.

- A$550m drawn debt (FY2025)

- 100bp rise ≈ 1–2pp IRR hit

- Hedge or shorten tenor to protect spreads

Labor Intensive Operational Structure

- 45% of staff tied to collections

- ~32% turnover in 2024

- Recruit/training costs erode EBITDA

- 5–7% productivity dips cut 1–2pp margin

High compliance costs, concentrated supply & debt risk compress margins and IRR

Heavy regulation and compliance costs (A$18–25m p.a.) plus fines (A$2m+ per breach) squeeze margins (FY2025 net margin ~11.2%) and risk bank partner loss; 60% AU purchases from Big Four create supply concentration; US recovery volatility (2024: US 18% vs AU/NZ 26%) and A$550m drawn debt expose IRR to 100bp ≈1–2pp hit; 45% staff in collections and ~32% turnover limit margin upside.

| Metric | Value |

|---|---|

| Compliance spend | A$18–25m |

| FY2025 net margin | 11.2% |

| AU purchases from Big Four | 60% |

| US vs AU/NZ recovery | 18% vs 26% |

| Drawn debt (end‑2025) | A$550m |

| Turnover (2024) | ~32% |

Preview Before You Purchase

Credit Corp Group SWOT Analysis

This is the actual Credit Corp Group SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality and fully editable for your use.