Daiichi Sankyo PESTLE Analysis

Your Competitive Advantage Starts with This Report

Explore how geopolitical shifts, regulatory pressure, and rapid biotech innovation are reshaping Daiichi Sankyo’s strategic outlook—our concise PESTLE snapshot highlights key risks and opportunities for investors and strategists; purchase the full PESTLE to get the complete, actionable breakdown and ready-to-use slides for decision-making.

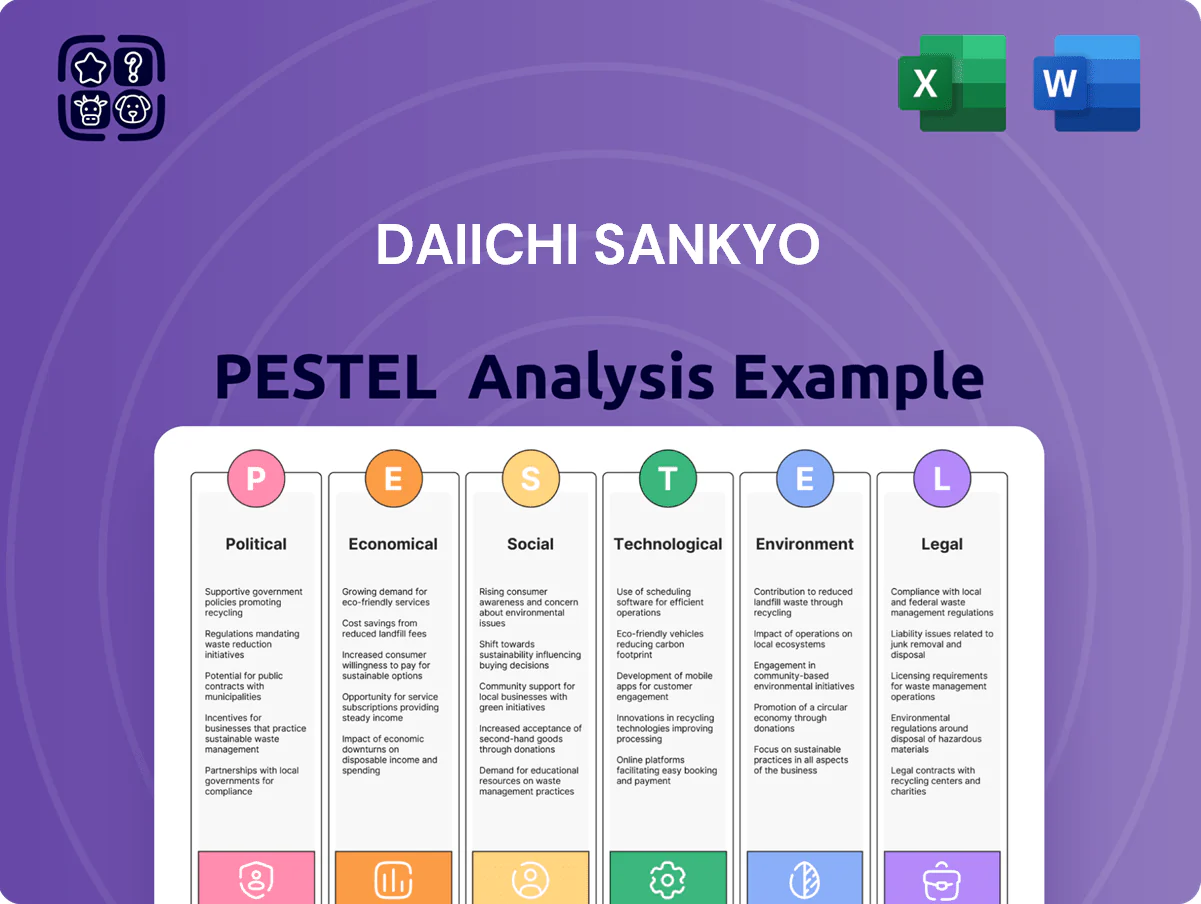

Political factors

US Inflation Reduction Act Implementation

Full implementation of drug-price negotiations under the US Inflation Reduction Act by late 2025 threatens Daiichi Sankyo’s oncology revenue, as CMS targets top-selling biologics—projected negotiated discounts average 25–35% in Congressional Budget Office scenarios—pressuring ADC sales that contributed roughly $1.2–1.6 billion in global revenue in 2024.

Negotiation authority creates risk of margin compression for flagship ADCs, potentially reducing US gross margins by 5–10 percentage points if similar discounts apply to high-revenue oncology drugs, affecting near-term EPS guidance.

To mitigate, Daiichi Sankyo must strengthen evidence-based value propositions, expand real-world outcomes and health-economic data, and pursue formulary and value-based contracting to sustain market access amid heightened price scrutiny.

Japanese Healthcare Reimbursement Reforms

Japanese biennial drug price revisions, aimed at curbing healthcare spending for a population with 29% aged 65+ (2025), regularly trimmed prices of mature drugs—Daiichi Sankyo saw domestic prescription sales fall 6% YoY in FY2024—pushing the firm to accelerate launches of innovative oncology and cardiovascular assets to offset revenue erosion; alignment with the Council for Health and Medical Strategy is critical to secure premium pricing for breakthrough medicines under value-based review.

Geopolitical Supply Chain Stability

Ongoing 2025 geopolitical tensions have driven Daiichi Sankyo to diversify manufacturing, shifting ~15% of API production away from single-region dependence and increasing contract manufacturing in India and Portugal.

Political instability in key trade corridors has led the firm to adopt proactive diplomacy and strategic stockpiling equal to roughly 3 months of oncology inventory to protect global supply of cancer therapies.

The company’s skill in navigating trade barriers and export controls is critical to sustaining international revenue—over 40% of Daiichi Sankyo’s 2024 revenue was from markets sensitive to such restrictions.

Global Regulatory Harmonization Efforts

Political support for ICH harmonization is reducing duplicative submissions and accelerating approvals across Europe, Asia and the Americas; ICH adoption helped lower average regulatory review times by ~15%–20% in ICH regions between 2018–2023.

Daiichi Sankyo benefits via reduced administrative burden and faster time-to-market for pipeline assets, improving NPV for late-stage drugs and supporting global launch strategies.

Political stability in key markets (EU, Japan, US) keeps regulatory frameworks predictable, underpinning multi-year R&D budgeting and partnership deals; Japan’s pharma R&D tax incentives and stable policy environment contributed to industry capex resilience in 2024.

- ICH harmonization: ~15%–20% faster average review times (2018–2023)

- Reduced administrative costs and improved time-to-market for Daiichi Sankyo

- Stable EU/Japan/US politics support predictable long-term R&D planning

Government Funding for Oncology Research

Public sector investment—US Cancer Moonshot funding reached about $1.8 billion for 2022–2024 initiatives—creates a collaborative environment that benefits Daiichi Sankyo’s oncology R&D across major markets.

Through public-private partnerships, the company can tap government grants and academic networks to accelerate early-stage discovery, lowering initial costs and time-to-clinic.

Political backing aligns Daiichi Sankyo’s pipeline strategy with national healthcare priorities, de-risking projects and improving access to co-funding in key regions.

- 2022–24 US Cancer Moonshot ≈ $1.8B

- Public-private grants reduce early-stage financing needs

- Alignment with national priorities aids market access

IRA cuts threaten 2025 oncology revenues as ADCs face $1.2–1.6B market shift

US IRA drug-price negotiations (25–35% projected discounts) risk 2025 oncology revenue; ADCs generated ~$1.2–1.6B in 2024. Japan price revisions cut domestic prescriptions 6% YoY in FY2024. Supply diversification moved ~15% API production offshore; oncology inventory stockpile ≈3 months. ICH adoption cut review times ~15–20% (2018–23); US Cancer Moonshot funding ≈$1.8B (2022–24).

| Factor | Metric | 2024/2025 |

|---|---|---|

| IRA discounts | Projected | 25–35% |

| ADC revenue | Global | $1.2–1.6B |

| Japan impact | Domestic sales YoY | -6% |

| API shift | Production moved | ~15% |

| Inventory | Months | ≈3 |

| ICH | Review time | -15–20% |

| Cancer Moonshot | Funding | $1.8B |

What is included in the product

Explores how external macro-environmental factors uniquely affect Daiichi Sankyo across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to help executives and investors identify risks, opportunities, and strategic responses tailored to the pharmaceutical industry and relevant regional markets.

Condensed PESTLE insights for Daiichi Sankyo, organized by category to streamline strategy meetings and quickly surface regulatory, market, and technological risks for easy inclusion in presentations.

Economic factors

Foreign Exchange Rate Volatility

As a Japan-headquartered firm with roughly 60% of 2024 revenues generated overseas, Daiichi Sankyo is highly sensitive to JPY/USD and JPY/EUR swings; a 10% yen depreciation in 2025 could boost translated sales materially but raise import and trial costs. Significant 2025 currency volatility complicates forecasting for international earnings and the cost of overseas clinical trials, which consumed over ¥120 billion in R&D in FY2024. The company uses layered hedging—forward contracts and options—to stabilize cash flows and safeguard its ¥200+ billion capex budget for global expansion.

R&D Investment Intensity

Daiichi Sankyo’s shift to a global oncology focus makes high-intensity R&D spending a structural economic requirement, with R&D expenses rising to ¥246.6 billion in FY2024 (about 17% of revenue) as investment centers on the DXd ADC platform.

Allocating a large revenue share to DXd development is critical to sustain a competitive pipeline against Roche, AstraZeneca and other ADC players, where time-to-market and clinical success rates drive market share.

Investors track ROI closely: Daiichi Sankyo targets mid-to-high single-digit CAGR in oncology revenue by 2027, so capital allocation efficiency is a key determinant of stock valuation and debt metrics.

Global Inflationary Pressures

Persistent global inflation through 2025 raised pharmaceutical input costs by ~6–8% year-over-year; active ingredient and logistics surcharges added pressure as Japan CPI hovered near 3% and global freight rates stayed elevated. Daiichi Sankyo faces constrained pricing power in regulated markets, so it pursues operational-excellence and digital initiatives—productivity programs aiming to cut SG&A by mid-single digits and automation investments indexed to save an estimated ¥20–30 billion over 2024–25—to protect operating margins.

Emerging Market Economic Growth

Expanding economic wealth in emerging markets, notably Southeast Asia where middle-class consumption rose ~40% from 2010–2020 and parts of Latin America with 3–4% GDP growth in 2023–24, creates substantial demand for specialty oncology and cardiovascular medicines, opening diversification opportunities for Daiichi Sankyo.

Rising middle classes increase willingness to pay for advanced therapies, but penetration will need tiered pricing and flexible reimbursement strategies to address income disparities and ensure affordability.

- SE Asia middle class +40% (2010–2020)

- LatAm GDP ~3–4% (2023–24)

- Need for tiered pricing and local reimbursement

Healthcare Spending Trends

Macroeconomic shifts toward value-based care force Daiichi Sankyo to justify premium pricing; global health spending reached $9.6 trillion in 2023, pushing payers to favor cost-effective therapies.

Payers now require real-world evidence: 78% of U.S. Medicare Part D formulary decisions in 2024 referenced real-world outcomes, pressuring market access timelines.

Daiichi Sankyo's revenue growth depends on proving reduced long-term hospitalizations—each avoided admission can save $14,000+—linking drug uptake to lower systemic costs.

- Value-based reimbursement rising; global health spend $9.6T (2023)

- 78% of U.S. formulary decisions cited real-world evidence (2024)

- Average hospital admission avoided saves ~$14,000 in the U.S.

Daiichi Sankyo: FX, inflation squeeze margins; R&D, automation and RWE drive oncology growth

Daiichi Sankyo faces currency risk (60% 2024 revenues overseas; ¥246.6bn R&D FY2024); 2025 yen moves and 6–8% input inflation compress margins, offset by hedging and ¥20–30bn automation savings; oncology DXd investment targets mid‑high single‑digit CAGR to 2027 amid value‑based pricing and payers demanding real‑world evidence (78% U.S. formulary cites, 2024).

| Metric | Value |

|---|---|

| Overseas revenue share (2024) | ~60% |

| R&D (FY2024) | ¥246.6bn |

| Automation savings (2024–25) | ¥20–30bn |

| U.S. formulary RWE citation (2024) | 78% |

Full Version Awaits

Daiichi Sankyo PESTLE Analysis

The preview shown here is the exact Daiichi Sankyo PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investor review.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Explore how geopolitical shifts, regulatory pressure, and rapid biotech innovation are reshaping Daiichi Sankyo’s strategic outlook—our concise PESTLE snapshot highlights key risks and opportunities for investors and strategists; purchase the full PESTLE to get the complete, actionable breakdown and ready-to-use slides for decision-making.

Political factors

US Inflation Reduction Act Implementation

Full implementation of drug-price negotiations under the US Inflation Reduction Act by late 2025 threatens Daiichi Sankyo’s oncology revenue, as CMS targets top-selling biologics—projected negotiated discounts average 25–35% in Congressional Budget Office scenarios—pressuring ADC sales that contributed roughly $1.2–1.6 billion in global revenue in 2024.

Negotiation authority creates risk of margin compression for flagship ADCs, potentially reducing US gross margins by 5–10 percentage points if similar discounts apply to high-revenue oncology drugs, affecting near-term EPS guidance.

To mitigate, Daiichi Sankyo must strengthen evidence-based value propositions, expand real-world outcomes and health-economic data, and pursue formulary and value-based contracting to sustain market access amid heightened price scrutiny.

Japanese Healthcare Reimbursement Reforms

Japanese biennial drug price revisions, aimed at curbing healthcare spending for a population with 29% aged 65+ (2025), regularly trimmed prices of mature drugs—Daiichi Sankyo saw domestic prescription sales fall 6% YoY in FY2024—pushing the firm to accelerate launches of innovative oncology and cardiovascular assets to offset revenue erosion; alignment with the Council for Health and Medical Strategy is critical to secure premium pricing for breakthrough medicines under value-based review.

Geopolitical Supply Chain Stability

Ongoing 2025 geopolitical tensions have driven Daiichi Sankyo to diversify manufacturing, shifting ~15% of API production away from single-region dependence and increasing contract manufacturing in India and Portugal.

Political instability in key trade corridors has led the firm to adopt proactive diplomacy and strategic stockpiling equal to roughly 3 months of oncology inventory to protect global supply of cancer therapies.

The company’s skill in navigating trade barriers and export controls is critical to sustaining international revenue—over 40% of Daiichi Sankyo’s 2024 revenue was from markets sensitive to such restrictions.

Global Regulatory Harmonization Efforts

Political support for ICH harmonization is reducing duplicative submissions and accelerating approvals across Europe, Asia and the Americas; ICH adoption helped lower average regulatory review times by ~15%–20% in ICH regions between 2018–2023.

Daiichi Sankyo benefits via reduced administrative burden and faster time-to-market for pipeline assets, improving NPV for late-stage drugs and supporting global launch strategies.

Political stability in key markets (EU, Japan, US) keeps regulatory frameworks predictable, underpinning multi-year R&D budgeting and partnership deals; Japan’s pharma R&D tax incentives and stable policy environment contributed to industry capex resilience in 2024.

- ICH harmonization: ~15%–20% faster average review times (2018–2023)

- Reduced administrative costs and improved time-to-market for Daiichi Sankyo

- Stable EU/Japan/US politics support predictable long-term R&D planning

Government Funding for Oncology Research

Public sector investment—US Cancer Moonshot funding reached about $1.8 billion for 2022–2024 initiatives—creates a collaborative environment that benefits Daiichi Sankyo’s oncology R&D across major markets.

Through public-private partnerships, the company can tap government grants and academic networks to accelerate early-stage discovery, lowering initial costs and time-to-clinic.

Political backing aligns Daiichi Sankyo’s pipeline strategy with national healthcare priorities, de-risking projects and improving access to co-funding in key regions.

- 2022–24 US Cancer Moonshot ≈ $1.8B

- Public-private grants reduce early-stage financing needs

- Alignment with national priorities aids market access

IRA cuts threaten 2025 oncology revenues as ADCs face $1.2–1.6B market shift

US IRA drug-price negotiations (25–35% projected discounts) risk 2025 oncology revenue; ADCs generated ~$1.2–1.6B in 2024. Japan price revisions cut domestic prescriptions 6% YoY in FY2024. Supply diversification moved ~15% API production offshore; oncology inventory stockpile ≈3 months. ICH adoption cut review times ~15–20% (2018–23); US Cancer Moonshot funding ≈$1.8B (2022–24).

| Factor | Metric | 2024/2025 |

|---|---|---|

| IRA discounts | Projected | 25–35% |

| ADC revenue | Global | $1.2–1.6B |

| Japan impact | Domestic sales YoY | -6% |

| API shift | Production moved | ~15% |

| Inventory | Months | ≈3 |

| ICH | Review time | -15–20% |

| Cancer Moonshot | Funding | $1.8B |

What is included in the product

Explores how external macro-environmental factors uniquely affect Daiichi Sankyo across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to help executives and investors identify risks, opportunities, and strategic responses tailored to the pharmaceutical industry and relevant regional markets.

Condensed PESTLE insights for Daiichi Sankyo, organized by category to streamline strategy meetings and quickly surface regulatory, market, and technological risks for easy inclusion in presentations.

Economic factors

Foreign Exchange Rate Volatility

As a Japan-headquartered firm with roughly 60% of 2024 revenues generated overseas, Daiichi Sankyo is highly sensitive to JPY/USD and JPY/EUR swings; a 10% yen depreciation in 2025 could boost translated sales materially but raise import and trial costs. Significant 2025 currency volatility complicates forecasting for international earnings and the cost of overseas clinical trials, which consumed over ¥120 billion in R&D in FY2024. The company uses layered hedging—forward contracts and options—to stabilize cash flows and safeguard its ¥200+ billion capex budget for global expansion.

R&D Investment Intensity

Daiichi Sankyo’s shift to a global oncology focus makes high-intensity R&D spending a structural economic requirement, with R&D expenses rising to ¥246.6 billion in FY2024 (about 17% of revenue) as investment centers on the DXd ADC platform.

Allocating a large revenue share to DXd development is critical to sustain a competitive pipeline against Roche, AstraZeneca and other ADC players, where time-to-market and clinical success rates drive market share.

Investors track ROI closely: Daiichi Sankyo targets mid-to-high single-digit CAGR in oncology revenue by 2027, so capital allocation efficiency is a key determinant of stock valuation and debt metrics.

Global Inflationary Pressures

Persistent global inflation through 2025 raised pharmaceutical input costs by ~6–8% year-over-year; active ingredient and logistics surcharges added pressure as Japan CPI hovered near 3% and global freight rates stayed elevated. Daiichi Sankyo faces constrained pricing power in regulated markets, so it pursues operational-excellence and digital initiatives—productivity programs aiming to cut SG&A by mid-single digits and automation investments indexed to save an estimated ¥20–30 billion over 2024–25—to protect operating margins.

Emerging Market Economic Growth

Expanding economic wealth in emerging markets, notably Southeast Asia where middle-class consumption rose ~40% from 2010–2020 and parts of Latin America with 3–4% GDP growth in 2023–24, creates substantial demand for specialty oncology and cardiovascular medicines, opening diversification opportunities for Daiichi Sankyo.

Rising middle classes increase willingness to pay for advanced therapies, but penetration will need tiered pricing and flexible reimbursement strategies to address income disparities and ensure affordability.

- SE Asia middle class +40% (2010–2020)

- LatAm GDP ~3–4% (2023–24)

- Need for tiered pricing and local reimbursement

Healthcare Spending Trends

Macroeconomic shifts toward value-based care force Daiichi Sankyo to justify premium pricing; global health spending reached $9.6 trillion in 2023, pushing payers to favor cost-effective therapies.

Payers now require real-world evidence: 78% of U.S. Medicare Part D formulary decisions in 2024 referenced real-world outcomes, pressuring market access timelines.

Daiichi Sankyo's revenue growth depends on proving reduced long-term hospitalizations—each avoided admission can save $14,000+—linking drug uptake to lower systemic costs.

- Value-based reimbursement rising; global health spend $9.6T (2023)

- 78% of U.S. formulary decisions cited real-world evidence (2024)

- Average hospital admission avoided saves ~$14,000 in the U.S.

Daiichi Sankyo: FX, inflation squeeze margins; R&D, automation and RWE drive oncology growth

Daiichi Sankyo faces currency risk (60% 2024 revenues overseas; ¥246.6bn R&D FY2024); 2025 yen moves and 6–8% input inflation compress margins, offset by hedging and ¥20–30bn automation savings; oncology DXd investment targets mid‑high single‑digit CAGR to 2027 amid value‑based pricing and payers demanding real‑world evidence (78% U.S. formulary cites, 2024).

| Metric | Value |

|---|---|

| Overseas revenue share (2024) | ~60% |

| R&D (FY2024) | ¥246.6bn |

| Automation savings (2024–25) | ¥20–30bn |

| U.S. formulary RWE citation (2024) | 78% |

Full Version Awaits

Daiichi Sankyo PESTLE Analysis

The preview shown here is the exact Daiichi Sankyo PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investor review.