De La Rue Boston Consulting Group Matrix

Actionable Strategy Starts Here

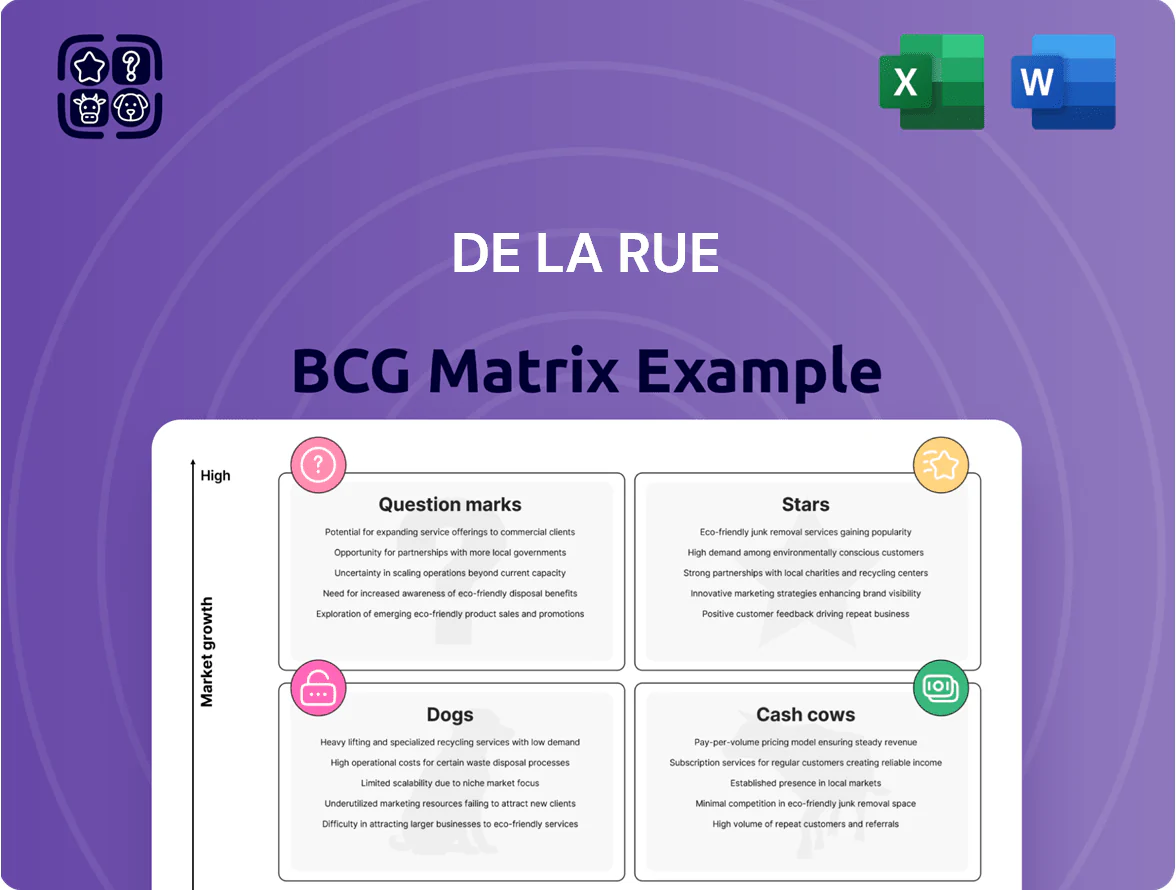

De La Rue’s BCG Matrix preview highlights how its cash-generating currency solutions and niche identity products stack up against growth opportunities and competitive pressures—offering a quick lens on Stars, Cash Cows, Question Marks, and Dogs. This snapshot teases strategic implications, but the full BCG Matrix delivers quadrant-level data, targeted recommendations, and editable Word/Excel files to guide capital allocation and product strategy. Purchase the complete report for a ready-to-use roadmap that turns analysis into actionable decisions.

Stars

SAFEGUARD Polymer Substrate

As of late 2025, SAFEGUARD polymer substrate is a high-growth offering for De La Rue, capturing strong share in a transitioning global currency market where 160+ denominations across 24 countries use polymer banknotes.

The polymer market is growing ~6.7% CAGR and SAFEGUARD drives both volume and margin via De La Rue’s bundled printing-services model, contributing materially to revenue mix.

Ongoing investments in tactile security and recyclability sustain competitive advantage versus peers such as CCL Secure and support higher ASPs and margins.

Advanced Banknote Security Features

De La Rue’s portfolio of advanced security features—color-shifting inks and surface-relief micro-structures—sits in the BCG Matrix as Stars: high-growth, high-share products within Currency.

Central banks increasingly mandate these techs to fight sophisticated counterfeiting, driving a robust order book of £347 million by Jan 2025.

They need heavy R&D spend but command premium pricing, so they sustain margins and define De La Rue’s competitive edge in commercial banknotes.

Next-Generation Passport Bio-Data Pages

Following the early-2026 joint venture with Canadian Bank Note Company, De La Rue’s identity document components moved into the Stars quadrant, driven by a targeted push for the £360m British passport tender and global contracts; revenue upside is clear as the unit pursues polycarbonate data-page tech amid a 2024–25 12% annual travel rebound.

Scaling manufacturing eats cash—capex ~£25–40m over 2026–27—but under Atlas Holdings’ private ownership the unit’s addressable market is pegged at ~£1.2bn by 2028, signalling strong long-term growth.

Cash Cycle Analytics Software

De La Rue’s Cash Cycle Analytics software is a high-growth digital offering that uses SaaS to give central banks data on banknote durability and circulation, tapping a niche expanding ~12–18% annually as cash-management digitization rises; it currently has smaller revenue share versus printing but higher ARR growth.

Promote integration with physical currency products and scale SaaS adoption to convert this star into a future cash cow; estimate: software ARR could double by 2028 from a 2025 base of ~£8–12m if retention stays >90%.

- High growth: ~12–18% CAGR

- 2025 software ARR estimate: £8–12m

- Customer retention target: >90%

- Strategy: bundle SaaS with printing services

Holographic Authentication Labels

Holographic Authentication Labels remain a Star for De La Rue: post-2025 sale the firm kept advanced holography, embedding it in passports and high-end brand protection; global e-commerce fraud rose ~23% YoY to 2024, driving label demand up ~18% in 2024–25.

The tech leads on sophistication, needs ongoing supply-chain placement support across pharma and luxury, and leverages De La Rue’s 200-year heritage to meet digital-physical hybrid security needs.

- High growth: ~18% CAGR 2022–25

- E‑com fraud ↑23% YoY to 2024

- Used in passports, pharma, luxury

- Requires supply-chain integration support

High‑growth polymer, holography & SaaS: £347m book, £360m passport upside

Stars: polymer banknotes, advanced security features, ID components, SaaS and holography show high share and high growth; order book £347m (Jan 2025), passport opportunity c.£360m, polymer market ~6.7% CAGR, SaaS ARR £8–12m (2025) with 12–18% CAGR, holography ~18% CAGR (2022–25); capex £25–40m (2026–27).

| Product | 2025 metric | Growth | Notes |

|---|---|---|---|

| Polymer | Order book £347m | 6.7% CAGR | 160+ denominations, 24 countries |

| ID components | Passport bid £360m | — | JV early‑2026, addressable £1.2bn by 2028 |

| SaaS | ARR £8–12m | 12–18% CAGR | Retention >90% target |

| Holography | — | ~18% CAGR | E‑com fraud ↑23% YoY to 2024 |

What is included in the product

BCG Matrix analysis of De La Rue’s portfolio: identifies Stars, Cash Cows, Question Marks, Dogs with investment, hold, or divest guidance.

One-page De La Rue BCG Matrix placing each business unit in a quadrant for fast strategic clarity

Cash Cows

Finished Banknote Printing

The Finished Banknote Printing unit is a classic cash cow: De La Rue serves over 50% of global issuing authorities and holds a multi‑hundred million pound contracted order book into 2026, delivering steady EBITDA that funds debt service and R&D.

Paper banknote growth is low versus polymer, but high market share and legacy infrastructure support gross margins above 25% and operational improvements under private equity are being used to maximize free cash flow.

Government Revenue Solutions (Tax Stamps)

Tax stamps for tobacco and alcohol are a mature market where De La Rue held roughly 40–50% share across key jurisdictions in 2025, giving a dominant, stable position and predictable annuity-like revenue.

These contracts need little extra marketing or capex, and high government procurement barriers keep share stable despite single-digit market growth; cashflows helped shore up the balance sheet in the 2025 restructuring, contributing an estimated £60–80m annual EBITDA.

Legacy Identity Document Issuance

De La Rue’s legacy identity-document issuance—national IDs and driving licences in ~140 countries—generates steady revenue (roughly 60–70% gross margin on personalization services) and low marketing spend since systems are embedded in government infrastructure.

These long-term contracts produce predictable cash flow; maintaining service levels and uptime (>99.5%) keeps customers sticky and reduces churn.

Stable earnings let De La Rue reinvest operational gains into higher-risk, high-growth partnerships and question-mark projects without stressing liquidity.

Security Thread Production

Security thread production is a mature, high-market-share cash cow in De La Rue’s Currency division, supporting ~60–70% of paper-note security features by volume in 2024 and leveraging company-wide scale to lower unit costs.

Market growth for basic threads is low (<2% CAGR 2024–27), but high production efficiency yields strong free cash flow; operating margins for the unit are estimated ~18–22% in FY2024.

Capital expenditure needs are minimal vs advanced features, letting De La Rue reallocate ~£10–15m annually toward R&D in micro-optics (star) development.

- High share: 60–70% volume support

- Low growth: <2% CAGR 2024–27

- Margins: ~18–22% FY2024

- Capex freed: £10–15m/year to R&D

Banknote Design Services

De La Rue’s banknote design services are a cash cow: market-leading, high-margin work sold to central banks and often winning printing contracts; design contributed an estimated 12–15% of group revenue in 2024 with >30% operating margin.

The segment is mature—low growth in new banknote series—but De La Rue’s 200-year reputation and ~40% share of commercial design keep steady demand and pricing power.

Design relies on skilled human capital not heavy capex, so cash conversion is strong (2024 operating cash conversion ~85%), making it a reliable profit engine.

- High margin: ~30% op margin (2024)

- Revenue share: 12–15% (2024)

- Market share: ~40% in commercial design

- Cash conversion: ~85% (2024)

De La Rue’s high‑margin, annuity cash cows: predictable £60–80m EBITDA & multi‑hundred £m orders

De La Rue’s cash cows—finished banknote printing, tax stamps, identity personalization, security threads, and design—produce predictable annuity revenue (multi‑hundred £m order book into 2026), high margins (paper printing & design ~25–30%+, threads ~18–22%), and freed capex (£10–15m/yr) that funded the 2025 restructuring and delivered estimated £60–80m annual EBITDA.

| Unit | Share | Margin | Growth | FY/Year |

|---|---|---|---|---|

| Banknote printing | >50% issuing authorities | ~25–30% | low | 2024–25 |

| Tax stamps | 40–50% | ~20%? | mature | 2025 |

| Identity | ~140 countries | 60–70% gross | stable | 2024–25 |

| Security threads | 60–70% vol | 18–22% | <2% CAGR | 2024 |

| Design | ~40% | ~30% op | low | 2024 |

Delivered as Shown

De La Rue BCG Matrix

The file you're previewing on this page is the exact De La Rue BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just the fully formatted, analysis-ready document crafted for strategic clarity and professional presentation.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

De La Rue’s BCG Matrix preview highlights how its cash-generating currency solutions and niche identity products stack up against growth opportunities and competitive pressures—offering a quick lens on Stars, Cash Cows, Question Marks, and Dogs. This snapshot teases strategic implications, but the full BCG Matrix delivers quadrant-level data, targeted recommendations, and editable Word/Excel files to guide capital allocation and product strategy. Purchase the complete report for a ready-to-use roadmap that turns analysis into actionable decisions.

Stars

SAFEGUARD Polymer Substrate

As of late 2025, SAFEGUARD polymer substrate is a high-growth offering for De La Rue, capturing strong share in a transitioning global currency market where 160+ denominations across 24 countries use polymer banknotes.

The polymer market is growing ~6.7% CAGR and SAFEGUARD drives both volume and margin via De La Rue’s bundled printing-services model, contributing materially to revenue mix.

Ongoing investments in tactile security and recyclability sustain competitive advantage versus peers such as CCL Secure and support higher ASPs and margins.

Advanced Banknote Security Features

De La Rue’s portfolio of advanced security features—color-shifting inks and surface-relief micro-structures—sits in the BCG Matrix as Stars: high-growth, high-share products within Currency.

Central banks increasingly mandate these techs to fight sophisticated counterfeiting, driving a robust order book of £347 million by Jan 2025.

They need heavy R&D spend but command premium pricing, so they sustain margins and define De La Rue’s competitive edge in commercial banknotes.

Next-Generation Passport Bio-Data Pages

Following the early-2026 joint venture with Canadian Bank Note Company, De La Rue’s identity document components moved into the Stars quadrant, driven by a targeted push for the £360m British passport tender and global contracts; revenue upside is clear as the unit pursues polycarbonate data-page tech amid a 2024–25 12% annual travel rebound.

Scaling manufacturing eats cash—capex ~£25–40m over 2026–27—but under Atlas Holdings’ private ownership the unit’s addressable market is pegged at ~£1.2bn by 2028, signalling strong long-term growth.

Cash Cycle Analytics Software

De La Rue’s Cash Cycle Analytics software is a high-growth digital offering that uses SaaS to give central banks data on banknote durability and circulation, tapping a niche expanding ~12–18% annually as cash-management digitization rises; it currently has smaller revenue share versus printing but higher ARR growth.

Promote integration with physical currency products and scale SaaS adoption to convert this star into a future cash cow; estimate: software ARR could double by 2028 from a 2025 base of ~£8–12m if retention stays >90%.

- High growth: ~12–18% CAGR

- 2025 software ARR estimate: £8–12m

- Customer retention target: >90%

- Strategy: bundle SaaS with printing services

Holographic Authentication Labels

Holographic Authentication Labels remain a Star for De La Rue: post-2025 sale the firm kept advanced holography, embedding it in passports and high-end brand protection; global e-commerce fraud rose ~23% YoY to 2024, driving label demand up ~18% in 2024–25.

The tech leads on sophistication, needs ongoing supply-chain placement support across pharma and luxury, and leverages De La Rue’s 200-year heritage to meet digital-physical hybrid security needs.

- High growth: ~18% CAGR 2022–25

- E‑com fraud ↑23% YoY to 2024

- Used in passports, pharma, luxury

- Requires supply-chain integration support

High‑growth polymer, holography & SaaS: £347m book, £360m passport upside

Stars: polymer banknotes, advanced security features, ID components, SaaS and holography show high share and high growth; order book £347m (Jan 2025), passport opportunity c.£360m, polymer market ~6.7% CAGR, SaaS ARR £8–12m (2025) with 12–18% CAGR, holography ~18% CAGR (2022–25); capex £25–40m (2026–27).

| Product | 2025 metric | Growth | Notes |

|---|---|---|---|

| Polymer | Order book £347m | 6.7% CAGR | 160+ denominations, 24 countries |

| ID components | Passport bid £360m | — | JV early‑2026, addressable £1.2bn by 2028 |

| SaaS | ARR £8–12m | 12–18% CAGR | Retention >90% target |

| Holography | — | ~18% CAGR | E‑com fraud ↑23% YoY to 2024 |

What is included in the product

BCG Matrix analysis of De La Rue’s portfolio: identifies Stars, Cash Cows, Question Marks, Dogs with investment, hold, or divest guidance.

One-page De La Rue BCG Matrix placing each business unit in a quadrant for fast strategic clarity

Cash Cows

Finished Banknote Printing

The Finished Banknote Printing unit is a classic cash cow: De La Rue serves over 50% of global issuing authorities and holds a multi‑hundred million pound contracted order book into 2026, delivering steady EBITDA that funds debt service and R&D.

Paper banknote growth is low versus polymer, but high market share and legacy infrastructure support gross margins above 25% and operational improvements under private equity are being used to maximize free cash flow.

Government Revenue Solutions (Tax Stamps)

Tax stamps for tobacco and alcohol are a mature market where De La Rue held roughly 40–50% share across key jurisdictions in 2025, giving a dominant, stable position and predictable annuity-like revenue.

These contracts need little extra marketing or capex, and high government procurement barriers keep share stable despite single-digit market growth; cashflows helped shore up the balance sheet in the 2025 restructuring, contributing an estimated £60–80m annual EBITDA.

Legacy Identity Document Issuance

De La Rue’s legacy identity-document issuance—national IDs and driving licences in ~140 countries—generates steady revenue (roughly 60–70% gross margin on personalization services) and low marketing spend since systems are embedded in government infrastructure.

These long-term contracts produce predictable cash flow; maintaining service levels and uptime (>99.5%) keeps customers sticky and reduces churn.

Stable earnings let De La Rue reinvest operational gains into higher-risk, high-growth partnerships and question-mark projects without stressing liquidity.

Security Thread Production

Security thread production is a mature, high-market-share cash cow in De La Rue’s Currency division, supporting ~60–70% of paper-note security features by volume in 2024 and leveraging company-wide scale to lower unit costs.

Market growth for basic threads is low (<2% CAGR 2024–27), but high production efficiency yields strong free cash flow; operating margins for the unit are estimated ~18–22% in FY2024.

Capital expenditure needs are minimal vs advanced features, letting De La Rue reallocate ~£10–15m annually toward R&D in micro-optics (star) development.

- High share: 60–70% volume support

- Low growth: <2% CAGR 2024–27

- Margins: ~18–22% FY2024

- Capex freed: £10–15m/year to R&D

Banknote Design Services

De La Rue’s banknote design services are a cash cow: market-leading, high-margin work sold to central banks and often winning printing contracts; design contributed an estimated 12–15% of group revenue in 2024 with >30% operating margin.

The segment is mature—low growth in new banknote series—but De La Rue’s 200-year reputation and ~40% share of commercial design keep steady demand and pricing power.

Design relies on skilled human capital not heavy capex, so cash conversion is strong (2024 operating cash conversion ~85%), making it a reliable profit engine.

- High margin: ~30% op margin (2024)

- Revenue share: 12–15% (2024)

- Market share: ~40% in commercial design

- Cash conversion: ~85% (2024)

De La Rue’s high‑margin, annuity cash cows: predictable £60–80m EBITDA & multi‑hundred £m orders

De La Rue’s cash cows—finished banknote printing, tax stamps, identity personalization, security threads, and design—produce predictable annuity revenue (multi‑hundred £m order book into 2026), high margins (paper printing & design ~25–30%+, threads ~18–22%), and freed capex (£10–15m/yr) that funded the 2025 restructuring and delivered estimated £60–80m annual EBITDA.

| Unit | Share | Margin | Growth | FY/Year |

|---|---|---|---|---|

| Banknote printing | >50% issuing authorities | ~25–30% | low | 2024–25 |

| Tax stamps | 40–50% | ~20%? | mature | 2025 |

| Identity | ~140 countries | 60–70% gross | stable | 2024–25 |

| Security threads | 60–70% vol | 18–22% | <2% CAGR | 2024 |

| Design | ~40% | ~30% op | low | 2024 |

Delivered as Shown

De La Rue BCG Matrix

The file you're previewing on this page is the exact De La Rue BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just the fully formatted, analysis-ready document crafted for strategic clarity and professional presentation.