Daifuku Porter's Five Forces Analysis

Don't Miss the Bigger Picture

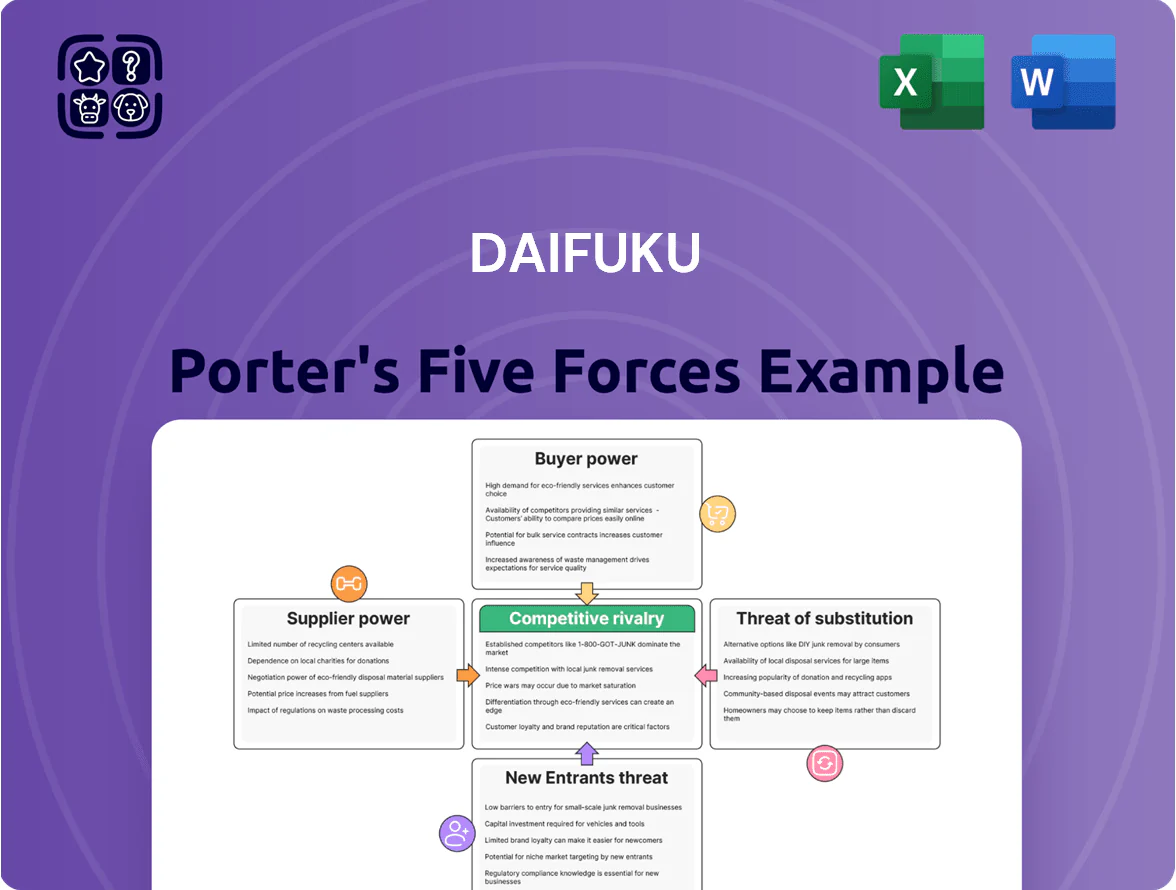

Daifuku faces moderate supplier power, high buyer expectations for integrated automation, and intensifying rivalry as logistic tech competitors scale globally—while barriers to entry remain significant due to capital intensity and IP. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Daifuku’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Electronic and Semiconductor Components

Daifuku depends on high-precision sensors, controllers, and semiconductor chips for its automated systems; by Q4 2025 the global supply chain recovery left only ~6–8 Tier-1 vendors able to meet required specs, giving suppliers pricing power and 8–14 week lead-time control. This niche dependency raises input-cost risk: component price inflation averaged 4.2% YoY in 2024–25 for specialized semiconductors, and AI-integrated hardware needs could push premiums further.

Raw Material Price Volatility for Steel and Aluminum

Raw material price volatility for steel and aluminum raises supplier power for Daifuku because AS/RS and conveyors need large volumes of high-grade metal; global hot-rolled coil (steel) rose 18% in 2024 and aluminum LME averaged $2,350/ton in 2024, up 12% vs 2023.

Geopolitical shifts (Russia-Ukraine, China export curbs) and tighter emissions rules raised input costs, making commodity pricing a key risk.

Sudden metal price spikes can compress margins on long-term fixed-price contracts, forcing Daifuku to hedge or pass costs to clients, which is hard in competitive tendering.

Availability of Specialized Installation Labor

The 2024–25 surge in automation projects tightened supply of skilled electrical/mechanical installers, creating a bottleneck: industry surveys show a 22% shortfall in certified technicians versus demand in key ports (source: IHS Markit 2025).

These local subcontractors hold high bargaining power since their expertise is critical for final commissioning of Daifuku’s complex systems, enabling premium rates and schedule control.

In regions like SE Asia and the US Gulf, scarcity lets suppliers charge 15–30% higher labor rates and insist on flexible windows, raising Daifuku’s project OPEX and timeline risk.

Integration of Third-Party Software and Cloud Services

- Major cloud vendors: high switching costs, months and $M migration

- 2023: Daifuku cloud Opex +12% signals rising reliance

- Cybersecurity and scalability needs increase supplier pricing power

- Proprietary algorithms tied to vendor platforms amplify dependency

Geographic Concentration of Component Manufacturing

A substantial share of precision components for Daifuku’s cleanroom systems—about 60–70% by volume in 2024–25—comes from a concentrated supplier base in East Asia, raising exposure to regional trade policy shifts and port/logistics disruptions.

Those suppliers can exert bargaining power by prioritizing domestic orders or tightening export terms after the 2022–25 regional supply shocks; a two-week port closure could delay deliveries by 15–25% and raise component costs 6–12%.

- 60–70% components from East Asia (2024–25)

- 2-week port closure → 15–25% delivery delays

- Cost pressure increase estimated 6–12%

- Suppliers may prioritize local demand or change export terms

Supply squeeze: concentrated East‑Asia vendors, rising input costs & installer shortfall

Suppliers hold moderate–high power: 6–8 Tier‑1 precision vendors, 60–70% East Asia concentration, 8–14 week lead times, 4.2% specialized semiconductor inflation (2024–25), steel +18% (2024), aluminum $2,350/t (2024), cloud Opex +12% (2023), skilled installer shortfall 22% (2025) — forcing hedging, premium labor, or cost pass-throughs.

| Metric | Value |

|---|---|

| Tier‑1 vendors | 6–8 |

| East Asia share | 60–70% |

| Lead time | 8–14 wk |

| Semiconductor inflation | 4.2% (24–25) |

| Steel | +18% (2024) |

| Aluminum | $2,350/t (2024) |

| Cloud Opex | +12% (2023) |

| Installer shortfall | 22% (2025) |

What is included in the product

Tailored Porter's Five Forces analysis for Daifuku uncovering competitive intensity, buyer and supplier power, substitution threats, and entry barriers—highlighting strategic levers to protect and grow market share.

Daifuku Porter's Five Forces summarized on one sheet—quickly spot competitive pressures and prioritize strategic moves to relieve pain points in operations, pricing, and market entry.

Customers Bargaining Power

Concentration of High-Volume E-commerce and Retail Giants

Around 40–55% of Daifuku’s FY2024 automation revenue comes from a handful of global retailers and e-commerce platforms that order automated warehouses at scale, giving these customers strong bargaining power to demand double-digit discounts and strict SLAs.

These buyers can switch among top integrators like Dematic, Swisslog, and Honeywell, so Daifuku keeps pricing competitive and accelerates innovation—R&D rose 18% in 2024 to defend margins.

High Switching Costs and Long-Term System Integration

Once a Daifuku system is embedded into a customer’s core logistics, switching costs—measured in downtime, retraining, and integration—often exceed 20–35% of annual system value, making moves to competitors prohibitively expensive and risky.

This technical lock-in gives Daifuku counter-leverage during maintenance and upgrades, supporting recurring service revenues that represented about 22% of group sales in FY2024 (¥166.8bn of ¥758.2bn).

That leverage only materializes post-deployment, so initial bids remain highly customer-centric, with procurement cycles focused on TCO, uptime guarantees, and integration timelines often spanning 9–18 months.

Demand for Bespoke Engineering and Customization

Sophisticated customers in semiconductor and automotive plants demand bespoke material-handling systems tied to specific factory layouts, forcing Daifuku to spend project-specific R&D—Daifuku reported R&D of ¥47.6 billion in FY2024—raising per-project costs and lengthening delivery. This customization requirement boosts customer bargaining power, since buyers can threaten switching to rivals (e.g., Murata, Applied Materials) if technical specs aren’t met; industry surveys show 62% of fabs prioritize vendor flexibility over price.

Price Sensitivity in Mature Regional Markets

In mature regional markets where basic automation is common, customers treat standard conveyors and racking as commodities, raising price sensitivity; a 2024 Frost & Sullivan note found 60% of APAC mid-market warehouses request three+ vendor quotes for such systems.

Daifuku must therefore push differentiation via 15–25% better energy efficiency or tighter software integration (WMS/WCS) to keep pricing power versus lower-cost regional rivals.

- 60% of buyers request 3+ quotes (Frost & Sullivan 2024)

Sensitivity to Macroeconomic Capital Expenditure Budgets

The bargaining power of customers ties closely to their CAPEX cycles and 2025 interest rates; global average policy rates stood near 4.5% in Q4 2025, pushing many logistics operators to defer projects and seek price concessions from suppliers like Daifuku.

Higher borrowing costs make customers more selective, lengthening procurement cycles by 3–6 months on average and increasing negotiation leverage to demand extended payment terms or bundled services.

This forces Daifuku to position as a strategic partner—offering financing, phased deployments, and ROI modeling—to win large contracts and limit order cancellations.

Top retailers squeeze automation margins; 22% recurring services amid longer, financed buys

Large retailers drive 40–55% of FY2024 automation revenue, forcing double-digit discounts and strict SLAs; switching among integrators keeps pricing tight while post-deployment lock-in (20–35% of system value) supports 22% recurring service revenue (¥166.8bn/¥758.2bn FY2024). Higher 2025 policy rates (~4.5%) lengthen procurement by 3–6 months, raising demand for financing and phased delivery.

| Metric | Value |

|---|---|

| Share from top buyers | 40–55% |

| Service revenue | 22% (¥166.8bn) |

| R&D FY2024 | ¥47.6bn |

| Policy rates Q4 2025 | ~4.5% |

| Procurement delay | +3–6 months |

Preview the Actual Deliverable

Daifuku Porter's Five Forces Analysis

This preview shows the exact Daifuku Porter's Five Forces analysis you'll receive immediately after purchase—no samples or placeholders, fully formatted and ready for use.

You're viewing the final, professionally written document; once you complete payment you'll get instant access to this identical file for download and application.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Daifuku faces moderate supplier power, high buyer expectations for integrated automation, and intensifying rivalry as logistic tech competitors scale globally—while barriers to entry remain significant due to capital intensity and IP. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Daifuku’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Electronic and Semiconductor Components

Daifuku depends on high-precision sensors, controllers, and semiconductor chips for its automated systems; by Q4 2025 the global supply chain recovery left only ~6–8 Tier-1 vendors able to meet required specs, giving suppliers pricing power and 8–14 week lead-time control. This niche dependency raises input-cost risk: component price inflation averaged 4.2% YoY in 2024–25 for specialized semiconductors, and AI-integrated hardware needs could push premiums further.

Raw Material Price Volatility for Steel and Aluminum

Raw material price volatility for steel and aluminum raises supplier power for Daifuku because AS/RS and conveyors need large volumes of high-grade metal; global hot-rolled coil (steel) rose 18% in 2024 and aluminum LME averaged $2,350/ton in 2024, up 12% vs 2023.

Geopolitical shifts (Russia-Ukraine, China export curbs) and tighter emissions rules raised input costs, making commodity pricing a key risk.

Sudden metal price spikes can compress margins on long-term fixed-price contracts, forcing Daifuku to hedge or pass costs to clients, which is hard in competitive tendering.

Availability of Specialized Installation Labor

The 2024–25 surge in automation projects tightened supply of skilled electrical/mechanical installers, creating a bottleneck: industry surveys show a 22% shortfall in certified technicians versus demand in key ports (source: IHS Markit 2025).

These local subcontractors hold high bargaining power since their expertise is critical for final commissioning of Daifuku’s complex systems, enabling premium rates and schedule control.

In regions like SE Asia and the US Gulf, scarcity lets suppliers charge 15–30% higher labor rates and insist on flexible windows, raising Daifuku’s project OPEX and timeline risk.

Integration of Third-Party Software and Cloud Services

- Major cloud vendors: high switching costs, months and $M migration

- 2023: Daifuku cloud Opex +12% signals rising reliance

- Cybersecurity and scalability needs increase supplier pricing power

- Proprietary algorithms tied to vendor platforms amplify dependency

Geographic Concentration of Component Manufacturing

A substantial share of precision components for Daifuku’s cleanroom systems—about 60–70% by volume in 2024–25—comes from a concentrated supplier base in East Asia, raising exposure to regional trade policy shifts and port/logistics disruptions.

Those suppliers can exert bargaining power by prioritizing domestic orders or tightening export terms after the 2022–25 regional supply shocks; a two-week port closure could delay deliveries by 15–25% and raise component costs 6–12%.

- 60–70% components from East Asia (2024–25)

- 2-week port closure → 15–25% delivery delays

- Cost pressure increase estimated 6–12%

- Suppliers may prioritize local demand or change export terms

Supply squeeze: concentrated East‑Asia vendors, rising input costs & installer shortfall

Suppliers hold moderate–high power: 6–8 Tier‑1 precision vendors, 60–70% East Asia concentration, 8–14 week lead times, 4.2% specialized semiconductor inflation (2024–25), steel +18% (2024), aluminum $2,350/t (2024), cloud Opex +12% (2023), skilled installer shortfall 22% (2025) — forcing hedging, premium labor, or cost pass-throughs.

| Metric | Value |

|---|---|

| Tier‑1 vendors | 6–8 |

| East Asia share | 60–70% |

| Lead time | 8–14 wk |

| Semiconductor inflation | 4.2% (24–25) |

| Steel | +18% (2024) |

| Aluminum | $2,350/t (2024) |

| Cloud Opex | +12% (2023) |

| Installer shortfall | 22% (2025) |

What is included in the product

Tailored Porter's Five Forces analysis for Daifuku uncovering competitive intensity, buyer and supplier power, substitution threats, and entry barriers—highlighting strategic levers to protect and grow market share.

Daifuku Porter's Five Forces summarized on one sheet—quickly spot competitive pressures and prioritize strategic moves to relieve pain points in operations, pricing, and market entry.

Customers Bargaining Power

Concentration of High-Volume E-commerce and Retail Giants

Around 40–55% of Daifuku’s FY2024 automation revenue comes from a handful of global retailers and e-commerce platforms that order automated warehouses at scale, giving these customers strong bargaining power to demand double-digit discounts and strict SLAs.

These buyers can switch among top integrators like Dematic, Swisslog, and Honeywell, so Daifuku keeps pricing competitive and accelerates innovation—R&D rose 18% in 2024 to defend margins.

High Switching Costs and Long-Term System Integration

Once a Daifuku system is embedded into a customer’s core logistics, switching costs—measured in downtime, retraining, and integration—often exceed 20–35% of annual system value, making moves to competitors prohibitively expensive and risky.

This technical lock-in gives Daifuku counter-leverage during maintenance and upgrades, supporting recurring service revenues that represented about 22% of group sales in FY2024 (¥166.8bn of ¥758.2bn).

That leverage only materializes post-deployment, so initial bids remain highly customer-centric, with procurement cycles focused on TCO, uptime guarantees, and integration timelines often spanning 9–18 months.

Demand for Bespoke Engineering and Customization

Sophisticated customers in semiconductor and automotive plants demand bespoke material-handling systems tied to specific factory layouts, forcing Daifuku to spend project-specific R&D—Daifuku reported R&D of ¥47.6 billion in FY2024—raising per-project costs and lengthening delivery. This customization requirement boosts customer bargaining power, since buyers can threaten switching to rivals (e.g., Murata, Applied Materials) if technical specs aren’t met; industry surveys show 62% of fabs prioritize vendor flexibility over price.

Price Sensitivity in Mature Regional Markets

In mature regional markets where basic automation is common, customers treat standard conveyors and racking as commodities, raising price sensitivity; a 2024 Frost & Sullivan note found 60% of APAC mid-market warehouses request three+ vendor quotes for such systems.

Daifuku must therefore push differentiation via 15–25% better energy efficiency or tighter software integration (WMS/WCS) to keep pricing power versus lower-cost regional rivals.

- 60% of buyers request 3+ quotes (Frost & Sullivan 2024)

Sensitivity to Macroeconomic Capital Expenditure Budgets

The bargaining power of customers ties closely to their CAPEX cycles and 2025 interest rates; global average policy rates stood near 4.5% in Q4 2025, pushing many logistics operators to defer projects and seek price concessions from suppliers like Daifuku.

Higher borrowing costs make customers more selective, lengthening procurement cycles by 3–6 months on average and increasing negotiation leverage to demand extended payment terms or bundled services.

This forces Daifuku to position as a strategic partner—offering financing, phased deployments, and ROI modeling—to win large contracts and limit order cancellations.

Top retailers squeeze automation margins; 22% recurring services amid longer, financed buys

Large retailers drive 40–55% of FY2024 automation revenue, forcing double-digit discounts and strict SLAs; switching among integrators keeps pricing tight while post-deployment lock-in (20–35% of system value) supports 22% recurring service revenue (¥166.8bn/¥758.2bn FY2024). Higher 2025 policy rates (~4.5%) lengthen procurement by 3–6 months, raising demand for financing and phased delivery.

| Metric | Value |

|---|---|

| Share from top buyers | 40–55% |

| Service revenue | 22% (¥166.8bn) |

| R&D FY2024 | ¥47.6bn |

| Policy rates Q4 2025 | ~4.5% |

| Procurement delay | +3–6 months |

Preview the Actual Deliverable

Daifuku Porter's Five Forces Analysis

This preview shows the exact Daifuku Porter's Five Forces analysis you'll receive immediately after purchase—no samples or placeholders, fully formatted and ready for use.

You're viewing the final, professionally written document; once you complete payment you'll get instant access to this identical file for download and application.