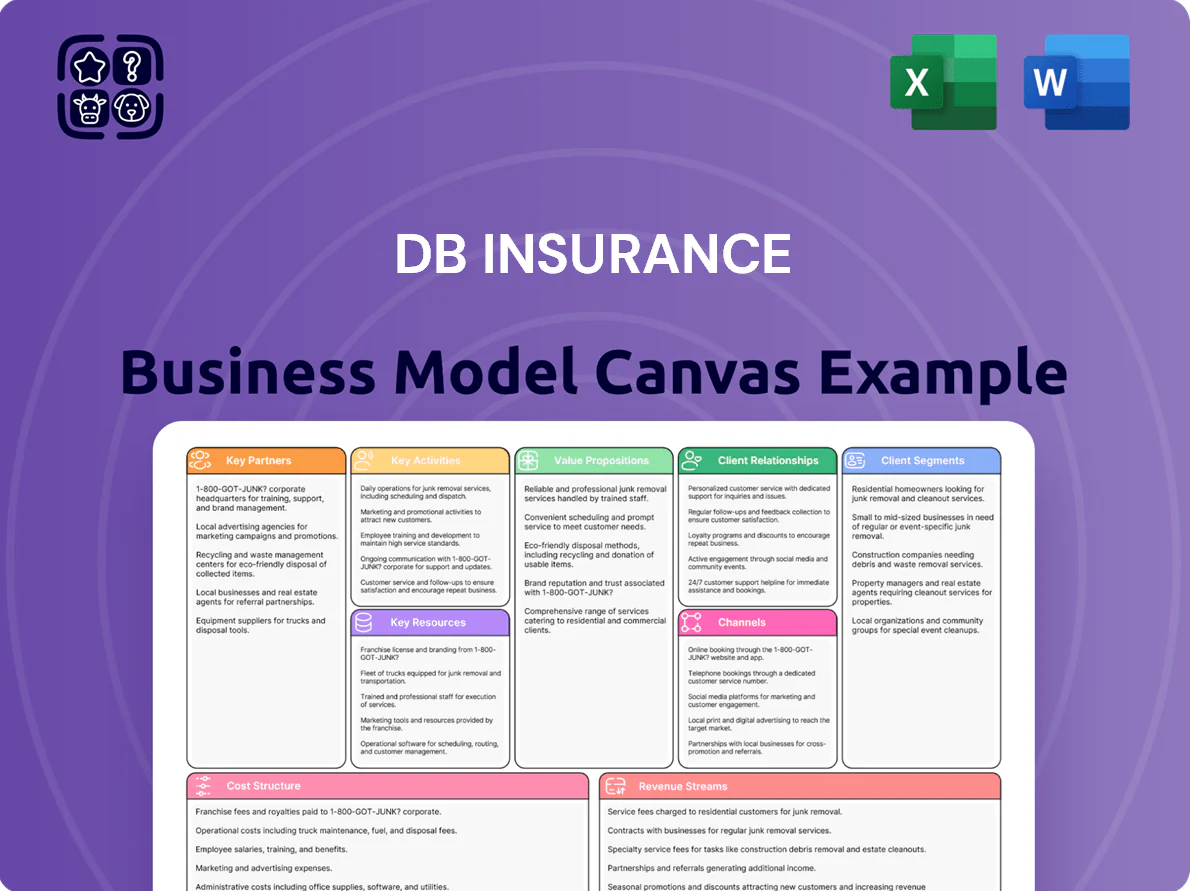

Db Insurance Business Model Canvas

Db Insurance: Ready-to-Use Business Model Canvas for Investors & Strategists

Unlock Db Insurance’s strategic playbook with our concise Business Model Canvas—revealing how it creates customer value, secures partnerships, and monetizes risk across segments; perfect for investors, consultants, and founders seeking actionable, ready-to-use insights. Download the full Word/Excel canvas for a section-by-section breakdown, financial implications, and benchmarking tools to accelerate your strategic planning.

Partnerships

Global Reinsurance Providers

DB Insurance partners with major global reinsurers (Munich Re, Swiss Re, Hannover Re) to cede ~20–30% of catastrophe exposure, supporting a K-ICS solvency buffer that exceeded 170% at YE 2024 and allowing high-limit corporate covers up to $500M while limiting balance-sheet volatility.

Automotive Repair and Service Networks

DB손해보험은 전국 3,200여 개 인증 정비소와 계약해 Promy Car 서비스를 운영, 연간 자동차 보험 수리건의 약 65%를 이 네트워크로 처리해 수리 품질 표준화와 비용 통제를 달성한다. 이 협력망은 평균 클레임 처리시간을 2024년 12.4일에서 2025년 목표 9일로 단축하는 데 기여해 고객만족도(NPS)를 2024년 42에서 2025년 48로 개선하는 핵심 요인이다.

Strategic Fintech and Insurtech Innovators

By end-2025, DB Insurance partnered with ~25 fintech/insurtech startups, deploying AI underwriting that cut quote-to-bind time 40% and blockchain-based data ledgers reducing fraud-related losses 18% (2024 baseline). These integrations enable hyper-personalized premiums and image-recognition claims automation, lowering loss-adjustment expense by ~12% and sharpening competitiveness vs digital-native insurers.

Bancassurance Banking Partners

DB Insurance uses a network of domestic and international banks to sell life and non-life products, tapping banks' retail and corporate client bases to cut customer acquisition costs and secure steady premium flows; in 2024 bancassurance accounted for about 28% of premiums, per company filings.

- Wide bank network: domestic + international

- Primary sales channel to retail/corporate clients

- Reduces acquisition cost, steady premium income

- 2024 bancassurance share ≈ 28% of premiums

Healthcare and Wellness Providers

Db Insurance partners with hospitals and digital health platforms to offer preventive programs and integrate wearable data into underwriting, lowering projected long-term loss ratios by up to 12% based on a 2024 insurer cohort study showing 8–15% claims reduction from prevention.

- Integrates wearables for dynamic pricing

- Rewards healthy behavior, improving retention

- Targets a 10–12% long-term loss-ratio reduction

DB Insurance: Partner-driven model cuts risk, speeds claims, boosts premiums and loss control

DB Insurance leverages global reinsurers (20–30% catastrophe cede), 3,200+ Promy Car repair shops (65% of repairs), ~25 fintech partners (40% faster quote-to-bind, 18% less fraud), bancassurance (28% of premiums 2024), and health/wearable integrations (target 10–12% loss-ratio reduction).

| Partnership | Key metric | 2024/2025 |

|---|---|---|

| Reinsurers | Cat exposure ceded | 20–30% |

| Promy Car network | Repair share | 65% (3,200 shops) |

| Fintech/insurtech | Quote-to-bind / Fraud | -40% / -18% |

| Bancassurance | Premium share | 28% |

| Health/wearables | Target loss-ratio drop | 10–12% |

What is included in the product

A concise, pre-written Business Model Canvas for DB Insurance detailing customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure, and customer relationships aligned with real-world operations and strategic plans.

High-level view of DB Insurance’s business model with editable cells to quickly pinpoint value propositions, customer segments, and cost drivers as a pain-point reliever for strategic clarity.

Activities

Advanced Underwriting and Risk Assessment

Advanced underwriting uses actuarial models plus real-time data and ML to price risk; in 2025 DB Insurance reports ML-driven loss-probability models cut claim prediction error by ~18% and supported a combined ratio near 94% (FY2024: 96%), keeping premiums competitive across auto, property, and commercial lines.

Efficient Claims Management and Settlement

DB Insurance processes claims end-to-end—reporting via mobile app, AI bots fast-track ~45% of simple claims, while specialists handle complex casualty and marine cases, cutting average settlement time to 6.2 days in 2024 versus 9.8 days in 2020. This efficient, transparent workflow drives retention (policy renewal rate 78% in 2024) and bolsters brand trust in non-life lines.

Continuous Product Innovation and Development

Db Insurance continuously designs products for cyber risk, climate and sharing-economy exposures; in 2024 the team launched 6 niche products (including EV and pet covers) after analyzing a 22% rise in cyber claims and 14% premium growth in specialty lines.

Strategic Asset and Investment Management

DB Insurance manages KRW 53.2 trillion of invested assets (2024) to turn premiums into income, allocating across domestic and global fixed income, equities, real estate, and infrastructure to secure long-term policy reserves and boost shareholder returns.

Here’s the quick math: target portfolio aims ~60% bonds, ~20% equities, ~15% real estate/infrastructure, seeking 4–6% risk-adjusted yield to cover liabilities and surplus growth.

- KRW 53.2T invested assets (2024)

- Allocation: ~60% fixed income

- ~20% equities, ~15% real estate/infrastructure

- Target yield 4–6% to match liabilities

Digital Marketing and Multi-Channel Sales

DB Insurance runs aggressive omnichannel marketing, spending about KRW 120 billion in 2024 to support 25,000 exclusive agents while expanding direct digital sales (online premiums rose 18% in 2024 to KRW 340 billion). Campaigns use behavioral analytics to target cohorts with personalized offers, lifting conversion rates ~12% vs 7% for non-personalized channels.

- KRW 120B 2024 marketing spend

- 25,000 exclusive agents

- Online premiums KRW 340B (+18% YoY)

- Personalized conversion ~12% vs 7%

DB Insurance boosts efficiency: ML-driven claims, 94% combined ratio, KRW 340B online

Advanced underwriting and ML cut claim-prediction error ~18%, supporting a combined ratio near 94% (FY2024); claims automation settles simple claims in ~6.2 days, lifting renewal to 78% in 2024. DB Insurance manages KRW 53.2T assets (60% bonds/20% equities/15% real estate) targeting 4–6% yield; marketing spend KRW 120B, online premiums KRW 340B (+18%).

| Metric | 2024 |

|---|---|

| Invested assets | KRW 53.2T |

| Combined ratio | ~94% |

| Policy renewal rate | 78% |

| Avg settlement time | 6.2 days |

| Marketing spend | KRW 120B |

| Online premiums | KRW 340B (+18%) |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Db Insurance Business Model Canvas—not a mockup or sample—and reflects the exact content and layout you will receive after purchase.

When you complete your order, you'll get this same professional, ready-to-edit file in full, formatted for immediate use in Word and Excel with no changes or omissions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Db Insurance: Ready-to-Use Business Model Canvas for Investors & Strategists

Unlock Db Insurance’s strategic playbook with our concise Business Model Canvas—revealing how it creates customer value, secures partnerships, and monetizes risk across segments; perfect for investors, consultants, and founders seeking actionable, ready-to-use insights. Download the full Word/Excel canvas for a section-by-section breakdown, financial implications, and benchmarking tools to accelerate your strategic planning.

Partnerships

Global Reinsurance Providers

DB Insurance partners with major global reinsurers (Munich Re, Swiss Re, Hannover Re) to cede ~20–30% of catastrophe exposure, supporting a K-ICS solvency buffer that exceeded 170% at YE 2024 and allowing high-limit corporate covers up to $500M while limiting balance-sheet volatility.

Automotive Repair and Service Networks

DB손해보험은 전국 3,200여 개 인증 정비소와 계약해 Promy Car 서비스를 운영, 연간 자동차 보험 수리건의 약 65%를 이 네트워크로 처리해 수리 품질 표준화와 비용 통제를 달성한다. 이 협력망은 평균 클레임 처리시간을 2024년 12.4일에서 2025년 목표 9일로 단축하는 데 기여해 고객만족도(NPS)를 2024년 42에서 2025년 48로 개선하는 핵심 요인이다.

Strategic Fintech and Insurtech Innovators

By end-2025, DB Insurance partnered with ~25 fintech/insurtech startups, deploying AI underwriting that cut quote-to-bind time 40% and blockchain-based data ledgers reducing fraud-related losses 18% (2024 baseline). These integrations enable hyper-personalized premiums and image-recognition claims automation, lowering loss-adjustment expense by ~12% and sharpening competitiveness vs digital-native insurers.

Bancassurance Banking Partners

DB Insurance uses a network of domestic and international banks to sell life and non-life products, tapping banks' retail and corporate client bases to cut customer acquisition costs and secure steady premium flows; in 2024 bancassurance accounted for about 28% of premiums, per company filings.

- Wide bank network: domestic + international

- Primary sales channel to retail/corporate clients

- Reduces acquisition cost, steady premium income

- 2024 bancassurance share ≈ 28% of premiums

Healthcare and Wellness Providers

Db Insurance partners with hospitals and digital health platforms to offer preventive programs and integrate wearable data into underwriting, lowering projected long-term loss ratios by up to 12% based on a 2024 insurer cohort study showing 8–15% claims reduction from prevention.

- Integrates wearables for dynamic pricing

- Rewards healthy behavior, improving retention

- Targets a 10–12% long-term loss-ratio reduction

DB Insurance: Partner-driven model cuts risk, speeds claims, boosts premiums and loss control

DB Insurance leverages global reinsurers (20–30% catastrophe cede), 3,200+ Promy Car repair shops (65% of repairs), ~25 fintech partners (40% faster quote-to-bind, 18% less fraud), bancassurance (28% of premiums 2024), and health/wearable integrations (target 10–12% loss-ratio reduction).

| Partnership | Key metric | 2024/2025 |

|---|---|---|

| Reinsurers | Cat exposure ceded | 20–30% |

| Promy Car network | Repair share | 65% (3,200 shops) |

| Fintech/insurtech | Quote-to-bind / Fraud | -40% / -18% |

| Bancassurance | Premium share | 28% |

| Health/wearables | Target loss-ratio drop | 10–12% |

What is included in the product

A concise, pre-written Business Model Canvas for DB Insurance detailing customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure, and customer relationships aligned with real-world operations and strategic plans.

High-level view of DB Insurance’s business model with editable cells to quickly pinpoint value propositions, customer segments, and cost drivers as a pain-point reliever for strategic clarity.

Activities

Advanced Underwriting and Risk Assessment

Advanced underwriting uses actuarial models plus real-time data and ML to price risk; in 2025 DB Insurance reports ML-driven loss-probability models cut claim prediction error by ~18% and supported a combined ratio near 94% (FY2024: 96%), keeping premiums competitive across auto, property, and commercial lines.

Efficient Claims Management and Settlement

DB Insurance processes claims end-to-end—reporting via mobile app, AI bots fast-track ~45% of simple claims, while specialists handle complex casualty and marine cases, cutting average settlement time to 6.2 days in 2024 versus 9.8 days in 2020. This efficient, transparent workflow drives retention (policy renewal rate 78% in 2024) and bolsters brand trust in non-life lines.

Continuous Product Innovation and Development

Db Insurance continuously designs products for cyber risk, climate and sharing-economy exposures; in 2024 the team launched 6 niche products (including EV and pet covers) after analyzing a 22% rise in cyber claims and 14% premium growth in specialty lines.

Strategic Asset and Investment Management

DB Insurance manages KRW 53.2 trillion of invested assets (2024) to turn premiums into income, allocating across domestic and global fixed income, equities, real estate, and infrastructure to secure long-term policy reserves and boost shareholder returns.

Here’s the quick math: target portfolio aims ~60% bonds, ~20% equities, ~15% real estate/infrastructure, seeking 4–6% risk-adjusted yield to cover liabilities and surplus growth.

- KRW 53.2T invested assets (2024)

- Allocation: ~60% fixed income

- ~20% equities, ~15% real estate/infrastructure

- Target yield 4–6% to match liabilities

Digital Marketing and Multi-Channel Sales

DB Insurance runs aggressive omnichannel marketing, spending about KRW 120 billion in 2024 to support 25,000 exclusive agents while expanding direct digital sales (online premiums rose 18% in 2024 to KRW 340 billion). Campaigns use behavioral analytics to target cohorts with personalized offers, lifting conversion rates ~12% vs 7% for non-personalized channels.

- KRW 120B 2024 marketing spend

- 25,000 exclusive agents

- Online premiums KRW 340B (+18% YoY)

- Personalized conversion ~12% vs 7%

DB Insurance boosts efficiency: ML-driven claims, 94% combined ratio, KRW 340B online

Advanced underwriting and ML cut claim-prediction error ~18%, supporting a combined ratio near 94% (FY2024); claims automation settles simple claims in ~6.2 days, lifting renewal to 78% in 2024. DB Insurance manages KRW 53.2T assets (60% bonds/20% equities/15% real estate) targeting 4–6% yield; marketing spend KRW 120B, online premiums KRW 340B (+18%).

| Metric | 2024 |

|---|---|

| Invested assets | KRW 53.2T |

| Combined ratio | ~94% |

| Policy renewal rate | 78% |

| Avg settlement time | 6.2 days |

| Marketing spend | KRW 120B |

| Online premiums | KRW 340B (+18%) |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Db Insurance Business Model Canvas—not a mockup or sample—and reflects the exact content and layout you will receive after purchase.

When you complete your order, you'll get this same professional, ready-to-edit file in full, formatted for immediate use in Word and Excel with no changes or omissions.