Public Power PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

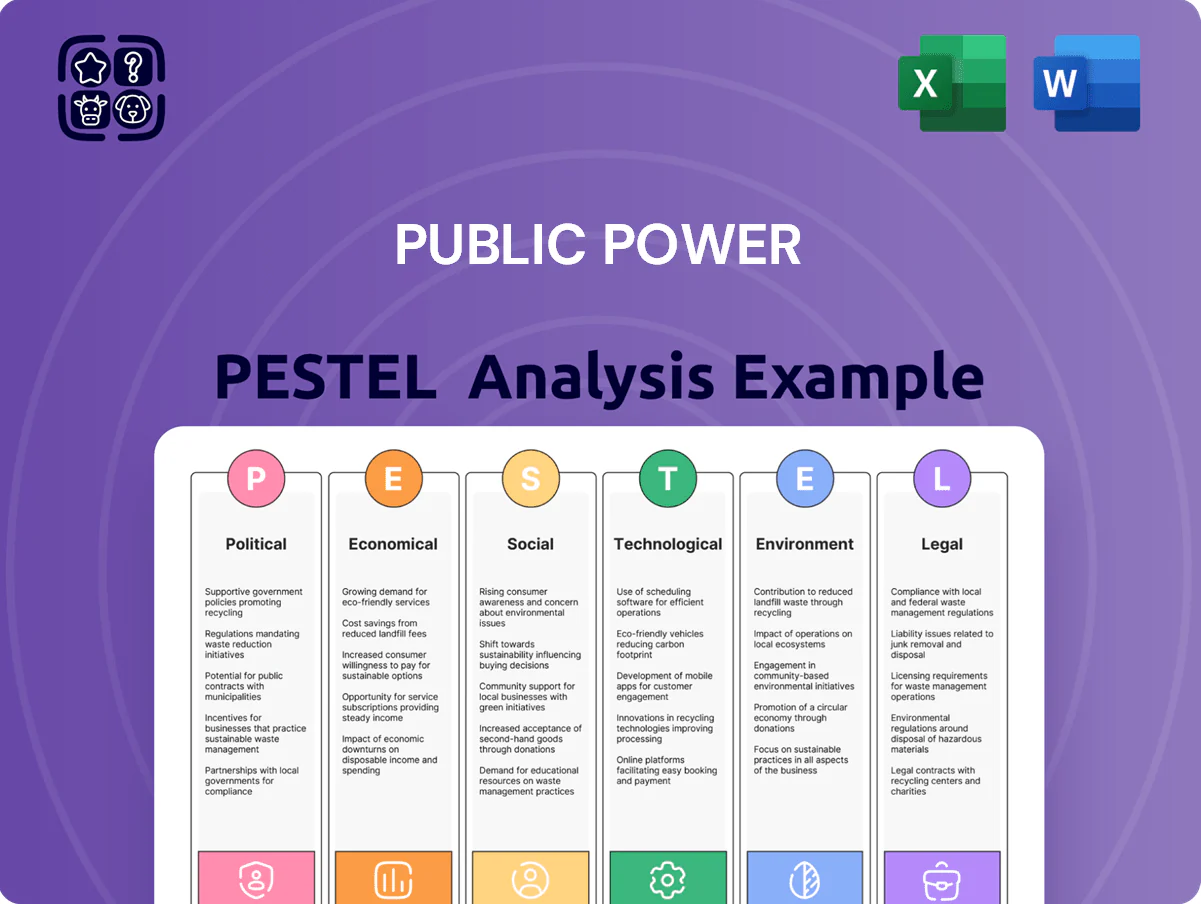

Unlock decisive insights with our PESTLE Analysis of Public Power—explore how political shifts, economic trends, social expectations, technological advances, legal constraints, and environmental pressures shape strategy and risk; buy the full report for a ready-to-use, fully researched brief that accelerates decisions and strengthens investor or board-level presentations.

Political factors

EU Energy Policy Alignment

As of late 2025, PPC must align with the EU REPowerEU and Green Deal, which target a 55% EU-wide emissions cut by 2030 and EUR 300+ billion mobilization for green transition; Greece received EUR 4.9 billion in Recovery funds (2021–2026) tied to energy reforms, making EU compliance essential for PPC to access grants, low-cost finance and market integration.

Geopolitical Stability in the Balkans

PPC’s expansion into Romania and North Macedonia—including the 2023 acquisition of a 60% stake in Romanian grid assets valued at EUR 420m and a 2024 purchase of North Macedonian distribution assets worth EUR 85m—ties its revenue of ~EUR 3.1bn (2024 group) to Balkan stability. Political unrest or government changes could disrupt cross-border corridors that carry ~18% of regional capacity, raising asset risk premiums and potentially lowering international valuations by several percentage points. Diplomatic tensions affecting permits or tariffs would directly impair operational efficiency and raise O&M costs across the regional network.

Government Stake and State Influence

Although PPC was partially privatized, the Greek state holds a strategic minority stake of about 34% as of 2025, so pricing and grid investment decisions are scrutinized for national interest.

State influence means tariffs and CAPEX—PPC’s 2024 CAPEX was €1.2bn—can reflect social policy, balancing profitability with energy poverty relief.

Political shifts in Athens have triggered leadership changes and policy pivots; recent 2023–25 debates increased industrial subsidies by roughly €300m annually.

Energy Security and Diversification

The Greek government, after the 2021–22 energy shock, set a target to cut gas import dependence by 30% by 2025; PPC is accelerating lignite phase-out while expanding renewables to reach 7.5 GW of PPC-owned RES by 2026.

State backing for EastMed and Greece-North Africa interconnectors positions PPC as a regional hub, with planned transmission projects expected to add 2.1 GW of cross-border capacity by 2028.

- Gas import reduction target: −30% by 2025

- PPC RES target: 7.5 GW by 2026

- Cross-border capacity planned: 2.1 GW by 2028

Regulatory Lobbying and Subsidy Frameworks

The political environment determines subsidy availability for green hydrogen and CCS; EU and national funds allocated €15.6bn to hydrogen 2024–27 and CCS pilot grants reached €1.2bn by 2025, affecting project feasibility.

PPC conducts active lobbying with policymakers to influence auction design and capacity remuneration, participating in stakeholder consultations that shaped Greece’s 2024 RES auction rules.

Shifts in political leadership can pause incentive rollout—approval timelines varied from 6 to 18 months across 2022–25, delaying disbursements and project starts.

- €15.6bn EU/national hydrogen funding 2024–27

- €1.2bn CCS pilot grants by 2025

- Lobbying influenced Greece 2024 RES auction rules

- Incentive approval timelines: 6–18 months (2022–25)

State-led PPC pivots to RES, EU H2/CCS funds and regional growth amid tariff politics

Political dynamics shape PPC’s access to EU green funds (Greece Recovery €4.9bn), state influence (34% stake) steers tariffs/CAPEX (€1.2bn 2024) and regional expansion (Romania €420m, N. Macedonia €85m), while targets—gas −30% by 2025, PPC RES 7.5 GW by 2026—and EU hydrogen/CCS funds (€15.6bn; €1.2bn) drive project feasibility.

| Metric | Value |

|---|---|

| State stake | 34% |

| 2024 CAPEX | €1.2bn |

| PPC revenue (2024) | €3.1bn |

| Recovery funds to Greece | €4.9bn |

| H2/CCS funds | €15.6bn/€1.2bn |

What is included in the product

Explores how political, economic, social, technological, environmental, and legal forces uniquely shape Public Power, with each category expanded into data-backed subpoints and region-specific examples to map risks and opportunities for executives and investors.

Condensed Public Power PESTLE insights organized by category for quick reference, ideal for inserting into presentations or sharing across teams to streamline risk discussions and strategic planning.

Economic factors

Inflationary Pressures and Interest Rates

By end-2025, rising cost of capital remains critical for PPC’s capital-intensive wind and solar projects; ECB policy rates averaging around 3.5–4.0% in 2024–25 push borrowing costs higher across Europe.

Higher interest rates raise PPC’s debt-servicing expenses for its multi-billion-euro investment program, squeezing net profit margins if returns fail to outpace financing costs.

PPC must balance aggressive expansion with prudent financial management—aiming to preserve its investment-grade credit metrics amid rate volatility and a leverage-sensitive energy sector.

Energy Market Price Volatility

PPC’s revenue is highly sensitive to wholesale electricity and international natural gas prices; in 2024 TTF averaged about 40 €/MWh vs 100 €/MWh in 2022, causing EBITDA swings for utilities of ±20-30%. Remaining thermal capacity exposes PPC to spot TTF volatility; by end-2025 PPC aims for >40% renewables but still needs active hedging—forward contracts, gas swap coverage and portfolio diversification—to stabilize margins and protect cash flow.

Regional Economic Integration

The acquisition of Enel Romania ties PPC to Balkan GDP dynamics—Romania grew 4.8% in 2023 and Bulgaria 1.5%, while IMF 2024 forecasts average regional growth near 3.2%, boosting industrial/residential electricity demand and supporting PPC revenue upside; conversely, a 1 percentage-point GDP shortfall across the region could reduce electricity consumption by ~0.5–1.0%, delaying grid investments and compressing cash flow for planned capital expenditures.

Carbon Credit Pricing

The EU Allowance (EUA) price averaged about €80–€95/tCO2 in 2024–2025, making carbon costs a material expenditure for PPC’s lignite and gas units and lifting operating margins pressure.

As the EU tightens quotas and the Market Stability Reserve reduces supply, rising EUA prices accelerate PPC’s shift to renewables to avoid escalating market-driven costs.

- 2024–25 EUA ≈ €80–95/tCO2

- Higher EUA → increased OPEX for fossil plants

- Stronger incentive to accelerate renewables

- PPC viability tied to carbon footprint reduction

Consumer Purchasing Power

The economic health of Greek households and businesses directly affects PPC’s collection rates and bad debt provisions; Greek household disposable income fell ~2.1% in 2023 while non-performing loan ratios rose, increasing collection risk.

High inflation (6.5% Greece 2023) and sluggish growth raise unpaid bill risk, prompting PPC to expand flexible payment schemes and social tariffs to mitigate arrears.

PPC’s retail strategy must reflect disposable income variance across Greece and Romania—Romania’s GDP per capita ~US$16,000 (2023) vs Greece ~US$22,500—affecting tariff segmentation and targeted subsidies.

- Greek disposable income -2.1% (2023)

- Greece inflation 6.5% (2023)

- Romania GDP per capita ~US$16,000 (2023)

- Greece GDP per capita ~US$22,500 (2023)

Rising ECB rates, high carbon costs squeeze PPC margins; volatility and weak incomes raise risk

Rising 2024–25 ECB rates (≈3.5–4.0%) and elevated EUA (€80–95/tCO2) inflate PPC’s financing and carbon costs, pressuring margins; TTF volatility (2024 avg ≈€40/MWh) and regional GDP growth (~3.2% IMF 2024) create revenue swings, while Greek disposable income (-2.1% 2023) and high inflation (6.5% 2023) raise collection risk, necessitating hedging and targeted retail measures.

| Metric | Value |

|---|---|

| ECB rate 2024–25 | 3.5–4.0% |

| EUA 2024–25 | €80–95/tCO2 |

| TTF 2024 avg | €40/MWh |

| Greece inflation 2023 | 6.5% |

| Greek disp. income 2023 | -2.1% |

| Regional GDP 2024 (IMF) | ≈3.2% |

What You See Is What You Get

Public Power PESTLE Analysis

The preview shown here is the exact Public Power PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock decisive insights with our PESTLE Analysis of Public Power—explore how political shifts, economic trends, social expectations, technological advances, legal constraints, and environmental pressures shape strategy and risk; buy the full report for a ready-to-use, fully researched brief that accelerates decisions and strengthens investor or board-level presentations.

Political factors

EU Energy Policy Alignment

As of late 2025, PPC must align with the EU REPowerEU and Green Deal, which target a 55% EU-wide emissions cut by 2030 and EUR 300+ billion mobilization for green transition; Greece received EUR 4.9 billion in Recovery funds (2021–2026) tied to energy reforms, making EU compliance essential for PPC to access grants, low-cost finance and market integration.

Geopolitical Stability in the Balkans

PPC’s expansion into Romania and North Macedonia—including the 2023 acquisition of a 60% stake in Romanian grid assets valued at EUR 420m and a 2024 purchase of North Macedonian distribution assets worth EUR 85m—ties its revenue of ~EUR 3.1bn (2024 group) to Balkan stability. Political unrest or government changes could disrupt cross-border corridors that carry ~18% of regional capacity, raising asset risk premiums and potentially lowering international valuations by several percentage points. Diplomatic tensions affecting permits or tariffs would directly impair operational efficiency and raise O&M costs across the regional network.

Government Stake and State Influence

Although PPC was partially privatized, the Greek state holds a strategic minority stake of about 34% as of 2025, so pricing and grid investment decisions are scrutinized for national interest.

State influence means tariffs and CAPEX—PPC’s 2024 CAPEX was €1.2bn—can reflect social policy, balancing profitability with energy poverty relief.

Political shifts in Athens have triggered leadership changes and policy pivots; recent 2023–25 debates increased industrial subsidies by roughly €300m annually.

Energy Security and Diversification

The Greek government, after the 2021–22 energy shock, set a target to cut gas import dependence by 30% by 2025; PPC is accelerating lignite phase-out while expanding renewables to reach 7.5 GW of PPC-owned RES by 2026.

State backing for EastMed and Greece-North Africa interconnectors positions PPC as a regional hub, with planned transmission projects expected to add 2.1 GW of cross-border capacity by 2028.

- Gas import reduction target: −30% by 2025

- PPC RES target: 7.5 GW by 2026

- Cross-border capacity planned: 2.1 GW by 2028

Regulatory Lobbying and Subsidy Frameworks

The political environment determines subsidy availability for green hydrogen and CCS; EU and national funds allocated €15.6bn to hydrogen 2024–27 and CCS pilot grants reached €1.2bn by 2025, affecting project feasibility.

PPC conducts active lobbying with policymakers to influence auction design and capacity remuneration, participating in stakeholder consultations that shaped Greece’s 2024 RES auction rules.

Shifts in political leadership can pause incentive rollout—approval timelines varied from 6 to 18 months across 2022–25, delaying disbursements and project starts.

- €15.6bn EU/national hydrogen funding 2024–27

- €1.2bn CCS pilot grants by 2025

- Lobbying influenced Greece 2024 RES auction rules

- Incentive approval timelines: 6–18 months (2022–25)

State-led PPC pivots to RES, EU H2/CCS funds and regional growth amid tariff politics

Political dynamics shape PPC’s access to EU green funds (Greece Recovery €4.9bn), state influence (34% stake) steers tariffs/CAPEX (€1.2bn 2024) and regional expansion (Romania €420m, N. Macedonia €85m), while targets—gas −30% by 2025, PPC RES 7.5 GW by 2026—and EU hydrogen/CCS funds (€15.6bn; €1.2bn) drive project feasibility.

| Metric | Value |

|---|---|

| State stake | 34% |

| 2024 CAPEX | €1.2bn |

| PPC revenue (2024) | €3.1bn |

| Recovery funds to Greece | €4.9bn |

| H2/CCS funds | €15.6bn/€1.2bn |

What is included in the product

Explores how political, economic, social, technological, environmental, and legal forces uniquely shape Public Power, with each category expanded into data-backed subpoints and region-specific examples to map risks and opportunities for executives and investors.

Condensed Public Power PESTLE insights organized by category for quick reference, ideal for inserting into presentations or sharing across teams to streamline risk discussions and strategic planning.

Economic factors

Inflationary Pressures and Interest Rates

By end-2025, rising cost of capital remains critical for PPC’s capital-intensive wind and solar projects; ECB policy rates averaging around 3.5–4.0% in 2024–25 push borrowing costs higher across Europe.

Higher interest rates raise PPC’s debt-servicing expenses for its multi-billion-euro investment program, squeezing net profit margins if returns fail to outpace financing costs.

PPC must balance aggressive expansion with prudent financial management—aiming to preserve its investment-grade credit metrics amid rate volatility and a leverage-sensitive energy sector.

Energy Market Price Volatility

PPC’s revenue is highly sensitive to wholesale electricity and international natural gas prices; in 2024 TTF averaged about 40 €/MWh vs 100 €/MWh in 2022, causing EBITDA swings for utilities of ±20-30%. Remaining thermal capacity exposes PPC to spot TTF volatility; by end-2025 PPC aims for >40% renewables but still needs active hedging—forward contracts, gas swap coverage and portfolio diversification—to stabilize margins and protect cash flow.

Regional Economic Integration

The acquisition of Enel Romania ties PPC to Balkan GDP dynamics—Romania grew 4.8% in 2023 and Bulgaria 1.5%, while IMF 2024 forecasts average regional growth near 3.2%, boosting industrial/residential electricity demand and supporting PPC revenue upside; conversely, a 1 percentage-point GDP shortfall across the region could reduce electricity consumption by ~0.5–1.0%, delaying grid investments and compressing cash flow for planned capital expenditures.

Carbon Credit Pricing

The EU Allowance (EUA) price averaged about €80–€95/tCO2 in 2024–2025, making carbon costs a material expenditure for PPC’s lignite and gas units and lifting operating margins pressure.

As the EU tightens quotas and the Market Stability Reserve reduces supply, rising EUA prices accelerate PPC’s shift to renewables to avoid escalating market-driven costs.

- 2024–25 EUA ≈ €80–95/tCO2

- Higher EUA → increased OPEX for fossil plants

- Stronger incentive to accelerate renewables

- PPC viability tied to carbon footprint reduction

Consumer Purchasing Power

The economic health of Greek households and businesses directly affects PPC’s collection rates and bad debt provisions; Greek household disposable income fell ~2.1% in 2023 while non-performing loan ratios rose, increasing collection risk.

High inflation (6.5% Greece 2023) and sluggish growth raise unpaid bill risk, prompting PPC to expand flexible payment schemes and social tariffs to mitigate arrears.

PPC’s retail strategy must reflect disposable income variance across Greece and Romania—Romania’s GDP per capita ~US$16,000 (2023) vs Greece ~US$22,500—affecting tariff segmentation and targeted subsidies.

- Greek disposable income -2.1% (2023)

- Greece inflation 6.5% (2023)

- Romania GDP per capita ~US$16,000 (2023)

- Greece GDP per capita ~US$22,500 (2023)

Rising ECB rates, high carbon costs squeeze PPC margins; volatility and weak incomes raise risk

Rising 2024–25 ECB rates (≈3.5–4.0%) and elevated EUA (€80–95/tCO2) inflate PPC’s financing and carbon costs, pressuring margins; TTF volatility (2024 avg ≈€40/MWh) and regional GDP growth (~3.2% IMF 2024) create revenue swings, while Greek disposable income (-2.1% 2023) and high inflation (6.5% 2023) raise collection risk, necessitating hedging and targeted retail measures.

| Metric | Value |

|---|---|

| ECB rate 2024–25 | 3.5–4.0% |

| EUA 2024–25 | €80–95/tCO2 |

| TTF 2024 avg | €40/MWh |

| Greece inflation 2023 | 6.5% |

| Greek disp. income 2023 | -2.1% |

| Regional GDP 2024 (IMF) | ≈3.2% |

What You See Is What You Get

Public Power PESTLE Analysis

The preview shown here is the exact Public Power PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.