CTBC Holding Porter's Five Forces Analysis

From Overview to Strategy Blueprint

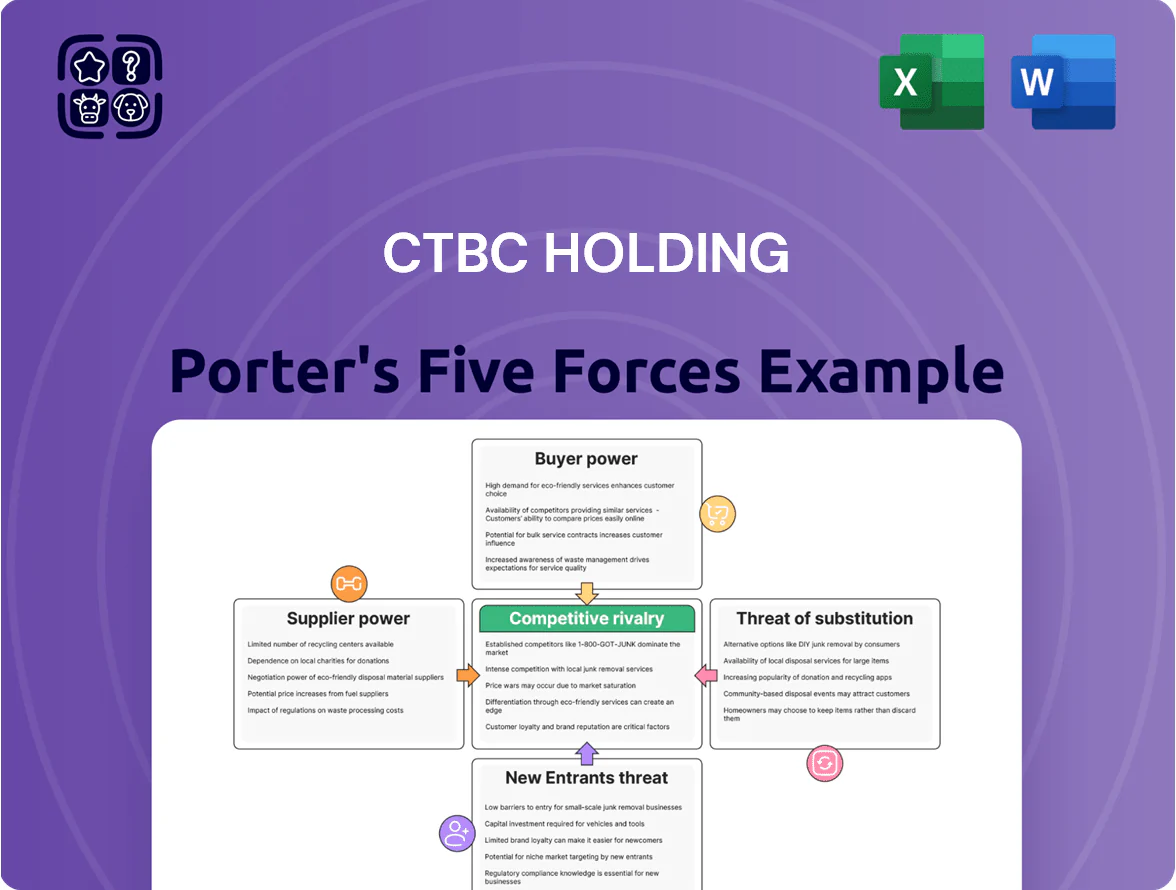

CTBC Holding faces moderate competitive intensity with strong brand loyalty and regulatory barriers that limit new entrants, yet digital disruption and margin pressure from larger banks remain key risks.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore CTBC Holding’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Access to Diverse Funding Sources

The primary suppliers for CTBC Holding are retail depositors and institutional lenders funding loans; depositors' bargaining power is low due to a fragmented retail base and fewer high-yield options, keeping core deposit rates down—CTBC reported NT$2.1 trillion in customer deposits in 2024, supporting stable low-cost funding.

Institutional wholesale lenders have higher leverage, pushing for competitive pricing tied to global liquidity and CTBC’s credit profile; CTBC’s 2024 CET1 ratio was about 13.8%, helping preserve access to wholesale markets.

CTBC’s strong Taiwanese brand and branch network sustain steady low-cost core deposits—retail deposit share remained roughly 68% of total funding in 2024—mitigating supplier pressure despite occasional market volatility.

Reliance on Specialized Technology Providers

CTBC’s shift to AI-driven banking makes it dependent on global vendors for cloud, cybersecurity, and core systems; major cloud providers and fintech firms wield power because migrating these platforms can cost tens of millions and take 12–24 months. By 2025, integrating generative AI into customer service and risk systems raised supplier leverage as these partnerships affect ~15–25% of IT spend. CTBC limits that power via multi-vendor sourcing and proprietary middle-layer software to cut switching time and costs.

Competition for High-Skilled Human Capital

The supply of specialists in data science, cybersecurity, and international wealth management is scarce; Taiwan's tech-fin talent gap widened in 2024 with a 12% year-on-year rise in demand for data engineers, pushing median salaries up 15% to NT$1.2M annually for senior roles.

As CTBC competes with Big Tech and regional banks in Singapore—where cybersecurity salaries average SGD 140k—bargaining power of talent stays high.

CTBC must offer pay premiums, equity-like incentives, and structured upskilling to retain staff during its digital transformation.

This sustained salary pressure increased CTBC's HR expense ratio by about 0.4 percentage points in 2024, and remains a key OPEX planning risk.

Regulatory Influence as a Quasi-Supplier

Regulators and central banks act as quasi-suppliers by setting capital adequacy and reserve rules that control CTBC Holding’s lendable funds and compliance costs.

As of 2025, higher ESG reporting mandates and stricter digital-banking rules raise compliance spend and steer product strategy, tightening regulators’ influence on CTBC’s risk appetite.

- 2025 capital ratio floors raise CET1 pressure

- Reserve requirements cut lendable liquidity

- ESG reporting demands boost compliance costs

- Digital rules force tech and product changes

Interbank Market and Liquidity Providers

CTBC uses the interbank market for short-term funding, so supplier power from large banks can spike in volatility or tighter policy, raising borrowing costs and squeezing net interest margins.

CTBC counters this with a Liquidity Coverage Ratio above 160% in 2024 and liquid assets (T-bills, repos) making up ~22% of total assets; real-time gross settlement adoption by 2025 sped funding, but major global banks still sway cross-border funding costs.

- Liquidity Coverage Ratio: >160% (2024)

- Liquid assets: ~22% of assets

- Real-time settlement: integrated by 2025

- Counterparty concentration: elevated in international funding

Stable retail funding and strong liquidity cushion amid rising IT, HR and regulatory costs

Suppliers (depositors, wholesale lenders, tech vendors, talent, regulators) exert mixed power: retail deposit power low—NT$2.1T deposits (2024), 68% retail share; CET1 ~13.8% (2024) keeps wholesale access; IT/talent supply raises IT spend 15–25% and HR costs +0.4pp; LCR >160% and liquid assets ~22% cushion funding shocks; 2025 rules raise compliance and capital pressure.

| Metric | Value |

|---|---|

| Customer deposits (2024) | NT$2.1T |

| Retail funding share | 68% |

| CET1 (2024) | 13.8% |

| LCR (2024) | >160% |

| Liquid assets | ~22% of assets |

What is included in the product

Tailored Porter's Five Forces analysis for CTBC Holding that uncovers key competitive drivers, evaluates buyer and supplier power, assesses entry barriers and substitute threats, and identifies disruptive forces and strategic levers to protect market share.

A concise Porter's Five Forces one-sheet for CTBC Holding—instantly highlights competitive pressures and strategic levers for faster, board-ready decisions.

Customers Bargaining Power

Low Switching Costs in Retail Banking

Individual retail customers in Taiwan face low switching costs due to a mature financial ecosystem and ubiquitous digital banking apps; 2024 data show 82% smartphone banking penetration and 68% active multi-bank users, so customers can move funds and change primary banks with minimal effort.

By late 2025 CTBC confronts high customer power as clients demand better digital UX and lower fees; in response CTBC is linking banking, lifestyle platforms, and retail rewards to raise stickiness and reduce churn.

Price Sensitivity in Corporate Lending

Large corporate clients wield strong bargaining power in corporate lending, sourcing roughly 30–40% of Taiwan issuers’ external funding from international markets in 2024 and frequently running multi-bank auctions to push spreads down 20–80 bps; CTBC counters by bundling supply-chain finance, cash management and cross-border advisory to retain deals. By 2025 CTBC layers data-driven analytics and client-level pricing to justify 10–25 bps premiums on bespoke solutions.

Transparency Driven by Digital Comparison Tools

The rise of aggregator platforms and AI comparison tools gives customers real-time rates on loans, insurance, and fees, raising transparency and bargaining power; 2025 surveys show 62% of Taiwanese consumers use comparison apps for financial products. This forces CTBC Holding to keep competitive pricing across deposits, loans, and wealth fees or risk share loss to aggressive rivals. Better-informed customers now negotiate terms or switch for short-term promos, and CTBC spent NT$2.1 billion in 2024–2025 on personalized marketing and targeted promotions to preempt churn.

High Expectations for Integrated Financial Services

Wealth and institutional clients demand a one-stop shop across banking, insurance, and securities, pushing CTBC to bundle services and assign dedicated relationship managers; HNW clients (top 5% of assets) often demand bespoke portfolios. As of 2025 CTBC reports cross-sell ratio improvements—group AUM rose ~6.2% YoY to NT$2.3 trillion—supporting retention. Still, lacking a unified digital asset view risks migration to fintech-forward rivals with superior UX.

- Dedicated RMs: expected by HNW clients

- 2025 group AUM: ~NT$2.3 trillion (+6.2% YoY)

- Cross-sell key to churn defence

- Poor unified digital view → higher defection risk

Influence of Institutional Investors and ESG Demands

Institutional clients—pension funds and asset managers holding >NT$3.5 trillion in Taiwanese mandates—now make ESG transparency a lock-in condition, shifting allocations if CTBC misses benchmarks.

By 2025 ESG scores and green loan share (now 18% of CTBC Group’s corporate book) are core to value for institutions; failure to meet targets risks multi-percentage-point fund outflows.

CTBC must update lending and investment policies, report on Scope 1–3 emissions, and hit green financing targets to retain mandates.

- Institutional leverage: large, concentrated mandates >NT$3.5T

- 2025 reality: ESG central to institutional value

- CTBC green loans ≈18% corporate book

- Risk: portfolio reallocation, multi-pp outflows

High customer power: digital-savvy, multi-bank users drive CTBC retention and green growth

Customers hold high bargaining power: 82% smartphone banking penetration (2024), 68% multi-bank users, 62% use comparison apps (2025), HNW cross-sell raised AUM to NT$2.3T (+6.2% YoY), green loans ≈18% of corporate book; CTBC spends NT$2.1B (2024–25) on personalized marketing to retain clients.

| Metric | Value |

|---|---|

| Smartphone banking | 82% (2024) |

| Multi-bank users | 68% (2024) |

| Comparison app use | 62% (2025) |

| Group AUM | NT$2.3T (+6.2% YoY, 2025) |

| Green loans | 18% corporate book (2025) |

| Retention spend | NT$2.1B (2024–25) |

Full Version Awaits

CTBC Holding Porter's Five Forces Analysis

This preview shows the exact CTBC Holding Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups.

The document displayed here is fully formatted and ready for download the moment you buy, containing the same comprehensive competitive assessment and actionable insights.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

CTBC Holding faces moderate competitive intensity with strong brand loyalty and regulatory barriers that limit new entrants, yet digital disruption and margin pressure from larger banks remain key risks.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore CTBC Holding’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Access to Diverse Funding Sources

The primary suppliers for CTBC Holding are retail depositors and institutional lenders funding loans; depositors' bargaining power is low due to a fragmented retail base and fewer high-yield options, keeping core deposit rates down—CTBC reported NT$2.1 trillion in customer deposits in 2024, supporting stable low-cost funding.

Institutional wholesale lenders have higher leverage, pushing for competitive pricing tied to global liquidity and CTBC’s credit profile; CTBC’s 2024 CET1 ratio was about 13.8%, helping preserve access to wholesale markets.

CTBC’s strong Taiwanese brand and branch network sustain steady low-cost core deposits—retail deposit share remained roughly 68% of total funding in 2024—mitigating supplier pressure despite occasional market volatility.

Reliance on Specialized Technology Providers

CTBC’s shift to AI-driven banking makes it dependent on global vendors for cloud, cybersecurity, and core systems; major cloud providers and fintech firms wield power because migrating these platforms can cost tens of millions and take 12–24 months. By 2025, integrating generative AI into customer service and risk systems raised supplier leverage as these partnerships affect ~15–25% of IT spend. CTBC limits that power via multi-vendor sourcing and proprietary middle-layer software to cut switching time and costs.

Competition for High-Skilled Human Capital

The supply of specialists in data science, cybersecurity, and international wealth management is scarce; Taiwan's tech-fin talent gap widened in 2024 with a 12% year-on-year rise in demand for data engineers, pushing median salaries up 15% to NT$1.2M annually for senior roles.

As CTBC competes with Big Tech and regional banks in Singapore—where cybersecurity salaries average SGD 140k—bargaining power of talent stays high.

CTBC must offer pay premiums, equity-like incentives, and structured upskilling to retain staff during its digital transformation.

This sustained salary pressure increased CTBC's HR expense ratio by about 0.4 percentage points in 2024, and remains a key OPEX planning risk.

Regulatory Influence as a Quasi-Supplier

Regulators and central banks act as quasi-suppliers by setting capital adequacy and reserve rules that control CTBC Holding’s lendable funds and compliance costs.

As of 2025, higher ESG reporting mandates and stricter digital-banking rules raise compliance spend and steer product strategy, tightening regulators’ influence on CTBC’s risk appetite.

- 2025 capital ratio floors raise CET1 pressure

- Reserve requirements cut lendable liquidity

- ESG reporting demands boost compliance costs

- Digital rules force tech and product changes

Interbank Market and Liquidity Providers

CTBC uses the interbank market for short-term funding, so supplier power from large banks can spike in volatility or tighter policy, raising borrowing costs and squeezing net interest margins.

CTBC counters this with a Liquidity Coverage Ratio above 160% in 2024 and liquid assets (T-bills, repos) making up ~22% of total assets; real-time gross settlement adoption by 2025 sped funding, but major global banks still sway cross-border funding costs.

- Liquidity Coverage Ratio: >160% (2024)

- Liquid assets: ~22% of assets

- Real-time settlement: integrated by 2025

- Counterparty concentration: elevated in international funding

Stable retail funding and strong liquidity cushion amid rising IT, HR and regulatory costs

Suppliers (depositors, wholesale lenders, tech vendors, talent, regulators) exert mixed power: retail deposit power low—NT$2.1T deposits (2024), 68% retail share; CET1 ~13.8% (2024) keeps wholesale access; IT/talent supply raises IT spend 15–25% and HR costs +0.4pp; LCR >160% and liquid assets ~22% cushion funding shocks; 2025 rules raise compliance and capital pressure.

| Metric | Value |

|---|---|

| Customer deposits (2024) | NT$2.1T |

| Retail funding share | 68% |

| CET1 (2024) | 13.8% |

| LCR (2024) | >160% |

| Liquid assets | ~22% of assets |

What is included in the product

Tailored Porter's Five Forces analysis for CTBC Holding that uncovers key competitive drivers, evaluates buyer and supplier power, assesses entry barriers and substitute threats, and identifies disruptive forces and strategic levers to protect market share.

A concise Porter's Five Forces one-sheet for CTBC Holding—instantly highlights competitive pressures and strategic levers for faster, board-ready decisions.

Customers Bargaining Power

Low Switching Costs in Retail Banking

Individual retail customers in Taiwan face low switching costs due to a mature financial ecosystem and ubiquitous digital banking apps; 2024 data show 82% smartphone banking penetration and 68% active multi-bank users, so customers can move funds and change primary banks with minimal effort.

By late 2025 CTBC confronts high customer power as clients demand better digital UX and lower fees; in response CTBC is linking banking, lifestyle platforms, and retail rewards to raise stickiness and reduce churn.

Price Sensitivity in Corporate Lending

Large corporate clients wield strong bargaining power in corporate lending, sourcing roughly 30–40% of Taiwan issuers’ external funding from international markets in 2024 and frequently running multi-bank auctions to push spreads down 20–80 bps; CTBC counters by bundling supply-chain finance, cash management and cross-border advisory to retain deals. By 2025 CTBC layers data-driven analytics and client-level pricing to justify 10–25 bps premiums on bespoke solutions.

Transparency Driven by Digital Comparison Tools

The rise of aggregator platforms and AI comparison tools gives customers real-time rates on loans, insurance, and fees, raising transparency and bargaining power; 2025 surveys show 62% of Taiwanese consumers use comparison apps for financial products. This forces CTBC Holding to keep competitive pricing across deposits, loans, and wealth fees or risk share loss to aggressive rivals. Better-informed customers now negotiate terms or switch for short-term promos, and CTBC spent NT$2.1 billion in 2024–2025 on personalized marketing and targeted promotions to preempt churn.

High Expectations for Integrated Financial Services

Wealth and institutional clients demand a one-stop shop across banking, insurance, and securities, pushing CTBC to bundle services and assign dedicated relationship managers; HNW clients (top 5% of assets) often demand bespoke portfolios. As of 2025 CTBC reports cross-sell ratio improvements—group AUM rose ~6.2% YoY to NT$2.3 trillion—supporting retention. Still, lacking a unified digital asset view risks migration to fintech-forward rivals with superior UX.

- Dedicated RMs: expected by HNW clients

- 2025 group AUM: ~NT$2.3 trillion (+6.2% YoY)

- Cross-sell key to churn defence

- Poor unified digital view → higher defection risk

Influence of Institutional Investors and ESG Demands

Institutional clients—pension funds and asset managers holding >NT$3.5 trillion in Taiwanese mandates—now make ESG transparency a lock-in condition, shifting allocations if CTBC misses benchmarks.

By 2025 ESG scores and green loan share (now 18% of CTBC Group’s corporate book) are core to value for institutions; failure to meet targets risks multi-percentage-point fund outflows.

CTBC must update lending and investment policies, report on Scope 1–3 emissions, and hit green financing targets to retain mandates.

- Institutional leverage: large, concentrated mandates >NT$3.5T

- 2025 reality: ESG central to institutional value

- CTBC green loans ≈18% corporate book

- Risk: portfolio reallocation, multi-pp outflows

High customer power: digital-savvy, multi-bank users drive CTBC retention and green growth

Customers hold high bargaining power: 82% smartphone banking penetration (2024), 68% multi-bank users, 62% use comparison apps (2025), HNW cross-sell raised AUM to NT$2.3T (+6.2% YoY), green loans ≈18% of corporate book; CTBC spends NT$2.1B (2024–25) on personalized marketing to retain clients.

| Metric | Value |

|---|---|

| Smartphone banking | 82% (2024) |

| Multi-bank users | 68% (2024) |

| Comparison app use | 62% (2025) |

| Group AUM | NT$2.3T (+6.2% YoY, 2025) |

| Green loans | 18% corporate book (2025) |

| Retention spend | NT$2.1B (2024–25) |

Full Version Awaits

CTBC Holding Porter's Five Forces Analysis

This preview shows the exact CTBC Holding Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups.

The document displayed here is fully formatted and ready for download the moment you buy, containing the same comprehensive competitive assessment and actionable insights.