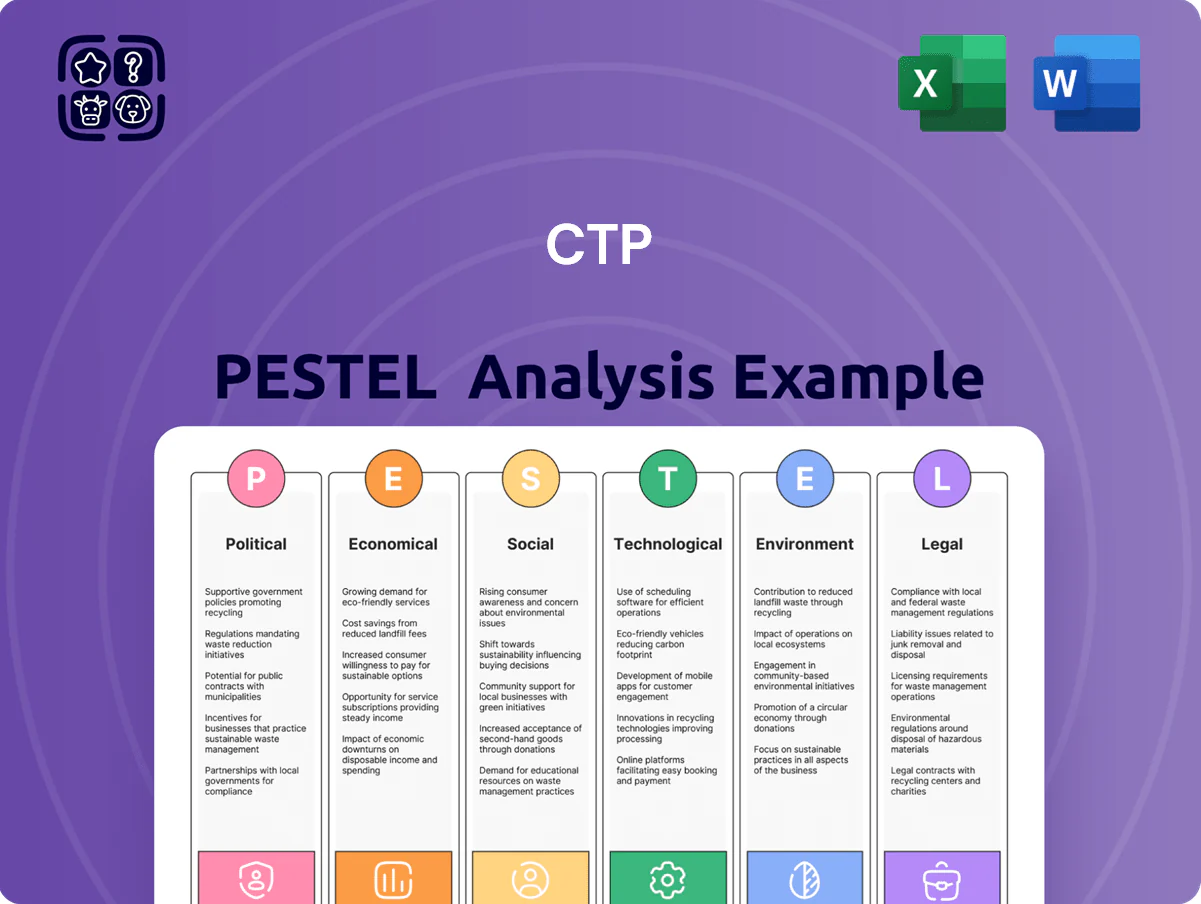

CTP PESTLE Analysis

Skip the Research. Get the Strategy.

Unlock how political, economic, social, technological, legal, and environmental forces are shaping CTP’s trajectory—our concise PESTLE highlights key risks and opportunities to inform smarter decisions; purchase the full report for the complete, editable analysis and actionable insights ready for strategy, investment, or due diligence.

Political factors

Geopolitical stability in CEE regions

The ongoing geopolitical tensions in Eastern Europe continue to weigh on investor sentiment into 2025, with FDI into CEE down 6% y/y in 2024 and risk premia for regional assets rising by ~40 bps; CTP must monitor spillovers from the Russia-Ukraine conflict and NATO posture changes across Poland, Romania and the Czech Republic.

Shifting alliances and security concerns require CTP to reassess leasing and development timelines—Poland and Romania accounted for ~60% of CTP’s 2024 rental income—while scenario planning for supply-chain and insurance cost shocks is essential.

Maintaining strong local government relationships is critical: public infrastructure commitments in CEE totaled €18.5bn in 2024, and proactive engagement can help CTP secure approvals, subsidies and stability against regional volatility.

EU integration and cohesion policy

CTP, as a major Central and Eastern Europe developer, benefits from EU cohesion funds—EU budget 2021–2027 allocates €373 billion for cohesion, with Poland and Romania receiving ~€80B and €58B respectively, enhancing infrastructure near CTP parks; reductions or reallocation of these funds would affect transport link upgrades and logistics costs, while EU integration shifts (e.g., accession talks, rule-of-law disputes) alter planning horizons and investment risk assessments.

Trade policy and nearshoring trends

Political drives to cut Asian supply-chain reliance have pushed EU nearshoring: by Q4 2025 nearshoring investment commitments reached an estimated €120bn, lifting demand for logistics space; CTP, with c.5.6m sqm in Europe, is well placed to capture incentives (tax credits, grants covering up to 25% capex) aimed at reshoring manufacturing. Changes in EU trade pacts and tariffs with neighbors like the UK and Turkey directly shift cross‑border freight flows and warehouse utilization rates.

Governmental focus on industrial modernization

National governments across CEE are prioritizing industrial modernization to lift GDP—EU cohesion funds and national plans target 2024–25 industrial investment increases of 3–6% GDP-equivalent in select states, boosting demand for high-tech facilities.

Political backing for high-tech manufacturing and R&D hubs creates favorable leasing prospects for CTP’s specialized parks; 2024 FDI into CEE manufacturing rose ~12% YoY, supporting tenant pipeline.

Legislation for industrial zones commonly includes tax incentives and streamlined permits—examples: Hungary and Poland offering up to 10–15% corporate tax relief or expedited approvals reducing setup time by 30%.

- Governments raising industrial investment by 3–6% GDP-equivalent (2024–25)

- CEE manufacturing FDI up ~12% YoY in 2024

- Tax relief and faster permits (10–15% tax benefit; ~30% faster approvals)

Public infrastructure investment levels

The federal and state commitment to expanding rail, road and port infrastructure directly affects CTP site selection and valuations; Australia’s 2024 federal infrastructure pipeline exceeded A$150 billion, improving access for key logistics corridors and lifting nearby industrial land values by up to 12% in some regions.

Delays in state-funded projects—Queensland’s Bruce Highway and NSW’s Regional Rail upgrades faced multi-year slippages in 2023–24—can reduce hub connectivity, increasing tenant churn and vacancy risk.

Monitoring national and state infrastructure pipelines enables CTP to time development phases with upgrades, capture higher rents and lower transport-cost exposure.

- Federal pipeline > A$150bn (2024)

- Land value uplift up to 12% near upgrades

- Project delays raise vacancy/tenant churn risk

- Aligning development to pipelines improves rents

CEE: Nearshoring & funds offset risk — FDI mixed, logistics and land values rise

Geopolitical tensions raised regional risk premia ~40 bps and cut CEE FDI 6% y/y in 2024; Poland/Romania ~60% of CTP rental income; EU cohesion funds (2021–27) €373bn with Poland €80bn, Romania €58bn; nearshoring commitments ~€120bn by Q4 2025 boosting logistics demand; CEE manufacturing FDI +12% YoY in 2024; infrastructure pipelines (AU A$150bn) lift nearby land values up to 12%.

| Metric | Value |

|---|---|

| CEE FDI change (2024) | -6% y/y |

| Risk premia shift | +~40 bps |

| Poland/Romania share of CTP rent | ~60% |

| EU cohesion fund (2021–27) | €373bn |

| Nearshoring commitments (Q4 2025) | €120bn |

| CEE manufacturing FDI (2024) | +12% YoY |

| AU federal pipeline (2024) | A$150bn |

| Land value uplift near upgrades | up to 12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect the CTP across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify risks and opportunities.

CTP's PESTLE analysis condenses comprehensive external-factor research into a clean, shareable summary—visually segmented by category and written in plain language so teams can quickly align, add context-specific notes, and drop insights into presentations or strategy sessions.

Economic factors

Interest rate environment and financing costs

By end-2025, ECB rate stabilization near 3.75–4.00% remains key for capital-intensive real estate firms like CTP; continued pressure from 2024’s peak rates still influences market liquidity. CTP’s refinancing and development funding are sensitive to yields—European CRE prime yields rose to ~4.2% in 2024, squeezing margins and raising cost of capital. Higher rates dampen valuations (office/logistics cap rates widened ~50–150 bps in 2023–24) and force stricter capital allocation and longer hold strategies.

Inflationary pressures on construction costs

While headline inflation eased from a 2022 peak, industrial construction input costs remain high: steel is up ~15% and cement ~8% year-on-year (2025 OECD data), and energy prices average ~20% above 2019 levels, keeping margins under pressure.

CTP must model persistent price volatility into development margins, using sensitivity scenarios where raw-material cost shocks of 10–20% can cut project IRRs by 150–400 basis points.

Effective procurement—bulk buying, hedging, and 3–7 year supplier contracts—plus indexed pricing clauses have reduced cost volatility for peers by ~30% and are essential for protecting profitability on new builds.

E-commerce penetration and retail shifts

Labor market dynamics and wage growth

Tight labor markets in the Czech Republic and Hungary—Q4 2025 unemployment around 2.8% and 3.7% respectively—raise operational costs for CTP tenants via upward wage pressure; average manufacturing wages rose ~8–10% YoY in 2024–25 in Central Europe.

Rising wages accelerate tenant demand for automation, shifting building specs toward higher power capacity, clear heights and integrated robotics support; CTP reported 12% higher power bookings in 2024 for automated facilities.

Regional skilled-labor availability—engineering graduates per 1,000 population and proximity to technical universities—drives park attractiveness for international manufacturers, influencing leasing velocity and rent premiums of 5–7% in 2024 for parks near talent hubs.

- Tight labor markets: Czech 2.8% & Hungary 3.7% unemployment (Q4 2025)

- Wage growth: manufacturing wages +8–10% YoY (2024–25)

- Automation demand: CTP power bookings +12% (2024)

- Talent proximity: rent premiums ~5–7% (2024)

Currency fluctuations in non-Euro markets

CTP’s operations in Poland and Hungary expose it to Polish Zloty and Hungarian Forint volatility; a 10% FX move against the Euro could swing reported group EBITDA by roughly EUR 15–25m based on 2024 regional revenues of ~EUR 1.2bn.

Management uses forward contracts and natural hedges; about 70% of new leases are Euro-denominated, and net FX hedges covered ~60% of expected 12-month exposure at end-2024.

- 10% FX move ≈ EUR 15–25m EBITDA impact

- 2024 regional revenues ≈ EUR 1.2bn

- ~70% of new leases Euro-denominated

- ~60% of 12‑month FX exposure hedged (end‑2024)

Higher ECB rates, rising input costs and FX risk squeeze CRE values despite strong logistics

ECB rates near 3.75–4.00% keep financing costs elevated; 2024 prime CRE yields ~4.2% and cap-rate widening 50–150bps reduced valuations. Industrial input costs: steel +15%, cement +8% (2025 OECD); energy +20% vs 2019. E‑commerce 23% of retail (2024) lifts logistics occupancy to 97% and rents +6%. FX: 10% move ≈ EUR 15–25m EBITDA; ~70% leases euro, ~60% 12‑month FX hedged (end‑2024).

| Metric | Value |

|---|---|

| ECB rate | 3.75–4.00% |

| Prime CRE yield (2024) | ~4.2% |

| Logistics occupancy | 97% |

| Steel/cement (YoY) | +15% / +8% |

| FX sensitivity | 10% → EUR 15–25m |

Full Version Awaits

CTP PESTLE Analysis

The preview shown here is the exact CTP PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Unlock how political, economic, social, technological, legal, and environmental forces are shaping CTP’s trajectory—our concise PESTLE highlights key risks and opportunities to inform smarter decisions; purchase the full report for the complete, editable analysis and actionable insights ready for strategy, investment, or due diligence.

Political factors

Geopolitical stability in CEE regions

The ongoing geopolitical tensions in Eastern Europe continue to weigh on investor sentiment into 2025, with FDI into CEE down 6% y/y in 2024 and risk premia for regional assets rising by ~40 bps; CTP must monitor spillovers from the Russia-Ukraine conflict and NATO posture changes across Poland, Romania and the Czech Republic.

Shifting alliances and security concerns require CTP to reassess leasing and development timelines—Poland and Romania accounted for ~60% of CTP’s 2024 rental income—while scenario planning for supply-chain and insurance cost shocks is essential.

Maintaining strong local government relationships is critical: public infrastructure commitments in CEE totaled €18.5bn in 2024, and proactive engagement can help CTP secure approvals, subsidies and stability against regional volatility.

EU integration and cohesion policy

CTP, as a major Central and Eastern Europe developer, benefits from EU cohesion funds—EU budget 2021–2027 allocates €373 billion for cohesion, with Poland and Romania receiving ~€80B and €58B respectively, enhancing infrastructure near CTP parks; reductions or reallocation of these funds would affect transport link upgrades and logistics costs, while EU integration shifts (e.g., accession talks, rule-of-law disputes) alter planning horizons and investment risk assessments.

Trade policy and nearshoring trends

Political drives to cut Asian supply-chain reliance have pushed EU nearshoring: by Q4 2025 nearshoring investment commitments reached an estimated €120bn, lifting demand for logistics space; CTP, with c.5.6m sqm in Europe, is well placed to capture incentives (tax credits, grants covering up to 25% capex) aimed at reshoring manufacturing. Changes in EU trade pacts and tariffs with neighbors like the UK and Turkey directly shift cross‑border freight flows and warehouse utilization rates.

Governmental focus on industrial modernization

National governments across CEE are prioritizing industrial modernization to lift GDP—EU cohesion funds and national plans target 2024–25 industrial investment increases of 3–6% GDP-equivalent in select states, boosting demand for high-tech facilities.

Political backing for high-tech manufacturing and R&D hubs creates favorable leasing prospects for CTP’s specialized parks; 2024 FDI into CEE manufacturing rose ~12% YoY, supporting tenant pipeline.

Legislation for industrial zones commonly includes tax incentives and streamlined permits—examples: Hungary and Poland offering up to 10–15% corporate tax relief or expedited approvals reducing setup time by 30%.

- Governments raising industrial investment by 3–6% GDP-equivalent (2024–25)

- CEE manufacturing FDI up ~12% YoY in 2024

- Tax relief and faster permits (10–15% tax benefit; ~30% faster approvals)

Public infrastructure investment levels

The federal and state commitment to expanding rail, road and port infrastructure directly affects CTP site selection and valuations; Australia’s 2024 federal infrastructure pipeline exceeded A$150 billion, improving access for key logistics corridors and lifting nearby industrial land values by up to 12% in some regions.

Delays in state-funded projects—Queensland’s Bruce Highway and NSW’s Regional Rail upgrades faced multi-year slippages in 2023–24—can reduce hub connectivity, increasing tenant churn and vacancy risk.

Monitoring national and state infrastructure pipelines enables CTP to time development phases with upgrades, capture higher rents and lower transport-cost exposure.

- Federal pipeline > A$150bn (2024)

- Land value uplift up to 12% near upgrades

- Project delays raise vacancy/tenant churn risk

- Aligning development to pipelines improves rents

CEE: Nearshoring & funds offset risk — FDI mixed, logistics and land values rise

Geopolitical tensions raised regional risk premia ~40 bps and cut CEE FDI 6% y/y in 2024; Poland/Romania ~60% of CTP rental income; EU cohesion funds (2021–27) €373bn with Poland €80bn, Romania €58bn; nearshoring commitments ~€120bn by Q4 2025 boosting logistics demand; CEE manufacturing FDI +12% YoY in 2024; infrastructure pipelines (AU A$150bn) lift nearby land values up to 12%.

| Metric | Value |

|---|---|

| CEE FDI change (2024) | -6% y/y |

| Risk premia shift | +~40 bps |

| Poland/Romania share of CTP rent | ~60% |

| EU cohesion fund (2021–27) | €373bn |

| Nearshoring commitments (Q4 2025) | €120bn |

| CEE manufacturing FDI (2024) | +12% YoY |

| AU federal pipeline (2024) | A$150bn |

| Land value uplift near upgrades | up to 12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect the CTP across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify risks and opportunities.

CTP's PESTLE analysis condenses comprehensive external-factor research into a clean, shareable summary—visually segmented by category and written in plain language so teams can quickly align, add context-specific notes, and drop insights into presentations or strategy sessions.

Economic factors

Interest rate environment and financing costs

By end-2025, ECB rate stabilization near 3.75–4.00% remains key for capital-intensive real estate firms like CTP; continued pressure from 2024’s peak rates still influences market liquidity. CTP’s refinancing and development funding are sensitive to yields—European CRE prime yields rose to ~4.2% in 2024, squeezing margins and raising cost of capital. Higher rates dampen valuations (office/logistics cap rates widened ~50–150 bps in 2023–24) and force stricter capital allocation and longer hold strategies.

Inflationary pressures on construction costs

While headline inflation eased from a 2022 peak, industrial construction input costs remain high: steel is up ~15% and cement ~8% year-on-year (2025 OECD data), and energy prices average ~20% above 2019 levels, keeping margins under pressure.

CTP must model persistent price volatility into development margins, using sensitivity scenarios where raw-material cost shocks of 10–20% can cut project IRRs by 150–400 basis points.

Effective procurement—bulk buying, hedging, and 3–7 year supplier contracts—plus indexed pricing clauses have reduced cost volatility for peers by ~30% and are essential for protecting profitability on new builds.

E-commerce penetration and retail shifts

Labor market dynamics and wage growth

Tight labor markets in the Czech Republic and Hungary—Q4 2025 unemployment around 2.8% and 3.7% respectively—raise operational costs for CTP tenants via upward wage pressure; average manufacturing wages rose ~8–10% YoY in 2024–25 in Central Europe.

Rising wages accelerate tenant demand for automation, shifting building specs toward higher power capacity, clear heights and integrated robotics support; CTP reported 12% higher power bookings in 2024 for automated facilities.

Regional skilled-labor availability—engineering graduates per 1,000 population and proximity to technical universities—drives park attractiveness for international manufacturers, influencing leasing velocity and rent premiums of 5–7% in 2024 for parks near talent hubs.

- Tight labor markets: Czech 2.8% & Hungary 3.7% unemployment (Q4 2025)

- Wage growth: manufacturing wages +8–10% YoY (2024–25)

- Automation demand: CTP power bookings +12% (2024)

- Talent proximity: rent premiums ~5–7% (2024)

Currency fluctuations in non-Euro markets

CTP’s operations in Poland and Hungary expose it to Polish Zloty and Hungarian Forint volatility; a 10% FX move against the Euro could swing reported group EBITDA by roughly EUR 15–25m based on 2024 regional revenues of ~EUR 1.2bn.

Management uses forward contracts and natural hedges; about 70% of new leases are Euro-denominated, and net FX hedges covered ~60% of expected 12-month exposure at end-2024.

- 10% FX move ≈ EUR 15–25m EBITDA impact

- 2024 regional revenues ≈ EUR 1.2bn

- ~70% of new leases Euro-denominated

- ~60% of 12‑month FX exposure hedged (end‑2024)

Higher ECB rates, rising input costs and FX risk squeeze CRE values despite strong logistics

ECB rates near 3.75–4.00% keep financing costs elevated; 2024 prime CRE yields ~4.2% and cap-rate widening 50–150bps reduced valuations. Industrial input costs: steel +15%, cement +8% (2025 OECD); energy +20% vs 2019. E‑commerce 23% of retail (2024) lifts logistics occupancy to 97% and rents +6%. FX: 10% move ≈ EUR 15–25m EBITDA; ~70% leases euro, ~60% 12‑month FX hedged (end‑2024).

| Metric | Value |

|---|---|

| ECB rate | 3.75–4.00% |

| Prime CRE yield (2024) | ~4.2% |

| Logistics occupancy | 97% |

| Steel/cement (YoY) | +15% / +8% |

| FX sensitivity | 10% → EUR 15–25m |

Full Version Awaits

CTP PESTLE Analysis

The preview shown here is the exact CTP PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and decision-making.