Criteo Porter's Five Forces Analysis

Don't Miss the Bigger Picture

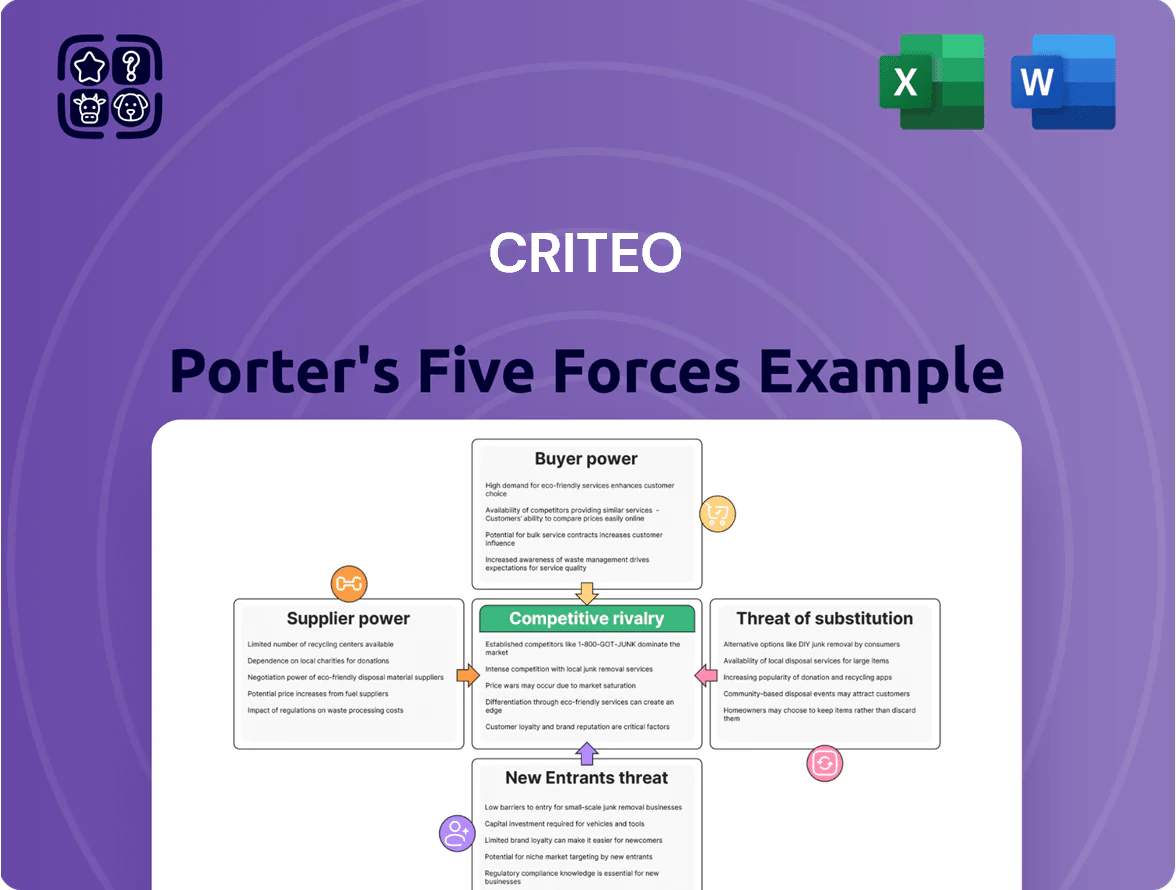

Criteo faces intense rivalry from major adtech platforms and rising programmatic entrants, moderate buyer power as advertisers demand ROI, and supplier leverage from data providers and publishers—while regulatory shifts and ad-blocking heighten substitute and threat risks.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Criteo’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Access to Premium Publisher Inventory

Criteo depends on thousands of publishers and SSPs for inventory, making them essential suppliers; in 2024 publishers delivered a large share of Criteo’s $1.6B ad-serving base. Premium publishers—top-tier sites that drive higher conversion rates—wield pricing and placement power, often commanding CPMs 2–4x market average. As the open internet shifts to curated, high-conversion slots, competition raises Criteo’s acquisition costs and squeezes margins.

Dependence on Cloud Infrastructure Providers

Criteo relies heavily on AWS and Google Cloud for AI/ML workloads, giving these providers strong bargaining power because their specialized infrastructure is costly to replicate and migrate; IDC estimated cloud migration costs average 200–400 USD per TB in 2024, so shifting Criteo’s petabytes would be material. Any price hike or SLA change by AWS/Google can squeeze Criteo’s 2024 adjusted EBIT margin (11.2%) and raise unit economics for programmatic ads.

Reliance on Web Browser and OS Policies

Suppliers of the technical environment, notably Google (Chrome) and Apple (iOS), set tracking and identity rules that directly shape Criteo’s ad tech; Google ended third-party cookie support in Chrome in 2024 and Apple’s App Tracking Transparency (launched 2021) persists, reducing addressable IDs by an estimated 30–40% for many ad platforms. Criteo must continually adapt its Commerce Media Platform to these gatekeepers’ privacy frameworks and SDK/API limits, which can materially cut targeting revenue and raise compliance costs.

Availability of Specialized AI Talent

The market for machine learning engineers and data scientists is highly competitive, making human capital a powerful supplier group; US median salary for ML engineers reached about $155,000 in 2024, and demand grew ~35% YoY in job postings. Criteo needs top-tier talent to keep its predictive bidding and recommendation edge, so wage pressure and richer benefits raise R&D and SG&A costs and tighten hiring timelines.

- ML engineer median pay $155k (US, 2024)

- Job postings +35% YoY (2023–24)

- Talent shortages increase R&D spend and hiring lag

- Employee leverage raises compensation and retention costs

Integration with Data Management Partners

Suppliers of third-party data and identity resolution remain crucial as Criteo shifts to first-party data; in 2024 Criteo reported first-party data now covers roughly 60% of signal needs but external providers still supply key enrichment and cross-device matching.

The consolidation of identity vendors post-cookie—top five providers controlling over 70% of market revenue in 2024—gives remaining leaders pricing power and raises switching costs for Criteo.

- First-party covers ~60% of signals (Criteo 2024)

- Top 5 identity vendors >70% market share (2024)

- Consolidation increases supplier leverage and switching cost

Criteo squeezed: publishers, cloud costs, talent, and identity vendors tighten margins

Criteo faces strong supplier power: publishers/SSPs drove a large share of its $1.6B 2024 revenue, premium publishers command 2–4x CPMs, AWS/Google cloud migration costs ~200–400 USD/TB raise switching costs, ML engineer median pay $155k (US, 2024) tightens hiring, and top‑5 identity vendors >70% market share; first‑party signals cover ~60% of needs (Criteo 2024).

| Metric | 2024 value |

|---|---|

| Revenue tied to publishers | $1.6B |

| Premium CPM premium | 2–4x |

| Cloud migration cost | $200–400/GB |

| ML median pay (US) | $155k |

| First‑party signal coverage | ~60% |

| Top5 identity market share | >70% |

What is included in the product

Tailored exclusively for Criteo, this Porter's Five Forces overview uncovers competitive intensity, buyer/supplier power, threat of new entrants and substitutes, and highlights disruptive trends and market entry risks shaping Criteo’s pricing power and profitability.

A concise Porter's Five Forces one-sheet for Criteo—instantly highlights competitive pressures and strategic levers to streamline boardroom decisions and investor briefings.

Customers Bargaining Power

Concentration of Large Retail Media Clients

Major retailers and global brands accounted for roughly 40% of Criteo's 2024 revenue (~€600m of €1.5bn), giving them strong negotiating leverage to demand lower prices, bespoke features, and tighter ecosystem integration.

Large clients can push for service-level concessions and data access; losing a top-5 retail partner would likely cut revenue by 5–10% and dent market share given Criteo’s concentrated client mix.

Demand for Transparent ROI and Attribution

Customers now demand clear ROI and attribution; 2024 surveys show 68% of e‑commerce advertisers require granular multi-touch attribution to justify ad spend, raising bargaining power.

That pressure forces Criteo to update reporting and attribution; Criteo reported product R&D spend of €169M in 2024 to improve measurement and machine‑learning models.

Easy cross‑platform comparisons—industry median ROAS (return on ad spend) variance ±12% across DSPs in 2024—makes switching cheaper if Criteo underperforms, increasing customer leverage.

Adoption of Multi-Platform Strategies

Many advertisers use multi-DSP (demand-side platform) mixes to avoid vendor lock-in and boost reach; industry surveys in 2024 show 68% of agencies run 3+ DSPs, cutting Criteo’s budget control.

Daily performance-based reallocations mean clients can shift spend within 24 hours; Criteo’s share of wallet fell to ~6–8% in programmatic retail ad segments in 2024, reflecting this churn.

Low switching friction forces Criteo to keep CPMs, ROAS, and reporting highly competitive; otherwise brands reallocate quickly, raising customer bargaining power.

Shift Toward In-House AdTech Capabilities

Agency Influence on Budget Allocation

Advertising agencies, which control roughly 30–40% of global digital ad budgets per WFA 2024 estimates, concentrate spend with preferred partners and can reallocate large volumes away from Criteo if platform UX or incentives falter.

Agencies can shift deals representing tens of millions in annual revenue; Criteo must prioritize agency-friendly tools, transparent fees, and bespoke incentives to retain steady allocations.

Strong, ongoing relationships with agency decision-makers reduce churn risk and support multi-year commitments—losing top agency accounts can cut programmatic revenue materially.

- Agencies control ~30–40% of digital budgets (WFA 2024)

- Shifts can represent tens of millions in revenue

- Focus: UX, transparent fees, tailored incentives

- Priority: sustained agency relationship management

Criteo: Top clients hold the cards—40% revenue concentration boosts buyer leverage

Major retailers and global brands drove ~40% of Criteo’s 2024 revenue (~€600M of €1.5B), giving them strong leverage to demand price cuts, bespoke features, and data access; losing a top-5 partner could cut revenue 5–10%.

68% of e‑commerce advertisers required granular multi‑touch attribution in 2024, 68% of agencies run 3+ DSPs, and Criteo’s programmatic retail share fell to ~6–8%, all raising customer bargaining power.

| Metric | 2024 Value |

|---|---|

| Revenue concentration (top clients) | ~40% (€600M) |

| R&D spend | €169M |

| Agencies using 3+ DSPs | 68% |

| Advertisers needing multi‑touch attribution | 68% |

| Programmatic retail share | ~6–8% |

Full Version Awaits

Criteo Porter's Five Forces Analysis

This preview shows the exact Criteo Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or abridgments; the full, professionally formatted document is ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Criteo faces intense rivalry from major adtech platforms and rising programmatic entrants, moderate buyer power as advertisers demand ROI, and supplier leverage from data providers and publishers—while regulatory shifts and ad-blocking heighten substitute and threat risks.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Criteo’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Access to Premium Publisher Inventory

Criteo depends on thousands of publishers and SSPs for inventory, making them essential suppliers; in 2024 publishers delivered a large share of Criteo’s $1.6B ad-serving base. Premium publishers—top-tier sites that drive higher conversion rates—wield pricing and placement power, often commanding CPMs 2–4x market average. As the open internet shifts to curated, high-conversion slots, competition raises Criteo’s acquisition costs and squeezes margins.

Dependence on Cloud Infrastructure Providers

Criteo relies heavily on AWS and Google Cloud for AI/ML workloads, giving these providers strong bargaining power because their specialized infrastructure is costly to replicate and migrate; IDC estimated cloud migration costs average 200–400 USD per TB in 2024, so shifting Criteo’s petabytes would be material. Any price hike or SLA change by AWS/Google can squeeze Criteo’s 2024 adjusted EBIT margin (11.2%) and raise unit economics for programmatic ads.

Reliance on Web Browser and OS Policies

Suppliers of the technical environment, notably Google (Chrome) and Apple (iOS), set tracking and identity rules that directly shape Criteo’s ad tech; Google ended third-party cookie support in Chrome in 2024 and Apple’s App Tracking Transparency (launched 2021) persists, reducing addressable IDs by an estimated 30–40% for many ad platforms. Criteo must continually adapt its Commerce Media Platform to these gatekeepers’ privacy frameworks and SDK/API limits, which can materially cut targeting revenue and raise compliance costs.

Availability of Specialized AI Talent

The market for machine learning engineers and data scientists is highly competitive, making human capital a powerful supplier group; US median salary for ML engineers reached about $155,000 in 2024, and demand grew ~35% YoY in job postings. Criteo needs top-tier talent to keep its predictive bidding and recommendation edge, so wage pressure and richer benefits raise R&D and SG&A costs and tighten hiring timelines.

- ML engineer median pay $155k (US, 2024)

- Job postings +35% YoY (2023–24)

- Talent shortages increase R&D spend and hiring lag

- Employee leverage raises compensation and retention costs

Integration with Data Management Partners

Suppliers of third-party data and identity resolution remain crucial as Criteo shifts to first-party data; in 2024 Criteo reported first-party data now covers roughly 60% of signal needs but external providers still supply key enrichment and cross-device matching.

The consolidation of identity vendors post-cookie—top five providers controlling over 70% of market revenue in 2024—gives remaining leaders pricing power and raises switching costs for Criteo.

- First-party covers ~60% of signals (Criteo 2024)

- Top 5 identity vendors >70% market share (2024)

- Consolidation increases supplier leverage and switching cost

Criteo squeezed: publishers, cloud costs, talent, and identity vendors tighten margins

Criteo faces strong supplier power: publishers/SSPs drove a large share of its $1.6B 2024 revenue, premium publishers command 2–4x CPMs, AWS/Google cloud migration costs ~200–400 USD/TB raise switching costs, ML engineer median pay $155k (US, 2024) tightens hiring, and top‑5 identity vendors >70% market share; first‑party signals cover ~60% of needs (Criteo 2024).

| Metric | 2024 value |

|---|---|

| Revenue tied to publishers | $1.6B |

| Premium CPM premium | 2–4x |

| Cloud migration cost | $200–400/GB |

| ML median pay (US) | $155k |

| First‑party signal coverage | ~60% |

| Top5 identity market share | >70% |

What is included in the product

Tailored exclusively for Criteo, this Porter's Five Forces overview uncovers competitive intensity, buyer/supplier power, threat of new entrants and substitutes, and highlights disruptive trends and market entry risks shaping Criteo’s pricing power and profitability.

A concise Porter's Five Forces one-sheet for Criteo—instantly highlights competitive pressures and strategic levers to streamline boardroom decisions and investor briefings.

Customers Bargaining Power

Concentration of Large Retail Media Clients

Major retailers and global brands accounted for roughly 40% of Criteo's 2024 revenue (~€600m of €1.5bn), giving them strong negotiating leverage to demand lower prices, bespoke features, and tighter ecosystem integration.

Large clients can push for service-level concessions and data access; losing a top-5 retail partner would likely cut revenue by 5–10% and dent market share given Criteo’s concentrated client mix.

Demand for Transparent ROI and Attribution

Customers now demand clear ROI and attribution; 2024 surveys show 68% of e‑commerce advertisers require granular multi-touch attribution to justify ad spend, raising bargaining power.

That pressure forces Criteo to update reporting and attribution; Criteo reported product R&D spend of €169M in 2024 to improve measurement and machine‑learning models.

Easy cross‑platform comparisons—industry median ROAS (return on ad spend) variance ±12% across DSPs in 2024—makes switching cheaper if Criteo underperforms, increasing customer leverage.

Adoption of Multi-Platform Strategies

Many advertisers use multi-DSP (demand-side platform) mixes to avoid vendor lock-in and boost reach; industry surveys in 2024 show 68% of agencies run 3+ DSPs, cutting Criteo’s budget control.

Daily performance-based reallocations mean clients can shift spend within 24 hours; Criteo’s share of wallet fell to ~6–8% in programmatic retail ad segments in 2024, reflecting this churn.

Low switching friction forces Criteo to keep CPMs, ROAS, and reporting highly competitive; otherwise brands reallocate quickly, raising customer bargaining power.

Shift Toward In-House AdTech Capabilities

Agency Influence on Budget Allocation

Advertising agencies, which control roughly 30–40% of global digital ad budgets per WFA 2024 estimates, concentrate spend with preferred partners and can reallocate large volumes away from Criteo if platform UX or incentives falter.

Agencies can shift deals representing tens of millions in annual revenue; Criteo must prioritize agency-friendly tools, transparent fees, and bespoke incentives to retain steady allocations.

Strong, ongoing relationships with agency decision-makers reduce churn risk and support multi-year commitments—losing top agency accounts can cut programmatic revenue materially.

- Agencies control ~30–40% of digital budgets (WFA 2024)

- Shifts can represent tens of millions in revenue

- Focus: UX, transparent fees, tailored incentives

- Priority: sustained agency relationship management

Criteo: Top clients hold the cards—40% revenue concentration boosts buyer leverage

Major retailers and global brands drove ~40% of Criteo’s 2024 revenue (~€600M of €1.5B), giving them strong leverage to demand price cuts, bespoke features, and data access; losing a top-5 partner could cut revenue 5–10%.

68% of e‑commerce advertisers required granular multi‑touch attribution in 2024, 68% of agencies run 3+ DSPs, and Criteo’s programmatic retail share fell to ~6–8%, all raising customer bargaining power.

| Metric | 2024 Value |

|---|---|

| Revenue concentration (top clients) | ~40% (€600M) |

| R&D spend | €169M |

| Agencies using 3+ DSPs | 68% |

| Advertisers needing multi‑touch attribution | 68% |

| Programmatic retail share | ~6–8% |

Full Version Awaits

Criteo Porter's Five Forces Analysis

This preview shows the exact Criteo Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or abridgments; the full, professionally formatted document is ready for download and use the moment you buy.