Dassault Aviation PESTLE Analysis

Your Competitive Advantage Starts with This Report

Navigate the external forces shaping Dassault Aviation—from defense procurement politics and supply-chain inflation to rapid aerospace tech shifts and tightening environmental regulations—and turn those insights into strategic advantage; purchase the full PESTLE to access a ready-to-use, deep-dive report that accelerates decision-making and investment confidence.

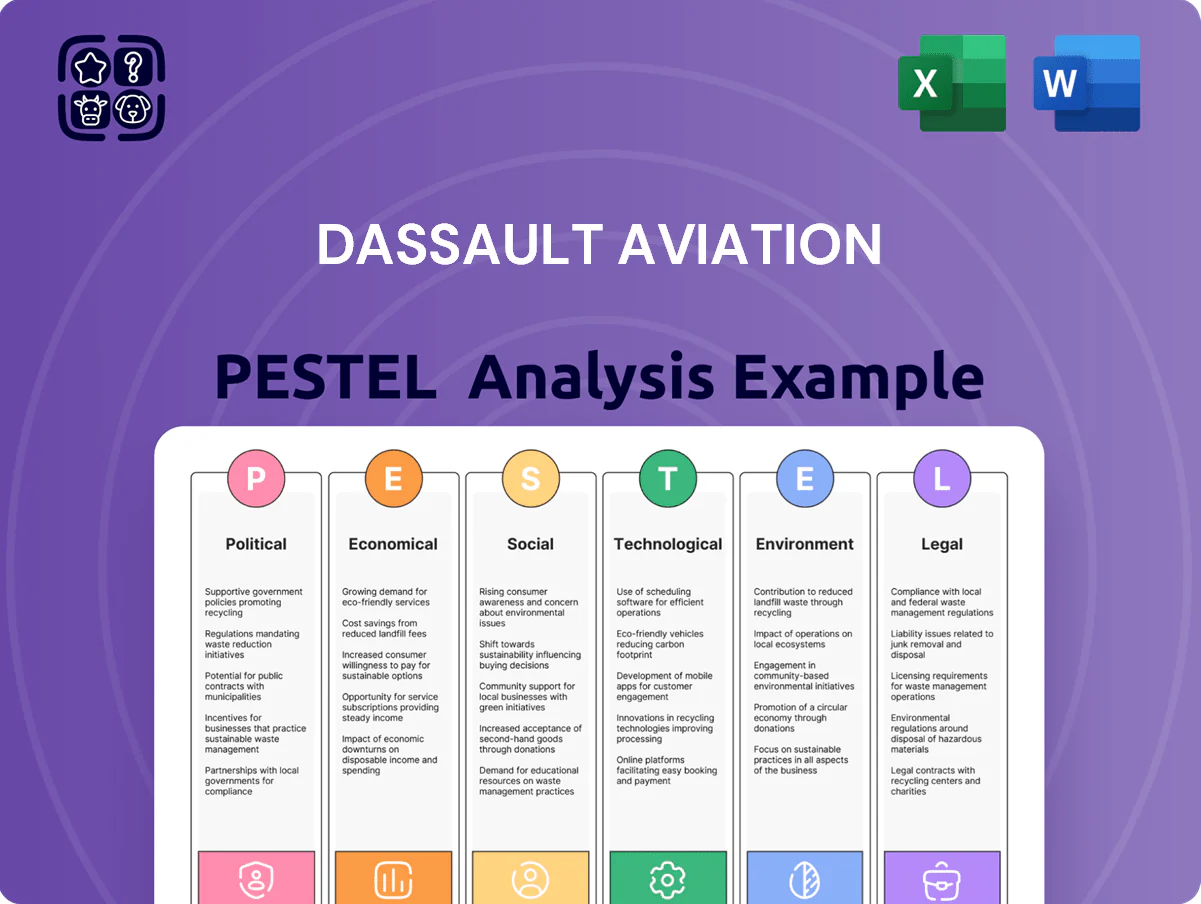

Political factors

European strategic autonomy

The French government’s push for European defense sovereignty positions Dassault Aviation as a cornerstone of regional military independence, underpinning a €65bn planned EU defense procurement pipeline through 2027 that favors domestic primes.

As of late 2025, emphasis on ITAR-free technologies remains a critical driver; EU funding and export rules aim to reduce US-controlled components, protecting deployment autonomy and program timelines for Rafale and New Generation Fighter projects.

Political alignment secures multi-year French orders—France committed €46bn to defense in 2024–2025 defense budgets—locking long-term domestic contracts and reinforcing Dassault’s strategic role in Europe’s defense industrial base.

Rafale export diplomacy

The French state remains deeply engaged in Rafale export diplomacy, securing government-to-government deals across the Middle East, Asia and Eastern Europe that embed strategic partnerships beyond hardware procurement. These agreements include offsets, training and joint maintenance, translating into geopolitical commitments and lifecycle revenues for Dassault. By end-2025 a record order backlog of about €45 billion underpins production stability through the 2030s, supporting multi-year revenue visibility and supply-chain planning.

FCAS program collaboration

The Future Combat Air System remains a complex political endeavor between France, Germany and Spain, with Dassault leading the New Generation Fighter pillar and vying for a €65–€80 billion program share as negotiations on workshare and leadership affect schedules and 2024–25 funding allocations.

French government shareholding

The French state holds a significant stake in Dassault Aviation and is the primary domestic customer, with French defence procurement accounting for roughly 35–45% of company revenues in recent years (2023–2025), offering a stabilizing safety net during downturns.

State shareholding and close alignment with the Dassault family secure long-term strategic direction but expose the company to shifts in national defense budgets and industrial policy decisions.

- State stake and main customer: stabilizes revenue (≈35–45% of sales, 2023–2025)

- Provides downside protection in downturns

- Exposes company to policy/budget shifts

- Dassault family–state alignment reinforces strategic continuity

Global geopolitical instability

Rising geopolitical instability has pushed NATO and allied defense budgets up—NATO members’ collective defense spending grew 5.9% in 2024 and reached over $1.3 trillion, with many nations accelerating procurements through 2025.

Governments favor proven multirole fighters to modernize air forces, benefiting Dassault’s Rafale program and export prospects as countries prioritize quick capability upgrades amid evolving threats.

- 2024 NATO defense spend +5.9%, >$1.3T

- Surge in multirole fighter procurement through 2025

- Favorable political climate for Dassault military sales

France boosts defense: €46bn budgets, €45bn Dassault backlog, EU €65bn pipeline

French state support, €46bn 2024–25 defense budgets, ~35–45% revenue from domestic procurement (2023–25), €45bn backlog end‑2025, EU €65bn defense pipeline to 2027, Rafale exports bolstered by G2G deals; NGF FCAS share contested (€65–80bn program) amid ITAR-free push and NATO spend rise (2024 +5.9% to >$1.3T).

| Metric | Value |

|---|---|

| France defense budget (2024–25) | €46bn |

| Dassault backlog (end‑2025) | €45bn |

| Domestic revenue share (2023–25) | 35–45% |

| EU defense pipeline | €65bn to 2027 |

| NATO spend 2024 | +5.9% to >$1.3T |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Dassault Aviation, with data-driven subpoints and trend analysis tailored to defense and business aviation markets.

A concise PESTLE summary of Dassault Aviation that highlights regulatory, technological, economic, environmental, social, and geopolitical factors for quick reference in meetings or presentations.

Economic factors

Global defense budget expansion

Rising national security concerns drove global defense spending to an estimated USD 2.24 trillion in 2024, up ~3.5% year-on-year, with key Dassault markets (France, India, UAE) raising budgets through 2025, securing multi-year Rafale orders and follow-on MRO contracts.

Business jet market resilience

Demand for Dassaults Falcon business jets stayed strong through 2025, with orders from ultra-high-net-worth individuals and corporations supporting a ~6% CAGR in deliveries for the premium segment since 2021, per industry reports.

Despite GDP volatility—IMF noting global growth of 3.0% in 2024—the premium business aviation market maintained resilience, with fractional and charter utilization up ~8% YoY by 2025.

Launch of the Falcon 10X drove market-share gains in the ultra-long-range class, contributing to Dassaults high-margin backlog expansion; Dassault reported a notable increase in high-value contracts, helping elevate EBIT margins in 2024–25.

Currency exchange volatility

As a French exporter, Dassault Aviation remains highly exposed to EUR/USD volatility; in 2024-25 the euro swung roughly 8% against the dollar, directly affecting USD-priced Falcon sales while many costs stay in euros. Aircraft contracts and long lead times mean exchange moves can swing margins by several percentage points, prompting reported use of forward contracts and options. By late 2025 Dassault continued deploying multi-year hedges covering a substantial portion of anticipated USD revenues to stabilize EBIT.

Supply chain inflation

Supply chain inflation has pushed aerospace input costs up: nickel, titanium and aluminum rose 12–18% year-over-year in 2024 and energy costs added ~4% to manufacturing overheads.

Dassault mitigated margins pressure by streamlining production, reducing unit assembly time and renegotiating supplier terms—reporting in 2024 a targeted cost-savings program contributing ~€120m in run-rate savings.

Maintaining supply-chain stability remains critical to meet Rafale and Falcon delivery schedules amid component lead-time volatility and a 2023–24 average supplier lead-time increase of ~20%.

- Raw material inflation: +12–18% (2024)

- Energy impact: +4% manufacturing overheads (2024)

- Cost-savings program: ~€120m run-rate (2024)

- Supplier lead-times: +20% (2023–24)

Financing and interest rates

As of late 2025, global policy rates average near 4.5% in advanced economies, reducing corporate and private buyer purchasing power and lengthening business-jet replacement cycles; Dassault notes many Falcon buyers use cash or bespoke leasing, mitigating some financing sensitivity.

Dassault tracks rate moves to tweak sales tactics and manage ~18-24 month Falcon inventory lead times, leaning on pre-owned and refurbishment services to smooth demand shifts.

- Avg policy rate ~4.5% (late 2025); higher borrowing costs depress demand

- Falcon buyers show lower reliance on bank loans—more cash/leasing

- Inventory lead times ~18–24 months; pre-owned strategy cushions cycles

Defense boom lifts deliveries and utilization despite inflation, FX swings and higher rates

Defense spending rose to ~USD2.24T (2024) boosting Rafale orders; Falcon deliveries grew ~6% CAGR (2021–25) while premium utilization +8% YoY (2025). EUR/USD swung ~8% (2024–25), hedges cover substantial USD revenues; raw material inflation +12–18% and energy +4% (2024) pressured margins, partly offset by ~€120m cost savings (2024). Policy rates ~4.5% (late‑2025) lengthen purchase cycles; pre‑owned/refurb strategy cushions demand.

| Metric | Value |

|---|---|

| Global defense spend (2024) | USD 2.24T |

| Falcon delivery CAGR (2021–25) | ~6% |

| Utilization change (2025 YoY) | +8% |

| EUR/USD swing (2024–25) | ~8% |

| Raw material inflation (2024) | +12–18% |

| Energy impact (2024) | +4% |

| Cost‑savings program (2024) | ~€120m |

| Avg policy rate (late‑2025) | ~4.5% |

Preview the Actual Deliverable

Dassault Aviation PESTLE Analysis

The preview shown here is the exact Dassault Aviation PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and insights visible in the preview are identical to the downloadable final file delivered immediately after payment.

What you see is what you’ll own—comprehensive PESTLE findings tailored for decision-makers and analysts.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Navigate the external forces shaping Dassault Aviation—from defense procurement politics and supply-chain inflation to rapid aerospace tech shifts and tightening environmental regulations—and turn those insights into strategic advantage; purchase the full PESTLE to access a ready-to-use, deep-dive report that accelerates decision-making and investment confidence.

Political factors

European strategic autonomy

The French government’s push for European defense sovereignty positions Dassault Aviation as a cornerstone of regional military independence, underpinning a €65bn planned EU defense procurement pipeline through 2027 that favors domestic primes.

As of late 2025, emphasis on ITAR-free technologies remains a critical driver; EU funding and export rules aim to reduce US-controlled components, protecting deployment autonomy and program timelines for Rafale and New Generation Fighter projects.

Political alignment secures multi-year French orders—France committed €46bn to defense in 2024–2025 defense budgets—locking long-term domestic contracts and reinforcing Dassault’s strategic role in Europe’s defense industrial base.

Rafale export diplomacy

The French state remains deeply engaged in Rafale export diplomacy, securing government-to-government deals across the Middle East, Asia and Eastern Europe that embed strategic partnerships beyond hardware procurement. These agreements include offsets, training and joint maintenance, translating into geopolitical commitments and lifecycle revenues for Dassault. By end-2025 a record order backlog of about €45 billion underpins production stability through the 2030s, supporting multi-year revenue visibility and supply-chain planning.

FCAS program collaboration

The Future Combat Air System remains a complex political endeavor between France, Germany and Spain, with Dassault leading the New Generation Fighter pillar and vying for a €65–€80 billion program share as negotiations on workshare and leadership affect schedules and 2024–25 funding allocations.

French government shareholding

The French state holds a significant stake in Dassault Aviation and is the primary domestic customer, with French defence procurement accounting for roughly 35–45% of company revenues in recent years (2023–2025), offering a stabilizing safety net during downturns.

State shareholding and close alignment with the Dassault family secure long-term strategic direction but expose the company to shifts in national defense budgets and industrial policy decisions.

- State stake and main customer: stabilizes revenue (≈35–45% of sales, 2023–2025)

- Provides downside protection in downturns

- Exposes company to policy/budget shifts

- Dassault family–state alignment reinforces strategic continuity

Global geopolitical instability

Rising geopolitical instability has pushed NATO and allied defense budgets up—NATO members’ collective defense spending grew 5.9% in 2024 and reached over $1.3 trillion, with many nations accelerating procurements through 2025.

Governments favor proven multirole fighters to modernize air forces, benefiting Dassault’s Rafale program and export prospects as countries prioritize quick capability upgrades amid evolving threats.

- 2024 NATO defense spend +5.9%, >$1.3T

- Surge in multirole fighter procurement through 2025

- Favorable political climate for Dassault military sales

France boosts defense: €46bn budgets, €45bn Dassault backlog, EU €65bn pipeline

French state support, €46bn 2024–25 defense budgets, ~35–45% revenue from domestic procurement (2023–25), €45bn backlog end‑2025, EU €65bn defense pipeline to 2027, Rafale exports bolstered by G2G deals; NGF FCAS share contested (€65–80bn program) amid ITAR-free push and NATO spend rise (2024 +5.9% to >$1.3T).

| Metric | Value |

|---|---|

| France defense budget (2024–25) | €46bn |

| Dassault backlog (end‑2025) | €45bn |

| Domestic revenue share (2023–25) | 35–45% |

| EU defense pipeline | €65bn to 2027 |

| NATO spend 2024 | +5.9% to >$1.3T |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Dassault Aviation, with data-driven subpoints and trend analysis tailored to defense and business aviation markets.

A concise PESTLE summary of Dassault Aviation that highlights regulatory, technological, economic, environmental, social, and geopolitical factors for quick reference in meetings or presentations.

Economic factors

Global defense budget expansion

Rising national security concerns drove global defense spending to an estimated USD 2.24 trillion in 2024, up ~3.5% year-on-year, with key Dassault markets (France, India, UAE) raising budgets through 2025, securing multi-year Rafale orders and follow-on MRO contracts.

Business jet market resilience

Demand for Dassaults Falcon business jets stayed strong through 2025, with orders from ultra-high-net-worth individuals and corporations supporting a ~6% CAGR in deliveries for the premium segment since 2021, per industry reports.

Despite GDP volatility—IMF noting global growth of 3.0% in 2024—the premium business aviation market maintained resilience, with fractional and charter utilization up ~8% YoY by 2025.

Launch of the Falcon 10X drove market-share gains in the ultra-long-range class, contributing to Dassaults high-margin backlog expansion; Dassault reported a notable increase in high-value contracts, helping elevate EBIT margins in 2024–25.

Currency exchange volatility

As a French exporter, Dassault Aviation remains highly exposed to EUR/USD volatility; in 2024-25 the euro swung roughly 8% against the dollar, directly affecting USD-priced Falcon sales while many costs stay in euros. Aircraft contracts and long lead times mean exchange moves can swing margins by several percentage points, prompting reported use of forward contracts and options. By late 2025 Dassault continued deploying multi-year hedges covering a substantial portion of anticipated USD revenues to stabilize EBIT.

Supply chain inflation

Supply chain inflation has pushed aerospace input costs up: nickel, titanium and aluminum rose 12–18% year-over-year in 2024 and energy costs added ~4% to manufacturing overheads.

Dassault mitigated margins pressure by streamlining production, reducing unit assembly time and renegotiating supplier terms—reporting in 2024 a targeted cost-savings program contributing ~€120m in run-rate savings.

Maintaining supply-chain stability remains critical to meet Rafale and Falcon delivery schedules amid component lead-time volatility and a 2023–24 average supplier lead-time increase of ~20%.

- Raw material inflation: +12–18% (2024)

- Energy impact: +4% manufacturing overheads (2024)

- Cost-savings program: ~€120m run-rate (2024)

- Supplier lead-times: +20% (2023–24)

Financing and interest rates

As of late 2025, global policy rates average near 4.5% in advanced economies, reducing corporate and private buyer purchasing power and lengthening business-jet replacement cycles; Dassault notes many Falcon buyers use cash or bespoke leasing, mitigating some financing sensitivity.

Dassault tracks rate moves to tweak sales tactics and manage ~18-24 month Falcon inventory lead times, leaning on pre-owned and refurbishment services to smooth demand shifts.

- Avg policy rate ~4.5% (late 2025); higher borrowing costs depress demand

- Falcon buyers show lower reliance on bank loans—more cash/leasing

- Inventory lead times ~18–24 months; pre-owned strategy cushions cycles

Defense boom lifts deliveries and utilization despite inflation, FX swings and higher rates

Defense spending rose to ~USD2.24T (2024) boosting Rafale orders; Falcon deliveries grew ~6% CAGR (2021–25) while premium utilization +8% YoY (2025). EUR/USD swung ~8% (2024–25), hedges cover substantial USD revenues; raw material inflation +12–18% and energy +4% (2024) pressured margins, partly offset by ~€120m cost savings (2024). Policy rates ~4.5% (late‑2025) lengthen purchase cycles; pre‑owned/refurb strategy cushions demand.

| Metric | Value |

|---|---|

| Global defense spend (2024) | USD 2.24T |

| Falcon delivery CAGR (2021–25) | ~6% |

| Utilization change (2025 YoY) | +8% |

| EUR/USD swing (2024–25) | ~8% |

| Raw material inflation (2024) | +12–18% |

| Energy impact (2024) | +4% |

| Cost‑savings program (2024) | ~€120m |

| Avg policy rate (late‑2025) | ~4.5% |

Preview the Actual Deliverable

Dassault Aviation PESTLE Analysis

The preview shown here is the exact Dassault Aviation PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and insights visible in the preview are identical to the downloadable final file delivered immediately after payment.

What you see is what you’ll own—comprehensive PESTLE findings tailored for decision-makers and analysts.