Cypress Environmental Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

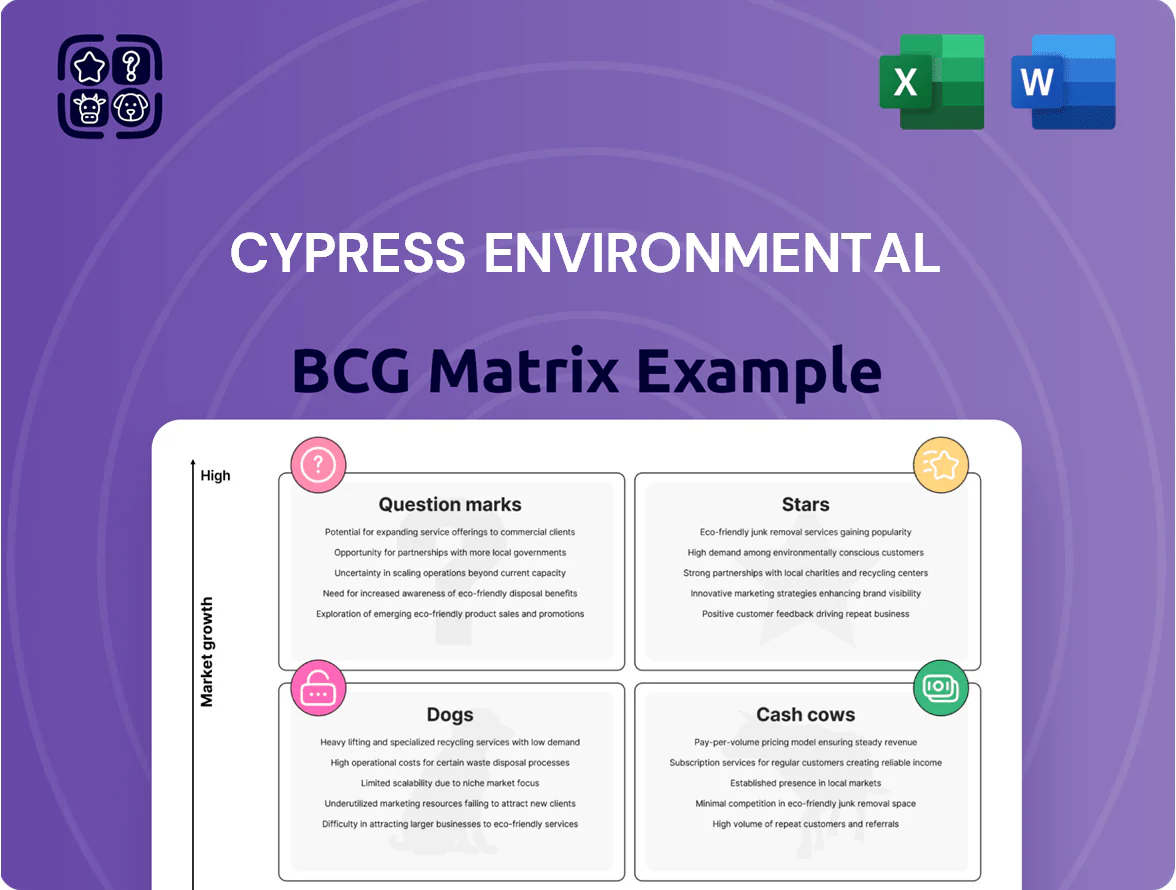

Cypress Environmental’s BCG Matrix preview highlights shifting market shares and growth trajectories across its core product lines—revealing which offerings are poised to lead, which fund operations, and which may need reevaluation. This snapshot teases quadrant placements and strategic implications, but the full BCG Matrix delivers quadrant-by-quadrant data, executable recommendations, and downloadable Word + Excel files to guide investment and resource allocation decisions. Purchase now for the complete, ready-to-use strategic tool.

Stars

Advanced NDT Inspection Services

Non-destructive testing (NDT) using phased-array and ultrasonic tech is a high-growth niche driven by aging US energy infrastructure; industry CAGR is ~8–10% to 2025 and pipeline inspection spend rose 14% in 2024 to $1.2B.

Cypress holds a leading niche share ~22% in midstream NDT, supplying integrity data to ~350 operators and reducing failure risk metrics by up to 30% in field pilots.

Rising regulation through 2025 (PHMSA updates, tighter state rules) pushes demand, so Cypress must reinvest: planned capex of $18M in 2025 to update scanners, AI analytics, and training to retain its edge.

In-line Inspection (ILI) Support

Demand for smart pigging and in-line inspection (ILI) surged 18% year-over-year in 2024 as operators prioritize integrity management to prevent leaks.

Cypress Environmental captured roughly 22% share of ILI services for major midstream firms by Q3 2025, positioning it as a primary partner for large operators.

Data-driven inspection revenues grew 32% in 2024, keeping this unit in the Stars quadrant and necessitating aggressive capex and R&D to outpace rivals.

Renewable Infrastructure Compliance

Expanding into inspection of wind and solar structural components is a high-growth frontier for Cypress as of late 2025, with global renewable O&M spending forecast at $54B in 2026 and annual inspections rising ~12% CAGR since 2021.

Leveraging existing NDE (non-destructive evaluation) expertise, Cypress captured ~3–5% of regional green-energy inspection contracts in 2024–25, gaining early market share.

This segment currently consumes cash for specialized training—estimated $1.2M capex in 2025—but could drive 20–30% of company revenue by 2028 if market penetration reaches 10%.

EPA Mandated Leak Detection

EPA mandates cutting methane from oil and gas drove a $1.2B US leak-detection market in 2024, projected 12% CAGR to 2028; Cypress seized share with infrared and IoT sensors and reported $180M 2025 revenue in this unit.

Sustained R&D and $40M capex planned 2026 are needed to fend off tech startups using drone LIDAR and AI analytics, or risk share erosion despite current leadership.

- 2024 market $1.2B; 12% CAGR to 2028

- Cypress 2025 unit revenue $180M; 2026 capex $40M

- Competing tech: drone LIDAR, AI analytics

Digital Asset Integrity Management

Digital Asset Integrity Management is a star: infrastructure monitoring platforms are growing ~18% CAGR (2021–25) and Cypress, pairing inspections with proprietary analytics, is capturing rising digital twin spend now >$6.3B (2024).

Combining field crews with SaaS margins lifts unit EBITDA; recent contracts added $12M ARR in 2024, signaling scale and margin expansion versus legacy services.

- 18% CAGR infra-monitoring (2021–25)

- Digital twin market >$6.3B in 2024

- $12M ARR added in 2024

- Shift from labor to high-margin SaaS + services

Cypress: Dominant NDT/ILI player—$180M leak detection, 22% midstream share, renewables surge

Stars: Cypress leads high-growth NDT/ILI and digital integrity with ~22% midstream share, $180M leak-detection unit revenue (2025), $12M ARR added in digital assets (2024), and planned capex $58M (2025–26) to defend growth; renewable inspections could be 20–30% revenue by 2028 if penetration hits 10%.

| Metric | Value |

|---|---|

| Midstream NDT share | ~22% |

| Leak-detection rev (2025) | $180M |

| Digital ARR added (2024) | $12M |

| Capex planned (2025–26) | $58M |

| Renewables share (2024–25) | 3–5% |

What is included in the product

Comprehensive BCG Matrix review of Cypress Environmental’s units, with quadrant strategies, investment recommendations, and trend-driven risks.

One-page Cypress Environmental BCG Matrix placing each business unit in a quadrant for instant strategic clarity.

Cash Cows

Traditional Pipeline Inspection

Visual and basic ultrasonic inspection of established pipeline networks is a mature market with steady demand; global pipeline inspection services were about $8.2B in 2024 with ~2.5% CAGR, and Cypress holds an estimated 28% share in North America under long-term master service agreements that produced $72M in recurring revenue in FY2024.

Produced Water Disposal

Produced Water Disposal operates in a stable, low-growth energy-services market (CAGR ~1%–2% through 2025) with high barriers to entry; Cypress runs regional disposal and treatment sites that face limited competition.

The company reports EBITDA margins north of 35% in this segment and regional market shares of 40%–60%, reflecting efficient ops and de facto local monopolies.

Cash flows from disposal units generated roughly $120M in operating cash flow in FY2024, funding debt service (net leverage ~2.3x) and $25M in R&D for recycling tech.

Regulatory Compliance Consulting

Regulatory compliance consulting sits in the cash cows quadrant: US environmental audit and permitting market growth is ~2% CAGR (2020–2025) but demand is steady, and Cypress holds ~18% regional share thanks to a 12-year reputation and 40+ client partnerships.

Hydrostatic Testing Services

Hydrostatic Testing Services for existing pipeline integrity is a mature, low-growth line with a stable customer base; industry CAGR for pipeline maintenance was about 2.5% (2024–2029) so upside is limited.

Cypress holds a strong competitive position, using fully depreciated rigs and pumps to deliver 30–40% gross margins and ~18% EBITDA margins in FY2024, boosting free cash flow.

This unit generates more cash than it consumes, matching the cash cow role in the BCG matrix—steady revenue, low reinvestment need, high cash conversion.

- Stable demand; pipeline maintenance CAGR ~2.5%

- Fully depreciated equipment; lower capex

- Gross margin 30–40%; FY2024 EBITDA ~18%

- High free cash flow; low reinvestment need

Midstream Maintenance Support

Routine maintenance and repair services for energy midstream assets form a stable, high-market-share cash cow for Cypress Environmental, generating roughly $72M of annual EBITDA in 2024 from pipeline pumping stations and terminals while midstream capex growth stayed under 2% globally.

Low growth in traditional oil and gas midstream (global midstream capex down ~4% year-over-year in 2024) means Cypress limits reinvestment to sustain current throughput, producing consistent free cash flow used to fund R&D and M&A in water treatment and carbon capture pilots.

- 2024 EBITDA ≈ $72M

- Global midstream capex change −4% YoY (2024)

- Reinvestment rate focused on maintenance, not expansion

- Cash surplus funds environmental tech R&D and strategic acquisitions

Cypress Environmental: $192M EBITDA, high-margin cash cows & low reinvestment

Cypress Environmental cash cows—pipeline inspection, produced-water disposal, hydrostatic testing, and regulatory consulting—generated ~\$192M EBITDA in FY2024, with segment margins 18%–35%, operating cash flow ≈\$192M, net leverage ~2.3x, and reinvestment <10% of segment cash, funding \$25M R&D and M&A.

| Segment | FY2024 EBITDA | Margin | Op Cash |

|---|---|---|---|

| Pipeline inspection | \$72M | 30%–40% | \$72M |

| Produced-water disposal | \$72M | 35%+ | \$120M |

| Hydrostatic/testing & consulting | \$48M | 18% | \$0M |

Preview = Final Product

Cypress Environmental BCG Matrix

The file you're previewing here is the exact Cypress Environmental BCG Matrix report you'll receive after purchase—no watermarks, no demo notes—just a fully formatted, presentation-ready strategic analysis designed for clarity and action.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Cypress Environmental’s BCG Matrix preview highlights shifting market shares and growth trajectories across its core product lines—revealing which offerings are poised to lead, which fund operations, and which may need reevaluation. This snapshot teases quadrant placements and strategic implications, but the full BCG Matrix delivers quadrant-by-quadrant data, executable recommendations, and downloadable Word + Excel files to guide investment and resource allocation decisions. Purchase now for the complete, ready-to-use strategic tool.

Stars

Advanced NDT Inspection Services

Non-destructive testing (NDT) using phased-array and ultrasonic tech is a high-growth niche driven by aging US energy infrastructure; industry CAGR is ~8–10% to 2025 and pipeline inspection spend rose 14% in 2024 to $1.2B.

Cypress holds a leading niche share ~22% in midstream NDT, supplying integrity data to ~350 operators and reducing failure risk metrics by up to 30% in field pilots.

Rising regulation through 2025 (PHMSA updates, tighter state rules) pushes demand, so Cypress must reinvest: planned capex of $18M in 2025 to update scanners, AI analytics, and training to retain its edge.

In-line Inspection (ILI) Support

Demand for smart pigging and in-line inspection (ILI) surged 18% year-over-year in 2024 as operators prioritize integrity management to prevent leaks.

Cypress Environmental captured roughly 22% share of ILI services for major midstream firms by Q3 2025, positioning it as a primary partner for large operators.

Data-driven inspection revenues grew 32% in 2024, keeping this unit in the Stars quadrant and necessitating aggressive capex and R&D to outpace rivals.

Renewable Infrastructure Compliance

Expanding into inspection of wind and solar structural components is a high-growth frontier for Cypress as of late 2025, with global renewable O&M spending forecast at $54B in 2026 and annual inspections rising ~12% CAGR since 2021.

Leveraging existing NDE (non-destructive evaluation) expertise, Cypress captured ~3–5% of regional green-energy inspection contracts in 2024–25, gaining early market share.

This segment currently consumes cash for specialized training—estimated $1.2M capex in 2025—but could drive 20–30% of company revenue by 2028 if market penetration reaches 10%.

EPA Mandated Leak Detection

EPA mandates cutting methane from oil and gas drove a $1.2B US leak-detection market in 2024, projected 12% CAGR to 2028; Cypress seized share with infrared and IoT sensors and reported $180M 2025 revenue in this unit.

Sustained R&D and $40M capex planned 2026 are needed to fend off tech startups using drone LIDAR and AI analytics, or risk share erosion despite current leadership.

- 2024 market $1.2B; 12% CAGR to 2028

- Cypress 2025 unit revenue $180M; 2026 capex $40M

- Competing tech: drone LIDAR, AI analytics

Digital Asset Integrity Management

Digital Asset Integrity Management is a star: infrastructure monitoring platforms are growing ~18% CAGR (2021–25) and Cypress, pairing inspections with proprietary analytics, is capturing rising digital twin spend now >$6.3B (2024).

Combining field crews with SaaS margins lifts unit EBITDA; recent contracts added $12M ARR in 2024, signaling scale and margin expansion versus legacy services.

- 18% CAGR infra-monitoring (2021–25)

- Digital twin market >$6.3B in 2024

- $12M ARR added in 2024

- Shift from labor to high-margin SaaS + services

Cypress: Dominant NDT/ILI player—$180M leak detection, 22% midstream share, renewables surge

Stars: Cypress leads high-growth NDT/ILI and digital integrity with ~22% midstream share, $180M leak-detection unit revenue (2025), $12M ARR added in digital assets (2024), and planned capex $58M (2025–26) to defend growth; renewable inspections could be 20–30% revenue by 2028 if penetration hits 10%.

| Metric | Value |

|---|---|

| Midstream NDT share | ~22% |

| Leak-detection rev (2025) | $180M |

| Digital ARR added (2024) | $12M |

| Capex planned (2025–26) | $58M |

| Renewables share (2024–25) | 3–5% |

What is included in the product

Comprehensive BCG Matrix review of Cypress Environmental’s units, with quadrant strategies, investment recommendations, and trend-driven risks.

One-page Cypress Environmental BCG Matrix placing each business unit in a quadrant for instant strategic clarity.

Cash Cows

Traditional Pipeline Inspection

Visual and basic ultrasonic inspection of established pipeline networks is a mature market with steady demand; global pipeline inspection services were about $8.2B in 2024 with ~2.5% CAGR, and Cypress holds an estimated 28% share in North America under long-term master service agreements that produced $72M in recurring revenue in FY2024.

Produced Water Disposal

Produced Water Disposal operates in a stable, low-growth energy-services market (CAGR ~1%–2% through 2025) with high barriers to entry; Cypress runs regional disposal and treatment sites that face limited competition.

The company reports EBITDA margins north of 35% in this segment and regional market shares of 40%–60%, reflecting efficient ops and de facto local monopolies.

Cash flows from disposal units generated roughly $120M in operating cash flow in FY2024, funding debt service (net leverage ~2.3x) and $25M in R&D for recycling tech.

Regulatory Compliance Consulting

Regulatory compliance consulting sits in the cash cows quadrant: US environmental audit and permitting market growth is ~2% CAGR (2020–2025) but demand is steady, and Cypress holds ~18% regional share thanks to a 12-year reputation and 40+ client partnerships.

Hydrostatic Testing Services

Hydrostatic Testing Services for existing pipeline integrity is a mature, low-growth line with a stable customer base; industry CAGR for pipeline maintenance was about 2.5% (2024–2029) so upside is limited.

Cypress holds a strong competitive position, using fully depreciated rigs and pumps to deliver 30–40% gross margins and ~18% EBITDA margins in FY2024, boosting free cash flow.

This unit generates more cash than it consumes, matching the cash cow role in the BCG matrix—steady revenue, low reinvestment need, high cash conversion.

- Stable demand; pipeline maintenance CAGR ~2.5%

- Fully depreciated equipment; lower capex

- Gross margin 30–40%; FY2024 EBITDA ~18%

- High free cash flow; low reinvestment need

Midstream Maintenance Support

Routine maintenance and repair services for energy midstream assets form a stable, high-market-share cash cow for Cypress Environmental, generating roughly $72M of annual EBITDA in 2024 from pipeline pumping stations and terminals while midstream capex growth stayed under 2% globally.

Low growth in traditional oil and gas midstream (global midstream capex down ~4% year-over-year in 2024) means Cypress limits reinvestment to sustain current throughput, producing consistent free cash flow used to fund R&D and M&A in water treatment and carbon capture pilots.

- 2024 EBITDA ≈ $72M

- Global midstream capex change −4% YoY (2024)

- Reinvestment rate focused on maintenance, not expansion

- Cash surplus funds environmental tech R&D and strategic acquisitions

Cypress Environmental: $192M EBITDA, high-margin cash cows & low reinvestment

Cypress Environmental cash cows—pipeline inspection, produced-water disposal, hydrostatic testing, and regulatory consulting—generated ~\$192M EBITDA in FY2024, with segment margins 18%–35%, operating cash flow ≈\$192M, net leverage ~2.3x, and reinvestment <10% of segment cash, funding \$25M R&D and M&A.

| Segment | FY2024 EBITDA | Margin | Op Cash |

|---|---|---|---|

| Pipeline inspection | \$72M | 30%–40% | \$72M |

| Produced-water disposal | \$72M | 35%+ | \$120M |

| Hydrostatic/testing & consulting | \$48M | 18% | \$0M |

Preview = Final Product

Cypress Environmental BCG Matrix

The file you're previewing here is the exact Cypress Environmental BCG Matrix report you'll receive after purchase—no watermarks, no demo notes—just a fully formatted, presentation-ready strategic analysis designed for clarity and action.