China National Building Porter's Five Forces Analysis

Don't Miss the Bigger Picture

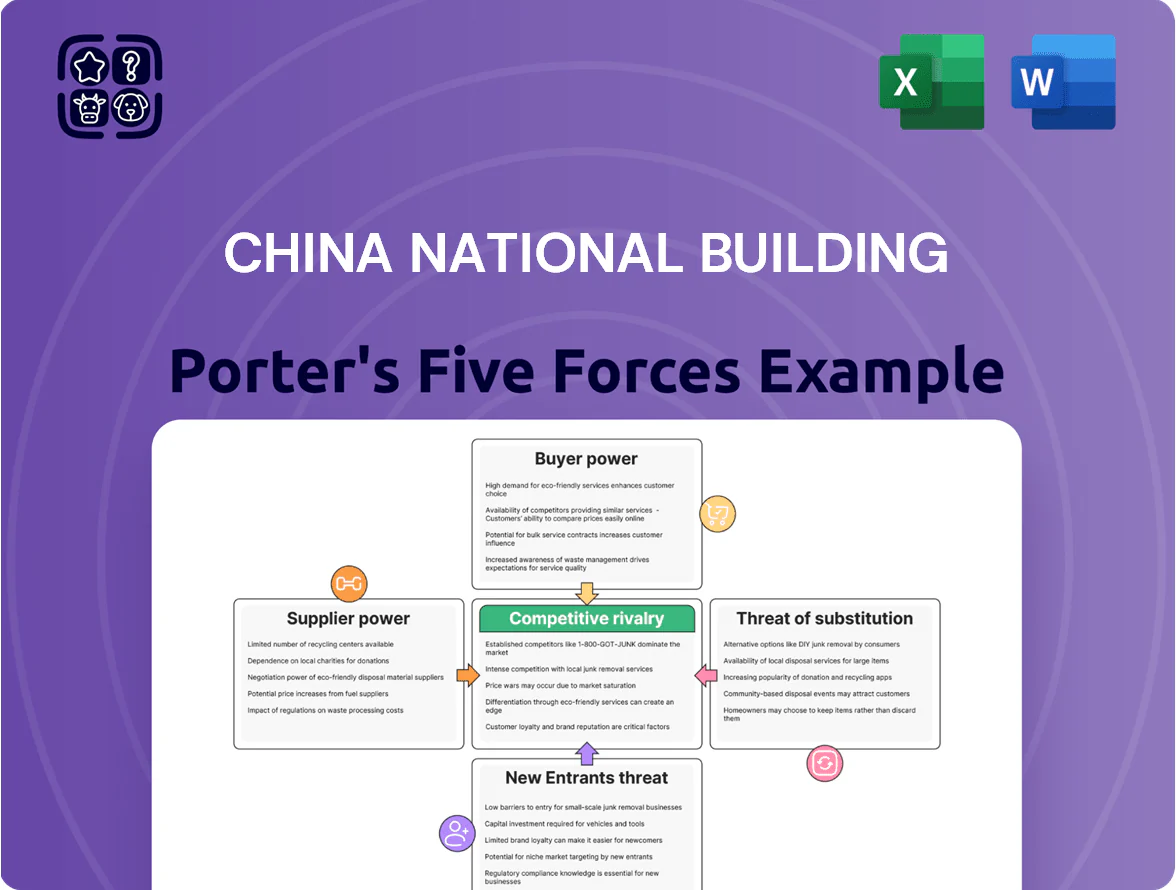

China National Building faces intense rivalry from large state-backed peers, moderate supplier power due to diversified material sources, and growing buyer sophistication as clients demand integrated, tech-enabled construction solutions.

Regulatory oversight and high capital barriers lower new entrant threats, while substitutes like modular construction and off-site prefabrication present rising risks to traditional models.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore China National Building’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Raw Material Providers

The supply of steel and cement in China is concentrated among state-owned giants like China Baowu Group and CNBM, limiting CSCEC’s unilateral price setting; Baowu produced 61.2 million tonnes of steel in 2024. By late 2025 CSCEC’s annual procurement—over RMB 300 billion—secures multi-year contracts that cut price volatility, while its volume gives leverage over smaller regional suppliers that depend on CSCEC for >30% of their sales.

Impact of Fluctuating Commodity Prices

Global energy and iron ore price swings raised input costs 18% YoY by Q4 2025, forcing many suppliers to pass increases to buyers; CSCEC (China State Construction Engineering Corporation) absorbed part via integrated supply-chain ops, trimming pass-through to ~6 percentage points.

CSCEC’s strategic stockpiles equal ~3 months of key materials and a diversified supplier base across 12 provinces and 8 countries reduced procurement disruption risk by an estimated 40% during 2024–25 spikes.

Labor Market Dynamics and Specialized Skills

Demographic aging cut China’s 15–59 working-age population by 22m from 2015–2020, tightening general labor and skilled engineer supply for construction.

Suppliers of high-tech equipment and specialized engineering services gained leverage as CSCEC (China State Construction Engineering Corporation) pivots to smart-city projects, where imported tech can carry 10–15% premium.

CSCEC has spent ~RMB 4.2bn in 2023–2024 on training and automation; internal upskilling and robotics aim to cut external labor dependence by an estimated 18% by 2026.

Technological Integration and Proprietary Systems

Suppliers of advanced building tech and sustainable materials gained leverage in 2025 as China tightened emissions rules, raising demand for low-carbon concrete and energy systems; CSCEC reported procurement of green materials rose 28% YoY in 2025, deepening supplier ties and reducing switching flexibility.

CSCEC’s frequent collaborations create mutual dependency that stabilizes pricing but locks workflows to partners; integrating proprietary construction software averages $6–12 million and 9–14 months per large project, strengthening supplier bargaining power.

- 2025: green-materials procurement +28% YoY

- Proprietary software cost $6–12M

- Integration time 9–14 months

- Higher switching costs, reduced supplier substitution

Geopolitical Influence on International Sourcing

- Local suppliers can command +10–25% price premium

- Importing materials can reduce costs ~15%

- Supplier leverage rises where few local providers exist

- Global logistics network is CSCEC’s primary countermeasure

Supplier concentration caps CSCEC pricing power despite RMB300bn buying, green surge

Suppliers concentrated (China Baowu, CNBM) limit CSCEC price-setting despite CSCEC’s RMB 300bn+ procurement and multi-year contracts; Baowu made 61.2mt steel in 2024. Energy/ore swings pushed input costs +18% YoY by Q4 2025; CSCEC integration trimmed pass-through to ~6pp. Green-materials procurement +28% YoY (2025) raised supplier leverage; stockpiles ~3 months cut disruption risk ~40%.

| Metric | Value |

|---|---|

| CSCEC procurement (annual) | RMB 300bn+ |

| Baowu steel output (2024) | 61.2 mt |

| Input cost change (2024–25) | +18% YoY |

| Pass-through after integration | ~6 percentage points |

| Green procurement growth (2025) | +28% YoY |

| Stockpile coverage | ~3 months (−40% disruption) |

What is included in the product

Offers a tailored Porter’s Five Forces assessment for China National Building, outlining competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and identifying disruptive forces and entry barriers that shape pricing, margins, and strategic positioning.

A concise Porter’s Five Forces snapshot tailored to China National Building—rapidly identify supplier, buyer, and competitive pressures to steer strategy and bidding decisions.

Customers Bargaining Power

Dominance of Government and Public Sector Clients

A significant share of China State Construction Engineering Corporation’s (CSCEC) revenue—about 55% in 2024—comes from government-led infrastructure and public housing, giving the state strong bargaining power; authorities commonly impose pricing caps and payment terms averaging 90–180 days, which pressure contractor cash flow. Still, by 2025 CSCEC’s pivot to high-quality, low-carbon projects and its technical track record let it extract slightly better margins and upfront guarantees on ~20% of new contracts.

Real Estate Market Consolidation and Buyer Sophistication

Rising buyer sophistication in China’s residential market has increased bargaining power: surveys show 62% of urban homebuyers in 2024 rated green certification and smart-home features as key purchase drivers, pushing CSCEC to upgrade offerings to protect margins. CSCEC faces premium developers and institutional investors demanding higher specs, so by late 2025 it targets LEED/China Three-Star certifications and smart-home penetration above 40% in new projects to retain share.

Contractual Power and Risk Allocation

Large industrial and commercial clients force risk onto contractors via turnkey contracts and competitive bids that cut margins; in 2024 Chinese port and infrastructure tenders drove average EPC margins down to ~4–6% for major projects. Clients demand cash-backed performance bonds often equal to 5–10% of contract value and liquidated damages of 0.5–1% monthly. CSCEC (China State Construction Engineering Corporation) offsets this by selling lifecycle management services—operations, maintenance, and asset upgrades—that raised recurring revenue to 12% of group revenue in 2023, spreading risk and boosting lifetime margin.

Availability of Alternative Service Providers

The presence of several large state-owned builders—notably China State Construction Engineering Corp (CSCEC), China Railway Construction Corp, and China Communications Construction Co—gives buyers multiple options for mega projects, raising buyer bargaining power during tenders.

Clients often leverage rival bids; CSCEC counters by stressing its edge in ultra-high-rise and complex infrastructure projects, where it won 28% of China’s top-tier urban megaproject contracts in 2024.

- Multiple SOEs available → higher buyer leverage

- Competitive tendering drives price and terms pressure

- CSCEC’s niche: ultra-high-rise & complex infra

- 2024: CSCEC captured 28% of top-tier megaproject contracts

Economic Influence on Private Development Spending

Slower Chinese and global GDP growth cuts private capex, boosting buyers' leverage to demand lower prices and flexible payment terms; private sector construction investment fell 4.8% y/y in 2024, raising contract renegotiations.

CSCEC shifted by end-2025 to innovative financing—more PPPs and deferred-payment schedules—helping keep c. RMB 120 billion of projects active and reducing cancellations by ~18%.

- Private construction investment down 4.8% in 2024

- CSCEC kept ~RMB 120bn projects via new financing

- Cancellations cut ~18% after PPP adoption

Buyers Drive Terms as Govt Projects Dominate; CSCEC Fights Back with Megaproject Wins

Buyers hold strong leverage: govt projects (55% revenue in 2024) set price caps and 90–180 day terms; private capex fell 4.8% y/y in 2024, raising renegotiations. Large SOE rivals increase tender pressure; EPC margins for major projects sat ~4–6% in 2024. CSCEC won 28% of top-tier megaprojects in 2024 and grew recurring revenue to 12% in 2023 to counter buyer power.

| Metric | Value |

|---|---|

| Govt revenue share (2024) | 55% |

| Private construction investment change (2024) | -4.8% |

| EPC margins (2024) | 4–6% |

| Megaproject share (CSCEC, 2024) | 28% |

| Recurring revenue (2023) | 12% |

Full Version Awaits

China National Building Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of China National Building you’ll receive—fully formatted, professionally written, and ready for immediate use upon purchase.

It’s the same complete document available for download after payment: no samples, no placeholders, and no further customization required.

The file you see here contains the final analysis and insights into competitive rivalry, supplier and buyer power, threats of substitutes, and barriers to entry—precisely what you’ll get.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

China National Building faces intense rivalry from large state-backed peers, moderate supplier power due to diversified material sources, and growing buyer sophistication as clients demand integrated, tech-enabled construction solutions.

Regulatory oversight and high capital barriers lower new entrant threats, while substitutes like modular construction and off-site prefabrication present rising risks to traditional models.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore China National Building’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Raw Material Providers

The supply of steel and cement in China is concentrated among state-owned giants like China Baowu Group and CNBM, limiting CSCEC’s unilateral price setting; Baowu produced 61.2 million tonnes of steel in 2024. By late 2025 CSCEC’s annual procurement—over RMB 300 billion—secures multi-year contracts that cut price volatility, while its volume gives leverage over smaller regional suppliers that depend on CSCEC for >30% of their sales.

Impact of Fluctuating Commodity Prices

Global energy and iron ore price swings raised input costs 18% YoY by Q4 2025, forcing many suppliers to pass increases to buyers; CSCEC (China State Construction Engineering Corporation) absorbed part via integrated supply-chain ops, trimming pass-through to ~6 percentage points.

CSCEC’s strategic stockpiles equal ~3 months of key materials and a diversified supplier base across 12 provinces and 8 countries reduced procurement disruption risk by an estimated 40% during 2024–25 spikes.

Labor Market Dynamics and Specialized Skills

Demographic aging cut China’s 15–59 working-age population by 22m from 2015–2020, tightening general labor and skilled engineer supply for construction.

Suppliers of high-tech equipment and specialized engineering services gained leverage as CSCEC (China State Construction Engineering Corporation) pivots to smart-city projects, where imported tech can carry 10–15% premium.

CSCEC has spent ~RMB 4.2bn in 2023–2024 on training and automation; internal upskilling and robotics aim to cut external labor dependence by an estimated 18% by 2026.

Technological Integration and Proprietary Systems

Suppliers of advanced building tech and sustainable materials gained leverage in 2025 as China tightened emissions rules, raising demand for low-carbon concrete and energy systems; CSCEC reported procurement of green materials rose 28% YoY in 2025, deepening supplier ties and reducing switching flexibility.

CSCEC’s frequent collaborations create mutual dependency that stabilizes pricing but locks workflows to partners; integrating proprietary construction software averages $6–12 million and 9–14 months per large project, strengthening supplier bargaining power.

- 2025: green-materials procurement +28% YoY

- Proprietary software cost $6–12M

- Integration time 9–14 months

- Higher switching costs, reduced supplier substitution

Geopolitical Influence on International Sourcing

- Local suppliers can command +10–25% price premium

- Importing materials can reduce costs ~15%

- Supplier leverage rises where few local providers exist

- Global logistics network is CSCEC’s primary countermeasure

Supplier concentration caps CSCEC pricing power despite RMB300bn buying, green surge

Suppliers concentrated (China Baowu, CNBM) limit CSCEC price-setting despite CSCEC’s RMB 300bn+ procurement and multi-year contracts; Baowu made 61.2mt steel in 2024. Energy/ore swings pushed input costs +18% YoY by Q4 2025; CSCEC integration trimmed pass-through to ~6pp. Green-materials procurement +28% YoY (2025) raised supplier leverage; stockpiles ~3 months cut disruption risk ~40%.

| Metric | Value |

|---|---|

| CSCEC procurement (annual) | RMB 300bn+ |

| Baowu steel output (2024) | 61.2 mt |

| Input cost change (2024–25) | +18% YoY |

| Pass-through after integration | ~6 percentage points |

| Green procurement growth (2025) | +28% YoY |

| Stockpile coverage | ~3 months (−40% disruption) |

What is included in the product

Offers a tailored Porter’s Five Forces assessment for China National Building, outlining competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and identifying disruptive forces and entry barriers that shape pricing, margins, and strategic positioning.

A concise Porter’s Five Forces snapshot tailored to China National Building—rapidly identify supplier, buyer, and competitive pressures to steer strategy and bidding decisions.

Customers Bargaining Power

Dominance of Government and Public Sector Clients

A significant share of China State Construction Engineering Corporation’s (CSCEC) revenue—about 55% in 2024—comes from government-led infrastructure and public housing, giving the state strong bargaining power; authorities commonly impose pricing caps and payment terms averaging 90–180 days, which pressure contractor cash flow. Still, by 2025 CSCEC’s pivot to high-quality, low-carbon projects and its technical track record let it extract slightly better margins and upfront guarantees on ~20% of new contracts.

Real Estate Market Consolidation and Buyer Sophistication

Rising buyer sophistication in China’s residential market has increased bargaining power: surveys show 62% of urban homebuyers in 2024 rated green certification and smart-home features as key purchase drivers, pushing CSCEC to upgrade offerings to protect margins. CSCEC faces premium developers and institutional investors demanding higher specs, so by late 2025 it targets LEED/China Three-Star certifications and smart-home penetration above 40% in new projects to retain share.

Contractual Power and Risk Allocation

Large industrial and commercial clients force risk onto contractors via turnkey contracts and competitive bids that cut margins; in 2024 Chinese port and infrastructure tenders drove average EPC margins down to ~4–6% for major projects. Clients demand cash-backed performance bonds often equal to 5–10% of contract value and liquidated damages of 0.5–1% monthly. CSCEC (China State Construction Engineering Corporation) offsets this by selling lifecycle management services—operations, maintenance, and asset upgrades—that raised recurring revenue to 12% of group revenue in 2023, spreading risk and boosting lifetime margin.

Availability of Alternative Service Providers

The presence of several large state-owned builders—notably China State Construction Engineering Corp (CSCEC), China Railway Construction Corp, and China Communications Construction Co—gives buyers multiple options for mega projects, raising buyer bargaining power during tenders.

Clients often leverage rival bids; CSCEC counters by stressing its edge in ultra-high-rise and complex infrastructure projects, where it won 28% of China’s top-tier urban megaproject contracts in 2024.

- Multiple SOEs available → higher buyer leverage

- Competitive tendering drives price and terms pressure

- CSCEC’s niche: ultra-high-rise & complex infra

- 2024: CSCEC captured 28% of top-tier megaproject contracts

Economic Influence on Private Development Spending

Slower Chinese and global GDP growth cuts private capex, boosting buyers' leverage to demand lower prices and flexible payment terms; private sector construction investment fell 4.8% y/y in 2024, raising contract renegotiations.

CSCEC shifted by end-2025 to innovative financing—more PPPs and deferred-payment schedules—helping keep c. RMB 120 billion of projects active and reducing cancellations by ~18%.

- Private construction investment down 4.8% in 2024

- CSCEC kept ~RMB 120bn projects via new financing

- Cancellations cut ~18% after PPP adoption

Buyers Drive Terms as Govt Projects Dominate; CSCEC Fights Back with Megaproject Wins

Buyers hold strong leverage: govt projects (55% revenue in 2024) set price caps and 90–180 day terms; private capex fell 4.8% y/y in 2024, raising renegotiations. Large SOE rivals increase tender pressure; EPC margins for major projects sat ~4–6% in 2024. CSCEC won 28% of top-tier megaprojects in 2024 and grew recurring revenue to 12% in 2023 to counter buyer power.

| Metric | Value |

|---|---|

| Govt revenue share (2024) | 55% |

| Private construction investment change (2024) | -4.8% |

| EPC margins (2024) | 4–6% |

| Megaproject share (CSCEC, 2024) | 28% |

| Recurring revenue (2023) | 12% |

Full Version Awaits

China National Building Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of China National Building you’ll receive—fully formatted, professionally written, and ready for immediate use upon purchase.

It’s the same complete document available for download after payment: no samples, no placeholders, and no further customization required.

The file you see here contains the final analysis and insights into competitive rivalry, supplier and buyer power, threats of substitutes, and barriers to entry—precisely what you’ll get.