Cumulus Media Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Cumulus Media faces intense industry pressures from digital ad platforms and streaming substitutes, moderate buyer power from advertisers, and limited supplier leverage, creating a challenging but navigable landscape for strategic action.

Suppliers Bargaining Power

High-Profile On-Air Talent

Elite on-air personalities and podcasters give suppliers high leverage: e.g., top hosts can lift station ad rates by 10–25% and Cumulus reported talent-related cash costs of $360M in 2024, so losing a star risks sizable revenue drops.

Music Licensing and Performance Rights Organizations

Entities such as ASCAP, BMI, and SESAC set statutory royalties for performance rights, giving them strong leverage over Cumulus Media’s music-formatted stations; Cumulus cannot operate those stations without licenses.

In 2023 U.S. performance royalties rose after rate settlements—ASCAP/BMI deals implied mid-single-digit percentage increases that, applied to Cumulus’s 2024 music airtime revenue (~$400M radio segment 2024 pro forma), cut margins.

Any future statutory increase feeds directly to operating costs and reduces EBITDA unless offset by ad rate hikes or cost cuts; negotiation space is minimal.

Technology and Digital Infrastructure Providers

As Cumulus shifts to an audio-first digital strategy, it depends on cloud hosting, streaming and analytics vendors that power Westwood One Podcast Network and ad-insertion tools; in 2025 Cumulus reported over 260M monthly podcast downloads, raising reliance on these stacks. Switching costs—data migration, retooling ad workflows—are high, so vendors can press for higher fees or service terms. Major providers' concentration gives them pricing leverage and contract control.

Syndicated Content and News Feed Providers

The company relies on external suppliers for specialized syndicated programming and international news feeds to maintain a 24-hour schedule; these partnerships remain critical despite in-house content production. In 2024 Cumulus Media reported 2023 total revenue of $910 million, and proprietary content reduces but does not eliminate third‑party spend on premium feeds. Dependence on a few high‑quality providers limits bargaining leverage and keeps procurement costs sticky.

- Key reliance: syndicated news/feeds

- 2023 revenue: $910 million (Cumulus Media)

- Limited suppliers → weaker price leverage

- In-house content lowers but won’t remove supplier need

Professional Sports Leagues and Teams

Securing live sports rights is a high-stakes market where leagues (NFL, NBA, MLB) hold leverage because live sports are scarce and drive strong male audiences advertisers pay premiums for; in 2024 U.S. sports rights exceeded $25B, keeping bargaining power with leagues.

For Cumulus, rising rights costs squeeze margins and force programming trade-offs—paying more reduces local ad inventory and increases risk if ratings dip.

- Live sports rights >$25B U.S. (2024)

- Male 18–49 premium for advertisers

- Higher rights cost → margin pressure for Cumulus

Supplier Power Strangles Cumulus: Talent, Royalties & Rights Squeeze Margins

Suppliers—talent, PROs (ASCAP/BMI/SESAC), cloud/streaming vendors, syndicated feeds, and leagues—hold high bargaining power over Cumulus; talent costs were $360M in 2024, 2023 revenue $910M, music airtime ~$400M (2024 pro forma), podcast downloads >260M/month (2025), and US sports rights >$25B (2024), all squeezing margins and raising switching costs.

| Supplier | Key 2023–25 Metric | Impact |

|---|---|---|

| On-air talent | $360M talent cash costs (2024) | High churn risk; raises ad rates |

| Performance rights | Music airtime ~$400M (2024) | Statutory royalty hikes cut margins |

| Cloud/streaming | 260M podcast downloads/month (2025) | High switching costs; vendor leverage |

| Sports leagues | US rights >$25B (2024) | Premium cost pressure on inventory |

What is included in the product

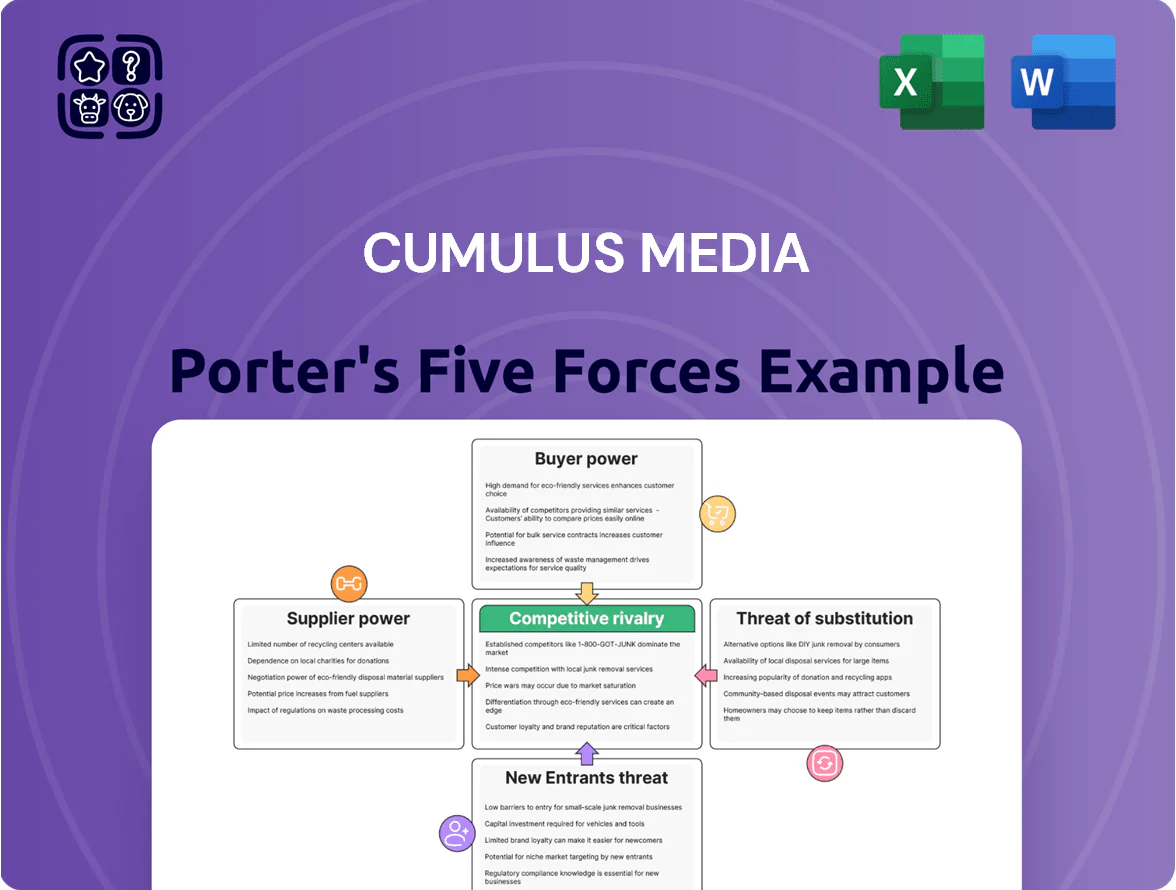

Comprehensive Porter’s Five Forces assessment tailored to Cumulus Media, highlighting competitive rivalry, buyer/supplier power, threats from substitutes and entrants, and strategic implications for pricing, profitability, and market positioning.

A concise Porter's Five Forces snapshot for Cumulus Media—quickly highlights competitive intensity and strategic levers to reduce risk and guide decisions.

Customers Bargaining Power

Consolidated Advertising Agencies

Large national ad agencies control roughly 60% of U.S. media buys and bundle dozens of brands, pressing for volume discounts and multi-channel deals; they demand granular attribution and cross-platform reach across radio and podcasts, where podcast ad revenue hit $2.1B in 2024. If Cumulus cannot match agency pricing, targeting, or measurement, agencies can shift spend to iHeart, Audacy, or digital-only platforms that offer better CPMs and programmatic scale.

Local Small Business Advertisers

Local small-business advertisers have less clout than national agencies but are highly ROI- and recession-sensitive; SMB ad spend fell about 22% in 2023 during tight local markets, per BIA Advisory. In a Cumulus market they can switch to radio, local newspapers, or social media—49% of local ad dollars flowed to digital in 2024—so Cumulus faces quick budget shifts. Their collective power forces competitive local rates and high service levels to retain short-term accounts.

Digital Programmatic Ad Buyers

Programmatic buyers using automated real-time bidding have shifted power to demand side platforms, commoditizing Cumulus Media’s ad inventory and forcing rates down as spots are compared to a global digital-audio pool; eMarketer estimated programmatic audio ad spend reached $1.1B in 2024, up 32% year-over-year.

Buyers prioritize CPM efficiency and audience targeting over station relationships, increasing revenue volatility for Cumulus—programmatic ad pricing volatility rose ~18% in 2024 per MediaRadar, squeezing long-term CPMs.

Listener Demands for Content Quality

Listeners now wield outsized power: over 80% of US adults used streaming audio or radio apps monthly in 2024, so if Cumulus’ programming quality slips or ad load rises, listeners can instantly switch to Spotify, Apple, or podcasts.

That churn cuts Cumulus’ sold reach and frequency, lowering ad CPMs and revenue; in 2024 radio ad CPMs fell ~3% YoY amid audience fragmentation.

- High listener choice: 80%+ monthly audio users (2024)

- Instant switching reduces reach/frequency

- Higher ad loads → higher churn → lower CPMs (radio CPMs -3% YoY 2024)

Measurement and Accountability Expectations

Agencies Dominate as Digital Audio Booms; SMB Cuts and CPM Pressure Loom

Buyers hold strong: national agencies control ~60% of U.S. media buys (2024), programmatic audio grew to $1.1B (+32% YoY 2024), digital audio spend ~$5.7B (2024), local SMB spend fell ~22% in 2023; listeners: 80%+ monthly audio users (2024) → high switch risk; Cumulus investing millions in measurement to protect CPMs (radio CPMs -3% YoY 2024).

| Metric | Value |

|---|---|

| Agency share | ~60% (2024) |

| Programmatic audio | $1.1B (2024) |

| Digital audio spend | $5.7B (2024) |

| Local SMB spend shock | -22% (2023) |

| Monthly audio users | 80%+ (2024) |

| Radio CPMs | -3% YoY (2024) |

Preview the Actual Deliverable

Cumulus Media Porter's Five Forces Analysis

This preview shows the exact Cumulus Media Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples.

The document is fully formatted and ready for use, covering supplier power, buyer power, competitive rivalry, threat of substitution, and barriers to entry in detail.

Once you complete your purchase, you’ll get instant access to this same file for download and application.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Cumulus Media faces intense industry pressures from digital ad platforms and streaming substitutes, moderate buyer power from advertisers, and limited supplier leverage, creating a challenging but navigable landscape for strategic action.

Suppliers Bargaining Power

High-Profile On-Air Talent

Elite on-air personalities and podcasters give suppliers high leverage: e.g., top hosts can lift station ad rates by 10–25% and Cumulus reported talent-related cash costs of $360M in 2024, so losing a star risks sizable revenue drops.

Music Licensing and Performance Rights Organizations

Entities such as ASCAP, BMI, and SESAC set statutory royalties for performance rights, giving them strong leverage over Cumulus Media’s music-formatted stations; Cumulus cannot operate those stations without licenses.

In 2023 U.S. performance royalties rose after rate settlements—ASCAP/BMI deals implied mid-single-digit percentage increases that, applied to Cumulus’s 2024 music airtime revenue (~$400M radio segment 2024 pro forma), cut margins.

Any future statutory increase feeds directly to operating costs and reduces EBITDA unless offset by ad rate hikes or cost cuts; negotiation space is minimal.

Technology and Digital Infrastructure Providers

As Cumulus shifts to an audio-first digital strategy, it depends on cloud hosting, streaming and analytics vendors that power Westwood One Podcast Network and ad-insertion tools; in 2025 Cumulus reported over 260M monthly podcast downloads, raising reliance on these stacks. Switching costs—data migration, retooling ad workflows—are high, so vendors can press for higher fees or service terms. Major providers' concentration gives them pricing leverage and contract control.

Syndicated Content and News Feed Providers

The company relies on external suppliers for specialized syndicated programming and international news feeds to maintain a 24-hour schedule; these partnerships remain critical despite in-house content production. In 2024 Cumulus Media reported 2023 total revenue of $910 million, and proprietary content reduces but does not eliminate third‑party spend on premium feeds. Dependence on a few high‑quality providers limits bargaining leverage and keeps procurement costs sticky.

- Key reliance: syndicated news/feeds

- 2023 revenue: $910 million (Cumulus Media)

- Limited suppliers → weaker price leverage

- In-house content lowers but won’t remove supplier need

Professional Sports Leagues and Teams

Securing live sports rights is a high-stakes market where leagues (NFL, NBA, MLB) hold leverage because live sports are scarce and drive strong male audiences advertisers pay premiums for; in 2024 U.S. sports rights exceeded $25B, keeping bargaining power with leagues.

For Cumulus, rising rights costs squeeze margins and force programming trade-offs—paying more reduces local ad inventory and increases risk if ratings dip.

- Live sports rights >$25B U.S. (2024)

- Male 18–49 premium for advertisers

- Higher rights cost → margin pressure for Cumulus

Supplier Power Strangles Cumulus: Talent, Royalties & Rights Squeeze Margins

Suppliers—talent, PROs (ASCAP/BMI/SESAC), cloud/streaming vendors, syndicated feeds, and leagues—hold high bargaining power over Cumulus; talent costs were $360M in 2024, 2023 revenue $910M, music airtime ~$400M (2024 pro forma), podcast downloads >260M/month (2025), and US sports rights >$25B (2024), all squeezing margins and raising switching costs.

| Supplier | Key 2023–25 Metric | Impact |

|---|---|---|

| On-air talent | $360M talent cash costs (2024) | High churn risk; raises ad rates |

| Performance rights | Music airtime ~$400M (2024) | Statutory royalty hikes cut margins |

| Cloud/streaming | 260M podcast downloads/month (2025) | High switching costs; vendor leverage |

| Sports leagues | US rights >$25B (2024) | Premium cost pressure on inventory |

What is included in the product

Comprehensive Porter’s Five Forces assessment tailored to Cumulus Media, highlighting competitive rivalry, buyer/supplier power, threats from substitutes and entrants, and strategic implications for pricing, profitability, and market positioning.

A concise Porter's Five Forces snapshot for Cumulus Media—quickly highlights competitive intensity and strategic levers to reduce risk and guide decisions.

Customers Bargaining Power

Consolidated Advertising Agencies

Large national ad agencies control roughly 60% of U.S. media buys and bundle dozens of brands, pressing for volume discounts and multi-channel deals; they demand granular attribution and cross-platform reach across radio and podcasts, where podcast ad revenue hit $2.1B in 2024. If Cumulus cannot match agency pricing, targeting, or measurement, agencies can shift spend to iHeart, Audacy, or digital-only platforms that offer better CPMs and programmatic scale.

Local Small Business Advertisers

Local small-business advertisers have less clout than national agencies but are highly ROI- and recession-sensitive; SMB ad spend fell about 22% in 2023 during tight local markets, per BIA Advisory. In a Cumulus market they can switch to radio, local newspapers, or social media—49% of local ad dollars flowed to digital in 2024—so Cumulus faces quick budget shifts. Their collective power forces competitive local rates and high service levels to retain short-term accounts.

Digital Programmatic Ad Buyers

Programmatic buyers using automated real-time bidding have shifted power to demand side platforms, commoditizing Cumulus Media’s ad inventory and forcing rates down as spots are compared to a global digital-audio pool; eMarketer estimated programmatic audio ad spend reached $1.1B in 2024, up 32% year-over-year.

Buyers prioritize CPM efficiency and audience targeting over station relationships, increasing revenue volatility for Cumulus—programmatic ad pricing volatility rose ~18% in 2024 per MediaRadar, squeezing long-term CPMs.

Listener Demands for Content Quality

Listeners now wield outsized power: over 80% of US adults used streaming audio or radio apps monthly in 2024, so if Cumulus’ programming quality slips or ad load rises, listeners can instantly switch to Spotify, Apple, or podcasts.

That churn cuts Cumulus’ sold reach and frequency, lowering ad CPMs and revenue; in 2024 radio ad CPMs fell ~3% YoY amid audience fragmentation.

- High listener choice: 80%+ monthly audio users (2024)

- Instant switching reduces reach/frequency

- Higher ad loads → higher churn → lower CPMs (radio CPMs -3% YoY 2024)

Measurement and Accountability Expectations

Agencies Dominate as Digital Audio Booms; SMB Cuts and CPM Pressure Loom

Buyers hold strong: national agencies control ~60% of U.S. media buys (2024), programmatic audio grew to $1.1B (+32% YoY 2024), digital audio spend ~$5.7B (2024), local SMB spend fell ~22% in 2023; listeners: 80%+ monthly audio users (2024) → high switch risk; Cumulus investing millions in measurement to protect CPMs (radio CPMs -3% YoY 2024).

| Metric | Value |

|---|---|

| Agency share | ~60% (2024) |

| Programmatic audio | $1.1B (2024) |

| Digital audio spend | $5.7B (2024) |

| Local SMB spend shock | -22% (2023) |

| Monthly audio users | 80%+ (2024) |

| Radio CPMs | -3% YoY (2024) |

Preview the Actual Deliverable

Cumulus Media Porter's Five Forces Analysis

This preview shows the exact Cumulus Media Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples.

The document is fully formatted and ready for use, covering supplier power, buyer power, competitive rivalry, threat of substitution, and barriers to entry in detail.

Once you complete your purchase, you’ll get instant access to this same file for download and application.