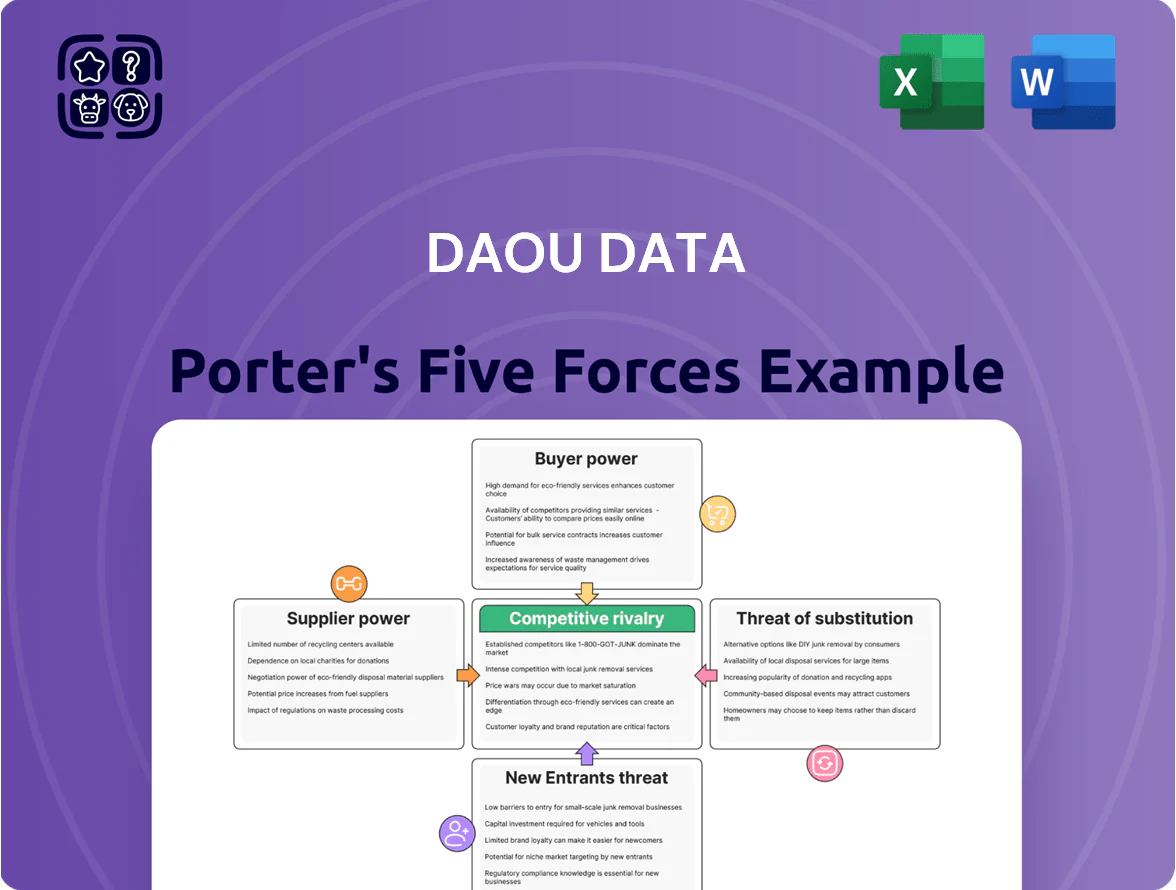

Daou Data Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Daou Data’s Five Forces snapshot highlights competitive intensity driven by concentrated buyers and rapid tech substitution risks, while supplier leverage and regulatory trends create nuanced pressure points investors should watch.

This brief preview only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications tailored to Daou Data for smarter investment and planning.

Suppliers Bargaining Power

Concentration of Hyperscale Cloud Providers

DAOU Data depends on AWS, Microsoft Azure, and Google Cloud for core infrastructure; together they held ~64% of global cloud IaaS/PaaS market in 2024, giving suppliers strong leverage.

High migration complexity—multi-month refactoring and egress fees—raises switching costs, so DAOU has limited room to demand lower prices or bespoke SLA terms.

Scarcity of Specialized Technical Talent

High-skilled human capital—developers and cybersecurity experts—is Daou Data’s primary resource, and by late 2025 demand for AI and cloud architects in South Korea exceeded supply by an estimated 25–30%, raising bargaining power for individuals and niche staffing agencies.

Wage inflation hit tech roles: median developer pay rose ~12% YoY in 2025, forcing Daou Data to raise compensation packages by roughly 8–15% to retain staff and avoid poaching.

Proprietary Software Licensing Constraints

For system integration and data management, DAOU Data must license core database and middleware tech from global vendors who enforce rigid pricing and mandatory maintenance—Oracle, Microsoft, and IBM still account for roughly 60% of enterprise DB market share as of 2025, so switching costs are high. Mandatory support fees can equal 15–25% of license value annually, constraining margins and giving suppliers clear pricing power. DAOU Data has limited vendor substitution options because those components are often integral to client architectures.

Hardware Supply Chain Volatility

Procurement of high-performance servers and networking gear for Daou Data’s private cloud is tied to global semiconductor cycles; chip shortages in 2021–22 pushed server lead times to 30–40 weeks, though 2024 averages fell to ~10–12 weeks per IDC.

Any renewed geopolitical tension in East Asia could extend lead times >20 weeks, forcing higher safety stock or accepting 5–15% price increases to hit project deadlines.

- Lead time baseline: ~10–12 weeks (2024, IDC)

- Upside risk: >20 weeks if tensions spike

- Cost impact: 5–15% price rise

- Mitigation: higher inventory or flexible suppliers

Strategic Partnerships with Security Vendors

In cybersecurity, DAOU Data distributes and integrates specialized global security software, relying on vendors who control threat-intel roadmaps and updates; in 2024, global security software market grew 11% to $63.5B, keeping vendor leverage high.

If a major partner shifts channel strategy or raises margins by 5–10%, DAOU Data’s cybersecurity segment margin could drop proportionally, materially hitting 2025 EBITDA in that line.

- Vendor control of updates = high switching cost

- 2024 market: $63.5B, +11%

- Margin shift 5–10% → direct profit hit

- Dependence raises negotiation risk

Supplier power tightens margins—cloud, DBs, wages, chips raise switching costs

Suppliers hold strong leverage: AWS/Azure/GCP ~64% IaaS/PaaS (2024), Oracle/Microsoft/IBM ~60% DB market (2025), security software $63.5B (+11% 2024), and developer pay +12% YoY (2025) raising wage costs 8–15% for retention; chip lead times 10–12w (2024) with >20w risk—together these raise switching costs, squeeze margins, and limit Daou Data’s negotiating room.

| Metric | Value |

|---|---|

| Cloud share (2024) | ~64% |

| DB vendors (2025) | ~60% |

| Security market (2024) | $63.5B |

| Dev pay change (2025) | +12% YoY |

| Server lead time (2024) | 10–12 wks |

What is included in the product

Comprehensive Five Forces assessment for Daou Data that identifies competitive pressures, customer and supplier bargaining power, entry barriers, substitute threats, and strategic implications for pricing, profitability, and market positioning.

Daou Data Porter's Five Forces delivers a concise, one-sheet assessment of competitive pressures with customizable ratings and a spider chart for instant strategic clarity—easy to drop into decks or link to broader Excel dashboards.

Customers Bargaining Power

Concentrated Public Sector Procurement

A large share of Daou Data Porter revenue—about 42% in FY2024—comes from government and public-sector contracts awarded via competitive bids, giving institutional buyers strong leverage to push prices down and demand strict SLAs; public tenders in 2024 showed average contract discounting of 18% versus commercial rates, and open procurement portals let agencies benchmark offers across at least five suppliers, raising pricing pressure and margin squeeze.

High Switching Costs for Financial Institutions

Clients in finance form DAOU Data’s core market for system integration and software; these deployments are mission-critical and often span payment, risk and trading systems where downtime costs can exceed $5k–$9k per minute (2023 Uptime Institute).

The deep technical integration creates high switching costs—estimated implementation times of 6–18 months and migration budgets of $0.5–$5M—so clients face material operational and regulatory risk.

This lock-in gives DAOU Data pricing leverage and protection from aggressive client negotiations, reducing churn: enterprise retention for mission-critical vendors often exceeds 90% annually (2024 surveys).

Demand for Bespoke Customization

Large manufacturing clients demand bespoke IT tied to specific workflows, letting them push Daou Data for extra features without higher fees; a 2024 Gartner report found 62% of manufacturers prioritize customization, raising customer bargaining power. Custom projects often consume 40–60% of implementation hours, locking resources to single clients for months and increasing revenue concentration risk when top 5 clients account for 48% of sales.

Information Symmetry and Market Transparency

By end-2025, a surge in IT consultancies pushed cloud and systems-integration (SI) pricing transparency: market-rate databases show median cloud migration fees down 12% year-over-year and SI hourly rates clustered within a ±8% band, limiting Daou Data’s premium pricing room.

Buyers use benchmarking and third-party reviews, so decision-makers prioritize measurable ROI and outcomes, forcing Daou Data to compete on value—service SLAs, integration speed, and post-deploy analytics—rather than opaque pricing.

- Median cloud migration fee down 12% YoY (2025)

- SI hourly rates within ±8% range

- Buyers demand ROI, SLAs, speed, analytics

Consolidation of Corporate IT Budgets

As enterprises consolidate digital transformation budgets, large accounts shift more spend to a handful of vendors, raising customer bargaining power; Gartner reported 2024 enterprise cloud spend grew 21% to $625B, concentrating negotiating leverage.

Major accounts now demand volume discounts and dedicated SLAs, so DAOU Data must offer integrated pricing, preferential support, and co-innovation to retain status in consolidated ecosystems.

- Gartner 2024: enterprise cloud spend +21% to $625B

- Top 10 accounts can represent 20–40% of vendor revenue

- Volume discounts, bespoke SLAs, joint roadmaps win retention

High customer leverage: public bids, heavy discounts, retention vs. SI price pressure

Customers hold mixed but strong bargaining power: public bids (~42% FY2024) drive average discounts of 18% and benchmarking; finance clients have high switching costs (6–18 months, $0.5–$5M) and >90% retention; manufacturing demands raise customization (62% prefer bespoke); market-rate SI fees down 12% YoY (2025), SI rates ±8%—forcing Daou Data to compete on SLAs, ROI, speed, and co-innovation.

| Metric | Value |

|---|---|

| Public revenue FY2024 | 42% |

| Avg public discount | 18% |

| Switching cost time | 6–18 months |

| Migration budget | $0.5–$5M |

| SI fees change (2025) | −12% YoY |

What You See Is What You Get

Daou Data Porter's Five Forces Analysis

This preview shows the exact Daou Data Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, no placeholders, and ready for download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Daou Data’s Five Forces snapshot highlights competitive intensity driven by concentrated buyers and rapid tech substitution risks, while supplier leverage and regulatory trends create nuanced pressure points investors should watch.

This brief preview only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications tailored to Daou Data for smarter investment and planning.

Suppliers Bargaining Power

Concentration of Hyperscale Cloud Providers

DAOU Data depends on AWS, Microsoft Azure, and Google Cloud for core infrastructure; together they held ~64% of global cloud IaaS/PaaS market in 2024, giving suppliers strong leverage.

High migration complexity—multi-month refactoring and egress fees—raises switching costs, so DAOU has limited room to demand lower prices or bespoke SLA terms.

Scarcity of Specialized Technical Talent

High-skilled human capital—developers and cybersecurity experts—is Daou Data’s primary resource, and by late 2025 demand for AI and cloud architects in South Korea exceeded supply by an estimated 25–30%, raising bargaining power for individuals and niche staffing agencies.

Wage inflation hit tech roles: median developer pay rose ~12% YoY in 2025, forcing Daou Data to raise compensation packages by roughly 8–15% to retain staff and avoid poaching.

Proprietary Software Licensing Constraints

For system integration and data management, DAOU Data must license core database and middleware tech from global vendors who enforce rigid pricing and mandatory maintenance—Oracle, Microsoft, and IBM still account for roughly 60% of enterprise DB market share as of 2025, so switching costs are high. Mandatory support fees can equal 15–25% of license value annually, constraining margins and giving suppliers clear pricing power. DAOU Data has limited vendor substitution options because those components are often integral to client architectures.

Hardware Supply Chain Volatility

Procurement of high-performance servers and networking gear for Daou Data’s private cloud is tied to global semiconductor cycles; chip shortages in 2021–22 pushed server lead times to 30–40 weeks, though 2024 averages fell to ~10–12 weeks per IDC.

Any renewed geopolitical tension in East Asia could extend lead times >20 weeks, forcing higher safety stock or accepting 5–15% price increases to hit project deadlines.

- Lead time baseline: ~10–12 weeks (2024, IDC)

- Upside risk: >20 weeks if tensions spike

- Cost impact: 5–15% price rise

- Mitigation: higher inventory or flexible suppliers

Strategic Partnerships with Security Vendors

In cybersecurity, DAOU Data distributes and integrates specialized global security software, relying on vendors who control threat-intel roadmaps and updates; in 2024, global security software market grew 11% to $63.5B, keeping vendor leverage high.

If a major partner shifts channel strategy or raises margins by 5–10%, DAOU Data’s cybersecurity segment margin could drop proportionally, materially hitting 2025 EBITDA in that line.

- Vendor control of updates = high switching cost

- 2024 market: $63.5B, +11%

- Margin shift 5–10% → direct profit hit

- Dependence raises negotiation risk

Supplier power tightens margins—cloud, DBs, wages, chips raise switching costs

Suppliers hold strong leverage: AWS/Azure/GCP ~64% IaaS/PaaS (2024), Oracle/Microsoft/IBM ~60% DB market (2025), security software $63.5B (+11% 2024), and developer pay +12% YoY (2025) raising wage costs 8–15% for retention; chip lead times 10–12w (2024) with >20w risk—together these raise switching costs, squeeze margins, and limit Daou Data’s negotiating room.

| Metric | Value |

|---|---|

| Cloud share (2024) | ~64% |

| DB vendors (2025) | ~60% |

| Security market (2024) | $63.5B |

| Dev pay change (2025) | +12% YoY |

| Server lead time (2024) | 10–12 wks |

What is included in the product

Comprehensive Five Forces assessment for Daou Data that identifies competitive pressures, customer and supplier bargaining power, entry barriers, substitute threats, and strategic implications for pricing, profitability, and market positioning.

Daou Data Porter's Five Forces delivers a concise, one-sheet assessment of competitive pressures with customizable ratings and a spider chart for instant strategic clarity—easy to drop into decks or link to broader Excel dashboards.

Customers Bargaining Power

Concentrated Public Sector Procurement

A large share of Daou Data Porter revenue—about 42% in FY2024—comes from government and public-sector contracts awarded via competitive bids, giving institutional buyers strong leverage to push prices down and demand strict SLAs; public tenders in 2024 showed average contract discounting of 18% versus commercial rates, and open procurement portals let agencies benchmark offers across at least five suppliers, raising pricing pressure and margin squeeze.

High Switching Costs for Financial Institutions

Clients in finance form DAOU Data’s core market for system integration and software; these deployments are mission-critical and often span payment, risk and trading systems where downtime costs can exceed $5k–$9k per minute (2023 Uptime Institute).

The deep technical integration creates high switching costs—estimated implementation times of 6–18 months and migration budgets of $0.5–$5M—so clients face material operational and regulatory risk.

This lock-in gives DAOU Data pricing leverage and protection from aggressive client negotiations, reducing churn: enterprise retention for mission-critical vendors often exceeds 90% annually (2024 surveys).

Demand for Bespoke Customization

Large manufacturing clients demand bespoke IT tied to specific workflows, letting them push Daou Data for extra features without higher fees; a 2024 Gartner report found 62% of manufacturers prioritize customization, raising customer bargaining power. Custom projects often consume 40–60% of implementation hours, locking resources to single clients for months and increasing revenue concentration risk when top 5 clients account for 48% of sales.

Information Symmetry and Market Transparency

By end-2025, a surge in IT consultancies pushed cloud and systems-integration (SI) pricing transparency: market-rate databases show median cloud migration fees down 12% year-over-year and SI hourly rates clustered within a ±8% band, limiting Daou Data’s premium pricing room.

Buyers use benchmarking and third-party reviews, so decision-makers prioritize measurable ROI and outcomes, forcing Daou Data to compete on value—service SLAs, integration speed, and post-deploy analytics—rather than opaque pricing.

- Median cloud migration fee down 12% YoY (2025)

- SI hourly rates within ±8% range

- Buyers demand ROI, SLAs, speed, analytics

Consolidation of Corporate IT Budgets

As enterprises consolidate digital transformation budgets, large accounts shift more spend to a handful of vendors, raising customer bargaining power; Gartner reported 2024 enterprise cloud spend grew 21% to $625B, concentrating negotiating leverage.

Major accounts now demand volume discounts and dedicated SLAs, so DAOU Data must offer integrated pricing, preferential support, and co-innovation to retain status in consolidated ecosystems.

- Gartner 2024: enterprise cloud spend +21% to $625B

- Top 10 accounts can represent 20–40% of vendor revenue

- Volume discounts, bespoke SLAs, joint roadmaps win retention

High customer leverage: public bids, heavy discounts, retention vs. SI price pressure

Customers hold mixed but strong bargaining power: public bids (~42% FY2024) drive average discounts of 18% and benchmarking; finance clients have high switching costs (6–18 months, $0.5–$5M) and >90% retention; manufacturing demands raise customization (62% prefer bespoke); market-rate SI fees down 12% YoY (2025), SI rates ±8%—forcing Daou Data to compete on SLAs, ROI, speed, and co-innovation.

| Metric | Value |

|---|---|

| Public revenue FY2024 | 42% |

| Avg public discount | 18% |

| Switching cost time | 6–18 months |

| Migration budget | $0.5–$5M |

| SI fees change (2025) | −12% YoY |

What You See Is What You Get

Daou Data Porter's Five Forces Analysis

This preview shows the exact Daou Data Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, no placeholders, and ready for download and use the moment you buy.