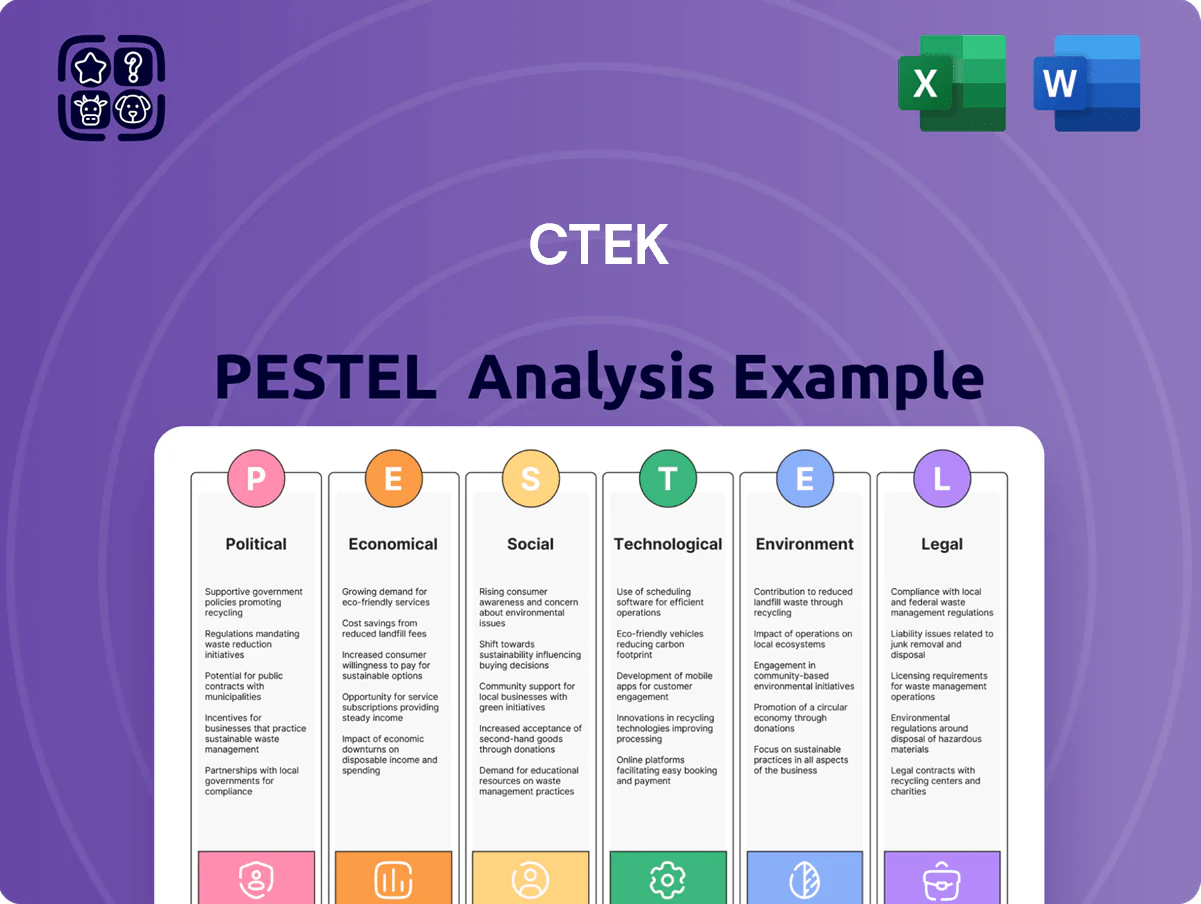

CTEK PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Uncover how political, economic, social, technological, environmental, and legal forces are shaping CTEK’s trajectory with our concise PESTLE snapshot—perfect for investors and strategists seeking actionable context. Purchase the full PESTLE for the complete, editable analysis and data-driven recommendations to inform decisions and sharpen competitive advantage.

Political factors

Government EV infrastructure incentives

Governmental support for EV charging infrastructure remains a critical driver for CTEK as of late 2025, with the US NEVI program allocating about $5 billion through 2026 and the EU mobilizing over €20 billion under recent Green Deal charging and grid modernization packages.

These funds prioritize smart, interoperable chargers; CTEK reported a 28% YoY increase in smart-charger inquiries in 2024 as procurement shifted toward NEVI-compliant solutions.

To capture subsidized public and private projects, CTEK must meet NEVI and EU compliance rules—metering, OCPP/OCPI interoperability, and cybersecurity standards—avoiding disqualification that could cost tens of millions in addressable contracts.

Global trade and tariff policies

The 2025 geopolitical landscape shows rising protective tariffs on electronic components and batteries; WTO data reports global tariff peaks up to 12% on semiconductor-containing goods. CTEK faces cost volatility tied to EU-China-US semiconductor trade—EU imports from China of integrated circuits rose 8% in 2024, while US restrictions tightened. Strategic sourcing, dual-sourcing, and nearshoring to EU plants can reduce tariff exposure and protect margins.

National energy security mandates

Many governments now mandate smart charging for energy independence, with the EU's Smart Charging Regulation targeting 95% of public chargers to support grid services by 2027 and US federal incentives linking funds to vehicle-to-grid readiness; such rules elevate demand for CTEK's load-balancing chargers across pro and consumer lines.

Policies requiring dynamic load management favor CTEK, whose high-end chargers meet EN 50663 and ISO 15118 standards, positioning the company to capture share as utilities seek compliant hardware—global smart charger market forecasted at CAGR 24% to reach $9.8bn by 2028.

Regulatory compliance thus becomes competitive advantage: mandates and procurement criteria de-risk premium device adoption and can improve CTEK's ASPs and margins as governments and fleets prioritize certified, grid-supportive chargers.

Standardization of charging protocols

Political pressure to standardize EV charging connectors and communication protocols has grown, with the EU pushing CEN-CENELEC mandates and the US Infrastructure Investment and Jobs Act funding $7.5bn for EV chargers to ensure cross-border interoperability for travelers.

CTEK must stay agile to adapt to regional laws that make CCS, Type 2, OCPP or ISO 15118 requirements mandatory at public points; noncompliance risks exclusion from infrastructure tenders and fleet contracts worth billions—EU public procurement for EV charging exceeded €1.2bn in 2024.

Failure to align with evolving political standards could bar CTEK from major tenders and fleet deals, reducing addressable market share in Europe and North America where standardized deployments account for over 60% of new public chargers in 2024.

- EU funding €7.5bn and US $7.5bn for charging infrastructure

- Mandatory standards: CCS, Type 2, OCPP, ISO 15118

- EU public procurement >€1.2bn (2024)

- Standardized deployments = >60% new public chargers (2024)

Sustainability and ESG reporting requirements

Political bodies increasingly demand transparent ESG reporting from mid-sized industrial firms like CTEK; EU Corporate Sustainability Reporting Directive now covers companies with >250 employees or €40m turnover, pushing detailed scope 3 carbon disclosures and conflict-mineral due diligence.

New requirements force CTEK to map supply-chain emissions and mineral sourcing; non-compliance risks exclusion from European capital markets where ESG-linked funds held €3.8tn in 2024 and institutional investors prioritize compliant issuers.

Massive EV charging subsidies, mandates and standards reshape supply, margins, procurement

Governments subsidize EV charging heavily (US NEVI $5bn to 2026; EU €20bn+ Green Deal); mandates (CCS/Type2, OCPP, ISO15118, Smart Charging) and CSRD (>250 emp/€40m) force compliance—EU public procurement €1.2bn (2024), standardized deployments >60% (2024); tariffs/semiconductor constraints (up to 12%) drive sourcing shifts impacting margins.

| Item | 2024/25 Data |

|---|---|

| US NEVI | $5bn to 2026 |

| EU funding | €20bn+ |

| EU procurement | €1.2bn (2024) |

| Std deployments | >60% (2024) |

What is included in the product

Explores how macro-environmental factors uniquely affect CTEK across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current data and trends to identify risks and opportunities for executives and investors.

A concise, PESTLE-organized summary that streamlines external risk analysis for quick reference in meetings or presentations, easily editable for local context and shareable across teams.

Economic factors

Global inflation and interest rate trends

By end-2025 global policy rates stabilized near 3.5–4.0% in advanced economies, easing auto loan costs and supporting EV purchase financing; vehicle loan rates fell ~120bps from 2023 peaks, boosting demand. However, input inflation for batteries and semiconductors remained elevated—cobalt and polysilicon costs ~15–25% above 2021 levels—compressing CTEK margins. CTEK must weigh premium pricing against stretched household real incomes and 2024–25 disposable income declines in key markets.

Fluctuations in raw material costs

The price of copper jumped about 18% in 2024 and averaged near 9,200 USD/ton, while aluminum rose ~12% and specialty polymers saw 10–15% yearly swings, driven by supply constraints and strong EV/renewables demand.

As a hardware manufacturer, CTEK faces direct margin pressure from these swings—raw material costs can account for 20–35% of COGS—making profitability highly sensitive to commodity cycles.

Effective hedging (forward contracts, metal-backed swaps) and JIT inventory reduced CTEK-like peers' input-cost volatility by ~60% in 2024, critical in an increasingly price-competitive market.

Growth of the secondary EV market

As first-generation mass-market EVs age—global used EV stock projected to exceed 10 million units by 2025—demand for aftermarket battery maintainers and diagnostic tools is rising, benefiting CTEK’s core battery-health expertise. Market reports estimate the global EV battery aftermarket could reach USD 6–8 billion by 2027, creating a lucrative niche for CTEK’s products. Serving second-hand EV owners offers a counter-cyclical revenue stream that can offset new vehicle sales volatility.

Labor market dynamics and automation

Rising labor costs in Europe and North America—wage inflation ~4–6% annually in manufacturing through 2024–25—have pushed CTEK to expand production automation and digital supply-chain tools, with capex on automation rising an estimated 12–18% YoY.

Shortage of skilled R&D talent keeps engineer/software wages elevated (median tech salary growth ~7% in 2024), constraining product development velocity.

Managing higher human-capital expenses while scaling output is a core economic challenge for CTEK executives through 2026.

- Automation capex +12–18% YoY

- Manufacturing wage inflation ~4–6% annually (2024–25)

- Tech/engineer pay growth ~7% in 2024

Currency exchange rate volatility

As a Swedish company with global operations, CTEK faces Krona volatility versus the Euro and USD; SEK weakened about 6% vs EUR and 8% vs USD in 2024, which can erode export competitiveness and raise import costs for charger components.

Significant FX moves can compress margins on exported units and increase landed costs of semiconductors and transformers; hedging and pricing adjustments are needed to protect 2024 consolidated results.

- 2024 FX moves: SEK -6% vs EUR, -8% vs USD

- Exposure: export price competitiveness, imported component costs

- Mitigation: active hedging, dynamic international pricing

Stabilizing rates fuel car demand but rising input costs squeeze margins

Global rates stabilized ~3.5–4.0% end-2025, easing auto loans; vehicle loan rates fell ~120bps vs 2023, boosting demand, while copper +18% (avg ~9,200 USD/t in 2024), aluminum +12%, and battery inputs 15–25% above 2021, squeezing margins; automation capex +12–18% YoY, manufacturing wage inflation ~4–6% and tech pay +7% in 2024; SEK -6% vs EUR, -8% vs USD in 2024, raising imported component costs.

Preview the Actual Deliverable

CTEK PESTLE Analysis

The preview shown here is the exact CTEK PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and conclusions visible in this preview are the final document available for immediate download after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Uncover how political, economic, social, technological, environmental, and legal forces are shaping CTEK’s trajectory with our concise PESTLE snapshot—perfect for investors and strategists seeking actionable context. Purchase the full PESTLE for the complete, editable analysis and data-driven recommendations to inform decisions and sharpen competitive advantage.

Political factors

Government EV infrastructure incentives

Governmental support for EV charging infrastructure remains a critical driver for CTEK as of late 2025, with the US NEVI program allocating about $5 billion through 2026 and the EU mobilizing over €20 billion under recent Green Deal charging and grid modernization packages.

These funds prioritize smart, interoperable chargers; CTEK reported a 28% YoY increase in smart-charger inquiries in 2024 as procurement shifted toward NEVI-compliant solutions.

To capture subsidized public and private projects, CTEK must meet NEVI and EU compliance rules—metering, OCPP/OCPI interoperability, and cybersecurity standards—avoiding disqualification that could cost tens of millions in addressable contracts.

Global trade and tariff policies

The 2025 geopolitical landscape shows rising protective tariffs on electronic components and batteries; WTO data reports global tariff peaks up to 12% on semiconductor-containing goods. CTEK faces cost volatility tied to EU-China-US semiconductor trade—EU imports from China of integrated circuits rose 8% in 2024, while US restrictions tightened. Strategic sourcing, dual-sourcing, and nearshoring to EU plants can reduce tariff exposure and protect margins.

National energy security mandates

Many governments now mandate smart charging for energy independence, with the EU's Smart Charging Regulation targeting 95% of public chargers to support grid services by 2027 and US federal incentives linking funds to vehicle-to-grid readiness; such rules elevate demand for CTEK's load-balancing chargers across pro and consumer lines.

Policies requiring dynamic load management favor CTEK, whose high-end chargers meet EN 50663 and ISO 15118 standards, positioning the company to capture share as utilities seek compliant hardware—global smart charger market forecasted at CAGR 24% to reach $9.8bn by 2028.

Regulatory compliance thus becomes competitive advantage: mandates and procurement criteria de-risk premium device adoption and can improve CTEK's ASPs and margins as governments and fleets prioritize certified, grid-supportive chargers.

Standardization of charging protocols

Political pressure to standardize EV charging connectors and communication protocols has grown, with the EU pushing CEN-CENELEC mandates and the US Infrastructure Investment and Jobs Act funding $7.5bn for EV chargers to ensure cross-border interoperability for travelers.

CTEK must stay agile to adapt to regional laws that make CCS, Type 2, OCPP or ISO 15118 requirements mandatory at public points; noncompliance risks exclusion from infrastructure tenders and fleet contracts worth billions—EU public procurement for EV charging exceeded €1.2bn in 2024.

Failure to align with evolving political standards could bar CTEK from major tenders and fleet deals, reducing addressable market share in Europe and North America where standardized deployments account for over 60% of new public chargers in 2024.

- EU funding €7.5bn and US $7.5bn for charging infrastructure

- Mandatory standards: CCS, Type 2, OCPP, ISO 15118

- EU public procurement >€1.2bn (2024)

- Standardized deployments = >60% new public chargers (2024)

Sustainability and ESG reporting requirements

Political bodies increasingly demand transparent ESG reporting from mid-sized industrial firms like CTEK; EU Corporate Sustainability Reporting Directive now covers companies with >250 employees or €40m turnover, pushing detailed scope 3 carbon disclosures and conflict-mineral due diligence.

New requirements force CTEK to map supply-chain emissions and mineral sourcing; non-compliance risks exclusion from European capital markets where ESG-linked funds held €3.8tn in 2024 and institutional investors prioritize compliant issuers.

Massive EV charging subsidies, mandates and standards reshape supply, margins, procurement

Governments subsidize EV charging heavily (US NEVI $5bn to 2026; EU €20bn+ Green Deal); mandates (CCS/Type2, OCPP, ISO15118, Smart Charging) and CSRD (>250 emp/€40m) force compliance—EU public procurement €1.2bn (2024), standardized deployments >60% (2024); tariffs/semiconductor constraints (up to 12%) drive sourcing shifts impacting margins.

| Item | 2024/25 Data |

|---|---|

| US NEVI | $5bn to 2026 |

| EU funding | €20bn+ |

| EU procurement | €1.2bn (2024) |

| Std deployments | >60% (2024) |

What is included in the product

Explores how macro-environmental factors uniquely affect CTEK across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current data and trends to identify risks and opportunities for executives and investors.

A concise, PESTLE-organized summary that streamlines external risk analysis for quick reference in meetings or presentations, easily editable for local context and shareable across teams.

Economic factors

Global inflation and interest rate trends

By end-2025 global policy rates stabilized near 3.5–4.0% in advanced economies, easing auto loan costs and supporting EV purchase financing; vehicle loan rates fell ~120bps from 2023 peaks, boosting demand. However, input inflation for batteries and semiconductors remained elevated—cobalt and polysilicon costs ~15–25% above 2021 levels—compressing CTEK margins. CTEK must weigh premium pricing against stretched household real incomes and 2024–25 disposable income declines in key markets.

Fluctuations in raw material costs

The price of copper jumped about 18% in 2024 and averaged near 9,200 USD/ton, while aluminum rose ~12% and specialty polymers saw 10–15% yearly swings, driven by supply constraints and strong EV/renewables demand.

As a hardware manufacturer, CTEK faces direct margin pressure from these swings—raw material costs can account for 20–35% of COGS—making profitability highly sensitive to commodity cycles.

Effective hedging (forward contracts, metal-backed swaps) and JIT inventory reduced CTEK-like peers' input-cost volatility by ~60% in 2024, critical in an increasingly price-competitive market.

Growth of the secondary EV market

As first-generation mass-market EVs age—global used EV stock projected to exceed 10 million units by 2025—demand for aftermarket battery maintainers and diagnostic tools is rising, benefiting CTEK’s core battery-health expertise. Market reports estimate the global EV battery aftermarket could reach USD 6–8 billion by 2027, creating a lucrative niche for CTEK’s products. Serving second-hand EV owners offers a counter-cyclical revenue stream that can offset new vehicle sales volatility.

Labor market dynamics and automation

Rising labor costs in Europe and North America—wage inflation ~4–6% annually in manufacturing through 2024–25—have pushed CTEK to expand production automation and digital supply-chain tools, with capex on automation rising an estimated 12–18% YoY.

Shortage of skilled R&D talent keeps engineer/software wages elevated (median tech salary growth ~7% in 2024), constraining product development velocity.

Managing higher human-capital expenses while scaling output is a core economic challenge for CTEK executives through 2026.

- Automation capex +12–18% YoY

- Manufacturing wage inflation ~4–6% annually (2024–25)

- Tech/engineer pay growth ~7% in 2024

Currency exchange rate volatility

As a Swedish company with global operations, CTEK faces Krona volatility versus the Euro and USD; SEK weakened about 6% vs EUR and 8% vs USD in 2024, which can erode export competitiveness and raise import costs for charger components.

Significant FX moves can compress margins on exported units and increase landed costs of semiconductors and transformers; hedging and pricing adjustments are needed to protect 2024 consolidated results.

- 2024 FX moves: SEK -6% vs EUR, -8% vs USD

- Exposure: export price competitiveness, imported component costs

- Mitigation: active hedging, dynamic international pricing

Stabilizing rates fuel car demand but rising input costs squeeze margins

Global rates stabilized ~3.5–4.0% end-2025, easing auto loans; vehicle loan rates fell ~120bps vs 2023, boosting demand, while copper +18% (avg ~9,200 USD/t in 2024), aluminum +12%, and battery inputs 15–25% above 2021, squeezing margins; automation capex +12–18% YoY, manufacturing wage inflation ~4–6% and tech pay +7% in 2024; SEK -6% vs EUR, -8% vs USD in 2024, raising imported component costs.

Preview the Actual Deliverable

CTEK PESTLE Analysis

The preview shown here is the exact CTEK PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and conclusions visible in this preview are the final document available for immediate download after checkout.