China CSSC Holdings Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

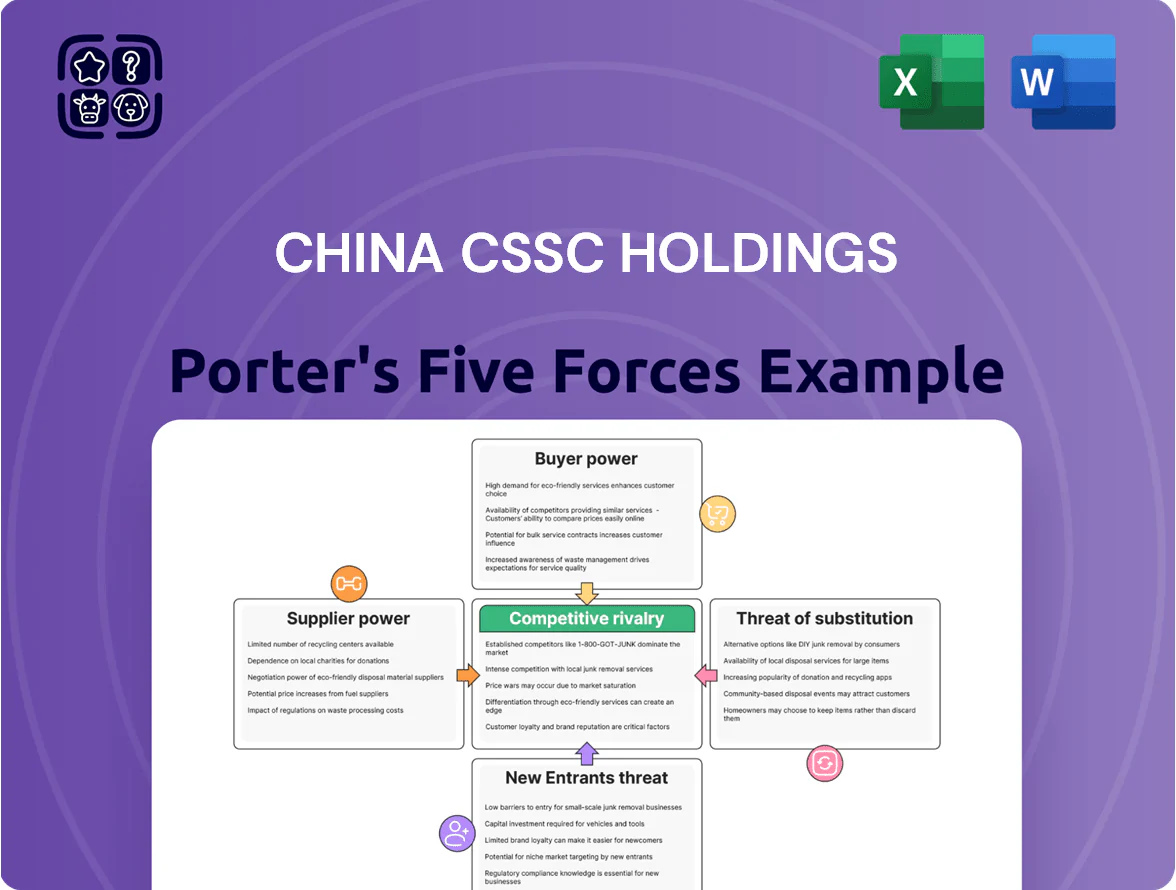

China CSSC Holdings operates in a capital-intensive shipbuilding sector where supplier relationships, state-linked competitive dynamics, and technological barriers shape its bargaining power and profitability.

Rising global trade volatility and green-shipping regulations increase competitive intensity and substitution risks from alternative transport modes and retrofitting solutions.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore China CSSC Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility in marine grade steel prices

The cost of marine-grade steel, which makes up roughly 30–40% of new-vessel build costs, directly squeezes CSSC Holdings’ margins; in 2024 steel accounted for an estimated CNY 18–24 billion of input costs across shipyards.

CSSC’s scale and sites near major Chinese mills lower procurement costs, but iron ore price swings—iron ore CFR China rose ~12% in 2024—keep expenses unpredictable.

By end-2025 CSSC had shifted ~40–60% of projected steel needs into multi-year hedges, cutting short-term volatility; still, dependence on specialized high-tensile steel remains a material supplier risk.

Dependence on high-tech propulsion components

As shipbuilding shifts to dual-fuel and ammonia-ready engines, bargaining power of specialized propulsion suppliers has risen; about 70% of advanced dual-fuel engine patents are held by three global vendors, tightening supply and pricing power in 2024.

CSSC Holdings (China State Shipbuilding Corporation) is investing CNY 4.2 billion in domestic R&D through 2025 to localize key propulsion IP and certifications, aiming to cut foreign supplier share from ~60% to under 30% by 2028.

Despite this, immediate production timelines remain tied to availability of certified systems, with lead times for ammonia-ready engines averaging 9–14 months in 2024, so supplier constraints still drive scheduling and margins.

Strategic integration with state-owned entities

CSSC benefits from deep ties to state-owned enterprises, giving it stable supply lines and preferential access to steel and ship components—state suppliers provided roughly 60% of inputs in 2024, lowering procurement volatility.

Vertical integration also secures better credit: CSSC’s group-linked financing helped cut weighted average borrowing costs by about 80 basis points versus domestic private peers in 2024.

Still, procurement and investment choices can follow national industrial policy; during 2023–24, 30% of new orders were aligned with government strategic directives, sometimes reducing market-cost efficiency.

Scarcity of specialized maritime labor

Energy costs and environmental compliance

Suppliers of energy and utility services have grown leverage as China CSSC Holdings faces stricter emissions rules and a national carbon price that averaged about CNY 60/ton CO2 in 2024, raising operating costs for shipyards.

Green manufacturing needs more electricity for electrified processes; a 15% rise in industrial power tariffs would cut 2025 EBITDA by an estimated 3–4% on current margins.

The company is testing onsite solar and battery projects targeting 50 MW by 2027 to hedge supplier power risk.

- Carbon price ~CNY 60/ton (2024)

- 15% tariff rise → EBITDA −3–4%

- Onsite renewables target 50 MW by 2027

Suppliers Drive Cost Risk: Steel, Engine OEMs & Carbon Pricing Squeeze Margins

Suppliers wield moderate-to-high power: steel (30–40% of build costs; CNY 18–24bn in 2024) and three engine OEMs (70% dual-fuel patents) drive price and lead-time risk, partially offset by CSSC’s state-linked procurement (60% inputs) and 40–60% multi‑year steel hedges by end‑2025; skilled labor hikes (6–8% y/y) and carbon price (~CNY 60/t in 2024) add pressure.

| Metric | 2024/2025 |

|---|---|

| Steel cost share | 30–40% |

| Steel input CNY | 18–24bn (2024) |

| Dual‑fuel patents (3 firms) | ~70% |

| State supplier share | ~60% |

| Steel hedged | 40–60% (end‑2025) |

| Skilled labor growth | 6–8% y/y |

| Carbon price | ~CNY 60/t |

What is included in the product

Tailored Porter’s Five Forces analysis for China CSSC Holdings that uncovers competitive intensity, buyer and supplier bargaining power, entry barriers, substitute threats, and regulatory/disruptive risks—designed for direct use in investor decks, strategy reports, or academic work.

A concise Porter's Five Forces one-sheet for China CSSC Holdings—quickly spot supplier, buyer, and competitive pressures to streamline strategic decisions.

Customers Bargaining Power

Consolidation of global shipping alliances

The consolidation of global shipping into three major alliances (THE Alliance, 2M, Ocean Alliance) gives buyers heavy leverage; in 2024 the top 10 liner companies accounted for ~75% of container capacity, letting them demand price cuts and preferred financing when placing fleet orders.

These alliances placed bulk orders worth over $30bn in 2023–24, pressuring shipbuilders like China CSSC Holdings to offer lower unit prices and extended payment terms to win contracts.

CSSC must balance these high-volume deals with margin preservation across a $20–25bn diversified order book, or risk margin erosion on smaller commercial and naval projects.

Strong demand for green vessel replacement

By end-2025, stricter IMO decarbonization rules shifted pricing power to shipbuilders like CSSC, as buyers pay 8–15% premiums for high-efficiency LNG and methanol ships and accept firmer delivery terms; Clarksons estimated green-fuel newbuild orders rose 42% in 2024–25.

CSSC’s certified LNG/methanol designs and 18–24 month guaranteed slots let it prioritize higher-margin contracts, raising gross margins on such builds by roughly 200–350 bps versus conventional vessels.

Even large buyers face scarcity: orderbooks for dual-fuel tankers reached 14% of global tanker newbuilds in 2025, so CSSC can reject low-margin bids and focus on repeat customers with long-term charters.

Cyclical nature of the maritime industry

The bargaining power of customers swings with the shipping cycle: when global freight rates surged—average container rates jumped ~260% in 2020–2021 and stayed elevated into 2022—buyers rushed for ship repairs and newbuild slots, cutting their leverage and letting CSSC raise prices; in 2023–2024 rates fell ~40% from peaks, forcing CSSC to offer discounts and flexible scheduling to fill dry docks and preserve cash flow, with utilization key to margins.

Availability of alternative global shipyards

Customers can shift orders to South Korea’s major yards or emerging Southeast Asian shipbuilders, keeping CSSC’s pricing under pressure; South Korea held about 36% of global shipyard newbuilding value in 2024 vs China’s 28% per Clarksons Research.

Global price transparency lets buyers benchmark CSSC quotes easily, reducing margin flexibility; reported global newbuild contract values averaged $70–90m for mid-size bulk carriers in 2024.

CSSC counters by bundling lifecycle repair and MRO services to boost stickiness—aftermarket services made up roughly 15–20% of Chinese shipyards’ revenue in 2023, raising customer switching costs.

- Rival share: South Korea ~36%, China ~28% (2024)

- Benchmark: mid-size newbuilds $70–90m (2024)

- Aftermarket revenue: 15–20% (2023)

Influence of financing and credit terms

Large-scale ship buyers need complex financing; their access to capital often decides sale terms, so buyers exert strong price pressure.

CSSC partners with state-affiliated banks like Bank of China and China Development Bank to offer low-rate, long-tenor loans; in 2024 CSSC-backed financing reportedly covered >40% of some LNG carrier deals, shifting negotiations in CSSC’s favor.

Providing below-market financing and export-credit support reduces price sensitivity and pressures rival yards to match terms, effectively lowering customer bargaining power.

- State-bank financing covers >40% of select 2024 deals

- Lower rates/longer tenors tilt buyer choice toward CSSC

- Financing often trumps sticker price in final decision

Buyers' leverage forces cuts as green orders lift CSSC margins and state-backed deals surge

Buyers hold strong leverage via three alliances and top liners (~75% capacity in 2024), forcing price cuts; CSSC faced >$30bn alliance orders in 2023–24 and balanced a $20–25bn orderbook. Green rules shifted 8–15% premiums to shipbuilders; green orders rose 42% in 2024–25, letting CSSC capture +200–350bps margins on LNG/methanol builds. State-backed financing covered >40% of select 2024 deals, lowering buyer price sensitivity.

| Metric | 2024–25 |

|---|---|

| Top-10 capacity | ~75% |

| Alliance orders | >$30bn |

| CSSC orderbook | $20–25bn |

| Green order growth | +42% |

| Green premium | 8–15% |

| Margin uplift | +200–350bps |

| State financing | >40% deals |

Preview Before You Purchase

China CSSC Holdings Porter's Five Forces Analysis

This preview shows the exact China CSSC Holdings Porter’s Five Forces analysis you’ll receive immediately after purchase—fully formatted, professional, and ready to download with no placeholders or samples.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

China CSSC Holdings operates in a capital-intensive shipbuilding sector where supplier relationships, state-linked competitive dynamics, and technological barriers shape its bargaining power and profitability.

Rising global trade volatility and green-shipping regulations increase competitive intensity and substitution risks from alternative transport modes and retrofitting solutions.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore China CSSC Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility in marine grade steel prices

The cost of marine-grade steel, which makes up roughly 30–40% of new-vessel build costs, directly squeezes CSSC Holdings’ margins; in 2024 steel accounted for an estimated CNY 18–24 billion of input costs across shipyards.

CSSC’s scale and sites near major Chinese mills lower procurement costs, but iron ore price swings—iron ore CFR China rose ~12% in 2024—keep expenses unpredictable.

By end-2025 CSSC had shifted ~40–60% of projected steel needs into multi-year hedges, cutting short-term volatility; still, dependence on specialized high-tensile steel remains a material supplier risk.

Dependence on high-tech propulsion components

As shipbuilding shifts to dual-fuel and ammonia-ready engines, bargaining power of specialized propulsion suppliers has risen; about 70% of advanced dual-fuel engine patents are held by three global vendors, tightening supply and pricing power in 2024.

CSSC Holdings (China State Shipbuilding Corporation) is investing CNY 4.2 billion in domestic R&D through 2025 to localize key propulsion IP and certifications, aiming to cut foreign supplier share from ~60% to under 30% by 2028.

Despite this, immediate production timelines remain tied to availability of certified systems, with lead times for ammonia-ready engines averaging 9–14 months in 2024, so supplier constraints still drive scheduling and margins.

Strategic integration with state-owned entities

CSSC benefits from deep ties to state-owned enterprises, giving it stable supply lines and preferential access to steel and ship components—state suppliers provided roughly 60% of inputs in 2024, lowering procurement volatility.

Vertical integration also secures better credit: CSSC’s group-linked financing helped cut weighted average borrowing costs by about 80 basis points versus domestic private peers in 2024.

Still, procurement and investment choices can follow national industrial policy; during 2023–24, 30% of new orders were aligned with government strategic directives, sometimes reducing market-cost efficiency.

Scarcity of specialized maritime labor

Energy costs and environmental compliance

Suppliers of energy and utility services have grown leverage as China CSSC Holdings faces stricter emissions rules and a national carbon price that averaged about CNY 60/ton CO2 in 2024, raising operating costs for shipyards.

Green manufacturing needs more electricity for electrified processes; a 15% rise in industrial power tariffs would cut 2025 EBITDA by an estimated 3–4% on current margins.

The company is testing onsite solar and battery projects targeting 50 MW by 2027 to hedge supplier power risk.

- Carbon price ~CNY 60/ton (2024)

- 15% tariff rise → EBITDA −3–4%

- Onsite renewables target 50 MW by 2027

Suppliers Drive Cost Risk: Steel, Engine OEMs & Carbon Pricing Squeeze Margins

Suppliers wield moderate-to-high power: steel (30–40% of build costs; CNY 18–24bn in 2024) and three engine OEMs (70% dual-fuel patents) drive price and lead-time risk, partially offset by CSSC’s state-linked procurement (60% inputs) and 40–60% multi‑year steel hedges by end‑2025; skilled labor hikes (6–8% y/y) and carbon price (~CNY 60/t in 2024) add pressure.

| Metric | 2024/2025 |

|---|---|

| Steel cost share | 30–40% |

| Steel input CNY | 18–24bn (2024) |

| Dual‑fuel patents (3 firms) | ~70% |

| State supplier share | ~60% |

| Steel hedged | 40–60% (end‑2025) |

| Skilled labor growth | 6–8% y/y |

| Carbon price | ~CNY 60/t |

What is included in the product

Tailored Porter’s Five Forces analysis for China CSSC Holdings that uncovers competitive intensity, buyer and supplier bargaining power, entry barriers, substitute threats, and regulatory/disruptive risks—designed for direct use in investor decks, strategy reports, or academic work.

A concise Porter's Five Forces one-sheet for China CSSC Holdings—quickly spot supplier, buyer, and competitive pressures to streamline strategic decisions.

Customers Bargaining Power

Consolidation of global shipping alliances

The consolidation of global shipping into three major alliances (THE Alliance, 2M, Ocean Alliance) gives buyers heavy leverage; in 2024 the top 10 liner companies accounted for ~75% of container capacity, letting them demand price cuts and preferred financing when placing fleet orders.

These alliances placed bulk orders worth over $30bn in 2023–24, pressuring shipbuilders like China CSSC Holdings to offer lower unit prices and extended payment terms to win contracts.

CSSC must balance these high-volume deals with margin preservation across a $20–25bn diversified order book, or risk margin erosion on smaller commercial and naval projects.

Strong demand for green vessel replacement

By end-2025, stricter IMO decarbonization rules shifted pricing power to shipbuilders like CSSC, as buyers pay 8–15% premiums for high-efficiency LNG and methanol ships and accept firmer delivery terms; Clarksons estimated green-fuel newbuild orders rose 42% in 2024–25.

CSSC’s certified LNG/methanol designs and 18–24 month guaranteed slots let it prioritize higher-margin contracts, raising gross margins on such builds by roughly 200–350 bps versus conventional vessels.

Even large buyers face scarcity: orderbooks for dual-fuel tankers reached 14% of global tanker newbuilds in 2025, so CSSC can reject low-margin bids and focus on repeat customers with long-term charters.

Cyclical nature of the maritime industry

The bargaining power of customers swings with the shipping cycle: when global freight rates surged—average container rates jumped ~260% in 2020–2021 and stayed elevated into 2022—buyers rushed for ship repairs and newbuild slots, cutting their leverage and letting CSSC raise prices; in 2023–2024 rates fell ~40% from peaks, forcing CSSC to offer discounts and flexible scheduling to fill dry docks and preserve cash flow, with utilization key to margins.

Availability of alternative global shipyards

Customers can shift orders to South Korea’s major yards or emerging Southeast Asian shipbuilders, keeping CSSC’s pricing under pressure; South Korea held about 36% of global shipyard newbuilding value in 2024 vs China’s 28% per Clarksons Research.

Global price transparency lets buyers benchmark CSSC quotes easily, reducing margin flexibility; reported global newbuild contract values averaged $70–90m for mid-size bulk carriers in 2024.

CSSC counters by bundling lifecycle repair and MRO services to boost stickiness—aftermarket services made up roughly 15–20% of Chinese shipyards’ revenue in 2023, raising customer switching costs.

- Rival share: South Korea ~36%, China ~28% (2024)

- Benchmark: mid-size newbuilds $70–90m (2024)

- Aftermarket revenue: 15–20% (2023)

Influence of financing and credit terms

Large-scale ship buyers need complex financing; their access to capital often decides sale terms, so buyers exert strong price pressure.

CSSC partners with state-affiliated banks like Bank of China and China Development Bank to offer low-rate, long-tenor loans; in 2024 CSSC-backed financing reportedly covered >40% of some LNG carrier deals, shifting negotiations in CSSC’s favor.

Providing below-market financing and export-credit support reduces price sensitivity and pressures rival yards to match terms, effectively lowering customer bargaining power.

- State-bank financing covers >40% of select 2024 deals

- Lower rates/longer tenors tilt buyer choice toward CSSC

- Financing often trumps sticker price in final decision

Buyers' leverage forces cuts as green orders lift CSSC margins and state-backed deals surge

Buyers hold strong leverage via three alliances and top liners (~75% capacity in 2024), forcing price cuts; CSSC faced >$30bn alliance orders in 2023–24 and balanced a $20–25bn orderbook. Green rules shifted 8–15% premiums to shipbuilders; green orders rose 42% in 2024–25, letting CSSC capture +200–350bps margins on LNG/methanol builds. State-backed financing covered >40% of select 2024 deals, lowering buyer price sensitivity.

| Metric | 2024–25 |

|---|---|

| Top-10 capacity | ~75% |

| Alliance orders | >$30bn |

| CSSC orderbook | $20–25bn |

| Green order growth | +42% |

| Green premium | 8–15% |

| Margin uplift | +200–350bps |

| State financing | >40% deals |

Preview Before You Purchase

China CSSC Holdings Porter's Five Forces Analysis

This preview shows the exact China CSSC Holdings Porter’s Five Forces analysis you’ll receive immediately after purchase—fully formatted, professional, and ready to download with no placeholders or samples.