CTP Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

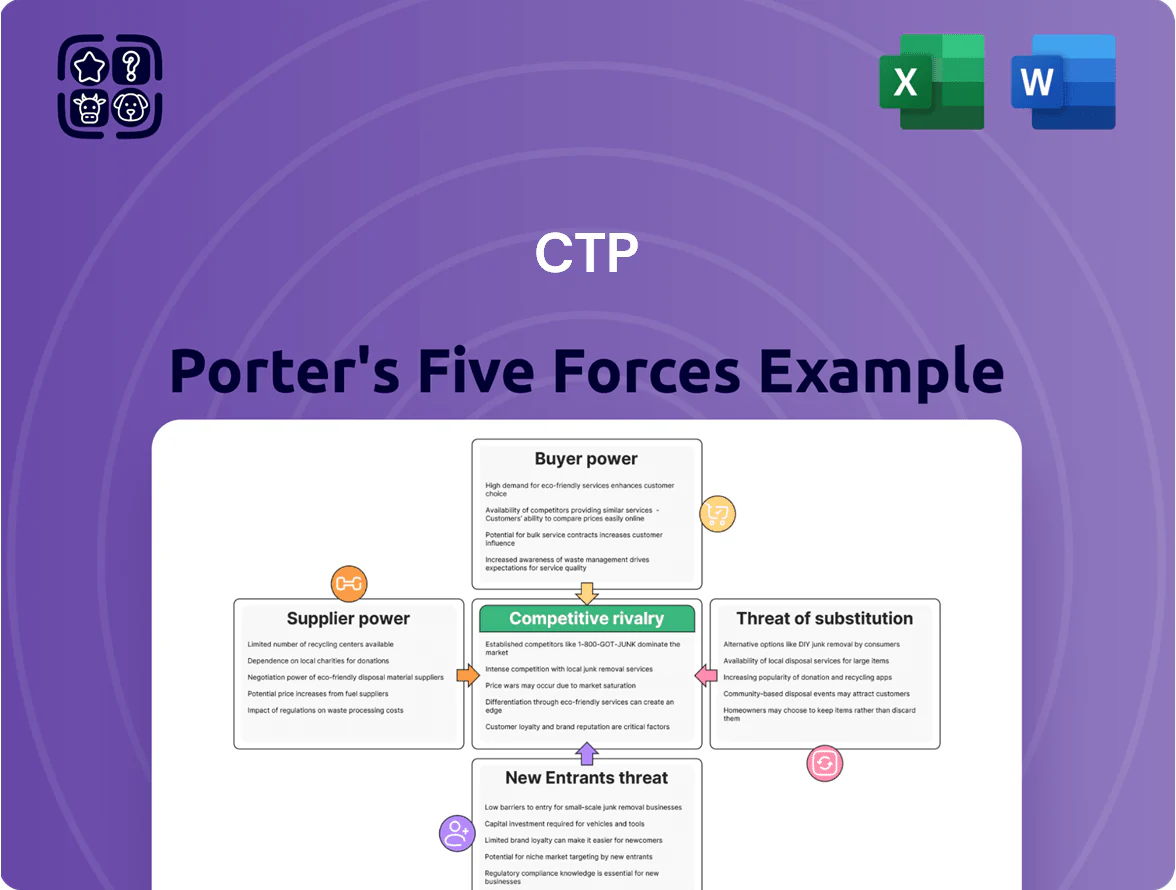

CTP’s Porter's Five Forces snapshot highlights key pressures—from supplier leverage and buyer dynamics to rivalry and substitute threats—showing where strategic risks and opportunities lie; this preview only scratches the surface. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable insights to inform investment decisions and strategic planning.

Suppliers Bargaining Power

Concentration of specialized construction firms

The pool of contractors able to build large-scale, sustainable industrial parks across CEE is concentrated, with roughly 10–15 firms handling >60% of major projects; that limits supplier choice for CTP. CTP’s €5.5bn development pipeline (2025 guidance) forces reliance on these specialists to meet strict ESG and technical specs. Still, CTP’s scale and repeat volume secure better pricing and payment terms versus smaller developers. What this hides: single-project delays can still disrupt timelines.

Scarcity of prime land plots

Landowners along strategic transport corridors wield high leverage as zoned industrial land in Central Europe fell by about 12% from 2018–2024 in major hubs, pushing plot premiums up to 30% above pre-2019 levels.

CTP counters this by holding roughly 40 km² of land bank (2025 company filings), locking future growth and reducing urgency to buy at peak prices.

Still, competition from residential and retail developers raises acquisition costs sharply in Prague, Bratislava and Debrecen, squeezing margins on new logistics projects.

Fluctuating costs of sustainable materials

Suppliers of green materials saw demand rise ~18% across the EU in 2024–25 after tighter energy-performance rules; this pushed solar-panel and low-carbon insulation prices up ~12% YoY by Q3 2025, hitting CTP given its BREEAM targets.

CTP's sensitivity to such volatility risks ~0.5–1.0% EBITDA margin pressure per 100 bp raw-material inflation; long-term contracts with three major suppliers covering ~65% of volumes limit spikes during peak builds.

Influence of debt capital markets

As a capital‑intensive developer, CTP relies heavily on banks and bond markets for funding; by Q4 2025 global corporate bond issuance was ~$8.2trn and eurozone yields eased, improving access to debt.

Interest rates stabilized late 2025, but lender covenants and margins still dictate project IRRs and rollout speed; tighter terms can delay new parks.

CTP’s investment‑grade rating (BBB–/Baa3 range in 2025) cuts its average funding cost by ~75–125bp versus unrated regional peers, easing expansion.

- High dependence on debt capital markets

- Q4 2025 bond market normalization aids access

- Lender terms remain key project constraint

- Investment‑grade rating reduces funding spread ~75–125bp

Energy and utility infrastructure providers

Logistics parks need large power connections as automation and EV fleets grow; CTP estimates site loads rising 40% by 2028 with chargers adding ~0.5–1 MW per site.

Local utility monopolies in CEE can set fees and timelines, delaying projects; average grid connection lead times range 6–24 months across Poland, Romania, Czechia (2024 ENTSO-E regional data).

CTP offsets supplier power leverage by investing in on-site renewables and storage—over 150 MWp rooftop solar and 70 MWh battery capacity pledged by end-2025—cutting grid demand and bargaining risk.

- Rising demand: +40% load by 2028 estimate

- Connection delays: 6–24 months typical

- CTP buildout: 150 MWp solar, 70 MWh batteries (target end‑2025)

Supplier squeeze vs CTP scale: €5.5bn pipeline, 40km² land, modest EBITDA sensitivity

Concentrated contractor pool (10–15 firms, >60% projects) and scarce zoned land (–12% 2018–24) give suppliers high leverage, but CTP’s €5.5bn pipeline and 40 km² land bank plus BBB–/Baa3 rating and long‑term contracts (covering ~65% volumes) mitigate cost and timing risk; material and grid price shifts still threaten ~0.5–1.0% EBITDA per 100bp raw‑material inflation.

| Metric | Value (2025) |

|---|---|

| Development pipeline | €5.5bn |

| CTP land bank | 40 km² |

| Contractor concentration | 10–15 firms, >60% |

| Material price impact | ~12% YoY (solar/insulation) |

| EBITDA sensitivity | 0.5–1.0% per 100bp |

| Renewables build | 150 MWp solar, 70 MWh batteries |

| Rating | BBB– / Baa3 |

What is included in the product

Tailored Porter's Five Forces analysis for CTP that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging disruptors—delivered in editable Word format for incorporation into investor decks or strategic plans.

A one-sheet CTP Porter's Five Forces view that quantifies competitive pressure and surfaces strategic levers—ready to drop into decks for faster, data-driven decisions.

Customers Bargaining Power

Dominance of global e-commerce and 3PL giants

Large tenants such as Amazon and DHL occupy up to 25–35% of CTP’s leasable area in key markets and can demand bespoke facility designs, forcing CapEx customization and longer fit-out timelines.

These sophisticated buyers run competitive tenders between CTP, Panattoni, and Prologis; in 2024, major logistics deals saw rent discounts of 10–22% and rent‑free periods averaging 3–6 months.

Increasing demand for flexible lease structures

By end-2025 tenants demand flexible leases to weather volatile consumer markets and supply-chain shocks; industry surveys show 42% of logistics occupiers prefer <12-month options, pressuring CTP to offer shorter terms or in-park expansion clauses to hold occupancy near its 95% target. This boosts retention and average lease renewals but shifts vacancy and capex timing risk from tenants to CTP, potentially lowering near-term cashflow visibility by an estimated 3–5%.

High switching costs for integrated logistics

Once a tenant embeds automation and conveyors into a specific CTPark, moving costs often exceed 1–3x annual rent and can halt operations for weeks, creating strong physical and operational lock-in.

That lock-in cuts customer bargaining power at renewal: industry data shows retention rises above 85% for integrated logistics tenants, so CTP extracts longer leases and steady rental growth.

CTP emphasizes premium property management, rapid maintenance response and capex coordination, making staying the most rational, cost-saving option.

Tenant sensitivity to total occupancy costs

Tenants now weigh energy and service charges with base rent; surveys show 62% of logistics tenants cite total occupancy cost as decisive in 2024.

CTP’s push for energy-neutral buildings and efficient operations cuts secondary costs—energy spend per sqm fell ~28% across its portfolio in 2023—so tenants face lower total occupancy bills.

That lets CTP keep higher base rents (like 6–8% premium in mature markets) while delivering a cheaper overall occupancy cost versus older parks.

- 62% of tenants prioritize total cost (2024 survey)

- CTP energy use down ~28% (2023)

- CTP base rent premium ~6–8% in mature markets

- Lower total occupancy cost vs older assets

Geographic concentration of tenant operations

CTP’s scale and efficiency drive long leases, 6–8% rent premium and ~28% lower costs

Large integrated tenants hold some leverage via bespoke demand and tendering, but high fit-out costs, automation lock-in (1–3x annual rent) and CTP’s 46% CEE GLA share (2024) reduce bargaining power; retention >80% and integrated tenant retention >85% let CTP secure longer leases and 6–8% base rent premium while total occupancy costs fall ~28% due to energy efficiency.

| Metric | Value |

|---|---|

| CTP CEE GLA share (2024) | 46% |

| Lease renewals (2024) | >80% |

| Integrated tenant retention | >85% |

| Automation move cost | 1–3x annual rent |

| Energy use reduction (2023) | ~28% |

| Base rent premium (mature) | 6–8% |

Full Version Awaits

CTP Porter's Five Forces Analysis

This preview shows the exact CTP Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The professionally formatted document you see is the final deliverable, ready to download and use the moment you buy. It contains the complete, actionable assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry. What’s previewed is precisely what you’ll get.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

CTP’s Porter's Five Forces snapshot highlights key pressures—from supplier leverage and buyer dynamics to rivalry and substitute threats—showing where strategic risks and opportunities lie; this preview only scratches the surface. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable insights to inform investment decisions and strategic planning.

Suppliers Bargaining Power

Concentration of specialized construction firms

The pool of contractors able to build large-scale, sustainable industrial parks across CEE is concentrated, with roughly 10–15 firms handling >60% of major projects; that limits supplier choice for CTP. CTP’s €5.5bn development pipeline (2025 guidance) forces reliance on these specialists to meet strict ESG and technical specs. Still, CTP’s scale and repeat volume secure better pricing and payment terms versus smaller developers. What this hides: single-project delays can still disrupt timelines.

Scarcity of prime land plots

Landowners along strategic transport corridors wield high leverage as zoned industrial land in Central Europe fell by about 12% from 2018–2024 in major hubs, pushing plot premiums up to 30% above pre-2019 levels.

CTP counters this by holding roughly 40 km² of land bank (2025 company filings), locking future growth and reducing urgency to buy at peak prices.

Still, competition from residential and retail developers raises acquisition costs sharply in Prague, Bratislava and Debrecen, squeezing margins on new logistics projects.

Fluctuating costs of sustainable materials

Suppliers of green materials saw demand rise ~18% across the EU in 2024–25 after tighter energy-performance rules; this pushed solar-panel and low-carbon insulation prices up ~12% YoY by Q3 2025, hitting CTP given its BREEAM targets.

CTP's sensitivity to such volatility risks ~0.5–1.0% EBITDA margin pressure per 100 bp raw-material inflation; long-term contracts with three major suppliers covering ~65% of volumes limit spikes during peak builds.

Influence of debt capital markets

As a capital‑intensive developer, CTP relies heavily on banks and bond markets for funding; by Q4 2025 global corporate bond issuance was ~$8.2trn and eurozone yields eased, improving access to debt.

Interest rates stabilized late 2025, but lender covenants and margins still dictate project IRRs and rollout speed; tighter terms can delay new parks.

CTP’s investment‑grade rating (BBB–/Baa3 range in 2025) cuts its average funding cost by ~75–125bp versus unrated regional peers, easing expansion.

- High dependence on debt capital markets

- Q4 2025 bond market normalization aids access

- Lender terms remain key project constraint

- Investment‑grade rating reduces funding spread ~75–125bp

Energy and utility infrastructure providers

Logistics parks need large power connections as automation and EV fleets grow; CTP estimates site loads rising 40% by 2028 with chargers adding ~0.5–1 MW per site.

Local utility monopolies in CEE can set fees and timelines, delaying projects; average grid connection lead times range 6–24 months across Poland, Romania, Czechia (2024 ENTSO-E regional data).

CTP offsets supplier power leverage by investing in on-site renewables and storage—over 150 MWp rooftop solar and 70 MWh battery capacity pledged by end-2025—cutting grid demand and bargaining risk.

- Rising demand: +40% load by 2028 estimate

- Connection delays: 6–24 months typical

- CTP buildout: 150 MWp solar, 70 MWh batteries (target end‑2025)

Supplier squeeze vs CTP scale: €5.5bn pipeline, 40km² land, modest EBITDA sensitivity

Concentrated contractor pool (10–15 firms, >60% projects) and scarce zoned land (–12% 2018–24) give suppliers high leverage, but CTP’s €5.5bn pipeline and 40 km² land bank plus BBB–/Baa3 rating and long‑term contracts (covering ~65% volumes) mitigate cost and timing risk; material and grid price shifts still threaten ~0.5–1.0% EBITDA per 100bp raw‑material inflation.

| Metric | Value (2025) |

|---|---|

| Development pipeline | €5.5bn |

| CTP land bank | 40 km² |

| Contractor concentration | 10–15 firms, >60% |

| Material price impact | ~12% YoY (solar/insulation) |

| EBITDA sensitivity | 0.5–1.0% per 100bp |

| Renewables build | 150 MWp solar, 70 MWh batteries |

| Rating | BBB– / Baa3 |

What is included in the product

Tailored Porter's Five Forces analysis for CTP that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging disruptors—delivered in editable Word format for incorporation into investor decks or strategic plans.

A one-sheet CTP Porter's Five Forces view that quantifies competitive pressure and surfaces strategic levers—ready to drop into decks for faster, data-driven decisions.

Customers Bargaining Power

Dominance of global e-commerce and 3PL giants

Large tenants such as Amazon and DHL occupy up to 25–35% of CTP’s leasable area in key markets and can demand bespoke facility designs, forcing CapEx customization and longer fit-out timelines.

These sophisticated buyers run competitive tenders between CTP, Panattoni, and Prologis; in 2024, major logistics deals saw rent discounts of 10–22% and rent‑free periods averaging 3–6 months.

Increasing demand for flexible lease structures

By end-2025 tenants demand flexible leases to weather volatile consumer markets and supply-chain shocks; industry surveys show 42% of logistics occupiers prefer <12-month options, pressuring CTP to offer shorter terms or in-park expansion clauses to hold occupancy near its 95% target. This boosts retention and average lease renewals but shifts vacancy and capex timing risk from tenants to CTP, potentially lowering near-term cashflow visibility by an estimated 3–5%.

High switching costs for integrated logistics

Once a tenant embeds automation and conveyors into a specific CTPark, moving costs often exceed 1–3x annual rent and can halt operations for weeks, creating strong physical and operational lock-in.

That lock-in cuts customer bargaining power at renewal: industry data shows retention rises above 85% for integrated logistics tenants, so CTP extracts longer leases and steady rental growth.

CTP emphasizes premium property management, rapid maintenance response and capex coordination, making staying the most rational, cost-saving option.

Tenant sensitivity to total occupancy costs

Tenants now weigh energy and service charges with base rent; surveys show 62% of logistics tenants cite total occupancy cost as decisive in 2024.

CTP’s push for energy-neutral buildings and efficient operations cuts secondary costs—energy spend per sqm fell ~28% across its portfolio in 2023—so tenants face lower total occupancy bills.

That lets CTP keep higher base rents (like 6–8% premium in mature markets) while delivering a cheaper overall occupancy cost versus older parks.

- 62% of tenants prioritize total cost (2024 survey)

- CTP energy use down ~28% (2023)

- CTP base rent premium ~6–8% in mature markets

- Lower total occupancy cost vs older assets

Geographic concentration of tenant operations

CTP’s scale and efficiency drive long leases, 6–8% rent premium and ~28% lower costs

Large integrated tenants hold some leverage via bespoke demand and tendering, but high fit-out costs, automation lock-in (1–3x annual rent) and CTP’s 46% CEE GLA share (2024) reduce bargaining power; retention >80% and integrated tenant retention >85% let CTP secure longer leases and 6–8% base rent premium while total occupancy costs fall ~28% due to energy efficiency.

| Metric | Value |

|---|---|

| CTP CEE GLA share (2024) | 46% |

| Lease renewals (2024) | >80% |

| Integrated tenant retention | >85% |

| Automation move cost | 1–3x annual rent |

| Energy use reduction (2023) | ~28% |

| Base rent premium (mature) | 6–8% |

Full Version Awaits

CTP Porter's Five Forces Analysis

This preview shows the exact CTP Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The professionally formatted document you see is the final deliverable, ready to download and use the moment you buy. It contains the complete, actionable assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry. What’s previewed is precisely what you’ll get.