CROWNHAITAI PESTLE Analysis

Your Shortcut to Market Insight Starts Here

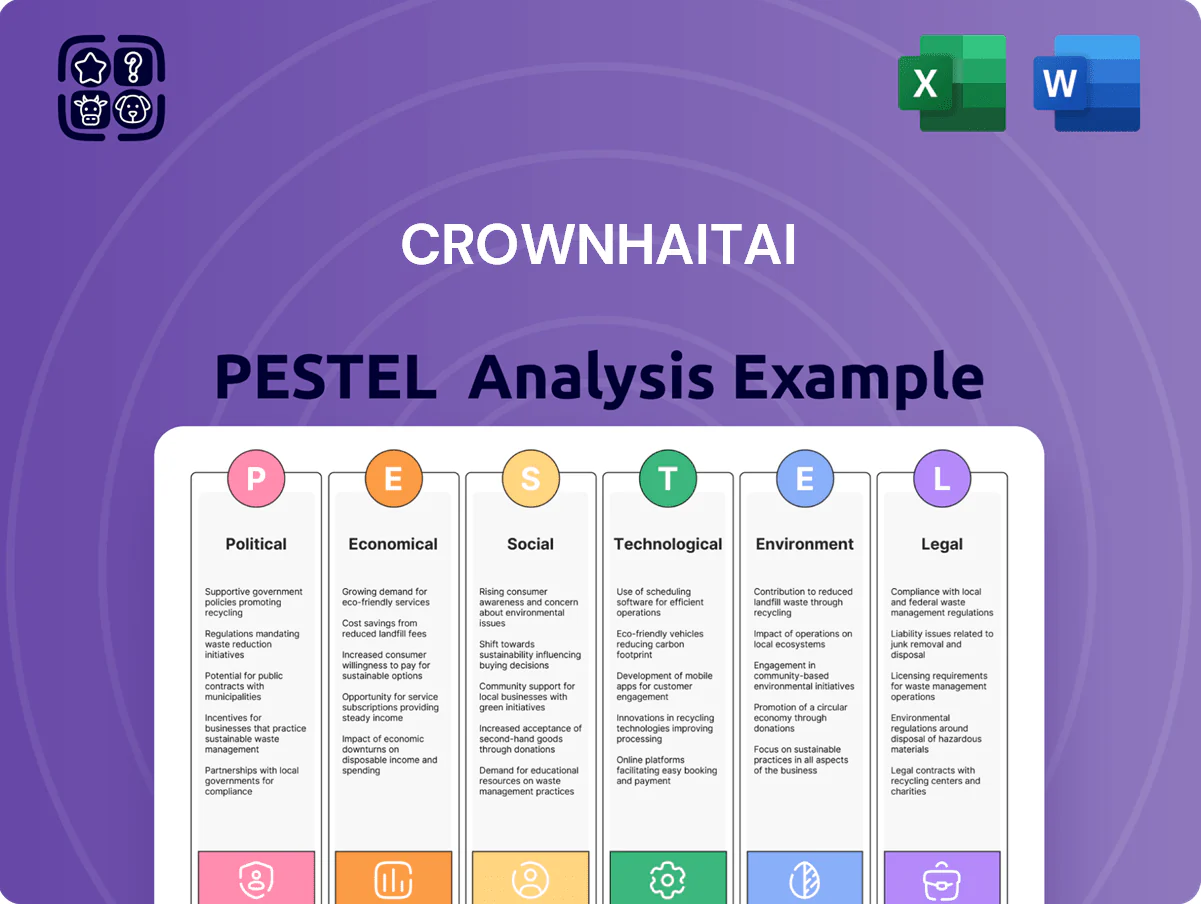

Gain strategic clarity with our PESTLE Analysis of CROWNHAITAI—unpack how political shifts, economic trends, social changes, technological advances, legal developments, and environmental pressures shape its prospects; buy the full report for actionable insights, ready-to-use charts, and strategic recommendations to inform investment and planning decisions.

Political factors

South Korean Trade Policy and Export Incentives

South Korea boosted K-Food export support in 2024–25, allocating about KRW 150 billion in subsidies and market-promotion funds to push into Southeast Asia and North America; CrownHaitai gains from tariff cuts under recent bilateral deals that lowered confectionery duties by up to 10% in partner markets.

Domestic Food Safety Regulations

The Ministry of Food and Drug Safety tightened additive limits and nutritional labeling rules through end-2025 mandates, raising compliance costs for CrownHaitai by an estimated 3–5% of COGS and risking fines up to KRW 500 million per violation.

CrownHaitai must modify production processes and supply chains to meet new standards, or face recalls that could cut domestic revenue by an estimated 8–12% in affected quarters.

While the rules aim to improve public health, increased quality-control spending and testing—projected at KRW 10–20 billion annually for major manufacturers—raise operating margins pressure.

Alignment with government health initiatives is now essential to retain market share in Korea, where domestic sales represent roughly 60% of CrownHaitai’s total revenue.

Geopolitical Stability and Supply Chain Security

Regional tensions in East Asia heighten risk for South Korean conglomerates; 2024 trade disruptions raised shipping insurance rates ~15% and contributed to a 7% YoY rise in import costs for food-grade sugar and a 5% rise for wheat. CrownHaitai tracks these developments as they directly affect input costs and supply timing. Government stockpiles—South Korea held ~1.3 million tonnes of wheat reserves in 2025—help buffer maritime shocks. Political stability is vital for CrownHaitai to proceed with planned logistics and packaging CAPEX totaling KRW 120 billion.

Labor Market Reforms and Minimum Wage Policies

Recent legislation capping the work week at 52 hours and annual minimum wage increases (minimum wage rose about 5.1% to 10.5% in 2024–2025 in South Korea) have raised labor costs for CrownHaitai’s snack and biscuit lines, squeezing margins in this labor-intensive segment.

The pro-worker political climate compels stronger protections, prompting CrownHaitai to accelerate automation investments and revise HR policies to sustain productivity and industrial harmony.

- 52-hour workweek enforcement

- Minimum wage hikes ~5–10% (2024–2025)

- Increased automation capex to offset labor costs

- Need for revised HR and shift scheduling

Corporate Governance and Chaebol Oversight

Enhanced Fair Trade Commission scrutiny of conglomerate structures and intra-group transactions forces CrownHaitai to tighten oversight of its 12 subsidiaries and report related-party transactions that accounted for 8% of consolidated revenue in 2024.

By late 2025, a strong political push for transparency in family-owned groups aims to protect minority shareholders, prompting CrownHaitai to expand internal audit headcount by 20% and adopt quarterly disclosure practices.

These governance standards require clearer communication with investors—improving ESG and governance scores (CrownHaitai’s Korea Corporate Governance Service rating target: A by 2026)—key to attracting institutional funds that now allocate 35% of equity to higher-governance Korean firms.

- FTC scrutiny → stricter related-party reporting (8% of 2024 revenue)

- 2025 transparency push → +20% internal audit capacity

- Target KCGS rating A by 2026 to attract institutional investors (35% allocation)

K-Food: KRW150bn export boost vs higher COGS, recalls, KRW120bn automation CAPEX

Political factors: stronger K-Food export support (KRW 150bn 2024–25), tighter MFDS rules raising COGS ~3–5% and recall risk cutting revenue 8–12% quarterly, labor cost pressure from 5–10% wage hikes and 52-hr cap driving KRW 120bn automation CAPEX, FTC scrutiny raised related-party oversight (8% of 2024 revenue) and +20% audit headcount to meet KCGS A target.

| Metric | Value |

|---|---|

| Export support | KRW 150bn |

| COGS impact | +3–5% |

| Recall revenue hit | 8–12% |

| Automation CAPEX | KRW 120bn |

| Related-party rev | 8% (2024) |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact CROWNHAITAI’s operations and growth prospects, with data-backed trends and region- and industry-tailored examples to help executives identify risks and opportunities for strategy and funding.

A concise, visually segmented PESTLE summary for CROWNHAITAI that streamlines meeting prep and slides, supports quick risk discussions, and is easily shared or annotated for local context and client reports.

Economic factors

Raw Material Price Volatility

Global cocoa, wheat and palm oil prices swung sharply into 2026 — cocoa up ~28% YoY, wheat/flour ~18% and palm oil ~22% — squeezing CrownHaitai’s margins; the firm reports COGS volatility increasing gross margin pressure in FY2025. The company uses hedging and multi‑year supply contracts covering ~60–75% of annual needs to smooth costs. Analysts flag COGS management as key; sustained agricultural price rises force targeted price hikes while protecting price‑sensitive customers.

Domestic Consumer Spending Power

In 2025 South Korea's economy posts a cautious recovery with GDP growth ~1.8% and household debt at about 104% of GDP, restraining discretionary spend on snacks and premium confectionery.

CrownHaitai tracks consumer confidence (Korea CCIs ~99 in 2025) to time product launches and promotions to prevailing demand conditions.

Basic snacks show resilience while high-end gift sets and premium chocolates are sensitive to disposable-income swings; prolonged stagnation could shift mix toward affordable, value-oriented SKUs.

Currency Exchange Rate Fluctuations

As a major importer of raw ingredients and exporter of finished goods, CrownHaitai faces significant exposure to KRW/USD and KRW/EUR swings; a 2024 average KRW/USD of ~1,290 vs 2023's 1,300 impacted gross margins by an estimated 40–60 bps on key input costs.

KRW appreciation reduces import costs but erodes export price competitiveness—exports accounted for ~18% of 2024 revenue, magnifying FX effects on sales.

The company uses hedging, FX forwards and options, and centralized treasury to smooth reported FX losses; 2024 hedged volume covered roughly 65–75% of expected FX exposure.

Investors monitor currency trends closely since quarterly FX swings contributed to earnings volatility of ±3–5% in 2024 for CrownHaitai.

Interest Rate Environment and Financing Costs

The late-2025 interest rate environment—with global benchmark rates averaging around 4.5% and South Korea’s base rate at 3.75%—raises CrownHaitai’s cost of capital for expansion and refinancing, increasing debt-servicing burdens and potentially delaying new plant or logistics investments.

Should rates stabilize, the firm can pursue more aggressive growth and R&D; maintaining a conservative debt-to-equity ratio (target ~0.5–0.8) remains critical for creditworthiness.

- Late-2025 benchmarks: global ~4.5%, South Korea 3.75%

- Higher rates → increased debt service, slower capex

- Stabilizing rates → more R&D and expansion

- Target debt-to-equity ~0.5–0.8 for strong credit

Logistics and Energy Cost Inflation

Rising global energy and freight costs — oil prices up ~15% in 2024 and container rates averaging 40% above pre‑pandemic levels — have increased CrownHaitai’s distribution expenses, prompting investments in fuel-efficient fleet upgrades and lightweight packaging that cut logistics spend per unit by an estimated 5–8%.

These inflationary pressures force adoption of route optimization, co-loading and regional hubs to protect typical snack industry margins near 5–8%, making logistics efficiency critical to profitability.

- Energy/fuel inflation: +15% (2024)

- Container rates: ~+40% vs 2019

- Estimated logistics cost reduction from initiatives: 5–8%

- Industry net margins to defend: 5–8%

Input cost surge and weak domestic demand squeeze margins amid 2025 rate drift

Volatile commodity prices (cocoa +28%, wheat +18%, palm oil +22% YoY) and higher energy/container costs (+15% oil, +40% containers) squeezed FY2025 margins; hedging/multi‑year contracts cover ~60–75% inputs and 65–75% FX. South Korea GDP ~1.8% (2025) and household debt ~104% dampen premium demand; exports ~18% revenue. Late‑2025 rates: KR base 3.75%, global ~4.5%; target D/E 0.5–0.8.

| Metric | 2024/25 |

|---|---|

| Cocoa | +28% YoY |

| Wheat | +18% YoY |

| Palm oil | +22% YoY |

| Oil | +15% |

| Containers | +40% |

| Exports | 18% rev |

| KR GDP | 1.8% |

| Household debt | 104% GDP |

| KR base rate | 3.75% |

What You See Is What You Get

CROWNHAITAI PESTLE Analysis

The preview shown here is the exact CROWNHAITAI PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Gain strategic clarity with our PESTLE Analysis of CROWNHAITAI—unpack how political shifts, economic trends, social changes, technological advances, legal developments, and environmental pressures shape its prospects; buy the full report for actionable insights, ready-to-use charts, and strategic recommendations to inform investment and planning decisions.

Political factors

South Korean Trade Policy and Export Incentives

South Korea boosted K-Food export support in 2024–25, allocating about KRW 150 billion in subsidies and market-promotion funds to push into Southeast Asia and North America; CrownHaitai gains from tariff cuts under recent bilateral deals that lowered confectionery duties by up to 10% in partner markets.

Domestic Food Safety Regulations

The Ministry of Food and Drug Safety tightened additive limits and nutritional labeling rules through end-2025 mandates, raising compliance costs for CrownHaitai by an estimated 3–5% of COGS and risking fines up to KRW 500 million per violation.

CrownHaitai must modify production processes and supply chains to meet new standards, or face recalls that could cut domestic revenue by an estimated 8–12% in affected quarters.

While the rules aim to improve public health, increased quality-control spending and testing—projected at KRW 10–20 billion annually for major manufacturers—raise operating margins pressure.

Alignment with government health initiatives is now essential to retain market share in Korea, where domestic sales represent roughly 60% of CrownHaitai’s total revenue.

Geopolitical Stability and Supply Chain Security

Regional tensions in East Asia heighten risk for South Korean conglomerates; 2024 trade disruptions raised shipping insurance rates ~15% and contributed to a 7% YoY rise in import costs for food-grade sugar and a 5% rise for wheat. CrownHaitai tracks these developments as they directly affect input costs and supply timing. Government stockpiles—South Korea held ~1.3 million tonnes of wheat reserves in 2025—help buffer maritime shocks. Political stability is vital for CrownHaitai to proceed with planned logistics and packaging CAPEX totaling KRW 120 billion.

Labor Market Reforms and Minimum Wage Policies

Recent legislation capping the work week at 52 hours and annual minimum wage increases (minimum wage rose about 5.1% to 10.5% in 2024–2025 in South Korea) have raised labor costs for CrownHaitai’s snack and biscuit lines, squeezing margins in this labor-intensive segment.

The pro-worker political climate compels stronger protections, prompting CrownHaitai to accelerate automation investments and revise HR policies to sustain productivity and industrial harmony.

- 52-hour workweek enforcement

- Minimum wage hikes ~5–10% (2024–2025)

- Increased automation capex to offset labor costs

- Need for revised HR and shift scheduling

Corporate Governance and Chaebol Oversight

Enhanced Fair Trade Commission scrutiny of conglomerate structures and intra-group transactions forces CrownHaitai to tighten oversight of its 12 subsidiaries and report related-party transactions that accounted for 8% of consolidated revenue in 2024.

By late 2025, a strong political push for transparency in family-owned groups aims to protect minority shareholders, prompting CrownHaitai to expand internal audit headcount by 20% and adopt quarterly disclosure practices.

These governance standards require clearer communication with investors—improving ESG and governance scores (CrownHaitai’s Korea Corporate Governance Service rating target: A by 2026)—key to attracting institutional funds that now allocate 35% of equity to higher-governance Korean firms.

- FTC scrutiny → stricter related-party reporting (8% of 2024 revenue)

- 2025 transparency push → +20% internal audit capacity

- Target KCGS rating A by 2026 to attract institutional investors (35% allocation)

K-Food: KRW150bn export boost vs higher COGS, recalls, KRW120bn automation CAPEX

Political factors: stronger K-Food export support (KRW 150bn 2024–25), tighter MFDS rules raising COGS ~3–5% and recall risk cutting revenue 8–12% quarterly, labor cost pressure from 5–10% wage hikes and 52-hr cap driving KRW 120bn automation CAPEX, FTC scrutiny raised related-party oversight (8% of 2024 revenue) and +20% audit headcount to meet KCGS A target.

| Metric | Value |

|---|---|

| Export support | KRW 150bn |

| COGS impact | +3–5% |

| Recall revenue hit | 8–12% |

| Automation CAPEX | KRW 120bn |

| Related-party rev | 8% (2024) |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact CROWNHAITAI’s operations and growth prospects, with data-backed trends and region- and industry-tailored examples to help executives identify risks and opportunities for strategy and funding.

A concise, visually segmented PESTLE summary for CROWNHAITAI that streamlines meeting prep and slides, supports quick risk discussions, and is easily shared or annotated for local context and client reports.

Economic factors

Raw Material Price Volatility

Global cocoa, wheat and palm oil prices swung sharply into 2026 — cocoa up ~28% YoY, wheat/flour ~18% and palm oil ~22% — squeezing CrownHaitai’s margins; the firm reports COGS volatility increasing gross margin pressure in FY2025. The company uses hedging and multi‑year supply contracts covering ~60–75% of annual needs to smooth costs. Analysts flag COGS management as key; sustained agricultural price rises force targeted price hikes while protecting price‑sensitive customers.

Domestic Consumer Spending Power

In 2025 South Korea's economy posts a cautious recovery with GDP growth ~1.8% and household debt at about 104% of GDP, restraining discretionary spend on snacks and premium confectionery.

CrownHaitai tracks consumer confidence (Korea CCIs ~99 in 2025) to time product launches and promotions to prevailing demand conditions.

Basic snacks show resilience while high-end gift sets and premium chocolates are sensitive to disposable-income swings; prolonged stagnation could shift mix toward affordable, value-oriented SKUs.

Currency Exchange Rate Fluctuations

As a major importer of raw ingredients and exporter of finished goods, CrownHaitai faces significant exposure to KRW/USD and KRW/EUR swings; a 2024 average KRW/USD of ~1,290 vs 2023's 1,300 impacted gross margins by an estimated 40–60 bps on key input costs.

KRW appreciation reduces import costs but erodes export price competitiveness—exports accounted for ~18% of 2024 revenue, magnifying FX effects on sales.

The company uses hedging, FX forwards and options, and centralized treasury to smooth reported FX losses; 2024 hedged volume covered roughly 65–75% of expected FX exposure.

Investors monitor currency trends closely since quarterly FX swings contributed to earnings volatility of ±3–5% in 2024 for CrownHaitai.

Interest Rate Environment and Financing Costs

The late-2025 interest rate environment—with global benchmark rates averaging around 4.5% and South Korea’s base rate at 3.75%—raises CrownHaitai’s cost of capital for expansion and refinancing, increasing debt-servicing burdens and potentially delaying new plant or logistics investments.

Should rates stabilize, the firm can pursue more aggressive growth and R&D; maintaining a conservative debt-to-equity ratio (target ~0.5–0.8) remains critical for creditworthiness.

- Late-2025 benchmarks: global ~4.5%, South Korea 3.75%

- Higher rates → increased debt service, slower capex

- Stabilizing rates → more R&D and expansion

- Target debt-to-equity ~0.5–0.8 for strong credit

Logistics and Energy Cost Inflation

Rising global energy and freight costs — oil prices up ~15% in 2024 and container rates averaging 40% above pre‑pandemic levels — have increased CrownHaitai’s distribution expenses, prompting investments in fuel-efficient fleet upgrades and lightweight packaging that cut logistics spend per unit by an estimated 5–8%.

These inflationary pressures force adoption of route optimization, co-loading and regional hubs to protect typical snack industry margins near 5–8%, making logistics efficiency critical to profitability.

- Energy/fuel inflation: +15% (2024)

- Container rates: ~+40% vs 2019

- Estimated logistics cost reduction from initiatives: 5–8%

- Industry net margins to defend: 5–8%

Input cost surge and weak domestic demand squeeze margins amid 2025 rate drift

Volatile commodity prices (cocoa +28%, wheat +18%, palm oil +22% YoY) and higher energy/container costs (+15% oil, +40% containers) squeezed FY2025 margins; hedging/multi‑year contracts cover ~60–75% inputs and 65–75% FX. South Korea GDP ~1.8% (2025) and household debt ~104% dampen premium demand; exports ~18% revenue. Late‑2025 rates: KR base 3.75%, global ~4.5%; target D/E 0.5–0.8.

| Metric | 2024/25 |

|---|---|

| Cocoa | +28% YoY |

| Wheat | +18% YoY |

| Palm oil | +22% YoY |

| Oil | +15% |

| Containers | +40% |

| Exports | 18% rev |

| KR GDP | 1.8% |

| Household debt | 104% GDP |

| KR base rate | 3.75% |

What You See Is What You Get

CROWNHAITAI PESTLE Analysis

The preview shown here is the exact CROWNHAITAI PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and decision-making.