Schenker-Joyau SAS Porter's Five Forces Analysis

From Overview to Strategy Blueprint

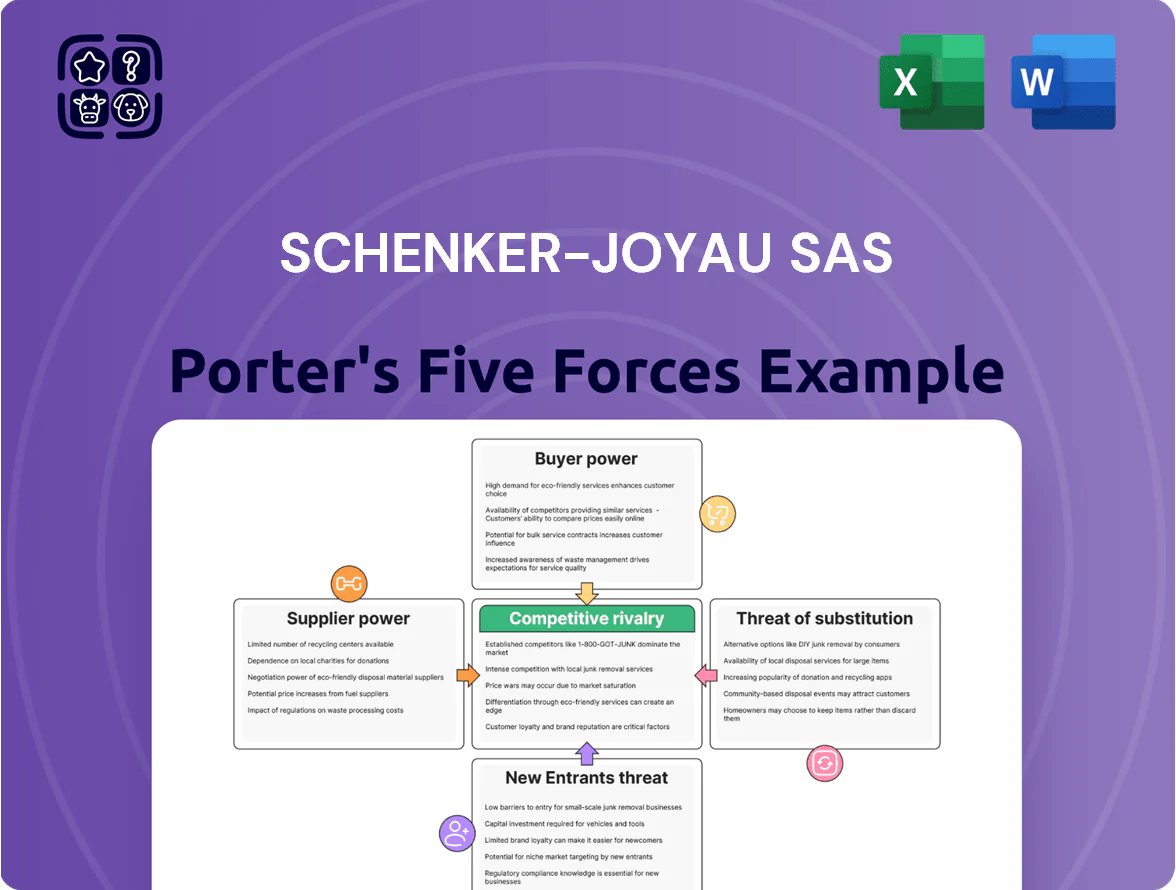

Schenker-Joyau SAS operates in a niche logistics-manufacturing space where supplier concentration and regulatory hurdles raise entry barriers, while customer bargaining power and digital disruption pressure margins—this snapshot highlights strategic tension points and likely profitability constraints.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Schenker-Joyau SAS’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fuel and Energy Provider Influence

Fluctuations in global oil prices—Brent rose ~15% in 2024 to average $86/bbl—directly raise Schenker-Joyau SAS’s road-fleet fuel costs, which make up about 18–22% of operating expenses for French trucking firms.

Fuel is a non-differentiable commodity, so Schenker-Joyau has limited bargaining power versus energy majors and primarily faces market prices.

That dependency increases vulnerability to geopolitical shocks and French carbon taxes; the 2024 CIFER levy hike added roughly €0.03–€0.05/km on heavy trucks.

Vehicle Manufacturers and Fleet Maintenance

The shift to electric and hydrogen heavy-duty trucks raises supplier power: by 2025, only ~10 OEMs and specialist converters supply certified e-trucks and H2 models at scale, concentrating leverage over Schenker-Joyau as it targets 2030 decarbonization.

Long-term maintenance and telematics contracts for high-voltage batteries and fuel-cell systems tie Schenker-Joyau to vendor ecosystems, raising switching costs and risking 5–10% higher TCO if renegotiation occurs.

Labor Market and Unionization in France

The supply of qualified heavy-truck drivers and logistics specialists in France is tight—unemployment in transport was 4.2% in 2024 versus 7.8% national average—giving workers leverage over wages and availability. Strong unions like CFDT and CGT in transport won average pay rises of 5–7% in 2023–24, pressuring operators' margins. Schenker-Joyau must raise driver pay and benefits while improving route productivity to keep costs per ton-km from rising. Retention investments (training, shifts) cut turnover, which averaged 28% in logistics in 2024.

Technology and Software Infrastructure

AI-driven SCM and real-time tracking create reliance on niche vendors; 2025 survey: 62% of logistics firms cite third-party AI providers as critical.

ERP switching costs are high—implementations average €3–7M and 12–18 months for global logistics firms, locking in suppliers.

Proprietary routing and warehouse algorithms give vendors leverage; a 2024 case showed a 4–7% fuel and labor cost reduction tied to one vendor’s model.

- 62% logistics dependence on AI vendors (2025 survey)

- ERP costs €3–7M, 12–18 months

- Vendor algorithms reduced costs 4–7% (2024)

Infrastructure and Real Estate Access

Access to strategic warehouse sites near hubs like Paris-CDG and Marseille is concentrated among a few industrial landlords, tightening supplier power for Schenker-Joyau.

With French logistics vacancy around 3.5% in 2024 and prime rents up ~8% YoY in 2024, landlords can push higher lease rates as e-commerce grows.

Schenker-Joyau’s contract-logistics scale hinges on securing these fixed assets; limited supply raises switching costs and capital needs.

- 3.5% national logistics vacancy (2024)

- Prime rents +8% YoY (2024)

- High landlord concentration near CDG/Marseille

Suppliers Gain Upper Hand: High Fuel Costs, Few E‑truck OEMs & Tight Logistics

Suppliers exert moderate–high power: fuel market exposure (Brent avg $86/bbl in 2024) and limited e-truck OEMs (~10 by 2025) raise costs and switching barriers; driver shortages (transport unemployment 4.2% in 2024) and landlord concentration (logistics vacancy 3.5%, prime rents +8% YoY 2024) further strengthen suppliers.

| Factor | Key data |

|---|---|

| Brent 2024 | $86/bbl |

| E-truck OEMs 2025 | ~10 |

| Transport unemployment 2024 | 4.2% |

| Logistics vacancy 2024 | 3.5% |

What is included in the product

Tailored Porter's Five Forces analysis for Schenker-Joyau SAS, uncovering competitive intensity, buyer and supplier power, substitute threats, and entry barriers to reveal strategic risks and opportunities for pricing and profitability.

A concise Porter's Five Forces sheet for Schenker-Joyau SAS—quickly highlights competitive threats and bargaining pressures for fast strategic decisions.

Customers Bargaining Power

Concentration of Large Corporate Accounts

Major industrial and retail clients account for roughly 40–55% of Schenker-Joyau SAS France revenue and have the scale to demand volume discounts and service SLAs; they commonly run RFPs and reverse auctions that pit Schenker-Joyau against DHL Global Forwarding and Kuehne+Nagel, driving average contract margin pressure of 150–300 bps. Losing a single top-5 account can cut annual turnover by about 8–12% for the French division.

Low Switching Costs for Standardized Freight

For basic palletized and standard road freight, customers can switch carriers with minimal disruption, and by 2025 digital freight platforms captured ~28% of European spot bookings, letting shippers compare rates in real time and raising price sensitivity; unless Schenker-Joyau SAS adds specialized value-added services (e.g., white-glove handling, integrated customs, or guaranteed lead times), it faces ongoing margin pressure and may need to cut prices to retain price-conscious clients.

Demand for Integrated Supply Chain Solutions

Professional buyers increasingly demand end-to-end visibility and integrated logistics over isolated transport; in 2024 62% of European shippers preferred combined warehousing+transport contracts, raising bargaining power versus single-service carriers. This trend deepens partnerships but lets customers insist on broader SLAs and strict KPIs—Schenker-Joyau faces requests for sub-48h delivery windows and 99.5% inventory accuracy. Missing these targets gives clients legal and commercial grounds to renegotiate rates or switch providers; in 2023 churn linked to SLA breaches rose 18% in logistics accounts.

E-commerce and Retailer Expectations

Retailers in France now demand same-day or next-day delivery—18% of online B2C orders in 2024 used same-day options—letting buyers set strict time slots that squeeze carriers like Schenker-Joyau SAS.

Large clients force adoption of live-tracking (RFID/real-time GPS) and 30% recycled or recyclable packaging; compliance raises operating costs but preserves contracts.

Because retailers own the final consumer link, they capture pricing and service terms, shifting bargaining power away from logistics firms.

- 18% same-day B2C orders (2024)

- Buyers demand real-time tracking tech

- 30% recycled/recyclable packaging mandates

- Higher ops cost; lower margin pressure on carriers

In-house Logistics Capabilities

Large retailers and manufacturers—like Carrefour (2024 revenues €78.1bn) and Renault Group—can credibly insource logistics if 3PL rates rise, capping Schenker-Joyau SAS pricing power.

Schenker-Joyau must show its scale and expertise beat in-house costs; global 3PL savings of 10–25% vs internal logistics (industry studies 2023–24) are the proof point.

Failing that, clients may pursue private fleets or dedicated DCs, raising churn risk and pressuring margins.

- Clients can insource—limits pricing.

- 3PL must deliver 10–25% cost advantage.

- Large clients (€bn scale) pose biggest threat.

- Continuous performance proof reduces churn.

Customers wield power: top clients, spot platforms and SLAs squeeze 3PL margins

Customers hold high bargaining power: top clients drive 40–55% of France revenue, single top-5 loss cuts turnover 8–12%, and RFPs compress margins ~150–300 bps; 28% of European spot bookings (2025) and 18% same-day B2C (2024) raise price sensitivity; 62% of shippers (2024) prefer integrated warehousing+transport, forcing strict SLAs (sub-48h, 99.5% accuracy) and tech/packaging mandates (30% recycled), so 3PL must prove 10–25% cost advantage.

| Metric | Value |

|---|---|

| Top-client revenue share | 40–55% |

| Top-5 loss impact | −8–12% turnover |

| Margin pressure from RFPs | 150–300 bps |

| European spot via platforms (2025) | 28% |

| Same-day B2C (France, 2024) | 18% |

| Shippers preferring integrated contracts (2024) | 62% |

| Packaging mandate | 30% recycled |

| Needed 3PL cost advantage | 10–25% |

Same Document Delivered

Schenker-Joyau SAS Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Schenker-Joyau SAS you’ll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally formatted report and will be available for instant download the moment you buy.

You’re viewing the final deliverable: a ready-to-use analysis that requires no setup or customization.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Schenker-Joyau SAS operates in a niche logistics-manufacturing space where supplier concentration and regulatory hurdles raise entry barriers, while customer bargaining power and digital disruption pressure margins—this snapshot highlights strategic tension points and likely profitability constraints.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Schenker-Joyau SAS’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fuel and Energy Provider Influence

Fluctuations in global oil prices—Brent rose ~15% in 2024 to average $86/bbl—directly raise Schenker-Joyau SAS’s road-fleet fuel costs, which make up about 18–22% of operating expenses for French trucking firms.

Fuel is a non-differentiable commodity, so Schenker-Joyau has limited bargaining power versus energy majors and primarily faces market prices.

That dependency increases vulnerability to geopolitical shocks and French carbon taxes; the 2024 CIFER levy hike added roughly €0.03–€0.05/km on heavy trucks.

Vehicle Manufacturers and Fleet Maintenance

The shift to electric and hydrogen heavy-duty trucks raises supplier power: by 2025, only ~10 OEMs and specialist converters supply certified e-trucks and H2 models at scale, concentrating leverage over Schenker-Joyau as it targets 2030 decarbonization.

Long-term maintenance and telematics contracts for high-voltage batteries and fuel-cell systems tie Schenker-Joyau to vendor ecosystems, raising switching costs and risking 5–10% higher TCO if renegotiation occurs.

Labor Market and Unionization in France

The supply of qualified heavy-truck drivers and logistics specialists in France is tight—unemployment in transport was 4.2% in 2024 versus 7.8% national average—giving workers leverage over wages and availability. Strong unions like CFDT and CGT in transport won average pay rises of 5–7% in 2023–24, pressuring operators' margins. Schenker-Joyau must raise driver pay and benefits while improving route productivity to keep costs per ton-km from rising. Retention investments (training, shifts) cut turnover, which averaged 28% in logistics in 2024.

Technology and Software Infrastructure

AI-driven SCM and real-time tracking create reliance on niche vendors; 2025 survey: 62% of logistics firms cite third-party AI providers as critical.

ERP switching costs are high—implementations average €3–7M and 12–18 months for global logistics firms, locking in suppliers.

Proprietary routing and warehouse algorithms give vendors leverage; a 2024 case showed a 4–7% fuel and labor cost reduction tied to one vendor’s model.

- 62% logistics dependence on AI vendors (2025 survey)

- ERP costs €3–7M, 12–18 months

- Vendor algorithms reduced costs 4–7% (2024)

Infrastructure and Real Estate Access

Access to strategic warehouse sites near hubs like Paris-CDG and Marseille is concentrated among a few industrial landlords, tightening supplier power for Schenker-Joyau.

With French logistics vacancy around 3.5% in 2024 and prime rents up ~8% YoY in 2024, landlords can push higher lease rates as e-commerce grows.

Schenker-Joyau’s contract-logistics scale hinges on securing these fixed assets; limited supply raises switching costs and capital needs.

- 3.5% national logistics vacancy (2024)

- Prime rents +8% YoY (2024)

- High landlord concentration near CDG/Marseille

Suppliers Gain Upper Hand: High Fuel Costs, Few E‑truck OEMs & Tight Logistics

Suppliers exert moderate–high power: fuel market exposure (Brent avg $86/bbl in 2024) and limited e-truck OEMs (~10 by 2025) raise costs and switching barriers; driver shortages (transport unemployment 4.2% in 2024) and landlord concentration (logistics vacancy 3.5%, prime rents +8% YoY 2024) further strengthen suppliers.

| Factor | Key data |

|---|---|

| Brent 2024 | $86/bbl |

| E-truck OEMs 2025 | ~10 |

| Transport unemployment 2024 | 4.2% |

| Logistics vacancy 2024 | 3.5% |

What is included in the product

Tailored Porter's Five Forces analysis for Schenker-Joyau SAS, uncovering competitive intensity, buyer and supplier power, substitute threats, and entry barriers to reveal strategic risks and opportunities for pricing and profitability.

A concise Porter's Five Forces sheet for Schenker-Joyau SAS—quickly highlights competitive threats and bargaining pressures for fast strategic decisions.

Customers Bargaining Power

Concentration of Large Corporate Accounts

Major industrial and retail clients account for roughly 40–55% of Schenker-Joyau SAS France revenue and have the scale to demand volume discounts and service SLAs; they commonly run RFPs and reverse auctions that pit Schenker-Joyau against DHL Global Forwarding and Kuehne+Nagel, driving average contract margin pressure of 150–300 bps. Losing a single top-5 account can cut annual turnover by about 8–12% for the French division.

Low Switching Costs for Standardized Freight

For basic palletized and standard road freight, customers can switch carriers with minimal disruption, and by 2025 digital freight platforms captured ~28% of European spot bookings, letting shippers compare rates in real time and raising price sensitivity; unless Schenker-Joyau SAS adds specialized value-added services (e.g., white-glove handling, integrated customs, or guaranteed lead times), it faces ongoing margin pressure and may need to cut prices to retain price-conscious clients.

Demand for Integrated Supply Chain Solutions

Professional buyers increasingly demand end-to-end visibility and integrated logistics over isolated transport; in 2024 62% of European shippers preferred combined warehousing+transport contracts, raising bargaining power versus single-service carriers. This trend deepens partnerships but lets customers insist on broader SLAs and strict KPIs—Schenker-Joyau faces requests for sub-48h delivery windows and 99.5% inventory accuracy. Missing these targets gives clients legal and commercial grounds to renegotiate rates or switch providers; in 2023 churn linked to SLA breaches rose 18% in logistics accounts.

E-commerce and Retailer Expectations

Retailers in France now demand same-day or next-day delivery—18% of online B2C orders in 2024 used same-day options—letting buyers set strict time slots that squeeze carriers like Schenker-Joyau SAS.

Large clients force adoption of live-tracking (RFID/real-time GPS) and 30% recycled or recyclable packaging; compliance raises operating costs but preserves contracts.

Because retailers own the final consumer link, they capture pricing and service terms, shifting bargaining power away from logistics firms.

- 18% same-day B2C orders (2024)

- Buyers demand real-time tracking tech

- 30% recycled/recyclable packaging mandates

- Higher ops cost; lower margin pressure on carriers

In-house Logistics Capabilities

Large retailers and manufacturers—like Carrefour (2024 revenues €78.1bn) and Renault Group—can credibly insource logistics if 3PL rates rise, capping Schenker-Joyau SAS pricing power.

Schenker-Joyau must show its scale and expertise beat in-house costs; global 3PL savings of 10–25% vs internal logistics (industry studies 2023–24) are the proof point.

Failing that, clients may pursue private fleets or dedicated DCs, raising churn risk and pressuring margins.

- Clients can insource—limits pricing.

- 3PL must deliver 10–25% cost advantage.

- Large clients (€bn scale) pose biggest threat.

- Continuous performance proof reduces churn.

Customers wield power: top clients, spot platforms and SLAs squeeze 3PL margins

Customers hold high bargaining power: top clients drive 40–55% of France revenue, single top-5 loss cuts turnover 8–12%, and RFPs compress margins ~150–300 bps; 28% of European spot bookings (2025) and 18% same-day B2C (2024) raise price sensitivity; 62% of shippers (2024) prefer integrated warehousing+transport, forcing strict SLAs (sub-48h, 99.5% accuracy) and tech/packaging mandates (30% recycled), so 3PL must prove 10–25% cost advantage.

| Metric | Value |

|---|---|

| Top-client revenue share | 40–55% |

| Top-5 loss impact | −8–12% turnover |

| Margin pressure from RFPs | 150–300 bps |

| European spot via platforms (2025) | 28% |

| Same-day B2C (France, 2024) | 18% |

| Shippers preferring integrated contracts (2024) | 62% |

| Packaging mandate | 30% recycled |

| Needed 3PL cost advantage | 10–25% |

Same Document Delivered

Schenker-Joyau SAS Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Schenker-Joyau SAS you’ll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally formatted report and will be available for instant download the moment you buy.

You’re viewing the final deliverable: a ready-to-use analysis that requires no setup or customization.