CyberArk Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

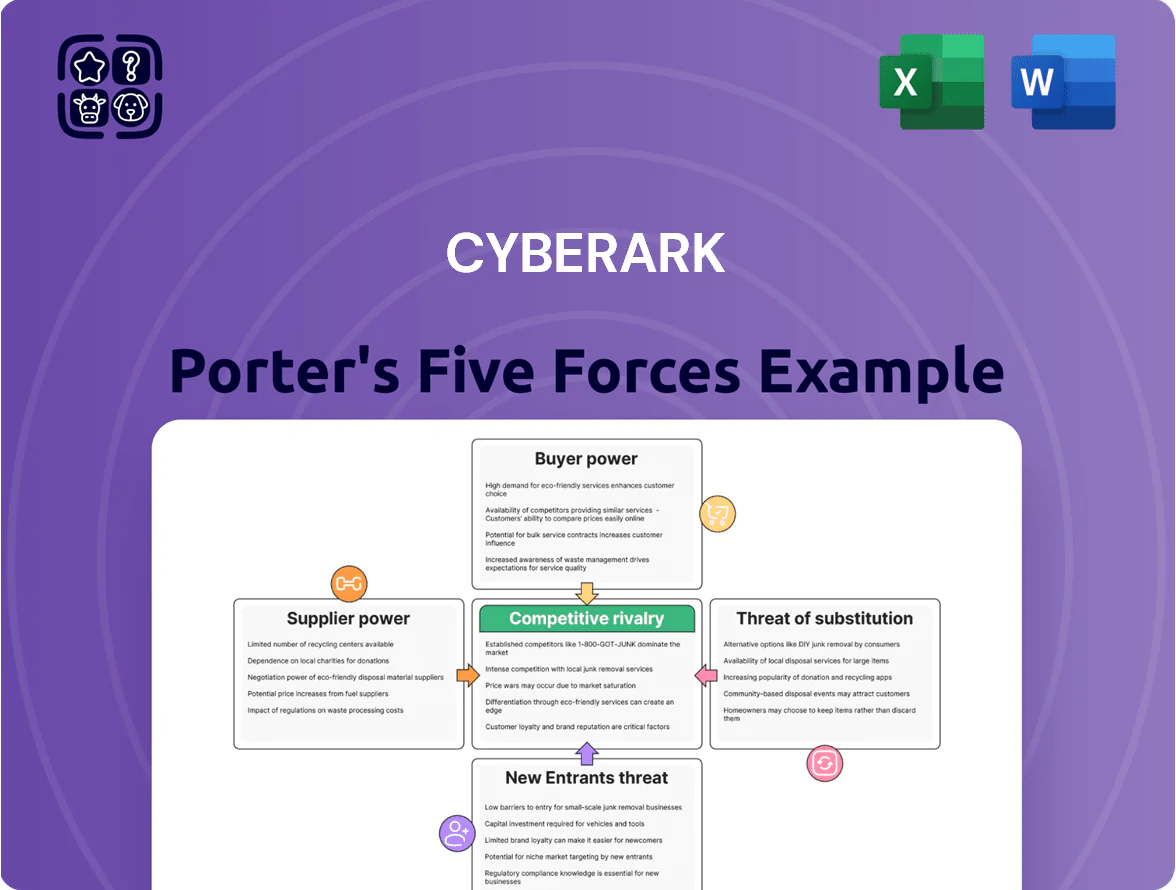

CyberArk operates in a high-stakes identity-security niche where intense rivalry, strong buyer expectations, and sophisticated substitute solutions shape strategy, while supplier leverage and barriers to entry moderate competitive risk.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore CyberArk’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cloud Infrastructure Dependence

CyberArk increasingly runs its SaaS identity platform on AWS and Azure, giving hyperscalers bargaining power through scale and integration; migrating multi-region workloads can cost hundreds of millions and take 12–24 months. As of late 2025, the top three cloud providers control ~70% of global IaaS/PaaS, making them near non‑substitutable partners for CyberArk’s uptime and compliance SLAs. This dependence raises supplier power and price/feature leverage.

Specialized Cybersecurity Talent

The global shortage of cybersecurity specialists—estimated at 3.4 million unfilled roles in 2023 and still over 3.2 million in 2024—gives elite identity-security engineers outsized leverage, forcing CyberArk to compete worldwide to sustain its Privileged Access Management and AI detection edge.

Average total compensation for senior security researchers rose ~15–25% in 2023–24; this wage pressure and the niche skill set make human capital a high-leverage supplier group for CyberArk’s product roadmap and time-to-market.

Third-Party Software Components

CyberArk integrates many open-source and proprietary third-party libraries to speed development, and while single components are often replaceable, integration and security validation create dependency on specific vendors. In 2024, supply-chain incidents rose 42% year-over-year, showing the risk that a vendor disruption could delay CyberArk releases and increase remediation costs. License changes or fee hikes can squeeze product gross margins—CyberArk reported 73% gross margin in FY2024, so a modest 200–300 bps pressure would reduce profitability noticeably. Replacing validated components can add 3–6 months to development cycles, raising time-to-market risk.

Data Center and Hardware Providers

Data center and hardware providers still hold bargaining power over CyberArk for on-premise deployments via long-term SLAs and specialized infrastructure needed to host sensitive identity security workloads, though these represent a shrinking share of revenue as CyberArk reported ~28% on-prem revenue in FY2024 (Sep 2023–Aug 2024).

As CyberArk shifts to subscription and SaaS—cloud ARR grew ~34% in FY2024—serverless and cloud-native trends reduce supplier leverage by enabling deployments that bypass dedicated hardware.

- On-premise reliance: ~28% of FY2024 revenue

- Cloud/SaaS growth: cloud ARR +34% FY2024

- Supplier leverage: long-term contracts, physical security needs

- Trend: declining power due to serverless/cloud-native adoption

Regulatory and Compliance Auditors

Regulatory and compliance auditors (SOC 2, FedRAMP) act as gatekeepers for CyberArk, since their certifications are required for sales into US federal agencies and top-tier financial firms that represented roughly 45% of CyberArk’s FY2024 revenue ($468M of $1.04B total revenue).

Loss or delay of those approvals would block access to high-margin contracts—FedRAMP authorizations can take 9–18 months—and concentrate negotiation leverage with auditors who set strict remediation demands.

- Certs required: SOC 2, FedRAMP

- High-security sectors ≈45% of FY2024 revenue ($468M)

- FedRAMP timelines: 9–18 months

- Auditors can force costly remediations

Suppliers Tighten Grip: Clouds, Talent Shortages & Supply Risks Threaten $468M Revenue

Suppliers hold moderate-to-high power: hyperscale clouds (~70% IaaS/PaaS) and on‑prem vendors constrain cost and migration time (multi‑hundred‑million, 12–24 months); talent shortage (~3.2M gap in 2024) and 15–25% compensation inflation raise human-capital costs; third‑party libs and rising supply‑chain incidents (+42% in 2024) risk delays; certifications (SOC 2, FedRAMP) gate ~45% of FY2024 revenue ($468M).

| Metric | Value |

|---|---|

| Top 3 cloud share | ~70% |

| On‑prem revenue FY2024 | ~28% |

| High‑security revenue | $468M (45%) |

| Talent gap 2024 | ~3.2M |

| Supply‑chain incidents 2024 YoY | +42% |

What is included in the product

Tailored Porter's Five Forces analysis for CyberArk that uncovers competitive drivers, supplier and buyer power, entrant threats, substitutes, and strategic levers affecting its pricing, profitability, and market defense.

Concise Porter's Five Forces snapshot for CyberArk—quickly highlights competitive pressures and cybersecurity market dynamics to streamline strategic decisions.

Customers Bargaining Power

High Switching Costs

Once an enterprise integrates CyberArk into core security architecture, ripping and replacing it involves high technical complexity and costs—implementations often span 6–18 months and total cost of replacement can exceed $1m for large firms, lowering customers’ short-term bargaining power.

Privileged Access Management (PAM) is embedded in workflows and CI/CD pipelines, so renewals favor CyberArk; fiscal 2024 showed net retention above 100% (reported 103%+), reflecting stickiness despite lower-priced competitors.

Concentration of Large Enterprise Buyers

CyberArk’s revenue is concentrated in Fortune 500 firms and large government agencies, which in 2024 accounted for roughly 65–70% of enterprise bookings, giving these buyers strong negotiating leverage.

High-volume customers routinely require custom integrations, white-glove support, and volume discounts, pressuring average contract value and gross margins during renewals.

By 2025, IT vendor consolidation—IDC reports 30% fewer suppliers in large accounts since 2020—further amplifies buyer power, letting buyers consolidate spend and extract deeper discounts.

Availability of Competitive Alternatives

The presence of strong competitors like Microsoft (Azure AD, $60B cloud revenue 2024) and Okta (identity revenue $1.6B FY2024) gives buyers credible alternatives, letting them press CyberArk for lower prices or bundled features during procurement.

Price Sensitivity in Mid-Market Segments

- 44% mid-market cite cost (2024)

- 62% prefer subscription/per-seat (2024)

- Need for simpler, lower-cost tiers

Informed and Sophisticated Procurement

Buyers—usually technical CISOs—run rigorous proof-of-concept tests and compare specs; 68% of enterprise security buyers ran POCs in 2024, raising switching readiness.

Their market knowledge and vendor benchmarks limit CyberArk’s pricing power unless the company shows continuous innovation; CyberArk’s 2024 R&D spend was $228M, helping but not guaranteeing differentiation.

Objective performance metrics and third-party tests force transparent SLAs and discount pressure, reducing negotiated margins.

- 68% of enterprises used POCs in 2024

- CyberArk R&D 2024: $228M

- High technical buyer sophistication → lower pricing power

High retention but concentrated, price‑sensitive buyers force discounts and flexible tiers

Customers hold moderate-to-high bargaining power: high switching costs and 103%+ net retention (FY2024) reduce short-term pressure, but concentration in large buyers (65–70% bookings 2024), vendor consolidation (30% fewer suppliers), strong rivals (Microsoft, Okta), 68% POC use, and mid‑market price sensitivity (44% cost-focused; 62% prefer subscription) force discounts and flexible tiers.

| Metric | 2024–25 |

|---|---|

| Net retention | 103%+ |

| Large-account bookings | 65–70% |

| Vendor consolidation | 30% fewer |

| POC usage | 68% |

| Mid-market cost focus | 44% |

| Mid-market subscription preference | 62% |

What You See Is What You Get

CyberArk Porter's Five Forces Analysis

This preview shows the exact CyberArk Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups—fully formatted and ready for use; the document displayed here is the same professionally written file available for instant download once you complete payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

CyberArk operates in a high-stakes identity-security niche where intense rivalry, strong buyer expectations, and sophisticated substitute solutions shape strategy, while supplier leverage and barriers to entry moderate competitive risk.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore CyberArk’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cloud Infrastructure Dependence

CyberArk increasingly runs its SaaS identity platform on AWS and Azure, giving hyperscalers bargaining power through scale and integration; migrating multi-region workloads can cost hundreds of millions and take 12–24 months. As of late 2025, the top three cloud providers control ~70% of global IaaS/PaaS, making them near non‑substitutable partners for CyberArk’s uptime and compliance SLAs. This dependence raises supplier power and price/feature leverage.

Specialized Cybersecurity Talent

The global shortage of cybersecurity specialists—estimated at 3.4 million unfilled roles in 2023 and still over 3.2 million in 2024—gives elite identity-security engineers outsized leverage, forcing CyberArk to compete worldwide to sustain its Privileged Access Management and AI detection edge.

Average total compensation for senior security researchers rose ~15–25% in 2023–24; this wage pressure and the niche skill set make human capital a high-leverage supplier group for CyberArk’s product roadmap and time-to-market.

Third-Party Software Components

CyberArk integrates many open-source and proprietary third-party libraries to speed development, and while single components are often replaceable, integration and security validation create dependency on specific vendors. In 2024, supply-chain incidents rose 42% year-over-year, showing the risk that a vendor disruption could delay CyberArk releases and increase remediation costs. License changes or fee hikes can squeeze product gross margins—CyberArk reported 73% gross margin in FY2024, so a modest 200–300 bps pressure would reduce profitability noticeably. Replacing validated components can add 3–6 months to development cycles, raising time-to-market risk.

Data Center and Hardware Providers

Data center and hardware providers still hold bargaining power over CyberArk for on-premise deployments via long-term SLAs and specialized infrastructure needed to host sensitive identity security workloads, though these represent a shrinking share of revenue as CyberArk reported ~28% on-prem revenue in FY2024 (Sep 2023–Aug 2024).

As CyberArk shifts to subscription and SaaS—cloud ARR grew ~34% in FY2024—serverless and cloud-native trends reduce supplier leverage by enabling deployments that bypass dedicated hardware.

- On-premise reliance: ~28% of FY2024 revenue

- Cloud/SaaS growth: cloud ARR +34% FY2024

- Supplier leverage: long-term contracts, physical security needs

- Trend: declining power due to serverless/cloud-native adoption

Regulatory and Compliance Auditors

Regulatory and compliance auditors (SOC 2, FedRAMP) act as gatekeepers for CyberArk, since their certifications are required for sales into US federal agencies and top-tier financial firms that represented roughly 45% of CyberArk’s FY2024 revenue ($468M of $1.04B total revenue).

Loss or delay of those approvals would block access to high-margin contracts—FedRAMP authorizations can take 9–18 months—and concentrate negotiation leverage with auditors who set strict remediation demands.

- Certs required: SOC 2, FedRAMP

- High-security sectors ≈45% of FY2024 revenue ($468M)

- FedRAMP timelines: 9–18 months

- Auditors can force costly remediations

Suppliers Tighten Grip: Clouds, Talent Shortages & Supply Risks Threaten $468M Revenue

Suppliers hold moderate-to-high power: hyperscale clouds (~70% IaaS/PaaS) and on‑prem vendors constrain cost and migration time (multi‑hundred‑million, 12–24 months); talent shortage (~3.2M gap in 2024) and 15–25% compensation inflation raise human-capital costs; third‑party libs and rising supply‑chain incidents (+42% in 2024) risk delays; certifications (SOC 2, FedRAMP) gate ~45% of FY2024 revenue ($468M).

| Metric | Value |

|---|---|

| Top 3 cloud share | ~70% |

| On‑prem revenue FY2024 | ~28% |

| High‑security revenue | $468M (45%) |

| Talent gap 2024 | ~3.2M |

| Supply‑chain incidents 2024 YoY | +42% |

What is included in the product

Tailored Porter's Five Forces analysis for CyberArk that uncovers competitive drivers, supplier and buyer power, entrant threats, substitutes, and strategic levers affecting its pricing, profitability, and market defense.

Concise Porter's Five Forces snapshot for CyberArk—quickly highlights competitive pressures and cybersecurity market dynamics to streamline strategic decisions.

Customers Bargaining Power

High Switching Costs

Once an enterprise integrates CyberArk into core security architecture, ripping and replacing it involves high technical complexity and costs—implementations often span 6–18 months and total cost of replacement can exceed $1m for large firms, lowering customers’ short-term bargaining power.

Privileged Access Management (PAM) is embedded in workflows and CI/CD pipelines, so renewals favor CyberArk; fiscal 2024 showed net retention above 100% (reported 103%+), reflecting stickiness despite lower-priced competitors.

Concentration of Large Enterprise Buyers

CyberArk’s revenue is concentrated in Fortune 500 firms and large government agencies, which in 2024 accounted for roughly 65–70% of enterprise bookings, giving these buyers strong negotiating leverage.

High-volume customers routinely require custom integrations, white-glove support, and volume discounts, pressuring average contract value and gross margins during renewals.

By 2025, IT vendor consolidation—IDC reports 30% fewer suppliers in large accounts since 2020—further amplifies buyer power, letting buyers consolidate spend and extract deeper discounts.

Availability of Competitive Alternatives

The presence of strong competitors like Microsoft (Azure AD, $60B cloud revenue 2024) and Okta (identity revenue $1.6B FY2024) gives buyers credible alternatives, letting them press CyberArk for lower prices or bundled features during procurement.

Price Sensitivity in Mid-Market Segments

- 44% mid-market cite cost (2024)

- 62% prefer subscription/per-seat (2024)

- Need for simpler, lower-cost tiers

Informed and Sophisticated Procurement

Buyers—usually technical CISOs—run rigorous proof-of-concept tests and compare specs; 68% of enterprise security buyers ran POCs in 2024, raising switching readiness.

Their market knowledge and vendor benchmarks limit CyberArk’s pricing power unless the company shows continuous innovation; CyberArk’s 2024 R&D spend was $228M, helping but not guaranteeing differentiation.

Objective performance metrics and third-party tests force transparent SLAs and discount pressure, reducing negotiated margins.

- 68% of enterprises used POCs in 2024

- CyberArk R&D 2024: $228M

- High technical buyer sophistication → lower pricing power

High retention but concentrated, price‑sensitive buyers force discounts and flexible tiers

Customers hold moderate-to-high bargaining power: high switching costs and 103%+ net retention (FY2024) reduce short-term pressure, but concentration in large buyers (65–70% bookings 2024), vendor consolidation (30% fewer suppliers), strong rivals (Microsoft, Okta), 68% POC use, and mid‑market price sensitivity (44% cost-focused; 62% prefer subscription) force discounts and flexible tiers.

| Metric | 2024–25 |

|---|---|

| Net retention | 103%+ |

| Large-account bookings | 65–70% |

| Vendor consolidation | 30% fewer |

| POC usage | 68% |

| Mid-market cost focus | 44% |

| Mid-market subscription preference | 62% |

What You See Is What You Get

CyberArk Porter's Five Forces Analysis

This preview shows the exact CyberArk Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups—fully formatted and ready for use; the document displayed here is the same professionally written file available for instant download once you complete payment.