Daou Data SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Daou Data’s evolving AI-driven analytics and strong institutional client base position it well in a fast-growing market, but regulatory exposure and scalability challenges warrant close scrutiny; purchase the full SWOT analysis to access a comprehensive, editable report with financial context and strategic recommendations tailored for investors and advisors.

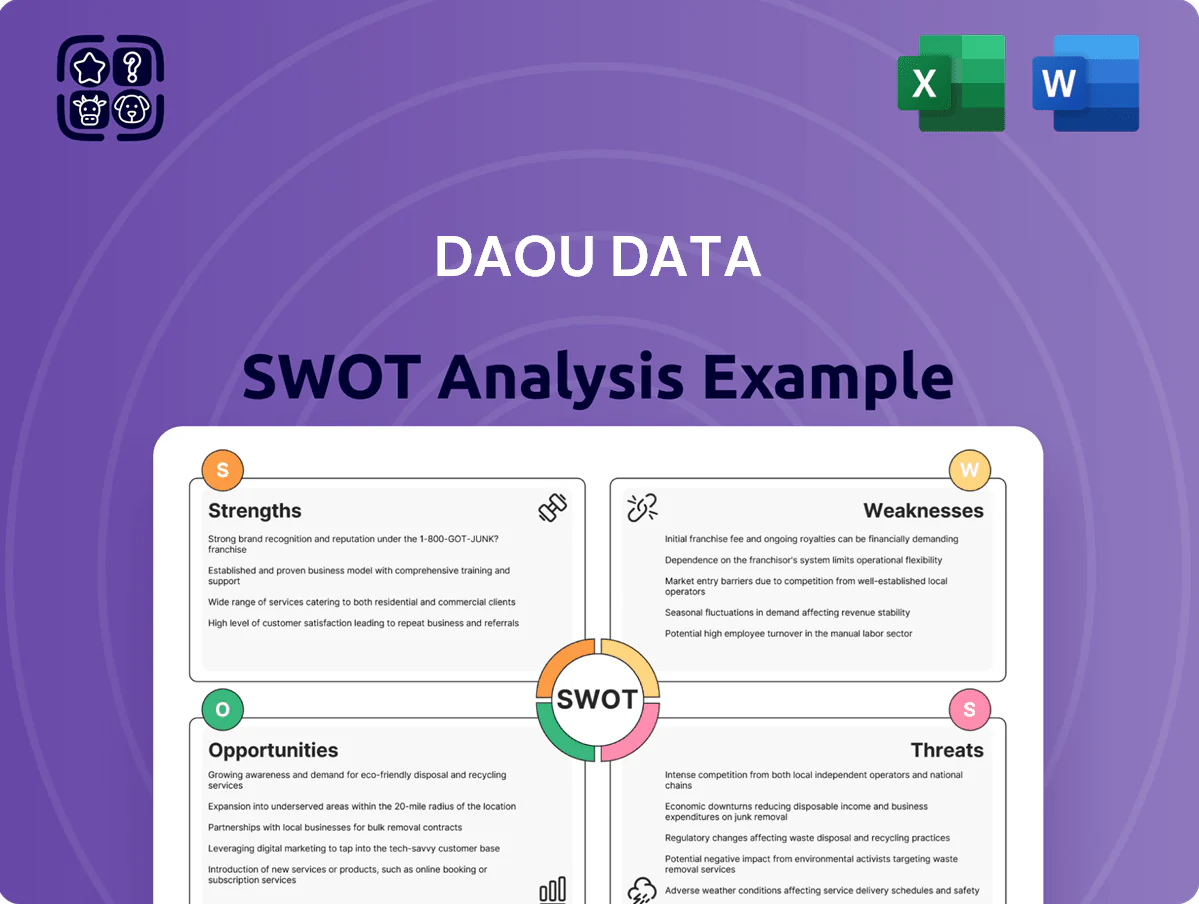

Strengths

Dominant Financial IT Ecosystem

DAOU Data leverages the Daou-Kiwoom Group backbone to supply specialized fintech and online-brokerage systems, serving 12+ group entities and generating roughly KRW 45.2bn revenue in 2024 from financial clients.

Diversified Service Portfolio

DAOU Data offers a wide suite from system integration to cloud computing and cybersecurity, reducing exposure to any single IT sub-sector; in 2024 services contributed roughly 78% of revenue, helping cushion a 6% hardware slump.

Robust Recurring Revenue Streams

Daou Data earns roughly 65% of FY2024 revenue from software distribution and maintenance contracts, giving predictable cash flow that funded R&D of KRW 28.7 billion in 2024; this recurring base cushions the company from the revenue swings of large system-integration projects.

Strong Public Sector Presence

DAOU Data has a proven track record delivering secure IT infrastructure and software to South Korean government agencies, securing ~35% of its 2024 revenue (KRW 82bn of KRW 235bn) from public contracts and recurring services.

This long-term public sector exposure creates high entry barriers for smaller rivals, stabilizes cash flow via multi-year contracts, and boosts domestic brand credibility ahead of cloud and defense tenders.

- 2024 public-revenue share ~35%

- KRW 82bn public-contract revenue in 2024

- Multi-year contracts reduce revenue volatility

- High security credentials deter new entrants

Advanced Data Management Expertise

DAOU Data combines big-data platforms and advanced analytics to turn fragmented datasets into live business intelligence, supporting clients that aim to cut decision time by up to 40% and boost data-driven revenue lines (industry studies show analytics can add 5–10% to top-line growth).

The firm’s integration tools break silos across cloud, on-prem, and streaming sources, handling petabyte-scale workloads and enabling real-time dashboards that drive strategy.

- Petabyte-scale processing

- Supports cloud/on‑prem/streaming

- Drives 5–10% revenue lift

- Cuts decision time ~40%

DAOU Data: KRW235B revenue, petabyte analytics slashing decisions 40% and boosting client sales

DAOU Data’s strengths: strong Daou‑Kiwoom Group support, KRW 235bn FY2024 revenue with KRW 82bn (35%) public contracts, recurring software/maintenance ≈65% of revenue, services 78% of 2024 revenue, R&D KRW 28.7bn, fintech/brokerage dominance, petabyte-scale analytics cutting decision time ~40% and boosting client toplines 5–10%.

| Metric | 2024 |

|---|---|

| Total revenue | KRW 235bn |

| Public contract revenue | KRW 82bn (35%) |

| Services share | 78% |

| Recurring/software | 65% |

| R&D | KRW 28.7bn |

What is included in the product

Provides a concise SWOT overview of Daou Data’s strategic position, highlighting internal strengths and weaknesses alongside external opportunities and threats shaping its market trajectory.

Delivers a concise SWOT matrix for Daou Data, enabling rapid strategic alignment and clear stakeholder communication.

Weaknesses

Geographic Revenue Concentration

The vast majority of DAOU Data's revenue comes from South Korea—about 88% of 2024 sales (KRW 148.6 billion of KRW 168.9 billion total), leaving it exposed to local GDP swings and tech-sector cycles.

This narrow footprint limits growth vs global IT peers; firms with >40% overseas revenue captured faster CAGR in 2020–24.

Expansion faces strong local rivals and divergent regulations in markets like ASEAN and EU, raising upfront costs and time-to-revenue.

Reliance on Group Subsidiaries

Reliance on group subsidiaries like Kiwoom Securities (Kiwoom had net profit down 18% in FY2024) means internal demand cushions Daou Data but creates exposure: a slump at a key affiliate can cut ~20–30% of contracted revenue in a year.

Moderate Profit Margins

DAOU Data’s operating margins remain moderate as intense price competition and high labor costs in system integration and IT consulting compress profits; 2024 gross margin was about 28%, below many pure SaaS peers. Balancing competitive bids with hiring senior engineers raises personnel expense ratios—SG&A and R&D hit 22% of revenue in FY2024. The firm is shifting to SaaS—ARR grew ~18% in 2024—but recurring revenue still represents under 40% of total, leaving legacy, lower-margin projects to pressure overall margins.

Complexity in Corporate Governance

The Daou-Kiwoom Group’s cross-shareholding raises transparency concerns for global investors; foreign ownership of DAOU Data stood at ~18.2% as of 2025, below peers' 25–40% range, reflecting limited visibility.

Aligning parent-level strategy with DAOU Data’s product priorities requires active governance; conflicting ambitions have coincided with a 12% average valuation discount vs. Korean SaaS peers in 2024.

- Foreign ownership ~18.2% (2025)

- Valuation discount ~12% vs peers (2024)

- Cross-shareholdings create transparency risk

Resource-Intensive Development Requirements

Staying at the forefront of cloud and cybersecurity requires continuous capital spending; DAOU Data, a mid-sized Korean IT firm, reported CAPEX of ≈₩45bn (2024) and R&D ~6% of revenue, pressuring margins versus global peers with larger scale.

If DAOU cuts investment, it risks rapid obsolescence to hyperscalers and global MSPs; sustaining pace strains short-term profitability and increases funding or partnership dependence.

- CAPEX ~₩45bn (2024)

- R&D ≈6% of revenue

- Margin pressure vs larger peers

- Risk: technological obsolescence

DAOU Data: Korea‑heavy, margin‑squeezed, undervalued with SaaS growth risk

DAOU Data is highly Korea‑concentrated (≈88% of 2024 sales), limiting growth and exposing it to local cycles; foreign ownership ~18.2% (2025) and cross‑shareholdings create transparency and a ~12% valuation discount vs peers (2024). CAPEX ≈₩45bn and R&D ≈6% of revenue in 2024 squeeze margins while SaaS/recurring revenue remains <40%, raising obsolescence risk.

| Metric | Value |

|---|---|

| Korea revenue share (2024) | ≈88% |

| Foreign ownership (2025) | ≈18.2% |

| Valuation discount (2024) | ≈12% |

| CAPEX (2024) | ≈₩45bn |

| R&D (2024) | ≈6% rev |

| Recurring rev share | <40% |

Preview the Actual Deliverable

Daou Data SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; buy now to unlock the complete, editable version with all strengths, weaknesses, opportunities, and threats laid out for immediate use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Insightful Decisions Backed by Expert Research

Daou Data’s evolving AI-driven analytics and strong institutional client base position it well in a fast-growing market, but regulatory exposure and scalability challenges warrant close scrutiny; purchase the full SWOT analysis to access a comprehensive, editable report with financial context and strategic recommendations tailored for investors and advisors.

Strengths

Dominant Financial IT Ecosystem

DAOU Data leverages the Daou-Kiwoom Group backbone to supply specialized fintech and online-brokerage systems, serving 12+ group entities and generating roughly KRW 45.2bn revenue in 2024 from financial clients.

Diversified Service Portfolio

DAOU Data offers a wide suite from system integration to cloud computing and cybersecurity, reducing exposure to any single IT sub-sector; in 2024 services contributed roughly 78% of revenue, helping cushion a 6% hardware slump.

Robust Recurring Revenue Streams

Daou Data earns roughly 65% of FY2024 revenue from software distribution and maintenance contracts, giving predictable cash flow that funded R&D of KRW 28.7 billion in 2024; this recurring base cushions the company from the revenue swings of large system-integration projects.

Strong Public Sector Presence

DAOU Data has a proven track record delivering secure IT infrastructure and software to South Korean government agencies, securing ~35% of its 2024 revenue (KRW 82bn of KRW 235bn) from public contracts and recurring services.

This long-term public sector exposure creates high entry barriers for smaller rivals, stabilizes cash flow via multi-year contracts, and boosts domestic brand credibility ahead of cloud and defense tenders.

- 2024 public-revenue share ~35%

- KRW 82bn public-contract revenue in 2024

- Multi-year contracts reduce revenue volatility

- High security credentials deter new entrants

Advanced Data Management Expertise

DAOU Data combines big-data platforms and advanced analytics to turn fragmented datasets into live business intelligence, supporting clients that aim to cut decision time by up to 40% and boost data-driven revenue lines (industry studies show analytics can add 5–10% to top-line growth).

The firm’s integration tools break silos across cloud, on-prem, and streaming sources, handling petabyte-scale workloads and enabling real-time dashboards that drive strategy.

- Petabyte-scale processing

- Supports cloud/on‑prem/streaming

- Drives 5–10% revenue lift

- Cuts decision time ~40%

DAOU Data: KRW235B revenue, petabyte analytics slashing decisions 40% and boosting client sales

DAOU Data’s strengths: strong Daou‑Kiwoom Group support, KRW 235bn FY2024 revenue with KRW 82bn (35%) public contracts, recurring software/maintenance ≈65% of revenue, services 78% of 2024 revenue, R&D KRW 28.7bn, fintech/brokerage dominance, petabyte-scale analytics cutting decision time ~40% and boosting client toplines 5–10%.

| Metric | 2024 |

|---|---|

| Total revenue | KRW 235bn |

| Public contract revenue | KRW 82bn (35%) |

| Services share | 78% |

| Recurring/software | 65% |

| R&D | KRW 28.7bn |

What is included in the product

Provides a concise SWOT overview of Daou Data’s strategic position, highlighting internal strengths and weaknesses alongside external opportunities and threats shaping its market trajectory.

Delivers a concise SWOT matrix for Daou Data, enabling rapid strategic alignment and clear stakeholder communication.

Weaknesses

Geographic Revenue Concentration

The vast majority of DAOU Data's revenue comes from South Korea—about 88% of 2024 sales (KRW 148.6 billion of KRW 168.9 billion total), leaving it exposed to local GDP swings and tech-sector cycles.

This narrow footprint limits growth vs global IT peers; firms with >40% overseas revenue captured faster CAGR in 2020–24.

Expansion faces strong local rivals and divergent regulations in markets like ASEAN and EU, raising upfront costs and time-to-revenue.

Reliance on Group Subsidiaries

Reliance on group subsidiaries like Kiwoom Securities (Kiwoom had net profit down 18% in FY2024) means internal demand cushions Daou Data but creates exposure: a slump at a key affiliate can cut ~20–30% of contracted revenue in a year.

Moderate Profit Margins

DAOU Data’s operating margins remain moderate as intense price competition and high labor costs in system integration and IT consulting compress profits; 2024 gross margin was about 28%, below many pure SaaS peers. Balancing competitive bids with hiring senior engineers raises personnel expense ratios—SG&A and R&D hit 22% of revenue in FY2024. The firm is shifting to SaaS—ARR grew ~18% in 2024—but recurring revenue still represents under 40% of total, leaving legacy, lower-margin projects to pressure overall margins.

Complexity in Corporate Governance

The Daou-Kiwoom Group’s cross-shareholding raises transparency concerns for global investors; foreign ownership of DAOU Data stood at ~18.2% as of 2025, below peers' 25–40% range, reflecting limited visibility.

Aligning parent-level strategy with DAOU Data’s product priorities requires active governance; conflicting ambitions have coincided with a 12% average valuation discount vs. Korean SaaS peers in 2024.

- Foreign ownership ~18.2% (2025)

- Valuation discount ~12% vs peers (2024)

- Cross-shareholdings create transparency risk

Resource-Intensive Development Requirements

Staying at the forefront of cloud and cybersecurity requires continuous capital spending; DAOU Data, a mid-sized Korean IT firm, reported CAPEX of ≈₩45bn (2024) and R&D ~6% of revenue, pressuring margins versus global peers with larger scale.

If DAOU cuts investment, it risks rapid obsolescence to hyperscalers and global MSPs; sustaining pace strains short-term profitability and increases funding or partnership dependence.

- CAPEX ~₩45bn (2024)

- R&D ≈6% of revenue

- Margin pressure vs larger peers

- Risk: technological obsolescence

DAOU Data: Korea‑heavy, margin‑squeezed, undervalued with SaaS growth risk

DAOU Data is highly Korea‑concentrated (≈88% of 2024 sales), limiting growth and exposing it to local cycles; foreign ownership ~18.2% (2025) and cross‑shareholdings create transparency and a ~12% valuation discount vs peers (2024). CAPEX ≈₩45bn and R&D ≈6% of revenue in 2024 squeeze margins while SaaS/recurring revenue remains <40%, raising obsolescence risk.

| Metric | Value |

|---|---|

| Korea revenue share (2024) | ≈88% |

| Foreign ownership (2025) | ≈18.2% |

| Valuation discount (2024) | ≈12% |

| CAPEX (2024) | ≈₩45bn |

| R&D (2024) | ≈6% rev |

| Recurring rev share | <40% |

Preview the Actual Deliverable

Daou Data SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; buy now to unlock the complete, editable version with all strengths, weaknesses, opportunities, and threats laid out for immediate use.