CSG PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political, economic, social, technological, legal, and environmental forces are shaping CSG's future with our concise PESTLE overview—perfect for investors and strategists seeking actionable context. Buy the full PESTLE analysis to access deep-dive insights, editable templates, and timely recommendations you can use immediately to de-risk decisions and seize growth opportunities.

Political factors

Geopolitical Trade Relations

Ongoing US-China tensions and EU trade policy shifts have led 18% of telecom procurement officers in 2024 to prioritize suppliers with limited exposure to sanctioned jurisdictions, forcing CSG to reassess supply chains and contracts worth an estimated $220m in annual international revenue.

Government Connectivity Mandates

Many governments target universal broadband: US BEAD program allocated $42.45B (2021) and EU Digital Decade aims 100% gigabit coverage by 2030, fueling demand for BSS platforms; CSG benefits as operators onboard millions of subsidized subscribers requiring billing and care systems.

Data Sovereignty Policies

An increasing number of countries—over 60 as of 2024 per UNCTAD—have enacted data localization rules requiring citizen data to be stored domestically; this forces CSG to rework cloud delivery into localized data centers or hybrid models, potentially raising capex by 15–25% per region versus centralized clouds. Noncompliance risks market exclusion and fines: e.g., India and EU regimes impose penalties up to 4% of global turnover under GDPR-style frameworks.

National Security Regulations

Political scrutiny on telecom infrastructure security has increased; in 2024, 68% of OECD regulators tightened vendor vetting, forcing software suppliers like CSG to pass enhanced cybersecurity audits and supply-chain checks.

CSG must provide demonstrable transparency, SOC 2/ISO 27001 evidence and real-time telemetry to satisfy oversight bodies guarding networks that carry over $1.5 trillion in global telecom revenue (2024).

Those rules restrict operator partner lists—countries reporting restrictions rose 22% in 2023—impacting CSG’s addressable market and contract qualification timelines.

- 68% of OECD regulators tightened vendor vetting (2024)

- CSG needs SOC 2/ISO 27001 and telemetry for compliance

- $1.5T global telecom revenue dependent on secure networks (2024)

- 22% increase in partner-restriction policies (2023)

Public Sector Digitalization

Governments worldwide increased IT modernization budgets to an estimated $280bn in 2024, boosting demand for BSS providers; CSG can leverage this as public-sector digitalization expands beyond telecom/media into citizen services and back-office automation.

Political backing and legislative funding—for example US federal IT modernization allocations of $28bn+ in 2024—enable CSG to diversify revenue streams and bid for long-term government contracts focused on citizen engagement platforms and efficiency gains.

- 2024 global gov IT spend ~$280bn

- US federal IT modernization >$28bn (2024)

- Opportunity: diversify client base beyond telco/media

- Focus: citizen engagement, operational efficiency via BSS

Regulatory squeeze risks $220M revenue; regional capex +15–25% amid gov IT opportunity

Geopolitical tensions, sanctions exposure and tightened vendor vetting (68% of OECD regulators in 2024) compress CSG’s addressable market and force supply‑chain reconfiguration, risking $220m in international revenue and longer contract timelines. Data localization in 60+ countries and GDPR-style fines (up to 4% global turnover) require localized cloud/hybrid deployments, raising regional capex 15–25%. Rising public IT budgets (~$280bn global, >$28bn US in 2024) open government BSS opportunities.

| Metric | 2024 value |

|---|---|

| OECD regulators tightening | 68% |

| Countries with data localization | 60+ |

| Potential revenue at risk | $220m |

| Regional capex uplift | 15–25% |

| Global gov IT spend | $280bn |

| US federal IT modernization | $28bn+ |

What is included in the product

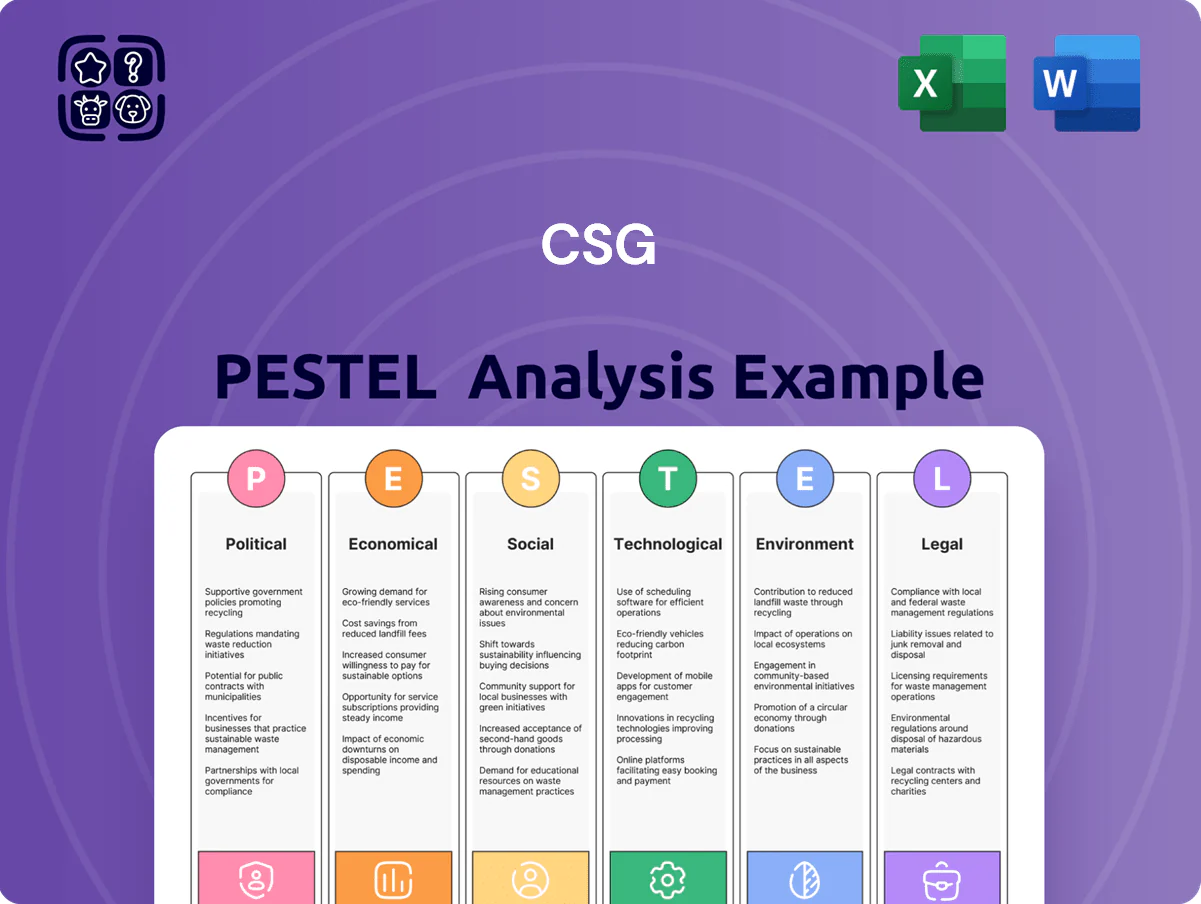

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact the CSG, combining data-driven trends and region-specific examples to highlight risks and opportunities.

Condenses the full CSG PESTLE into a clean, shareable summary that’s visually segmented by category for quick interpretation and easily dropped into presentations or planning sessions.

Economic factors

Global Inflationary Pressures

Persistent global inflation through 2024–2025, with US CPI averaging ~3–4% in 2024 and eurozone inflation near 2.5% by late 2025, has raised CSG’s operational costs and those of telecom clients; wage inflation for software engineers rose ~5–7% in 2024, squeezing margins. High inflation risks reduced consumer discretionary spend, with global pay-TV churn up ~2–3% in 2024 as households cut premium media. CSG must adjust pricing to protect margins while offering cost-management tools to clients facing price-sensitive subscriber bases.

Currency Exchange Volatility

As a global entity, CSG faces FX risk that can swing reported revenue and EBIT; FX movements erased about 2–4% of comparable revenues for similar tech firms in 2024, and a 10% local currency devaluation in emerging markets can raise dollar-priced services by roughly the same magnitude, reducing demand. Strategic hedging (forwards/options) and localized pricing models proved crucial—companies using hedges covered 60–80% of exposure in 2024 to stabilize margins.

Telecom Sector Consolidation

Industry consolidation cut global telecom operators with revenue >$1B by ~12% from 2018–2023; M&A deal value in telecoms hit $84B in 2023, concentrating spend among fewer buyers. Larger contracts post-merger can raise ARPU per client but raise churn risk—integration-related platform exits accounted for ~15% of lost contract value in recent large deals. CSG must position its BSS as the default unified ops platform to capture higher-value consolidated contracts and mitigate migration losses.

Subscription Economy Growth

The global subscription economy reached about $1.8 trillion in recurring revenue in 2024, growing ~11% year-over-year, underpinning steady demand for CSG’s revenue management tools.

As non-telecom sectors—SaaS, streaming, health, and IoT—drive adoption, CSG’s addressable market expands; McKinsey estimates 30–40% of enterprise revenues shifting to subscriptions by 2026.

The shift demands advanced analytics and flexible billing; CSG’s platform supports complex pricing, configured bundles, and usage-based models that enterprises increasingly require.

- 2024 subscription economy ~$1.8T, +11% YoY

- 30–40% enterprise revenue to subscriptions by 2026

- Rising demand for usage-based billing and analytics

Capital Expenditure Trends

The pace of 5G rollout hinges on operator capex for radio and core upgrades plus BSS/OSS; global telco capex reached about $347 billion in 2024, up ~3% YoY, supporting demand for monetization platforms.

Rising rates in 2023–2025 pressured operator balance sheets — average telco net debt/EBITDA ~2.8x in 2024 — which can delay advanced BSS investments and slow CSG revenue growth tied to infrastructure cycles.

CSG’s FY2024 exposure to network-driven spend links its growth to the global infrastructure investment cycle; a 1% decline in operator capex could materially dent near-term BSS project starts.

- Global telco capex ~ $347B in 2024 (+3% YoY)

- Average telco net debt/EBITDA ~2.8x in 2024

- Higher rates (2023–25) constrain capex, slowing BSS adoption

- CSG growth closely correlated with operator infrastructure spend

Telco margins squeezed as subscription boom meets inflation, FX hits and cautious capex

Inflation (US CPI ~3–4% in 2024; eurozone ~2.5% by 2025) and 5–7% wage growth squeezed margins; subscription economy ~$1.8T in 2024 (+11% YoY) expands demand; FX volatility shaved ~2–4% revenue for peers in 2024; global telco capex ~$347B in 2024 (+3% YoY) but net debt/EBITDA ~2.8x constrains spend.

| Metric | 2024 |

|---|---|

| Subscription economy | $1.8T (+11%) |

| Global telco capex | $347B (+3%) |

| Telco net debt/EBITDA | ~2.8x |

| FX revenue impact | −2–4% |

What You See Is What You Get

CSG PESTLE Analysis

The preview shown here is the exact CSG PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic analysis.

No placeholders or teasers: the layout, content, and conclusions visible in this preview are the same file you’ll download immediately after payment.

Everything displayed is part of the final product, giving you a complete, actionable PESTLE assessment of CSG upon checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political, economic, social, technological, legal, and environmental forces are shaping CSG's future with our concise PESTLE overview—perfect for investors and strategists seeking actionable context. Buy the full PESTLE analysis to access deep-dive insights, editable templates, and timely recommendations you can use immediately to de-risk decisions and seize growth opportunities.

Political factors

Geopolitical Trade Relations

Ongoing US-China tensions and EU trade policy shifts have led 18% of telecom procurement officers in 2024 to prioritize suppliers with limited exposure to sanctioned jurisdictions, forcing CSG to reassess supply chains and contracts worth an estimated $220m in annual international revenue.

Government Connectivity Mandates

Many governments target universal broadband: US BEAD program allocated $42.45B (2021) and EU Digital Decade aims 100% gigabit coverage by 2030, fueling demand for BSS platforms; CSG benefits as operators onboard millions of subsidized subscribers requiring billing and care systems.

Data Sovereignty Policies

An increasing number of countries—over 60 as of 2024 per UNCTAD—have enacted data localization rules requiring citizen data to be stored domestically; this forces CSG to rework cloud delivery into localized data centers or hybrid models, potentially raising capex by 15–25% per region versus centralized clouds. Noncompliance risks market exclusion and fines: e.g., India and EU regimes impose penalties up to 4% of global turnover under GDPR-style frameworks.

National Security Regulations

Political scrutiny on telecom infrastructure security has increased; in 2024, 68% of OECD regulators tightened vendor vetting, forcing software suppliers like CSG to pass enhanced cybersecurity audits and supply-chain checks.

CSG must provide demonstrable transparency, SOC 2/ISO 27001 evidence and real-time telemetry to satisfy oversight bodies guarding networks that carry over $1.5 trillion in global telecom revenue (2024).

Those rules restrict operator partner lists—countries reporting restrictions rose 22% in 2023—impacting CSG’s addressable market and contract qualification timelines.

- 68% of OECD regulators tightened vendor vetting (2024)

- CSG needs SOC 2/ISO 27001 and telemetry for compliance

- $1.5T global telecom revenue dependent on secure networks (2024)

- 22% increase in partner-restriction policies (2023)

Public Sector Digitalization

Governments worldwide increased IT modernization budgets to an estimated $280bn in 2024, boosting demand for BSS providers; CSG can leverage this as public-sector digitalization expands beyond telecom/media into citizen services and back-office automation.

Political backing and legislative funding—for example US federal IT modernization allocations of $28bn+ in 2024—enable CSG to diversify revenue streams and bid for long-term government contracts focused on citizen engagement platforms and efficiency gains.

- 2024 global gov IT spend ~$280bn

- US federal IT modernization >$28bn (2024)

- Opportunity: diversify client base beyond telco/media

- Focus: citizen engagement, operational efficiency via BSS

Regulatory squeeze risks $220M revenue; regional capex +15–25% amid gov IT opportunity

Geopolitical tensions, sanctions exposure and tightened vendor vetting (68% of OECD regulators in 2024) compress CSG’s addressable market and force supply‑chain reconfiguration, risking $220m in international revenue and longer contract timelines. Data localization in 60+ countries and GDPR-style fines (up to 4% global turnover) require localized cloud/hybrid deployments, raising regional capex 15–25%. Rising public IT budgets (~$280bn global, >$28bn US in 2024) open government BSS opportunities.

| Metric | 2024 value |

|---|---|

| OECD regulators tightening | 68% |

| Countries with data localization | 60+ |

| Potential revenue at risk | $220m |

| Regional capex uplift | 15–25% |

| Global gov IT spend | $280bn |

| US federal IT modernization | $28bn+ |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact the CSG, combining data-driven trends and region-specific examples to highlight risks and opportunities.

Condenses the full CSG PESTLE into a clean, shareable summary that’s visually segmented by category for quick interpretation and easily dropped into presentations or planning sessions.

Economic factors

Global Inflationary Pressures

Persistent global inflation through 2024–2025, with US CPI averaging ~3–4% in 2024 and eurozone inflation near 2.5% by late 2025, has raised CSG’s operational costs and those of telecom clients; wage inflation for software engineers rose ~5–7% in 2024, squeezing margins. High inflation risks reduced consumer discretionary spend, with global pay-TV churn up ~2–3% in 2024 as households cut premium media. CSG must adjust pricing to protect margins while offering cost-management tools to clients facing price-sensitive subscriber bases.

Currency Exchange Volatility

As a global entity, CSG faces FX risk that can swing reported revenue and EBIT; FX movements erased about 2–4% of comparable revenues for similar tech firms in 2024, and a 10% local currency devaluation in emerging markets can raise dollar-priced services by roughly the same magnitude, reducing demand. Strategic hedging (forwards/options) and localized pricing models proved crucial—companies using hedges covered 60–80% of exposure in 2024 to stabilize margins.

Telecom Sector Consolidation

Industry consolidation cut global telecom operators with revenue >$1B by ~12% from 2018–2023; M&A deal value in telecoms hit $84B in 2023, concentrating spend among fewer buyers. Larger contracts post-merger can raise ARPU per client but raise churn risk—integration-related platform exits accounted for ~15% of lost contract value in recent large deals. CSG must position its BSS as the default unified ops platform to capture higher-value consolidated contracts and mitigate migration losses.

Subscription Economy Growth

The global subscription economy reached about $1.8 trillion in recurring revenue in 2024, growing ~11% year-over-year, underpinning steady demand for CSG’s revenue management tools.

As non-telecom sectors—SaaS, streaming, health, and IoT—drive adoption, CSG’s addressable market expands; McKinsey estimates 30–40% of enterprise revenues shifting to subscriptions by 2026.

The shift demands advanced analytics and flexible billing; CSG’s platform supports complex pricing, configured bundles, and usage-based models that enterprises increasingly require.

- 2024 subscription economy ~$1.8T, +11% YoY

- 30–40% enterprise revenue to subscriptions by 2026

- Rising demand for usage-based billing and analytics

Capital Expenditure Trends

The pace of 5G rollout hinges on operator capex for radio and core upgrades plus BSS/OSS; global telco capex reached about $347 billion in 2024, up ~3% YoY, supporting demand for monetization platforms.

Rising rates in 2023–2025 pressured operator balance sheets — average telco net debt/EBITDA ~2.8x in 2024 — which can delay advanced BSS investments and slow CSG revenue growth tied to infrastructure cycles.

CSG’s FY2024 exposure to network-driven spend links its growth to the global infrastructure investment cycle; a 1% decline in operator capex could materially dent near-term BSS project starts.

- Global telco capex ~ $347B in 2024 (+3% YoY)

- Average telco net debt/EBITDA ~2.8x in 2024

- Higher rates (2023–25) constrain capex, slowing BSS adoption

- CSG growth closely correlated with operator infrastructure spend

Telco margins squeezed as subscription boom meets inflation, FX hits and cautious capex

Inflation (US CPI ~3–4% in 2024; eurozone ~2.5% by 2025) and 5–7% wage growth squeezed margins; subscription economy ~$1.8T in 2024 (+11% YoY) expands demand; FX volatility shaved ~2–4% revenue for peers in 2024; global telco capex ~$347B in 2024 (+3% YoY) but net debt/EBITDA ~2.8x constrains spend.

| Metric | 2024 |

|---|---|

| Subscription economy | $1.8T (+11%) |

| Global telco capex | $347B (+3%) |

| Telco net debt/EBITDA | ~2.8x |

| FX revenue impact | −2–4% |

What You See Is What You Get

CSG PESTLE Analysis

The preview shown here is the exact CSG PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic analysis.

No placeholders or teasers: the layout, content, and conclusions visible in this preview are the same file you’ll download immediately after payment.

Everything displayed is part of the final product, giving you a complete, actionable PESTLE assessment of CSG upon checkout.