CTP Boston Consulting Group Matrix

Unlock Strategic Clarity

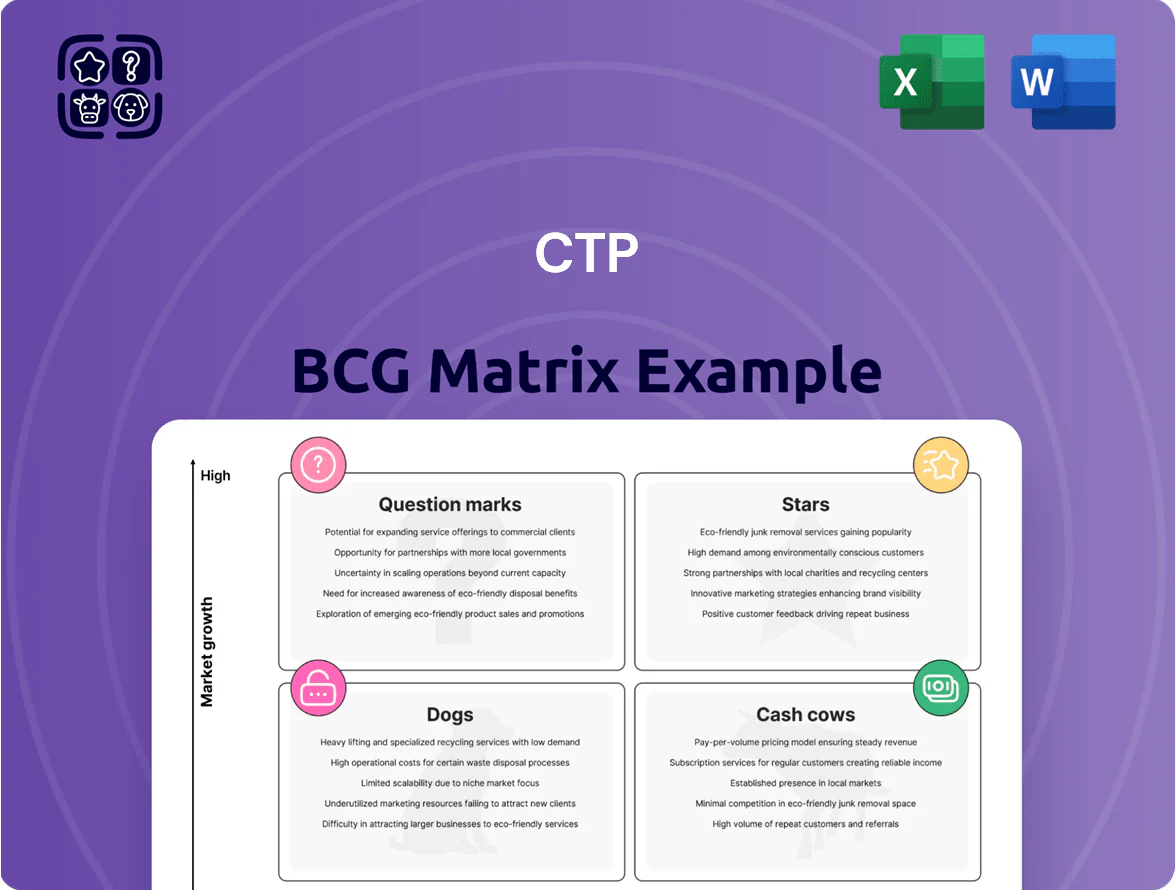

The CTP BCG Matrix preview highlights how product lines map to market growth and relative share—revealing potential Stars, Cash Cows, Question Marks, and Dogs to guide resource allocation and portfolio strategy. This snapshot surfaces key trends but leaves out quadrant-level detail, quantitative thresholds, and tailored moves you need to act decisively. Purchase the full BCG Matrix for a complete, data-driven breakdown, strategic recommendations, and ready-to-use Word and Excel deliverables that accelerate confident investment and product decisions.

Stars

Western European Expansion

CTP has pushed into Germany and the Netherlands, capturing ~5–7% logistics-hub share in key metros in 2024 as nearshoring lifted vacancy-demand spread by ~250 bps year-on-year; land and development capex per sqm in these markets sits near €1,200–€1,800, raising upfront spend but enabling higher rent growth.

Solar Energy and Renewables

Solar Energy and Renewables is a high-growth unit as rooftop PV rollouts meet rising tenant demand for green power; CTP reported 2025 on-site generation rising to 120 GWh/year (up 45% vs 2023) and expects 200 GWh by 2027.

The segment needs steady capex—CTP allocated €85m for energy infrastructure in 2024–25—but boosts ESG scores and lowers tenant energy costs, improving leasing appeal.

As capacity scales, income shifts: energy sales and PPA revenue grew to €18m in 2025, moving the unit from value-add to a primary revenue driver.

Data Center Development

As of late 2025, CTP has pivoted toward specialized data center development, targeting AI and hyperscale cloud demand that grew ~35% CAGR 2022–25; these projects carry higher margins but need heavy capex for power and cooling, often $1,200–1,800/kW installed.

CTP is using its 5,000+ ha land bank to rapidly scale capacity, aiming for 300–500 MW commissioned by 2027, funding build via €600m debt and reinvested free cash flow.

Polish Market Penetration

Poland is a star: logistics demand grew ~8.5% in 2024 and CTP now holds ~6% market share, scaling developments to match its Czech success with 620k m2 under construction as of Dec 2025.

Strong inflows from e-commerce and manufacturing—vacancy ~3.2% in 2024 and GDP growth 3.7%—make Poland high-growth; CTP is actively building new parks in Silesia and near Warsaw.

Continuous capex—CTP invested €420m in Poland 2024–2025—is required to keep pace with Prologis, GLP and local rivals.

- 2024 logistics demand +8.5%

- CTP ~6% market share

- 620k m2 under construction (Dec 2025)

- vacancy ~3.2% (2024)

- CTP capex €420m (2024–2025)

Urban Last-Mile Logistics

CTP’s push to develop CTPark Network hubs nearer city centers targets last-mile demand; projects yield higher rents—often 15–30% above standard logistics parks—and capture fast-delivery volume in congested markets.

Brownfield redevelopments are capital intensive, with capex per sqm often 20–40% higher, but secure dominant market share in supply-constrained urban cores where vacancy can dip below 3%.

This focus locks CTP into the most valuable supply-chain segment, driving yield expansion and rent growth while meeting the 24–48 hour delivery expectations of urban consumers.

- Higher rents: +15–30% vs standard parks

- Capex premium: +20–40% per sqm

- Urban vacancy: often <3%

- Delivery window targeted: 24–48 hours

CTP: Poland logistics, solar and data centers fuel rapid growth with €505m capex plan

Stars: Poland logistics, rooftop solar, and data centers drive high growth for CTP—Poland 620k m2 UC, ~6% share, vacancy 3.2%; solar 120 GWh (2025) → 200 GWh (2027); data center target 300–500 MW by 2027 with $1,200–1,800/kW capex; 2024–25 capex: Poland €420m, energy €85m, funding €600m debt.

| Asset | Key metric | 2024–25 |

|---|---|---|

| Poland logistics | Under construction / market share / vacancy | 620k m2 / ~6% / 3.2% |

| Solar | On-site gen / target | 120 GWh (2025) → 200 GWh (2027) |

| Data centers | Target MW / capex | 300–500 MW by 2027 / $1,200–1,800/kW |

| Capex | Allocated | Poland €420m; Energy €85m; Funding €600m debt |

What is included in the product

Comprehensive CTP BCG Matrix: quadrant-by-quadrant strategic guidance on Stars, Cash Cows, Question Marks, and Dogs, with invest/hold/divest advice.

One-page CTP BCG Matrix placing each product in a quadrant for fast portfolio decisions and stakeholder alignment

Cash Cows

Czech Republic Core Portfolio

CTP’s Czech Republic core portfolio, the company’s foundation, commands roughly a 40–45% industrial market share in a mature market as of 2025, delivering stable, high-margin rents (estimated NOI margin ~68% in 2024). These assets need minimal leasing promotion and generate predictable cash flow—CTP reported EUR 220m of recurring rental income from the Czech portfolio in 2024. That cash flow is the primary funding source for CTP’s expansion into higher-risk CEE and Western European markets, supporting EUR 1.1bn of acquisitions since 2022.

Romanian Industrial Parks

CTP dominates Romanian industrial parks with ~3.8 million m² GLA (2025), hosting multinational manufacturers and 95%+ stabilized occupancy, making it the market leader.

Market maturity drives predictable long-term lease renewals (avg. WAULT 6.2 years), enabling low capex on stabilized assets and steady cash flow.

Low reinvestment needs let CTP allocate free cash to service €1.6bn net debt (2025) and fund dividends, fitting the cash cow profile.

Property Management Services

The in-house property management of CTP’s 12.3 million m2 portfolio (YE 2024) generates stable service income, with estimated EBITDA margins above 40% due to fixed infrastructure and centralized ops.

Growth is limited—market rental growth of 2–3% (EU Q4 2024 average) caps expansion—but high margins and 95%+ occupancy deliver predictable cash flow and fund capex and acquisitions.

Slovakian Logistics Hubs

Slovakian logistics hubs are CTPs cash cows: they hold a dominant market share in automotive supply-chain logistics, delivering stable rents and EBITDA margins around 40% in 2025; vacancy rates remain very low at ~2% and yield compression keeps NOI high despite slowed new development.

- High market share in automotive logistics

- 2025 vacancy ~2%

- NOI and EBITDA margins ~40%

- Limited land for large builds; low growth

- Reliable, high-yield cash generation

Long-term Triple Net Leases

A large share of CTP's portfolio sits in long-term, inflation-linked triple net (NNN) leases with blue-chip tenants, providing predictable rent growth; at year-end 2024, NNN leases represented ~58% of rental income and CPI-linked clauses averaged 2.5% annual indexation.

Tenants pay property taxes, insurance, and maintenance, so CTP reports >85% net cash flow retention from these assets, requiring minimal capex and supporting stable free cash flow.

This steady NNN income underpins CTP's investment-grade credit: 2024 net debt/EBITDA was ~6.0x and interest coverage stayed near 3.2x, consistent with rating agency thresholds.

- 58% rental income from NNN leases

- 2.5% average CPI indexation (2024)

- >85% net cash flow retention

- Net debt/EBITDA ~6.0x (2024)

- Interest coverage ~3.2x (2024)

CTP cash cows: dominant CZ share, ~95% RO occ, €220m rent, robust margins, 6.0x leverage

CTP’s Czech/Slovak/Romanian cash cows (YE 2025) deliver stable cash flow: ~40–45% Czech market share, 95%+ occupancy Romania, Slovakia vacancy ~2%, NOI/EBITDA margins ~40–68%, NNN rents ~58% of income with 2.5% CPI indexation, EUR 220m Czech rental income (2024), net debt/EBITDA ~6.0x (2024).

| Metric | Value |

|---|---|

| Czech mkt share | 40–45% |

| Romania GLA occ. | 95%+ |

| Slovakia vacancy | ~2% |

| NOI/EBITDA margins | 40–68% |

| NNN share | 58% |

| CPI indexation | 2.5% |

| Czech rental income | €220m (2024) |

| Net debt/EBITDA | ~6.0x (2024) |

What You’re Viewing Is Included

CTP BCG Matrix

The preview you see is the exact CTP BCG Matrix document you’ll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready report crafted for strategic clarity and professional use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

The CTP BCG Matrix preview highlights how product lines map to market growth and relative share—revealing potential Stars, Cash Cows, Question Marks, and Dogs to guide resource allocation and portfolio strategy. This snapshot surfaces key trends but leaves out quadrant-level detail, quantitative thresholds, and tailored moves you need to act decisively. Purchase the full BCG Matrix for a complete, data-driven breakdown, strategic recommendations, and ready-to-use Word and Excel deliverables that accelerate confident investment and product decisions.

Stars

Western European Expansion

CTP has pushed into Germany and the Netherlands, capturing ~5–7% logistics-hub share in key metros in 2024 as nearshoring lifted vacancy-demand spread by ~250 bps year-on-year; land and development capex per sqm in these markets sits near €1,200–€1,800, raising upfront spend but enabling higher rent growth.

Solar Energy and Renewables

Solar Energy and Renewables is a high-growth unit as rooftop PV rollouts meet rising tenant demand for green power; CTP reported 2025 on-site generation rising to 120 GWh/year (up 45% vs 2023) and expects 200 GWh by 2027.

The segment needs steady capex—CTP allocated €85m for energy infrastructure in 2024–25—but boosts ESG scores and lowers tenant energy costs, improving leasing appeal.

As capacity scales, income shifts: energy sales and PPA revenue grew to €18m in 2025, moving the unit from value-add to a primary revenue driver.

Data Center Development

As of late 2025, CTP has pivoted toward specialized data center development, targeting AI and hyperscale cloud demand that grew ~35% CAGR 2022–25; these projects carry higher margins but need heavy capex for power and cooling, often $1,200–1,800/kW installed.

CTP is using its 5,000+ ha land bank to rapidly scale capacity, aiming for 300–500 MW commissioned by 2027, funding build via €600m debt and reinvested free cash flow.

Polish Market Penetration

Poland is a star: logistics demand grew ~8.5% in 2024 and CTP now holds ~6% market share, scaling developments to match its Czech success with 620k m2 under construction as of Dec 2025.

Strong inflows from e-commerce and manufacturing—vacancy ~3.2% in 2024 and GDP growth 3.7%—make Poland high-growth; CTP is actively building new parks in Silesia and near Warsaw.

Continuous capex—CTP invested €420m in Poland 2024–2025—is required to keep pace with Prologis, GLP and local rivals.

- 2024 logistics demand +8.5%

- CTP ~6% market share

- 620k m2 under construction (Dec 2025)

- vacancy ~3.2% (2024)

- CTP capex €420m (2024–2025)

Urban Last-Mile Logistics

CTP’s push to develop CTPark Network hubs nearer city centers targets last-mile demand; projects yield higher rents—often 15–30% above standard logistics parks—and capture fast-delivery volume in congested markets.

Brownfield redevelopments are capital intensive, with capex per sqm often 20–40% higher, but secure dominant market share in supply-constrained urban cores where vacancy can dip below 3%.

This focus locks CTP into the most valuable supply-chain segment, driving yield expansion and rent growth while meeting the 24–48 hour delivery expectations of urban consumers.

- Higher rents: +15–30% vs standard parks

- Capex premium: +20–40% per sqm

- Urban vacancy: often <3%

- Delivery window targeted: 24–48 hours

CTP: Poland logistics, solar and data centers fuel rapid growth with €505m capex plan

Stars: Poland logistics, rooftop solar, and data centers drive high growth for CTP—Poland 620k m2 UC, ~6% share, vacancy 3.2%; solar 120 GWh (2025) → 200 GWh (2027); data center target 300–500 MW by 2027 with $1,200–1,800/kW capex; 2024–25 capex: Poland €420m, energy €85m, funding €600m debt.

| Asset | Key metric | 2024–25 |

|---|---|---|

| Poland logistics | Under construction / market share / vacancy | 620k m2 / ~6% / 3.2% |

| Solar | On-site gen / target | 120 GWh (2025) → 200 GWh (2027) |

| Data centers | Target MW / capex | 300–500 MW by 2027 / $1,200–1,800/kW |

| Capex | Allocated | Poland €420m; Energy €85m; Funding €600m debt |

What is included in the product

Comprehensive CTP BCG Matrix: quadrant-by-quadrant strategic guidance on Stars, Cash Cows, Question Marks, and Dogs, with invest/hold/divest advice.

One-page CTP BCG Matrix placing each product in a quadrant for fast portfolio decisions and stakeholder alignment

Cash Cows

Czech Republic Core Portfolio

CTP’s Czech Republic core portfolio, the company’s foundation, commands roughly a 40–45% industrial market share in a mature market as of 2025, delivering stable, high-margin rents (estimated NOI margin ~68% in 2024). These assets need minimal leasing promotion and generate predictable cash flow—CTP reported EUR 220m of recurring rental income from the Czech portfolio in 2024. That cash flow is the primary funding source for CTP’s expansion into higher-risk CEE and Western European markets, supporting EUR 1.1bn of acquisitions since 2022.

Romanian Industrial Parks

CTP dominates Romanian industrial parks with ~3.8 million m² GLA (2025), hosting multinational manufacturers and 95%+ stabilized occupancy, making it the market leader.

Market maturity drives predictable long-term lease renewals (avg. WAULT 6.2 years), enabling low capex on stabilized assets and steady cash flow.

Low reinvestment needs let CTP allocate free cash to service €1.6bn net debt (2025) and fund dividends, fitting the cash cow profile.

Property Management Services

The in-house property management of CTP’s 12.3 million m2 portfolio (YE 2024) generates stable service income, with estimated EBITDA margins above 40% due to fixed infrastructure and centralized ops.

Growth is limited—market rental growth of 2–3% (EU Q4 2024 average) caps expansion—but high margins and 95%+ occupancy deliver predictable cash flow and fund capex and acquisitions.

Slovakian Logistics Hubs

Slovakian logistics hubs are CTPs cash cows: they hold a dominant market share in automotive supply-chain logistics, delivering stable rents and EBITDA margins around 40% in 2025; vacancy rates remain very low at ~2% and yield compression keeps NOI high despite slowed new development.

- High market share in automotive logistics

- 2025 vacancy ~2%

- NOI and EBITDA margins ~40%

- Limited land for large builds; low growth

- Reliable, high-yield cash generation

Long-term Triple Net Leases

A large share of CTP's portfolio sits in long-term, inflation-linked triple net (NNN) leases with blue-chip tenants, providing predictable rent growth; at year-end 2024, NNN leases represented ~58% of rental income and CPI-linked clauses averaged 2.5% annual indexation.

Tenants pay property taxes, insurance, and maintenance, so CTP reports >85% net cash flow retention from these assets, requiring minimal capex and supporting stable free cash flow.

This steady NNN income underpins CTP's investment-grade credit: 2024 net debt/EBITDA was ~6.0x and interest coverage stayed near 3.2x, consistent with rating agency thresholds.

- 58% rental income from NNN leases

- 2.5% average CPI indexation (2024)

- >85% net cash flow retention

- Net debt/EBITDA ~6.0x (2024)

- Interest coverage ~3.2x (2024)

CTP cash cows: dominant CZ share, ~95% RO occ, €220m rent, robust margins, 6.0x leverage

CTP’s Czech/Slovak/Romanian cash cows (YE 2025) deliver stable cash flow: ~40–45% Czech market share, 95%+ occupancy Romania, Slovakia vacancy ~2%, NOI/EBITDA margins ~40–68%, NNN rents ~58% of income with 2.5% CPI indexation, EUR 220m Czech rental income (2024), net debt/EBITDA ~6.0x (2024).

| Metric | Value |

|---|---|

| Czech mkt share | 40–45% |

| Romania GLA occ. | 95%+ |

| Slovakia vacancy | ~2% |

| NOI/EBITDA margins | 40–68% |

| NNN share | 58% |

| CPI indexation | 2.5% |

| Czech rental income | €220m (2024) |

| Net debt/EBITDA | ~6.0x (2024) |

What You’re Viewing Is Included

CTP BCG Matrix

The preview you see is the exact CTP BCG Matrix document you’ll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready report crafted for strategic clarity and professional use.