CS Wind Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

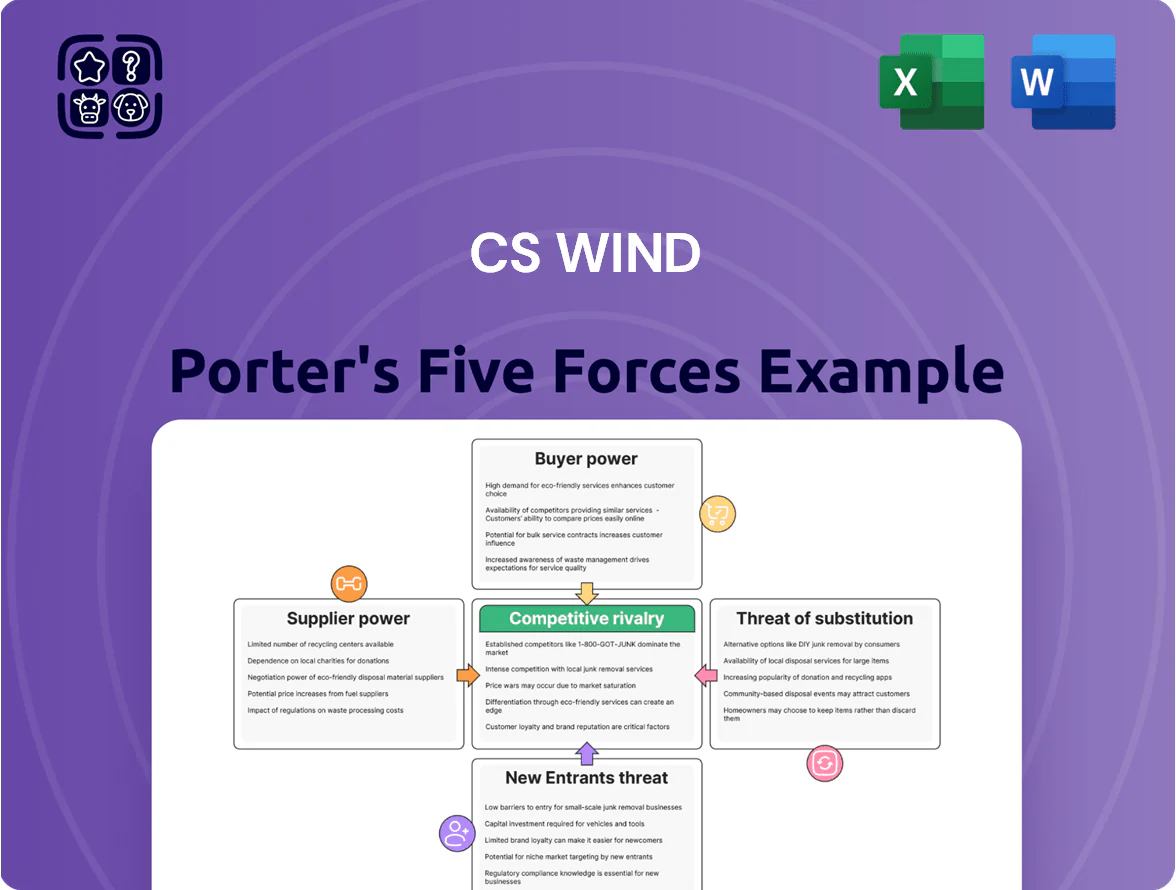

CS Wind faces mixed pressures: strong supplier influence for specialized components, rising buyer sophistication from utility-scale developers, and moderate new-entrant threats as manufacturing scale remains a barrier; substitutes are limited but technological disruption looms.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore CS Wind’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Price Volatility

Raw material price volatility poses a strong supplier power risk for CS Wind because high-grade steel plates make up about 45–55% of tower manufacturing cost; in 2024 global hot-rolled coil prices averaged roughly $860/ton, swinging ±20% year-over-year due to iron ore moves and tariffs. Suppliers gain leverage during spikes, compressing CS Wind margins unless costs are passed on. CS Wind should use diversified sourcing, multi-year contracts, and index-linked pass-through clauses to protect EBITDA. In 2025, a 10% steel price rise could cut tower gross margin by ~3–4 percentage points.

Specialized Logistics and Transportation

Specialized heavy-lift vessels and land rigs for moving massive offshore wind tower sections are scarce—global fleet capacity for wind turbine installation vessels totaled about 60 units in 2024—so logistics providers command strong supplier power over CS Wind; with few alternatives, a 10–20% shortage in transport capacity can delay deliveries by weeks and raise per-tower transport costs by an estimated $30k–$80k, squeezing margins and project timelines.

Energy Intensive Manufacturing Requirements

CS Wind's rolling, welding, and coating operations consume large power and gas; industrial steel processes can use 1–3 MWh per tonne and ≥100 GJ/tonne of thermal energy, so energy costs can be 10–20% of manufacturing OPEX.

Factories sit on local utility grids or single suppliers in markets like Vietnam, Turkey, and Poland, giving regional energy providers near-monopoly pricing power.

That dependence exposed CS Wind in 2022–2023 when European gas prices spiked over 400% year-on-year, showing suppliers can force price hikes with little room to negotiate.

Concentration of Certified Steel Mills

Only a handful of global steel mills can make the ultra-thick, high-strength steel for newest offshore turbines; about 4–6 certified mills service top OEMs as of 2025, narrowing CS Wind’s supplier pool.

These mills undergo OEM certification and audits, so qualified capacity is limited; during 2023–25 offshore build peaks, premiums of 8–15% and lead times of 30–48 weeks were common.

Concentration gives mills pricing power and control over delivery schedules, raising CS Wind’s procurement cost and schedule risk during demand spikes.

- 4–6 certified mills globally (2025)

- Premiums 8–15% in 2023–25

- Lead times 30–48 weeks at peaks

- Certification needs restrict switching

Technical Component Specialization

CS Wind faces supplier power from specialized internal tower components—elevators, high-tension bolts, and electrical systems—often produced by niche firms with patents or de facto technical standards tied to turbine OEMs.

These suppliers can charge premiums; global specialty fastener margins reached ~12–15% in 2024, and proprietary elevator modules add 5–8% to tower BOM (bill of materials), raising switching costs.

As a result, CS Wind risks non-compliance and warranty exposure if it swaps vendors, creating functional dependence that limits negotiation leverage.

- Patent-locked subcomponents

- Switching raises warranty/non-compliance risk

- Specialty margins 12–15% (2024)

- Elevator modules +5–8% of tower BOM

Supplier bottlenecks: steel, vessels & premiums squeeze tower margins and raise costs

Suppliers exert strong power: 4–6 certified steel mills (2025) plus scarce heavy-lift vessels (≈60 units in 2024) and regional energy monopolies drive prices and lead times; steel (45–55% of tower cost) averaged $860/t in 2024 with ±20% swings, causing a 10% steel rise to cut gross margin ~3–4 ppt; transport shortages raise per-tower cost $30k–$80k; specialty parts add premiums 8–15% and elevate switching risk.

| Item | 2024–25 metric |

|---|---|

| Steel price (HRC) | $860/t ±20% |

| Certified mills | 4–6 (2025) |

| Vessels (global) | ≈60 units (2024) |

| Transport cost rise | $30k–$80k per tower |

| Steel share of cost | 45–55% |

| Specialty premiums | 8–15% |

What is included in the product

Tailored Porter's Five Forces assessment of CS Wind that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats to its wind-turbine component business, with strategic commentary for investors and management.

One-sheet Porter's Five Forces for CS Wind—quickly spot competitive pressures and relieve strategic uncertainty with a clean radar chart and editable pressure levels.

Customers Bargaining Power

Concentration of Major Turbine OEMs

The customer base for CS Wind is highly concentrated: Vestas, GE Renewable Energy, and Siemens Gamesa accounted for roughly 60–70% of group orders in 2024, giving them outsized leverage.

These OEMs can consolidate large-volume orders, pressuring CS Wind on unit prices; reported margin compression in 2024 showed gross margin fell to about 12–14% amid intense price negotiation.

The buyers also extract favorable payment terms and risk-sharing clauses, increasing CS Wind’s working capital needs and cash conversion cycle by several weeks in 2024.

Long Term Framework Agreements

Buyers tie CS Wind into long-term framework agreements that lock manufacturing capacity and shift price-stability risk to the supplier; in 2024 CS Wind reported backlog visibility of ~EUR 300m but contract clauses often cap price pass-through, squeezing margins.

Low Switching Costs for Standardized Sections

While offshore towers stay complex, onshore tower sections are standardized, so buyers can pick among global and regional makers; in 2024 the top 10 suppliers accounted for ~68% of onshore segment volume, easing supplier substitution. If CS Wind loses price competitiveness, OEMs can reallocate orders to peers like CS Wind’s rivals with similar quality scores, and procurement shifts of ±10–15% per year are common. This switching pressure keeps downward margin pressure; CS Wind’s 2024 gross margin for towers of ~12% vs industry peers at ~14–18% shows the impact.

Threat of Backward Integration

Large turbine OEMs like Siemens Gamesa and Vestas have capex and engineering to internalize tower production if supplier prices rise; in 2024 Vestas reported EUR 6.1bn capex guidance across 2023–25, showing scale to invest in captive supply.

That credible backward-integration threat caps CS Wind’s pricing power and forces sub-6% gross-margin competition in many contracts; independent makers must stay cost-competitive and flexible.

- OEMs’ capex scale (Vestas EUR 6.1bn 2023–25) enables insourcing

- Credible threat limits CS Wind pricing power

- Market pressure keeps independent tower margins tight (~<6%)

Sensitivity to Project Financing and LCOE

Wind farm developers are highly sensitive to Levelized Cost of Energy (LCOE) and interest rates; a 100 bp rise in rates can raise weighted average cost of capital by ~0.5–1.0 percentage points, pushing LCOE up 3–8% and triggering stronger price demands.

Higher capital costs force developers to extract discounts from turbine OEMs, who then pressure component suppliers like CS Wind, increasing supplier bargaining pressure and margin compression.

The developer’s balance-sheet health and project IRR directly set bargaining aggressiveness; projects with IRRs under target (often <6–8%) show the fiercest price pressure.

- 100 bp rate rise → LCOE +3–8%

- IRR target <6–8% → aggressive bargaining

- OEMs pass ~10–30% of price cuts to suppliers

OEMs squeeze suppliers: concentrated orders, margin hit, insourcing & rate risks

Customers (Vestas, GE, Siemens Gamesa) accounted for ~60–70% of CS Wind orders in 2024, giving them strong price and terms leverage; CS Wind gross margin fell to ~12–14% in 2024 as OEMs pushed price cuts and tougher payment terms. Buyers can switch suppliers (top‑10 onshore suppliers = ~68% volume) or insource—Vestas capex guidance EUR 6.1bn (2023–25) signals real backward‑integration risk; rate shocks (100bp) raise LCOE ~3–8%, intensifying buyer pressure and passing ~10–30% of cuts to suppliers.

| Metric | 2024 / Source |

|---|---|

| Customer concentration | 60–70% orders (Vestas/GE/Siemens) |

| CS Wind gross margin | ~12–14% |

| Top‑10 onshore suppliers | ~68% volume |

| Vestas capex (2023–25) | EUR 6.1bn |

| Rate shock impact | 100bp → LCOE +3–8% |

| OEM pass‑through to suppliers | ~10–30% |

Same Document Delivered

CS Wind Porter's Five Forces Analysis

This preview shows the exact CS Wind Porter’s Five Forces analysis document you'll receive immediately after purchase—no placeholders, no mockups.

The file displayed is the same professionally written, fully formatted report available for instant download once you complete your purchase.

What you see here is the complete, ready-to-use analysis—precisely the deliverable you’ll get, with no additional setup or customization required.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

CS Wind faces mixed pressures: strong supplier influence for specialized components, rising buyer sophistication from utility-scale developers, and moderate new-entrant threats as manufacturing scale remains a barrier; substitutes are limited but technological disruption looms.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore CS Wind’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Price Volatility

Raw material price volatility poses a strong supplier power risk for CS Wind because high-grade steel plates make up about 45–55% of tower manufacturing cost; in 2024 global hot-rolled coil prices averaged roughly $860/ton, swinging ±20% year-over-year due to iron ore moves and tariffs. Suppliers gain leverage during spikes, compressing CS Wind margins unless costs are passed on. CS Wind should use diversified sourcing, multi-year contracts, and index-linked pass-through clauses to protect EBITDA. In 2025, a 10% steel price rise could cut tower gross margin by ~3–4 percentage points.

Specialized Logistics and Transportation

Specialized heavy-lift vessels and land rigs for moving massive offshore wind tower sections are scarce—global fleet capacity for wind turbine installation vessels totaled about 60 units in 2024—so logistics providers command strong supplier power over CS Wind; with few alternatives, a 10–20% shortage in transport capacity can delay deliveries by weeks and raise per-tower transport costs by an estimated $30k–$80k, squeezing margins and project timelines.

Energy Intensive Manufacturing Requirements

CS Wind's rolling, welding, and coating operations consume large power and gas; industrial steel processes can use 1–3 MWh per tonne and ≥100 GJ/tonne of thermal energy, so energy costs can be 10–20% of manufacturing OPEX.

Factories sit on local utility grids or single suppliers in markets like Vietnam, Turkey, and Poland, giving regional energy providers near-monopoly pricing power.

That dependence exposed CS Wind in 2022–2023 when European gas prices spiked over 400% year-on-year, showing suppliers can force price hikes with little room to negotiate.

Concentration of Certified Steel Mills

Only a handful of global steel mills can make the ultra-thick, high-strength steel for newest offshore turbines; about 4–6 certified mills service top OEMs as of 2025, narrowing CS Wind’s supplier pool.

These mills undergo OEM certification and audits, so qualified capacity is limited; during 2023–25 offshore build peaks, premiums of 8–15% and lead times of 30–48 weeks were common.

Concentration gives mills pricing power and control over delivery schedules, raising CS Wind’s procurement cost and schedule risk during demand spikes.

- 4–6 certified mills globally (2025)

- Premiums 8–15% in 2023–25

- Lead times 30–48 weeks at peaks

- Certification needs restrict switching

Technical Component Specialization

CS Wind faces supplier power from specialized internal tower components—elevators, high-tension bolts, and electrical systems—often produced by niche firms with patents or de facto technical standards tied to turbine OEMs.

These suppliers can charge premiums; global specialty fastener margins reached ~12–15% in 2024, and proprietary elevator modules add 5–8% to tower BOM (bill of materials), raising switching costs.

As a result, CS Wind risks non-compliance and warranty exposure if it swaps vendors, creating functional dependence that limits negotiation leverage.

- Patent-locked subcomponents

- Switching raises warranty/non-compliance risk

- Specialty margins 12–15% (2024)

- Elevator modules +5–8% of tower BOM

Supplier bottlenecks: steel, vessels & premiums squeeze tower margins and raise costs

Suppliers exert strong power: 4–6 certified steel mills (2025) plus scarce heavy-lift vessels (≈60 units in 2024) and regional energy monopolies drive prices and lead times; steel (45–55% of tower cost) averaged $860/t in 2024 with ±20% swings, causing a 10% steel rise to cut gross margin ~3–4 ppt; transport shortages raise per-tower cost $30k–$80k; specialty parts add premiums 8–15% and elevate switching risk.

| Item | 2024–25 metric |

|---|---|

| Steel price (HRC) | $860/t ±20% |

| Certified mills | 4–6 (2025) |

| Vessels (global) | ≈60 units (2024) |

| Transport cost rise | $30k–$80k per tower |

| Steel share of cost | 45–55% |

| Specialty premiums | 8–15% |

What is included in the product

Tailored Porter's Five Forces assessment of CS Wind that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats to its wind-turbine component business, with strategic commentary for investors and management.

One-sheet Porter's Five Forces for CS Wind—quickly spot competitive pressures and relieve strategic uncertainty with a clean radar chart and editable pressure levels.

Customers Bargaining Power

Concentration of Major Turbine OEMs

The customer base for CS Wind is highly concentrated: Vestas, GE Renewable Energy, and Siemens Gamesa accounted for roughly 60–70% of group orders in 2024, giving them outsized leverage.

These OEMs can consolidate large-volume orders, pressuring CS Wind on unit prices; reported margin compression in 2024 showed gross margin fell to about 12–14% amid intense price negotiation.

The buyers also extract favorable payment terms and risk-sharing clauses, increasing CS Wind’s working capital needs and cash conversion cycle by several weeks in 2024.

Long Term Framework Agreements

Buyers tie CS Wind into long-term framework agreements that lock manufacturing capacity and shift price-stability risk to the supplier; in 2024 CS Wind reported backlog visibility of ~EUR 300m but contract clauses often cap price pass-through, squeezing margins.

Low Switching Costs for Standardized Sections

While offshore towers stay complex, onshore tower sections are standardized, so buyers can pick among global and regional makers; in 2024 the top 10 suppliers accounted for ~68% of onshore segment volume, easing supplier substitution. If CS Wind loses price competitiveness, OEMs can reallocate orders to peers like CS Wind’s rivals with similar quality scores, and procurement shifts of ±10–15% per year are common. This switching pressure keeps downward margin pressure; CS Wind’s 2024 gross margin for towers of ~12% vs industry peers at ~14–18% shows the impact.

Threat of Backward Integration

Large turbine OEMs like Siemens Gamesa and Vestas have capex and engineering to internalize tower production if supplier prices rise; in 2024 Vestas reported EUR 6.1bn capex guidance across 2023–25, showing scale to invest in captive supply.

That credible backward-integration threat caps CS Wind’s pricing power and forces sub-6% gross-margin competition in many contracts; independent makers must stay cost-competitive and flexible.

- OEMs’ capex scale (Vestas EUR 6.1bn 2023–25) enables insourcing

- Credible threat limits CS Wind pricing power

- Market pressure keeps independent tower margins tight (~<6%)

Sensitivity to Project Financing and LCOE

Wind farm developers are highly sensitive to Levelized Cost of Energy (LCOE) and interest rates; a 100 bp rise in rates can raise weighted average cost of capital by ~0.5–1.0 percentage points, pushing LCOE up 3–8% and triggering stronger price demands.

Higher capital costs force developers to extract discounts from turbine OEMs, who then pressure component suppliers like CS Wind, increasing supplier bargaining pressure and margin compression.

The developer’s balance-sheet health and project IRR directly set bargaining aggressiveness; projects with IRRs under target (often <6–8%) show the fiercest price pressure.

- 100 bp rate rise → LCOE +3–8%

- IRR target <6–8% → aggressive bargaining

- OEMs pass ~10–30% of price cuts to suppliers

OEMs squeeze suppliers: concentrated orders, margin hit, insourcing & rate risks

Customers (Vestas, GE, Siemens Gamesa) accounted for ~60–70% of CS Wind orders in 2024, giving them strong price and terms leverage; CS Wind gross margin fell to ~12–14% in 2024 as OEMs pushed price cuts and tougher payment terms. Buyers can switch suppliers (top‑10 onshore suppliers = ~68% volume) or insource—Vestas capex guidance EUR 6.1bn (2023–25) signals real backward‑integration risk; rate shocks (100bp) raise LCOE ~3–8%, intensifying buyer pressure and passing ~10–30% of cuts to suppliers.

| Metric | 2024 / Source |

|---|---|

| Customer concentration | 60–70% orders (Vestas/GE/Siemens) |

| CS Wind gross margin | ~12–14% |

| Top‑10 onshore suppliers | ~68% volume |

| Vestas capex (2023–25) | EUR 6.1bn |

| Rate shock impact | 100bp → LCOE +3–8% |

| OEM pass‑through to suppliers | ~10–30% |

Same Document Delivered

CS Wind Porter's Five Forces Analysis

This preview shows the exact CS Wind Porter’s Five Forces analysis document you'll receive immediately after purchase—no placeholders, no mockups.

The file displayed is the same professionally written, fully formatted report available for instant download once you complete your purchase.

What you see here is the complete, ready-to-use analysis—precisely the deliverable you’ll get, with no additional setup or customization required.