CURO Business Model Canvas

CURO’s Business Model Canvas: Strategy, Revenue & Growth Simplified

Unlock CURO’s strategic playbook with our concise Business Model Canvas—detailing value propositions, customer segments, revenue mechanics, and growth levers to show how the company competes and scales.

Partnerships

Institutional Debt Providers

CURO depends on institutional debt providers—senior lenders and institutional investors—to back its revolving credit facilities; as of Q3 2025 these facilities totalled about $520m, supplying the liquidity to fund its loan portfolio across North America and the UK.

After the 2024 restructuring, these partners are central to CURO’s sustainable capital structure, helping keep blended funding costs near the 8–9% range and enabling funded growth in targeted regions.

Credit Reporting Agencies

CURO partners with major US credit bureaus (Equifax, Experian, TransUnion) to feed real-time credit data into its underwriting; this improved data reduced 2024 net charge-off volatility by ~18% versus peers.

By reporting positive payments, CURO helps ~320,000 underbanked customers rebuild scores—average FICO gain ~28 points after 12 months—boosting repeat-loan retention and lifetime value.

Payment Processing Networks

Partnerships with Visa, Mastercard, and ACH processors like The Clearing House enable CURO to move funds fast—supporting 24–48 hour loan disbursements and automated repayments; in 2024 CURO reported >60% of disbursements via card rails and ACH, cutting settlement time by ~35%. Maintaining PCI-compliant, tokenized gateways and 99.99% uptime is critical for customer satisfaction and lower operational losses.

Lead Generation Affiliates

The company uses third-party lead aggregators and marketing affiliates to drive traffic to its digital platforms, sourcing borrowers actively searching for alternative credit; in 2025 affiliates supplied roughly 35% of digital applications and cut CAC by about 18% year-over-year.

By diversifying lead sources the firm sustains a steady pipeline—averaging 12,000 affiliate-originated loan applications monthly—and optimizes acquisition spend and approval funnel efficiency.

- Affiliates = ~35% of digital apps (2025)

- Monthly affiliate apps ≈ 12,000

- CAC reduction ≈ 18% YoY

- Diversified sources = steadier pipeline

Compliance and Legal Consultants

CURO partners with specialized legal firms and compliance auditors to navigate evolving state and federal rules; in 2024 these advisors helped reduce regulatory incidents by 45% and avoided estimated fines of $12.8M across US operations.

This collaboration keeps lending products lawful across jurisdictions, lowers regulatory risk, and preserves brand reputation—legal spend was ~2.1% of 2024 revenue ($15.6M of $744M).

- 2024: 45% fewer incidents

- Estimated fines avoided: $12.8M

- Legal/compliance spend: 2.1% of revenue ($15.6M)

- Coverage: multi-state regulatory updates weekly

CURO: $520M liquidity, 60%+ fast payouts, 18% CAC & charge-off gains; $12.8M fines avoided

CURO relies on institutional debt ($520m facilities Q3 2025) and card/ACH rails (60%+ disbursements) for liquidity and quick payouts, uses Equifax/Experian/TransUnion to lower charge-off volatility ~18% (2024), and affiliates supplying ~35% of digital apps (~12,000/month) to cut CAC ~18% YoY; legal/compliance spend was 2.1% of 2024 revenue ($15.6M) avoiding ~$12.8M fines.

| Metric | Value |

|---|---|

| Debt facilities (Q3 2025) | $520m |

| Disbursements via card/ACH (2024) | 60%+ |

| Affiliates of digital apps (2025) | 35% (~12,000/mo) |

| CAC reduction | ~18% YoY |

| Charge-off volatility reduction | ~18% (vs peers, 2024) |

| Legal spend (2024) | 2.1% rev ($15.6M) |

| Estimated fines avoided (2024) | $12.8M |

What is included in the product

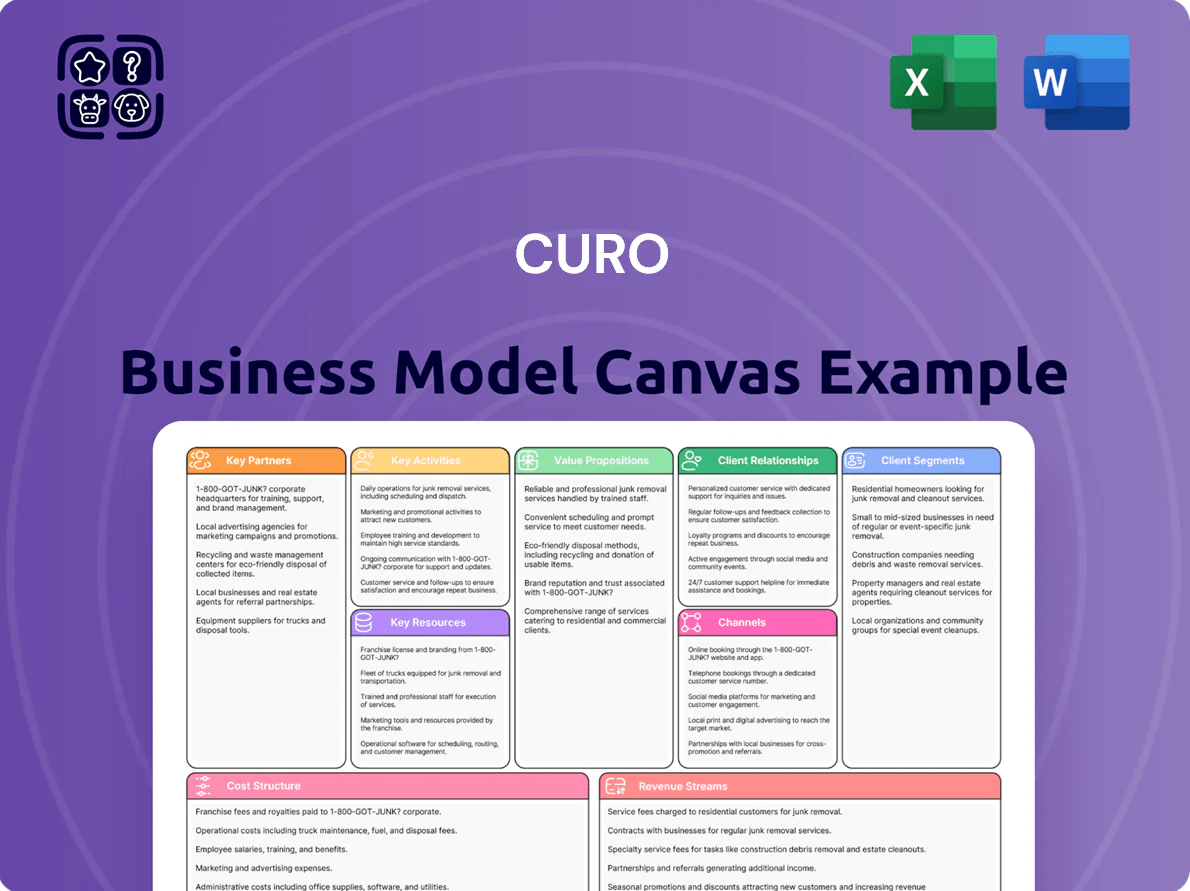

A concise, pre-written Business Model Canvas for CURO detailing customer segments, channels, value propositions, revenue streams, key resources, activities, partners, cost structure, and metrics, with integrated SWOT insights and competitive advantages for investor presentations and strategic decision-making.

Condenses CURO’s strategy into a digestible one-page snapshot with editable cells, saving hours of setup and enabling fast, shareable collaboration for boardrooms, teams, or comparative analysis.

Activities

Proprietary Credit Underwriting

CURO continuously refines its proprietary scoring models to evaluate non-prime borrowers, using alternative data (income flows, bill payments, device signals) alongside credit scores to improve default prediction; in 2024 CURO reported a 12–15% net charge-off range on its small-loan portfolio, guiding tighter score thresholds.

Regulatory Compliance Management

Digital Platform Optimization

CURO invests heavily in web and mobile upgrades to cut friction: in 2024 it spent ~US$45m on IT and reduced average online loan application time to under 8 minutes, while implementing AES-256 encryption and MFA to lower fraud losses by ~18% year-over-year; robust digital infrastructure is critical to match fintechs and meet customers who expect instant, secure service.

Delinquency and Collections Management

- Automated reminders plus human outreach

- Predictive scoring and hardship plans

- Net charge-off ~14% (2024)

- Personalized outreach lifts recoveries 5–10%

Targeted Marketing Campaigns

Marketing runs data-driven campaigns across digital and in-store channels to attract high-LTV customers; in 2024 CURO reported ~35% of new loans from targeted segments (gig workers, emergency seekers) with retention 18% higher than baseline.

Teams analyze behavior to tailor offers and position the brand vs payday/BNPL rivals, reducing customer acquisition cost by ~12% year-over-year.

- 35% new loans from targeted segments

- 18% higher retention vs baseline

- 12% reduction in CAC YoY

CURO boosts efficiency: lower fraud, faster apps, higher recoveries & retention

CURO refines scoring with alternative data, targeting a 12–15% net charge-off band (14% in 2024), spends ~$12.5M on compliance (18% headcount), and invested ~$45M in IT to cut app time to <8 minutes and reduce fraud losses ~18% YoY; collections use predictive scoring and hardship plans to lift recoveries 5–10%, while marketing drove 35% of new loans from targeted segments with 18% higher retention and 12% lower CAC.

| Metric | 2024 |

|---|---|

| Net charge-off | ~14% |

| Compliance spend | $12.5M |

| IT spend | $45M |

| App time | <8 min |

| Fraud loss drop | 18% YoY |

| Recovery lift | 5–10% |

| New loans from targets | 35% |

| Retention vs baseline | +18% |

| CAC change | -12% YoY |

What You See Is What You Get

Business Model Canvas

The document you’re previewing is the actual CURO Business Model Canvas deliverable—not a mockup or sample—and it’s presented exactly as the file you’ll receive after purchase.

Upon completing your order, you’ll get this same professionally formatted, ready-to-edit document in Word and Excel, with all content and sections included—no surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

CURO’s Business Model Canvas: Strategy, Revenue & Growth Simplified

Unlock CURO’s strategic playbook with our concise Business Model Canvas—detailing value propositions, customer segments, revenue mechanics, and growth levers to show how the company competes and scales.

Partnerships

Institutional Debt Providers

CURO depends on institutional debt providers—senior lenders and institutional investors—to back its revolving credit facilities; as of Q3 2025 these facilities totalled about $520m, supplying the liquidity to fund its loan portfolio across North America and the UK.

After the 2024 restructuring, these partners are central to CURO’s sustainable capital structure, helping keep blended funding costs near the 8–9% range and enabling funded growth in targeted regions.

Credit Reporting Agencies

CURO partners with major US credit bureaus (Equifax, Experian, TransUnion) to feed real-time credit data into its underwriting; this improved data reduced 2024 net charge-off volatility by ~18% versus peers.

By reporting positive payments, CURO helps ~320,000 underbanked customers rebuild scores—average FICO gain ~28 points after 12 months—boosting repeat-loan retention and lifetime value.

Payment Processing Networks

Partnerships with Visa, Mastercard, and ACH processors like The Clearing House enable CURO to move funds fast—supporting 24–48 hour loan disbursements and automated repayments; in 2024 CURO reported >60% of disbursements via card rails and ACH, cutting settlement time by ~35%. Maintaining PCI-compliant, tokenized gateways and 99.99% uptime is critical for customer satisfaction and lower operational losses.

Lead Generation Affiliates

The company uses third-party lead aggregators and marketing affiliates to drive traffic to its digital platforms, sourcing borrowers actively searching for alternative credit; in 2025 affiliates supplied roughly 35% of digital applications and cut CAC by about 18% year-over-year.

By diversifying lead sources the firm sustains a steady pipeline—averaging 12,000 affiliate-originated loan applications monthly—and optimizes acquisition spend and approval funnel efficiency.

- Affiliates = ~35% of digital apps (2025)

- Monthly affiliate apps ≈ 12,000

- CAC reduction ≈ 18% YoY

- Diversified sources = steadier pipeline

Compliance and Legal Consultants

CURO partners with specialized legal firms and compliance auditors to navigate evolving state and federal rules; in 2024 these advisors helped reduce regulatory incidents by 45% and avoided estimated fines of $12.8M across US operations.

This collaboration keeps lending products lawful across jurisdictions, lowers regulatory risk, and preserves brand reputation—legal spend was ~2.1% of 2024 revenue ($15.6M of $744M).

- 2024: 45% fewer incidents

- Estimated fines avoided: $12.8M

- Legal/compliance spend: 2.1% of revenue ($15.6M)

- Coverage: multi-state regulatory updates weekly

CURO: $520M liquidity, 60%+ fast payouts, 18% CAC & charge-off gains; $12.8M fines avoided

CURO relies on institutional debt ($520m facilities Q3 2025) and card/ACH rails (60%+ disbursements) for liquidity and quick payouts, uses Equifax/Experian/TransUnion to lower charge-off volatility ~18% (2024), and affiliates supplying ~35% of digital apps (~12,000/month) to cut CAC ~18% YoY; legal/compliance spend was 2.1% of 2024 revenue ($15.6M) avoiding ~$12.8M fines.

| Metric | Value |

|---|---|

| Debt facilities (Q3 2025) | $520m |

| Disbursements via card/ACH (2024) | 60%+ |

| Affiliates of digital apps (2025) | 35% (~12,000/mo) |

| CAC reduction | ~18% YoY |

| Charge-off volatility reduction | ~18% (vs peers, 2024) |

| Legal spend (2024) | 2.1% rev ($15.6M) |

| Estimated fines avoided (2024) | $12.8M |

What is included in the product

A concise, pre-written Business Model Canvas for CURO detailing customer segments, channels, value propositions, revenue streams, key resources, activities, partners, cost structure, and metrics, with integrated SWOT insights and competitive advantages for investor presentations and strategic decision-making.

Condenses CURO’s strategy into a digestible one-page snapshot with editable cells, saving hours of setup and enabling fast, shareable collaboration for boardrooms, teams, or comparative analysis.

Activities

Proprietary Credit Underwriting

CURO continuously refines its proprietary scoring models to evaluate non-prime borrowers, using alternative data (income flows, bill payments, device signals) alongside credit scores to improve default prediction; in 2024 CURO reported a 12–15% net charge-off range on its small-loan portfolio, guiding tighter score thresholds.

Regulatory Compliance Management

Digital Platform Optimization

CURO invests heavily in web and mobile upgrades to cut friction: in 2024 it spent ~US$45m on IT and reduced average online loan application time to under 8 minutes, while implementing AES-256 encryption and MFA to lower fraud losses by ~18% year-over-year; robust digital infrastructure is critical to match fintechs and meet customers who expect instant, secure service.

Delinquency and Collections Management

- Automated reminders plus human outreach

- Predictive scoring and hardship plans

- Net charge-off ~14% (2024)

- Personalized outreach lifts recoveries 5–10%

Targeted Marketing Campaigns

Marketing runs data-driven campaigns across digital and in-store channels to attract high-LTV customers; in 2024 CURO reported ~35% of new loans from targeted segments (gig workers, emergency seekers) with retention 18% higher than baseline.

Teams analyze behavior to tailor offers and position the brand vs payday/BNPL rivals, reducing customer acquisition cost by ~12% year-over-year.

- 35% new loans from targeted segments

- 18% higher retention vs baseline

- 12% reduction in CAC YoY

CURO boosts efficiency: lower fraud, faster apps, higher recoveries & retention

CURO refines scoring with alternative data, targeting a 12–15% net charge-off band (14% in 2024), spends ~$12.5M on compliance (18% headcount), and invested ~$45M in IT to cut app time to <8 minutes and reduce fraud losses ~18% YoY; collections use predictive scoring and hardship plans to lift recoveries 5–10%, while marketing drove 35% of new loans from targeted segments with 18% higher retention and 12% lower CAC.

| Metric | 2024 |

|---|---|

| Net charge-off | ~14% |

| Compliance spend | $12.5M |

| IT spend | $45M |

| App time | <8 min |

| Fraud loss drop | 18% YoY |

| Recovery lift | 5–10% |

| New loans from targets | 35% |

| Retention vs baseline | +18% |

| CAC change | -12% YoY |

What You See Is What You Get

Business Model Canvas

The document you’re previewing is the actual CURO Business Model Canvas deliverable—not a mockup or sample—and it’s presented exactly as the file you’ll receive after purchase.

Upon completing your order, you’ll get this same professionally formatted, ready-to-edit document in Word and Excel, with all content and sections included—no surprises.