Citic Securities Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

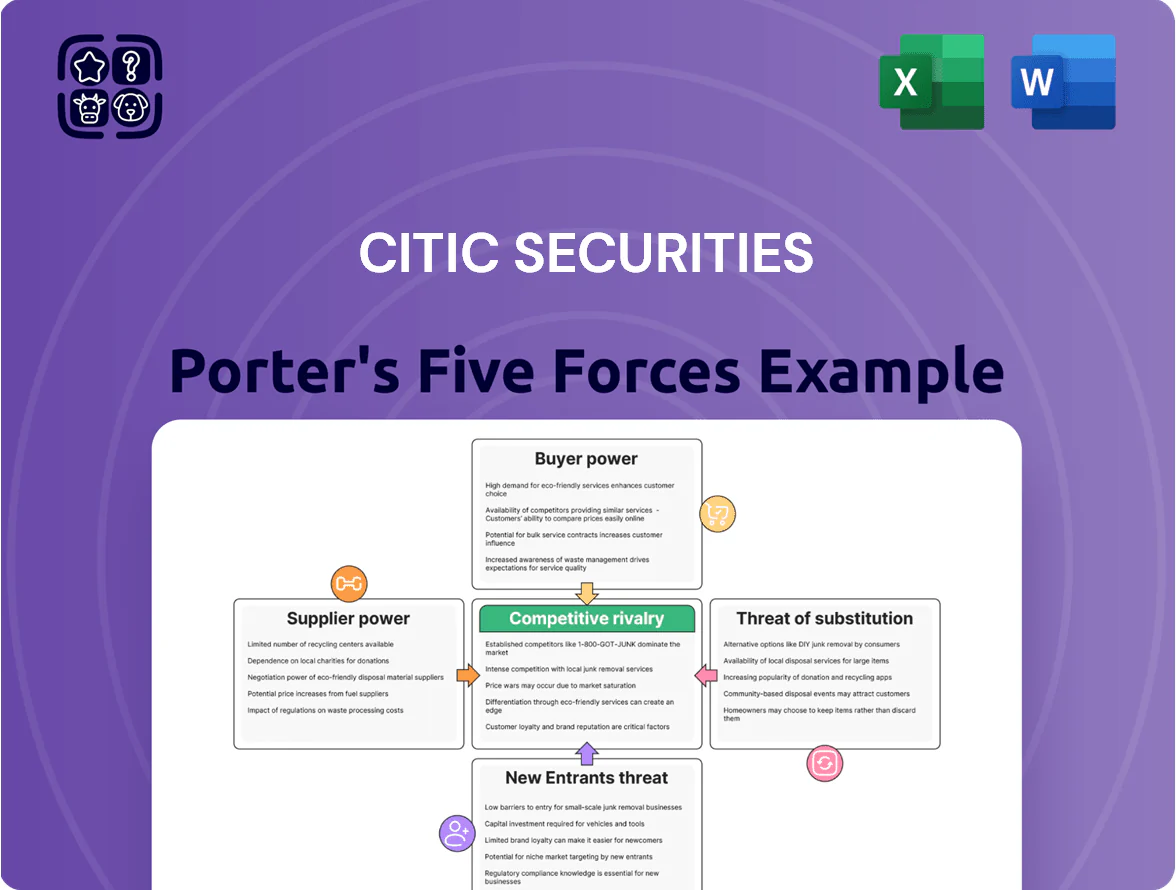

Citic Securities faces intense rivalry from domestic and international brokerages, regulatory scrutiny that shapes market access, and concentrated client bargaining power—while technology and new entrants modestly pressure margins; this snapshot highlights strategic strengths and vulnerabilities that influence profitability.

Suppliers Bargaining Power

Concentration of High-End Financial Talent

The primary suppliers for CITIC Securities are senior investment bankers, quantitative analysts, and portfolio managers whose scarcity drives high bargaining power; as of Q4 2025, top-tier hires command 30–50% higher cash-plus-equity packages versus 2019 benchmarks. Global banks and domestic boutiques competed for the same limited pool, with China financial headcount growth slowing to 2% in 2024, tightening supply. CITIC sustains aggressive salaries, sign-on bonuses, and long-term equity to curb churn; turnover among senior hires rose to 12% in 2025 without such measures.

Dependence on Financial Data and Technology Providers

CITIC Securities depends on data vendors Bloomberg, Wind, and Refinitiv and on proprietary tech providers; these platforms are embedded across trading and research, accounting for an estimated 6–9% of annual IT and vendor spend as of 2024. The deep integration raises switching costs—operational disruption and retraining can exceed millions of yuan—so suppliers hold leverage. During renewals vendors can push price increases; a 2023 market survey showed 60% of APAC brokerages faced vendor price hikes of 5–12%.

Access to Interbank Liquidity and Capital Markets

As a financial intermediary, CITIC Securities relies on interbank and institutional funding; in 2024 China’s money-market tightness saw 7-day repo rates spike to ~4.2% in June, raising short-term funding costs and strengthening supplier leverage over balance-sheet activities.

Regulatory Infrastructure and Exchange Dependencies

Stock exchanges and clearinghouses in China, like Shanghai and Shenzhen Stock Exchanges and the China Securities Depository and Clearing Corporation (CSDC), are state-sanctioned utilities that CITIC Securities cannot bypass, leaving it with effectively zero bargaining power over transaction fees and compliance rules.

Exchange rule changes and settlement procedure updates must be implemented immediately; for example, Shanghai's 2024 fee schedule raised certain transaction levies by up to 12%, forcing broker cost increases and creating a fixed-cost environment where the infrastructure supplier dictates operational terms.

Specialized Professional Service Firms

CITIC Securities depends on top-tier law firms, Big Four accountants, and major credit-rating agencies for complex IPOs and cross-border M&A; their brand and regulatory need for independent verification give these suppliers strong bargaining power.

In 2024 CITIC paid premiums—legal/accounting fees often 0.5–1.2% of deal value on mega-deals; only ~10–15 global firms handle transactions >$1bn, concentrating power and limiting negotiation leverage.

Accepting higher fees preserves credibility for investors and regulators, so CITIC routinely trades price for reputational assurance.

- Regulatory need: independent verification

- Fee range: 0.5–1.2% on mega-deals (2024)

- Supplier concentration: ~10–15 global firms

Suppliers’ Squeeze: Talent, Data & Fees Drive Costs Higher Across Finance

Suppliers (senior talent, data vendors, exchanges, legal/accounting) wield strong bargaining power: senior hire packages +30–50% vs 2019 (Q4 2025), data/vendor spend 6–9% of IT (2024), 60% APAC brokerages saw vendor hikes 5–12% (2023), Shanghai fee hike ~12% (2024), legal/accounting 0.5–1.2% on mega-deals (2024).

| Supplier | Key metric |

|---|---|

| Senior hires | +30–50% pay (Q4 2025) |

| Data vendors | 6–9% IT spend (2024) |

| Exchanges | ~12% fee hike (2024) |

| Legal/Acct | 0.5–1.2% deal fees (2024) |

What is included in the product

Uncovers key competitive drivers for Citic Securities—assessing rival intensity, buyer/supplier power, entry barriers, substitutes, and emerging disruptors to illuminate pricing, market share risks, and strategic defenses.

A concise Porter's Five Forces one-sheet for Citic Securities—instantly highlights competitive pressures and strategic levers for fast, board-ready decisions.

Customers Bargaining Power

Institutional Investor Influence on Commission Rates

Large institutional clients—mutual funds and insurers—wield strong bargaining power at CITIC Securities due to trade volumes: top 50 clients accounted for ~35% of flow in 2024, so they demand lower commissions and bespoke research.

Since 2025, commission unbundling (separating research from execution) has cut opaque fees; buyers now secure ~10–25% cheaper execution fees in negotiated deals.

CITIC must prove superior execution (sub-5bps slippage on large blocks) and deliver alpha-generating research to retain these high-value accounts.

Corporate Client Leverage in Underwriting Fees

Corporate issuers can shop among top-tier banks, and in 2024 around 60% of large PRC IPOs ran competitive processes, letting SOEs and tech firms push down underwriting spreads by 10–30 basis points.

Retail Investor Price Sensitivity and Low Switching Costs

The retail brokerage segment has many individual investors who, per China Securities Regulatory Commission 2024 figures, drove retail trades to ~70% of transaction volume, making clients highly price-sensitive to commissions and fees.

With mobile apps (e.g., 2025 active mobile trading users ~200m in China), switching costs from CITIC Securities are near-zero, so retention demands heavy investment in UX and services.

Commoditized core brokerage services have shifted bargaining power to consumers, forcing CITIC to add research, wealth management, and lower fees to reduce churn.

High Net Worth Individuals and Bespoke Demands

High-net-worth clients demand tailored wealth management, exclusive private equity and structured products; globally, HNW customers control about 45% of China’s investable wealth as of 2024, raising stakes for CITIC Securities.

Their financial literacy lets them benchmark CITIC vs global private banks, pressuring fees down and service up; in 2023, fee-sensitive flows moved toward boutiques offering 1–1.2% AUM fees.

To retain share, CITIC must offer sophisticated, high-alpha products that justify fees; failure leads to rapid capital flight to niche managers with superior customization.

- HNW control ~45% China investable wealth (2024)

- Boutique AUM fees 1–1.2% (2023)

- Exclusive PE access, structured products required

Sophistication of Asset Management Clients

Clients in CITIC Securities’ asset management arm are shifting to passive funds and performance-based fees, cutting demand for traditional active management and refusing to pay for underperformance; global ETF flows hit US$2.1trn in 2024, raising client expectations.

Wider access to global products and transparent performance metrics—industry average active manager outflows of 8% in 2023—mean CITIC must compete for every yuan of AUM, strengthening buyer bargaining power.

- Global ETF flows US$2.1trn (2024)

- Active manager net outflows 8% (2023)

- Rise in performance-fee mandates across APAC (2022–24)

CITIC faces fee squeeze: win mandates with <5bps execution & high‑alpha research

Buyers hold strong power: top 50 clients ~35% flow (2024), retail ~70% trade volume (CSRC 2024), HNW hold ~45% investable wealth (2024); commission unbundling cut fees 10–25% (since 2025); CITIC must deliver sub-5bps block execution and high-alpha research or lose mandates to boutiques (AUM fees 1–1.2% in 2023).

| Metric | Value |

|---|---|

| Top-50 flow | ~35% (2024) |

| Retail trade vol | ~70% (2024) |

| HNW wealth | ~45% (2024) |

| Fee cut | 10–25% (since 2025) |

| Boutique AUM fee | 1–1.2% (2023) |

Preview the Actual Deliverable

Citic Securities Porter's Five Forces Analysis

This preview shows the exact Citic Securities Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready to use. It contains the complete assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, along with concise implications for strategy and valuation. Purchase grants instant access to this same document for download.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Citic Securities faces intense rivalry from domestic and international brokerages, regulatory scrutiny that shapes market access, and concentrated client bargaining power—while technology and new entrants modestly pressure margins; this snapshot highlights strategic strengths and vulnerabilities that influence profitability.

Suppliers Bargaining Power

Concentration of High-End Financial Talent

The primary suppliers for CITIC Securities are senior investment bankers, quantitative analysts, and portfolio managers whose scarcity drives high bargaining power; as of Q4 2025, top-tier hires command 30–50% higher cash-plus-equity packages versus 2019 benchmarks. Global banks and domestic boutiques competed for the same limited pool, with China financial headcount growth slowing to 2% in 2024, tightening supply. CITIC sustains aggressive salaries, sign-on bonuses, and long-term equity to curb churn; turnover among senior hires rose to 12% in 2025 without such measures.

Dependence on Financial Data and Technology Providers

CITIC Securities depends on data vendors Bloomberg, Wind, and Refinitiv and on proprietary tech providers; these platforms are embedded across trading and research, accounting for an estimated 6–9% of annual IT and vendor spend as of 2024. The deep integration raises switching costs—operational disruption and retraining can exceed millions of yuan—so suppliers hold leverage. During renewals vendors can push price increases; a 2023 market survey showed 60% of APAC brokerages faced vendor price hikes of 5–12%.

Access to Interbank Liquidity and Capital Markets

As a financial intermediary, CITIC Securities relies on interbank and institutional funding; in 2024 China’s money-market tightness saw 7-day repo rates spike to ~4.2% in June, raising short-term funding costs and strengthening supplier leverage over balance-sheet activities.

Regulatory Infrastructure and Exchange Dependencies

Stock exchanges and clearinghouses in China, like Shanghai and Shenzhen Stock Exchanges and the China Securities Depository and Clearing Corporation (CSDC), are state-sanctioned utilities that CITIC Securities cannot bypass, leaving it with effectively zero bargaining power over transaction fees and compliance rules.

Exchange rule changes and settlement procedure updates must be implemented immediately; for example, Shanghai's 2024 fee schedule raised certain transaction levies by up to 12%, forcing broker cost increases and creating a fixed-cost environment where the infrastructure supplier dictates operational terms.

Specialized Professional Service Firms

CITIC Securities depends on top-tier law firms, Big Four accountants, and major credit-rating agencies for complex IPOs and cross-border M&A; their brand and regulatory need for independent verification give these suppliers strong bargaining power.

In 2024 CITIC paid premiums—legal/accounting fees often 0.5–1.2% of deal value on mega-deals; only ~10–15 global firms handle transactions >$1bn, concentrating power and limiting negotiation leverage.

Accepting higher fees preserves credibility for investors and regulators, so CITIC routinely trades price for reputational assurance.

- Regulatory need: independent verification

- Fee range: 0.5–1.2% on mega-deals (2024)

- Supplier concentration: ~10–15 global firms

Suppliers’ Squeeze: Talent, Data & Fees Drive Costs Higher Across Finance

Suppliers (senior talent, data vendors, exchanges, legal/accounting) wield strong bargaining power: senior hire packages +30–50% vs 2019 (Q4 2025), data/vendor spend 6–9% of IT (2024), 60% APAC brokerages saw vendor hikes 5–12% (2023), Shanghai fee hike ~12% (2024), legal/accounting 0.5–1.2% on mega-deals (2024).

| Supplier | Key metric |

|---|---|

| Senior hires | +30–50% pay (Q4 2025) |

| Data vendors | 6–9% IT spend (2024) |

| Exchanges | ~12% fee hike (2024) |

| Legal/Acct | 0.5–1.2% deal fees (2024) |

What is included in the product

Uncovers key competitive drivers for Citic Securities—assessing rival intensity, buyer/supplier power, entry barriers, substitutes, and emerging disruptors to illuminate pricing, market share risks, and strategic defenses.

A concise Porter's Five Forces one-sheet for Citic Securities—instantly highlights competitive pressures and strategic levers for fast, board-ready decisions.

Customers Bargaining Power

Institutional Investor Influence on Commission Rates

Large institutional clients—mutual funds and insurers—wield strong bargaining power at CITIC Securities due to trade volumes: top 50 clients accounted for ~35% of flow in 2024, so they demand lower commissions and bespoke research.

Since 2025, commission unbundling (separating research from execution) has cut opaque fees; buyers now secure ~10–25% cheaper execution fees in negotiated deals.

CITIC must prove superior execution (sub-5bps slippage on large blocks) and deliver alpha-generating research to retain these high-value accounts.

Corporate Client Leverage in Underwriting Fees

Corporate issuers can shop among top-tier banks, and in 2024 around 60% of large PRC IPOs ran competitive processes, letting SOEs and tech firms push down underwriting spreads by 10–30 basis points.

Retail Investor Price Sensitivity and Low Switching Costs

The retail brokerage segment has many individual investors who, per China Securities Regulatory Commission 2024 figures, drove retail trades to ~70% of transaction volume, making clients highly price-sensitive to commissions and fees.

With mobile apps (e.g., 2025 active mobile trading users ~200m in China), switching costs from CITIC Securities are near-zero, so retention demands heavy investment in UX and services.

Commoditized core brokerage services have shifted bargaining power to consumers, forcing CITIC to add research, wealth management, and lower fees to reduce churn.

High Net Worth Individuals and Bespoke Demands

High-net-worth clients demand tailored wealth management, exclusive private equity and structured products; globally, HNW customers control about 45% of China’s investable wealth as of 2024, raising stakes for CITIC Securities.

Their financial literacy lets them benchmark CITIC vs global private banks, pressuring fees down and service up; in 2023, fee-sensitive flows moved toward boutiques offering 1–1.2% AUM fees.

To retain share, CITIC must offer sophisticated, high-alpha products that justify fees; failure leads to rapid capital flight to niche managers with superior customization.

- HNW control ~45% China investable wealth (2024)

- Boutique AUM fees 1–1.2% (2023)

- Exclusive PE access, structured products required

Sophistication of Asset Management Clients

Clients in CITIC Securities’ asset management arm are shifting to passive funds and performance-based fees, cutting demand for traditional active management and refusing to pay for underperformance; global ETF flows hit US$2.1trn in 2024, raising client expectations.

Wider access to global products and transparent performance metrics—industry average active manager outflows of 8% in 2023—mean CITIC must compete for every yuan of AUM, strengthening buyer bargaining power.

- Global ETF flows US$2.1trn (2024)

- Active manager net outflows 8% (2023)

- Rise in performance-fee mandates across APAC (2022–24)

CITIC faces fee squeeze: win mandates with <5bps execution & high‑alpha research

Buyers hold strong power: top 50 clients ~35% flow (2024), retail ~70% trade volume (CSRC 2024), HNW hold ~45% investable wealth (2024); commission unbundling cut fees 10–25% (since 2025); CITIC must deliver sub-5bps block execution and high-alpha research or lose mandates to boutiques (AUM fees 1–1.2% in 2023).

| Metric | Value |

|---|---|

| Top-50 flow | ~35% (2024) |

| Retail trade vol | ~70% (2024) |

| HNW wealth | ~45% (2024) |

| Fee cut | 10–25% (since 2025) |

| Boutique AUM fee | 1–1.2% (2023) |

Preview the Actual Deliverable

Citic Securities Porter's Five Forces Analysis

This preview shows the exact Citic Securities Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready to use. It contains the complete assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, along with concise implications for strategy and valuation. Purchase grants instant access to this same document for download.