Crossroads Systems Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

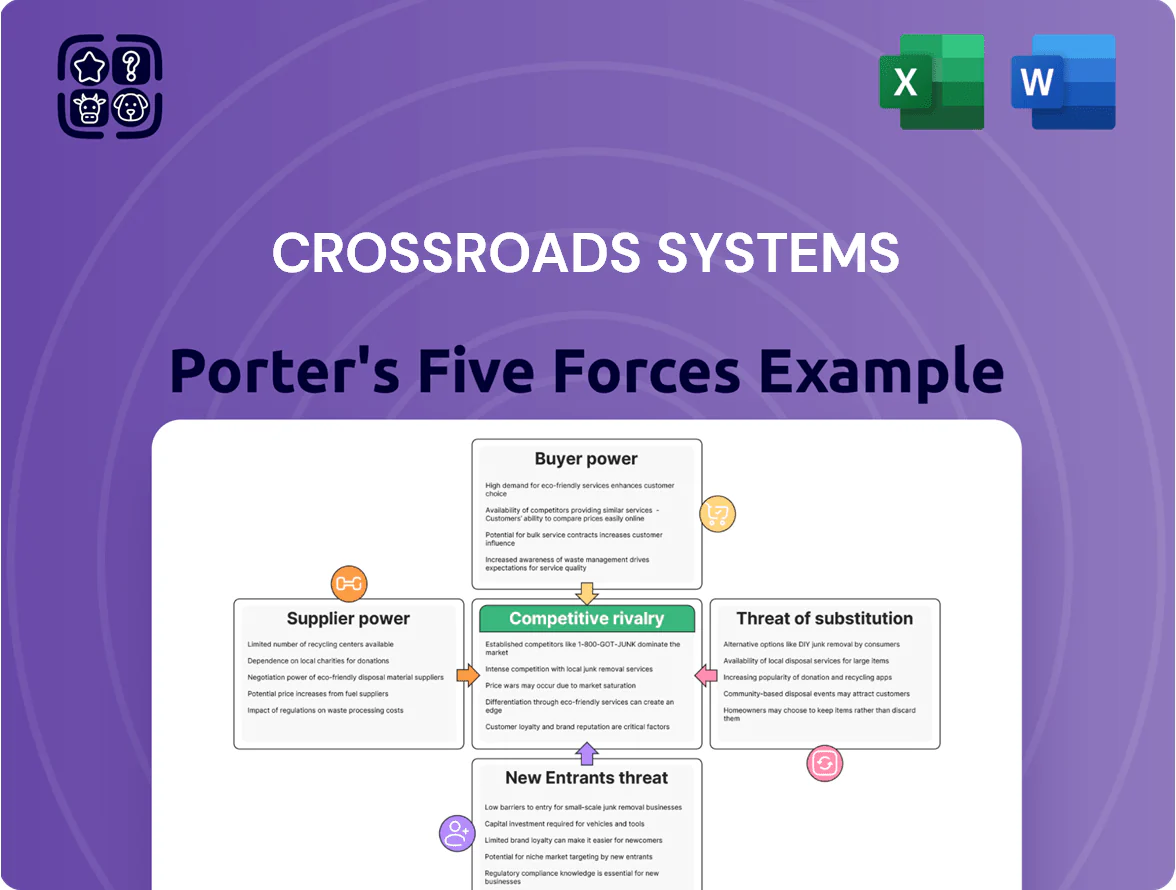

Crossroads Systems faces nuanced competitive pressures—from concentrated supplier relationships to evolving substitute threats—that shape margins and strategic choices; this snapshot highlights key tensions but omits detailed force ratings and scenario analysis.

This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Crossroads Systems’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Specialized Component Providers

The industrial tech sector depends on about 8–12 niche makers for high-precision sensors and microprocessors; these suppliers command price premiums of 10–25% and often 12–20 week lead times, giving them strong leverage over pricing and delivery.

With supplier consolidation—top 3 firms holding ~60% market share—Notis Global must lock long-term contracts and dual sourcing to prevent margin squeeze across its portfolio, since a 5% input-cost rise could cut EBITDA by ~2–4% per company.

Scarcity of Technical and Engineering Talent

The scarcity of industrial tech talent—global shortfall estimated at 40% for advanced automation skills in 2024—pushes up wages; Notis Global saw labor expense pressure with engineer pay premiums rising 12–18% in 2023–24, boosting supplier (labor) bargaining power. Specialized engineers and data scientists, especially in robotics and IIoT (industrial internet of things), can command higher offers, increasing holdco operating costs and deal premiums for acquisitions.

Dependency on Third-Party Software and Intellectual Property

Many industrial tech solutions rely on third-party software or patented IP; if Notis Global subsidiaries lack core ownership they face licensing risk—US software vendor price hikes averaged 6.4% in 2024 and enterprise license renewals rose 8% median, so fee increases or abrupt TOS changes can raise operating costs materially. This dependency boosts supplier leverage, potentially compressing EBITDA margins and raising capex for workarounds or buyouts.

Fluctuation in Raw Material and Energy Costs

High Switching Costs Between Suppliers

Transitioning to new suppliers in industrial tech often needs months of re-engineering and recertification; industry surveys show average integration time of 6–12 months and conversion costs equal to 5–15% of annual spend.

Those high switching costs let suppliers keep prices higher—suppliers in 2024 raised specialized-component margins ~150–300 basis points versus commodity peers—so buyers face sticky costs.

For a holding company like Notis Global, multi-year supply contracts and indexed pricing are essential to cap sudden cost spikes and secure uptime.

- Integration: 6–12 months, 5–15% of annual spend

- Supplier margin premium: +150–300 bps (2024)

- Mitigation: multi-year contracts, indexed pricing

Supplier concentration, price shocks cut EBITDA 3–5%—hedge with indexed contracts & dual sourcing

Suppliers hold strong leverage: 8–12 niche makers, top 3 = ~60% share, 12–20 week lead times, component premiums +10–25%, 2024 price shocks (copper +24%, neodymium +18%) mean a 10% input rise → ~3–5% EBITDA hit; switching 6–12 months, conversion cost 5–15% of spend, mitigation: multi‑year indexed contracts and dual sourcing.

| Metric | Value (2024) |

|---|---|

| Top-3 share | ~60% |

| Copper | +24% |

| Neodymium | +18% |

| Input rise → EBITDA | 10% → 3–5% |

What is included in the product

Tailored Porter's Five Forces analysis for Crossroads Systems, identifying competitive pressures, buyer/supplier influence, entrant barriers, substitution threats, and strategic levers to protect market share and profitability.

Compact Porter's Five Forces snapshot tailored for Crossroads Systems—instantly highlights competitive pressures so teams can prioritize strategic moves without sifting through clutter.

Customers Bargaining Power

Concentration of Large-Scale Industrial Buyers

Low Switching Costs for Standardized Hardware

In commoditized industrial hardware segments, customers switch easily with minimal downtime, so Notis Global must compete largely on price and basic service; 2024 industry surveys show 62% of purchasers prioritize cost over differentiation. Maintaining loyalty demands relentless operational efficiency and margin discipline—Notis reported a 3.8% YoY gross margin squeeze in 2024 in price-sensitive lines—plus aggressive pricing to curb churn.

High Access to Market and Pricing Information

In the digital economy, industrial buyers can access transparent pricing and detailed performance reviews for competing tech solutions, shrinking information asymmetries that once let Notis Global subsidiaries charge premiums; 2024 procurement surveys show 68% of enterprise buyers compare three+ vendors online before bidding.

Demand for Integrated and Bespoke Solutions

- 62% OEMs prefer single-vendor (2024 survey)

- Service revenue growth target 15–20% (2025 plan)

- Estimated margin pressure 8–12% on bespoke deals

Impact of Economic Cycles on Capital Expenditure

Industrial tech buys hinge on client capex, which fell 8.5% globally in 2023 amid rising rates; when GDP contracts and policy rates rose to a global 2023 average ~3.5%, buyers delayed or renegotiated purchases.

In downturns buyers gain leverage to demand longer payment terms, discounts, or cancel orders; Notis Global portfolio firms must offer flexible leasing, pay-per-use, or phased deliveries to win deals.

- Capex sensitivity: -8.5% global capex 2023

- Interest pressure: avg policy rate ~3.5% 2023

- Buyer tactics: delay, renegotiate, demand financing

- Response: leasing, subscription, phased contracts

Concentrated Buyers Drive Deep Discounts, Longer Terms—Bundled Services Key to Margin Recovery

| Metric | Value |

|---|---|

| Top10 share | 35–45% |

| Discounts | 10–25% |

| Payment terms | 60–120 days |

| Buyers compare vendors | 68% |

| Prefer single-vendor | 62% |

Preview Before You Purchase

Crossroads Systems Porter's Five Forces Analysis

This preview is the exact Crossroads Systems Porter's Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples; fully formatted and ready for use. The document shown is the final deliverable, containing complete evaluations of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry. Upon payment you’ll get instant access to this identical file for download and implementation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Crossroads Systems faces nuanced competitive pressures—from concentrated supplier relationships to evolving substitute threats—that shape margins and strategic choices; this snapshot highlights key tensions but omits detailed force ratings and scenario analysis.

This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Crossroads Systems’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Specialized Component Providers

The industrial tech sector depends on about 8–12 niche makers for high-precision sensors and microprocessors; these suppliers command price premiums of 10–25% and often 12–20 week lead times, giving them strong leverage over pricing and delivery.

With supplier consolidation—top 3 firms holding ~60% market share—Notis Global must lock long-term contracts and dual sourcing to prevent margin squeeze across its portfolio, since a 5% input-cost rise could cut EBITDA by ~2–4% per company.

Scarcity of Technical and Engineering Talent

The scarcity of industrial tech talent—global shortfall estimated at 40% for advanced automation skills in 2024—pushes up wages; Notis Global saw labor expense pressure with engineer pay premiums rising 12–18% in 2023–24, boosting supplier (labor) bargaining power. Specialized engineers and data scientists, especially in robotics and IIoT (industrial internet of things), can command higher offers, increasing holdco operating costs and deal premiums for acquisitions.

Dependency on Third-Party Software and Intellectual Property

Many industrial tech solutions rely on third-party software or patented IP; if Notis Global subsidiaries lack core ownership they face licensing risk—US software vendor price hikes averaged 6.4% in 2024 and enterprise license renewals rose 8% median, so fee increases or abrupt TOS changes can raise operating costs materially. This dependency boosts supplier leverage, potentially compressing EBITDA margins and raising capex for workarounds or buyouts.

Fluctuation in Raw Material and Energy Costs

High Switching Costs Between Suppliers

Transitioning to new suppliers in industrial tech often needs months of re-engineering and recertification; industry surveys show average integration time of 6–12 months and conversion costs equal to 5–15% of annual spend.

Those high switching costs let suppliers keep prices higher—suppliers in 2024 raised specialized-component margins ~150–300 basis points versus commodity peers—so buyers face sticky costs.

For a holding company like Notis Global, multi-year supply contracts and indexed pricing are essential to cap sudden cost spikes and secure uptime.

- Integration: 6–12 months, 5–15% of annual spend

- Supplier margin premium: +150–300 bps (2024)

- Mitigation: multi-year contracts, indexed pricing

Supplier concentration, price shocks cut EBITDA 3–5%—hedge with indexed contracts & dual sourcing

Suppliers hold strong leverage: 8–12 niche makers, top 3 = ~60% share, 12–20 week lead times, component premiums +10–25%, 2024 price shocks (copper +24%, neodymium +18%) mean a 10% input rise → ~3–5% EBITDA hit; switching 6–12 months, conversion cost 5–15% of spend, mitigation: multi‑year indexed contracts and dual sourcing.

| Metric | Value (2024) |

|---|---|

| Top-3 share | ~60% |

| Copper | +24% |

| Neodymium | +18% |

| Input rise → EBITDA | 10% → 3–5% |

What is included in the product

Tailored Porter's Five Forces analysis for Crossroads Systems, identifying competitive pressures, buyer/supplier influence, entrant barriers, substitution threats, and strategic levers to protect market share and profitability.

Compact Porter's Five Forces snapshot tailored for Crossroads Systems—instantly highlights competitive pressures so teams can prioritize strategic moves without sifting through clutter.

Customers Bargaining Power

Concentration of Large-Scale Industrial Buyers

Low Switching Costs for Standardized Hardware

In commoditized industrial hardware segments, customers switch easily with minimal downtime, so Notis Global must compete largely on price and basic service; 2024 industry surveys show 62% of purchasers prioritize cost over differentiation. Maintaining loyalty demands relentless operational efficiency and margin discipline—Notis reported a 3.8% YoY gross margin squeeze in 2024 in price-sensitive lines—plus aggressive pricing to curb churn.

High Access to Market and Pricing Information

In the digital economy, industrial buyers can access transparent pricing and detailed performance reviews for competing tech solutions, shrinking information asymmetries that once let Notis Global subsidiaries charge premiums; 2024 procurement surveys show 68% of enterprise buyers compare three+ vendors online before bidding.

Demand for Integrated and Bespoke Solutions

- 62% OEMs prefer single-vendor (2024 survey)

- Service revenue growth target 15–20% (2025 plan)

- Estimated margin pressure 8–12% on bespoke deals

Impact of Economic Cycles on Capital Expenditure

Industrial tech buys hinge on client capex, which fell 8.5% globally in 2023 amid rising rates; when GDP contracts and policy rates rose to a global 2023 average ~3.5%, buyers delayed or renegotiated purchases.

In downturns buyers gain leverage to demand longer payment terms, discounts, or cancel orders; Notis Global portfolio firms must offer flexible leasing, pay-per-use, or phased deliveries to win deals.

- Capex sensitivity: -8.5% global capex 2023

- Interest pressure: avg policy rate ~3.5% 2023

- Buyer tactics: delay, renegotiate, demand financing

- Response: leasing, subscription, phased contracts

Concentrated Buyers Drive Deep Discounts, Longer Terms—Bundled Services Key to Margin Recovery

| Metric | Value |

|---|---|

| Top10 share | 35–45% |

| Discounts | 10–25% |

| Payment terms | 60–120 days |

| Buyers compare vendors | 68% |

| Prefer single-vendor | 62% |

Preview Before You Purchase

Crossroads Systems Porter's Five Forces Analysis

This preview is the exact Crossroads Systems Porter's Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples; fully formatted and ready for use. The document shown is the final deliverable, containing complete evaluations of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry. Upon payment you’ll get instant access to this identical file for download and implementation.