Daou Data Boston Consulting Group Matrix

Download Your Competitive Advantage

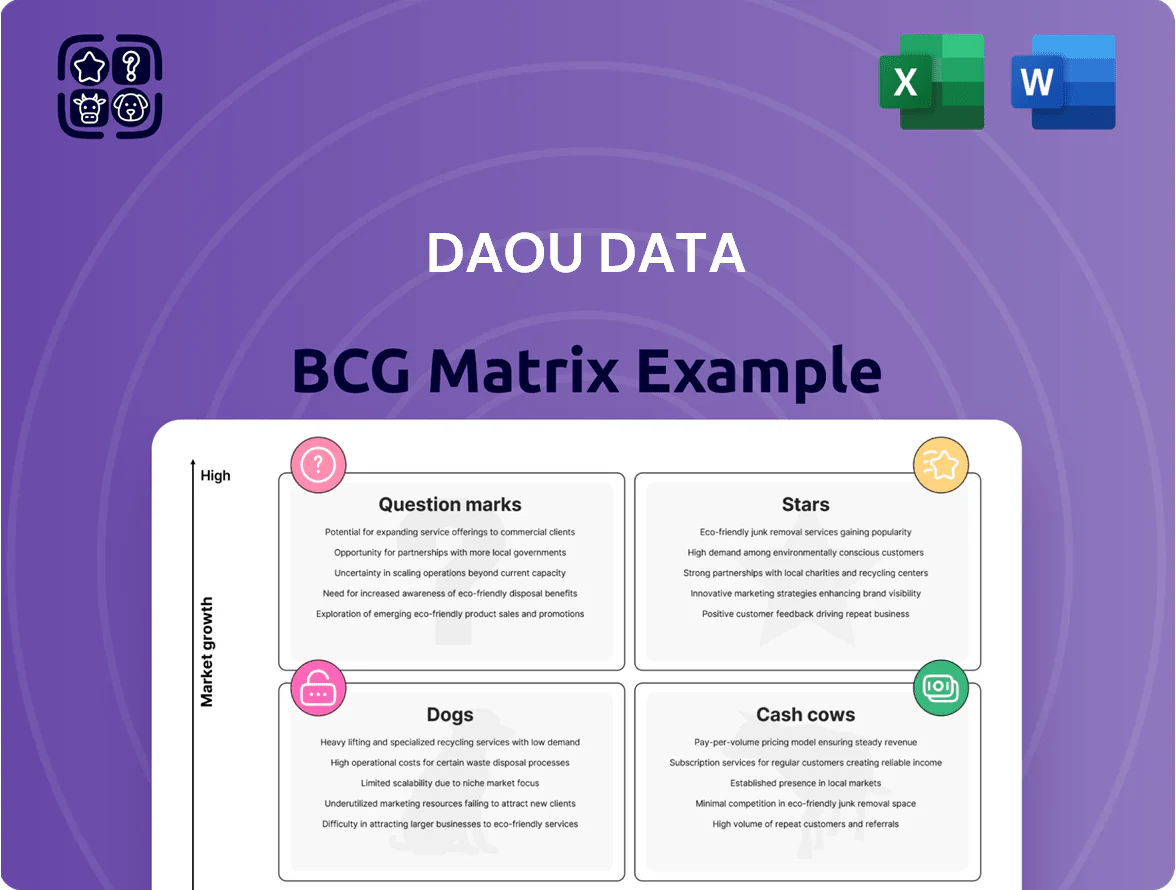

Daou Data’s BCG Matrix preview highlights where its core offerings sit in the competitive landscape—identifying emerging Stars, steady Cash Cows, and potential Dogs or Question Marks that require attention; this snapshot helps prioritize capital and product strategy now. Purchase the full BCG Matrix to unlock quadrant-by-quadrant placements, data-driven recommendations, and ready-to-use Word and Excel deliverables that turn analysis into actionable decisions—get the complete report for strategic clarity and faster, smarter planning.

Stars

Cloud Computing and SaaS Solutions

As of late 2025, Daou Data leads South Korea’s cloud market with a ~28% domestic share in cloud orchestration and SaaS deployments, driven by SME digitalization growing at ~14% CAGR (2023–25). New SME contracts rose 32% year-on-year in 2025, keeping revenue growth near 27% and placing the segment in the BCG Stars quadrant. Heavy capex—≈KRW 120 billion in 2024–25—funds edge services and AI ops to fend off hyperscalers. Continued high market growth and leading share justify sustained investment to retain scale advantages.

Fintech and Digital Payment Infrastructure

Fintech and Digital Payment Infrastructure is Daou Data’s star, driven by a 2021–2025 surge in digital-only banking and contactless payments; global digital payments grew ~18% CAGR to reach $7.2T in 2025, and Daou captures an estimated 4–6% of APAC transaction-processing volume.

As core architecture for high-volume flows, this unit fuels top-line growth while operating margins stay healthy; transaction throughput scaled 3x from 2022–2025, supporting revenue growth of ~28% CAGR.

High R&D spend—about 12% of unit revenue in 2025—remains essential to meet evolving PSD2-like rules, Korea’s Financial Services Commission updates, and rising cyberthreats; ongoing compliance costs cut near-term free cash flow but protect long-term market share.

AI-Integrated Data Analytics Platforms

Daou Data’s AI-integrated analytics platforms, riding the mid-2020s AI boom, hold roughly 18% share in manufacturing analytics and 13% in retail as of Q4 2025, driving 42% year-over-year revenue growth and $62M ARR in 2025.

Platforms are in the BCG Stars quadrant: high market growth (estimated 28% CAGR 2024–27) and high relative market share, used for predictive maintenance and consumer-behavior models.

Profit margins exceed 28% EBITDA, but intense competition forces Daou to spend ~22% of revenue on R&D and 15% on sales/marketing to defend leadership.

Cybersecurity for Public Infrastructure

By 2025 Daou Data’s Cybersecurity for Public Infrastructure is a Star: specialized security offerings drove 42% year-over-year revenue growth in 2024 and now account for 38% of government contract revenue.

The company holds a commanding share—estimated 22%—of secure data management contracts in its domestic market, fueled by national security mandates that raised public-sector security budgets 18% from 2022–2024.

This segment dominates a high-growth niche needing continuous innovation; R&D spend for the unit rose 27% in 2024 to $48 million to support zero-trust and OT protection solutions.

- 2024 revenue growth 42%

- 38% of gov contract revenue

- Estimated 22% market share

- R&D $48M (up 27%)

Enterprise Mobility Management (EMM)

By 2025 Daou Data’s Enterprise Mobility Management (EMM) moved into high-growth territory as hybrid work became standard, with reported EMM revenue up ~42% year-over-year and market share rising to roughly 11% globally in 2025.

The suite secures mobile access for large corporate workforces, targeting enterprises with 5,000+ employees where demand still grows about 12% CAGR worldwide.

Daou Data is reinvesting profits to add biometric authentication and zero-trust features, budgeting an estimated KRW 18 billion in R&D through 2026 to accelerate rollouts.

- 2025 EMM revenue +42% YoY

- Approx. 11% global EMM market share (2025)

- Target segment: enterprises 5,000+ employees

- Market growth ~12% CAGR

- R&D allocation KRW 18 billion through 2026

Daou Data 2025: Rapid multi‑segment growth — cloud, fintech, AI, security, EMM leaders

Daou Data’s Stars (2025): cloud/SaaS (~28% KR market share; revenue +27% YoY; capex KRW 120B 2024–25), fintech payments (4–6% APAC volume; revenue +28% CAGR 2021–25), AI analytics ($62M ARR; 42% YoY; 18% manuf. share), cybersecurity (22% gov market share; revenue +42% 2024; R&D $48M), EMM (+42% YoY; 11% global share).

| Unit | Key metric | 2025 figure |

|---|---|---|

| Cloud/SaaS | Market share / capex | ~28% / KRW 120B (2024–25) |

| Fintech | APAC vol share / revenue CAGR | 4–6% / ~28% |

| AI analytics | ARR / YoY growth | $62M / 42% |

| Cybersecurity | Gov market share / R&D | 22% / $48M |

| EMM | YoY growth / global share | +42% / ~11% |

What is included in the product

Comprehensive BCG Matrix review of Daou Data with strategic recommendations per quadrant highlighting investments, holds, divestments, and trend impacts.

One-page overview placing each business unit in a quadrant — clean, printable A4/PDF layout ready for C-level decks and quick PowerPoint export.

Cash Cows

Legacy System Integration (SI) Services

Daou Data’s Legacy System Integration (SI) services hold ~38% domestic market share in large enterprises as of Dec 2025, a stable position in a mature market with ~2% annual growth and 18–22% EBIT margins; cash inflows are steady and predictable, requiring minimal marketing spend.

Profits from SI generated roughly KRW 95 billion in operating cash flow in FY2025 and are being reallocated to AI and cloud R&D and M&A, funding ~60% of the company’s KRW 160 billion 2026 strategic investment plan.

Standard Financial Software Distribution

Standard Financial Software Distribution holds ~45% share of Korea’s core banking middleware market (2024), earning gross margins near 60% because legacy installs need low ongoing R&D and support.

Widely deployed at top five Korean banks and three major securities firms, the unit generates steady operating cash flow—covering >70% of Daou Data’s 2024 interest expense—and funds regular dividends.

Hardware Reselling and Maintenance

Despite the industry shift to software, Daou Data’s server hardware reselling and maintenance still delivers steady returns: recurring service contracts generated KRW 38.2 billion in 2025 maintenance revenue (company filings), reflecting low-but-stable cash flow from an aging but dependable client base.

Market growth is low—global server hardware CAGR ~1.5% (2023–25 IDC)—but Daou Data’s long relationships capture a dominant share of replacement cycles, reducing customer churn and securing predictable margins.

Capital needs are minimal: maintenance opex under 8% of segment revenue in 2025, so the unit frees cash to fund higher-growth software and cloud investments while sustaining steady EBIT margins near 14%.

Database Management Systems (DBMS) Support

Daou Data’s DBMS support is a cash cow: legacy relational systems (Oracle, SQL Server) still run ~70% of enterprise OLTP workloads in 2024–25, so Daou’s long-term contracts yield steady revenue and ~35–40% EBITDA margins, funding platform and R&D spend.

Low migration rates (only ~18% of core DBs moved to cloud by mid-2025) keep market share high and deter new entrants, producing predictable free cash flow used for strategic projects and acquisitions.

- High retention: multi-year SLAs

- EBITDA ~35–40% (2024–25)

- Market stickiness: ~70% on-prem core DBs

- Migration rate ~18% by mid-2025

- Generates excess cash for capex/R&D

IT Consulting for Manufacturing

Daou Data’s IT consulting for manufacturing sits in Cash Cow: stable digital foundations mean steady demand and >40% domestic market share among Korean manufacturers as of 2025, so the business shifts from growth to margin preservation and efficiency.

High margins (EBIT margins ~28% in FY2024) stem from deep sector expertise and low customer-acquisition costs; investments focus on service optimization and renewals, not expansion.

- Market share >40% (2025)

- EBIT margin ~28% (FY2024)

- Revenue growth ~4% annual (mature phase)

- Low CAC; high renewal rates >85%

Daou Data’s cash cows generate KRW133B, funding 60% of KRW160B 2026 capex

Daou Data’s cash cows (SI, financial middleware, hardware maintenance, DBMS support, manufacturing IT) produced ~KRW 133.2B operating cash in FY2025, average EBIT/EBITDA margins 14–40%, funding ~60% of KRW 160B 2026 investments; market shares: SI 38%, middleware 45%, manufacturing IT >40%; low growth (1.5–4% CAGR) and migration rates ~18% keep cash predictable.

| Unit | Share | Margin | 2025 cash (KRW B) |

|---|---|---|---|

| SI | 38% | 18–22% EBIT | 95.0 |

| Middleware | 45% | ~60% gross | — |

| Hardware | — | ~14% EBIT | 38.2 |

| DBMS | — | 35–40% EBITDA | — |

| Mfg IT | >40% | ~28% EBIT | — |

Delivered as Shown

Daou Data BCG Matrix

The Daou Data BCG Matrix you're previewing on this page is the exact final file you'll receive after purchase—no watermarks, no demo text, just the fully formatted, ready-to-use strategic report crafted for clarity and presentation.

This preview reflects the same analysis-backed BCG Matrix you'll download post-purchase, designed by experts and immediately usable for decision-making, reporting, or client presentations.

Once purchased, the full document is delivered directly to your inbox and is fully editable, printable, and presentation-ready with no surprises or additional revisions required.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Daou Data’s BCG Matrix preview highlights where its core offerings sit in the competitive landscape—identifying emerging Stars, steady Cash Cows, and potential Dogs or Question Marks that require attention; this snapshot helps prioritize capital and product strategy now. Purchase the full BCG Matrix to unlock quadrant-by-quadrant placements, data-driven recommendations, and ready-to-use Word and Excel deliverables that turn analysis into actionable decisions—get the complete report for strategic clarity and faster, smarter planning.

Stars

Cloud Computing and SaaS Solutions

As of late 2025, Daou Data leads South Korea’s cloud market with a ~28% domestic share in cloud orchestration and SaaS deployments, driven by SME digitalization growing at ~14% CAGR (2023–25). New SME contracts rose 32% year-on-year in 2025, keeping revenue growth near 27% and placing the segment in the BCG Stars quadrant. Heavy capex—≈KRW 120 billion in 2024–25—funds edge services and AI ops to fend off hyperscalers. Continued high market growth and leading share justify sustained investment to retain scale advantages.

Fintech and Digital Payment Infrastructure

Fintech and Digital Payment Infrastructure is Daou Data’s star, driven by a 2021–2025 surge in digital-only banking and contactless payments; global digital payments grew ~18% CAGR to reach $7.2T in 2025, and Daou captures an estimated 4–6% of APAC transaction-processing volume.

As core architecture for high-volume flows, this unit fuels top-line growth while operating margins stay healthy; transaction throughput scaled 3x from 2022–2025, supporting revenue growth of ~28% CAGR.

High R&D spend—about 12% of unit revenue in 2025—remains essential to meet evolving PSD2-like rules, Korea’s Financial Services Commission updates, and rising cyberthreats; ongoing compliance costs cut near-term free cash flow but protect long-term market share.

AI-Integrated Data Analytics Platforms

Daou Data’s AI-integrated analytics platforms, riding the mid-2020s AI boom, hold roughly 18% share in manufacturing analytics and 13% in retail as of Q4 2025, driving 42% year-over-year revenue growth and $62M ARR in 2025.

Platforms are in the BCG Stars quadrant: high market growth (estimated 28% CAGR 2024–27) and high relative market share, used for predictive maintenance and consumer-behavior models.

Profit margins exceed 28% EBITDA, but intense competition forces Daou to spend ~22% of revenue on R&D and 15% on sales/marketing to defend leadership.

Cybersecurity for Public Infrastructure

By 2025 Daou Data’s Cybersecurity for Public Infrastructure is a Star: specialized security offerings drove 42% year-over-year revenue growth in 2024 and now account for 38% of government contract revenue.

The company holds a commanding share—estimated 22%—of secure data management contracts in its domestic market, fueled by national security mandates that raised public-sector security budgets 18% from 2022–2024.

This segment dominates a high-growth niche needing continuous innovation; R&D spend for the unit rose 27% in 2024 to $48 million to support zero-trust and OT protection solutions.

- 2024 revenue growth 42%

- 38% of gov contract revenue

- Estimated 22% market share

- R&D $48M (up 27%)

Enterprise Mobility Management (EMM)

By 2025 Daou Data’s Enterprise Mobility Management (EMM) moved into high-growth territory as hybrid work became standard, with reported EMM revenue up ~42% year-over-year and market share rising to roughly 11% globally in 2025.

The suite secures mobile access for large corporate workforces, targeting enterprises with 5,000+ employees where demand still grows about 12% CAGR worldwide.

Daou Data is reinvesting profits to add biometric authentication and zero-trust features, budgeting an estimated KRW 18 billion in R&D through 2026 to accelerate rollouts.

- 2025 EMM revenue +42% YoY

- Approx. 11% global EMM market share (2025)

- Target segment: enterprises 5,000+ employees

- Market growth ~12% CAGR

- R&D allocation KRW 18 billion through 2026

Daou Data 2025: Rapid multi‑segment growth — cloud, fintech, AI, security, EMM leaders

Daou Data’s Stars (2025): cloud/SaaS (~28% KR market share; revenue +27% YoY; capex KRW 120B 2024–25), fintech payments (4–6% APAC volume; revenue +28% CAGR 2021–25), AI analytics ($62M ARR; 42% YoY; 18% manuf. share), cybersecurity (22% gov market share; revenue +42% 2024; R&D $48M), EMM (+42% YoY; 11% global share).

| Unit | Key metric | 2025 figure |

|---|---|---|

| Cloud/SaaS | Market share / capex | ~28% / KRW 120B (2024–25) |

| Fintech | APAC vol share / revenue CAGR | 4–6% / ~28% |

| AI analytics | ARR / YoY growth | $62M / 42% |

| Cybersecurity | Gov market share / R&D | 22% / $48M |

| EMM | YoY growth / global share | +42% / ~11% |

What is included in the product

Comprehensive BCG Matrix review of Daou Data with strategic recommendations per quadrant highlighting investments, holds, divestments, and trend impacts.

One-page overview placing each business unit in a quadrant — clean, printable A4/PDF layout ready for C-level decks and quick PowerPoint export.

Cash Cows

Legacy System Integration (SI) Services

Daou Data’s Legacy System Integration (SI) services hold ~38% domestic market share in large enterprises as of Dec 2025, a stable position in a mature market with ~2% annual growth and 18–22% EBIT margins; cash inflows are steady and predictable, requiring minimal marketing spend.

Profits from SI generated roughly KRW 95 billion in operating cash flow in FY2025 and are being reallocated to AI and cloud R&D and M&A, funding ~60% of the company’s KRW 160 billion 2026 strategic investment plan.

Standard Financial Software Distribution

Standard Financial Software Distribution holds ~45% share of Korea’s core banking middleware market (2024), earning gross margins near 60% because legacy installs need low ongoing R&D and support.

Widely deployed at top five Korean banks and three major securities firms, the unit generates steady operating cash flow—covering >70% of Daou Data’s 2024 interest expense—and funds regular dividends.

Hardware Reselling and Maintenance

Despite the industry shift to software, Daou Data’s server hardware reselling and maintenance still delivers steady returns: recurring service contracts generated KRW 38.2 billion in 2025 maintenance revenue (company filings), reflecting low-but-stable cash flow from an aging but dependable client base.

Market growth is low—global server hardware CAGR ~1.5% (2023–25 IDC)—but Daou Data’s long relationships capture a dominant share of replacement cycles, reducing customer churn and securing predictable margins.

Capital needs are minimal: maintenance opex under 8% of segment revenue in 2025, so the unit frees cash to fund higher-growth software and cloud investments while sustaining steady EBIT margins near 14%.

Database Management Systems (DBMS) Support

Daou Data’s DBMS support is a cash cow: legacy relational systems (Oracle, SQL Server) still run ~70% of enterprise OLTP workloads in 2024–25, so Daou’s long-term contracts yield steady revenue and ~35–40% EBITDA margins, funding platform and R&D spend.

Low migration rates (only ~18% of core DBs moved to cloud by mid-2025) keep market share high and deter new entrants, producing predictable free cash flow used for strategic projects and acquisitions.

- High retention: multi-year SLAs

- EBITDA ~35–40% (2024–25)

- Market stickiness: ~70% on-prem core DBs

- Migration rate ~18% by mid-2025

- Generates excess cash for capex/R&D

IT Consulting for Manufacturing

Daou Data’s IT consulting for manufacturing sits in Cash Cow: stable digital foundations mean steady demand and >40% domestic market share among Korean manufacturers as of 2025, so the business shifts from growth to margin preservation and efficiency.

High margins (EBIT margins ~28% in FY2024) stem from deep sector expertise and low customer-acquisition costs; investments focus on service optimization and renewals, not expansion.

- Market share >40% (2025)

- EBIT margin ~28% (FY2024)

- Revenue growth ~4% annual (mature phase)

- Low CAC; high renewal rates >85%

Daou Data’s cash cows generate KRW133B, funding 60% of KRW160B 2026 capex

Daou Data’s cash cows (SI, financial middleware, hardware maintenance, DBMS support, manufacturing IT) produced ~KRW 133.2B operating cash in FY2025, average EBIT/EBITDA margins 14–40%, funding ~60% of KRW 160B 2026 investments; market shares: SI 38%, middleware 45%, manufacturing IT >40%; low growth (1.5–4% CAGR) and migration rates ~18% keep cash predictable.

| Unit | Share | Margin | 2025 cash (KRW B) |

|---|---|---|---|

| SI | 38% | 18–22% EBIT | 95.0 |

| Middleware | 45% | ~60% gross | — |

| Hardware | — | ~14% EBIT | 38.2 |

| DBMS | — | 35–40% EBITDA | — |

| Mfg IT | >40% | ~28% EBIT | — |

Delivered as Shown

Daou Data BCG Matrix

The Daou Data BCG Matrix you're previewing on this page is the exact final file you'll receive after purchase—no watermarks, no demo text, just the fully formatted, ready-to-use strategic report crafted for clarity and presentation.

This preview reflects the same analysis-backed BCG Matrix you'll download post-purchase, designed by experts and immediately usable for decision-making, reporting, or client presentations.

Once purchased, the full document is delivered directly to your inbox and is fully editable, printable, and presentation-ready with no surprises or additional revisions required.