Dell Porter's Five Forces Analysis

Don't Miss the Bigger Picture

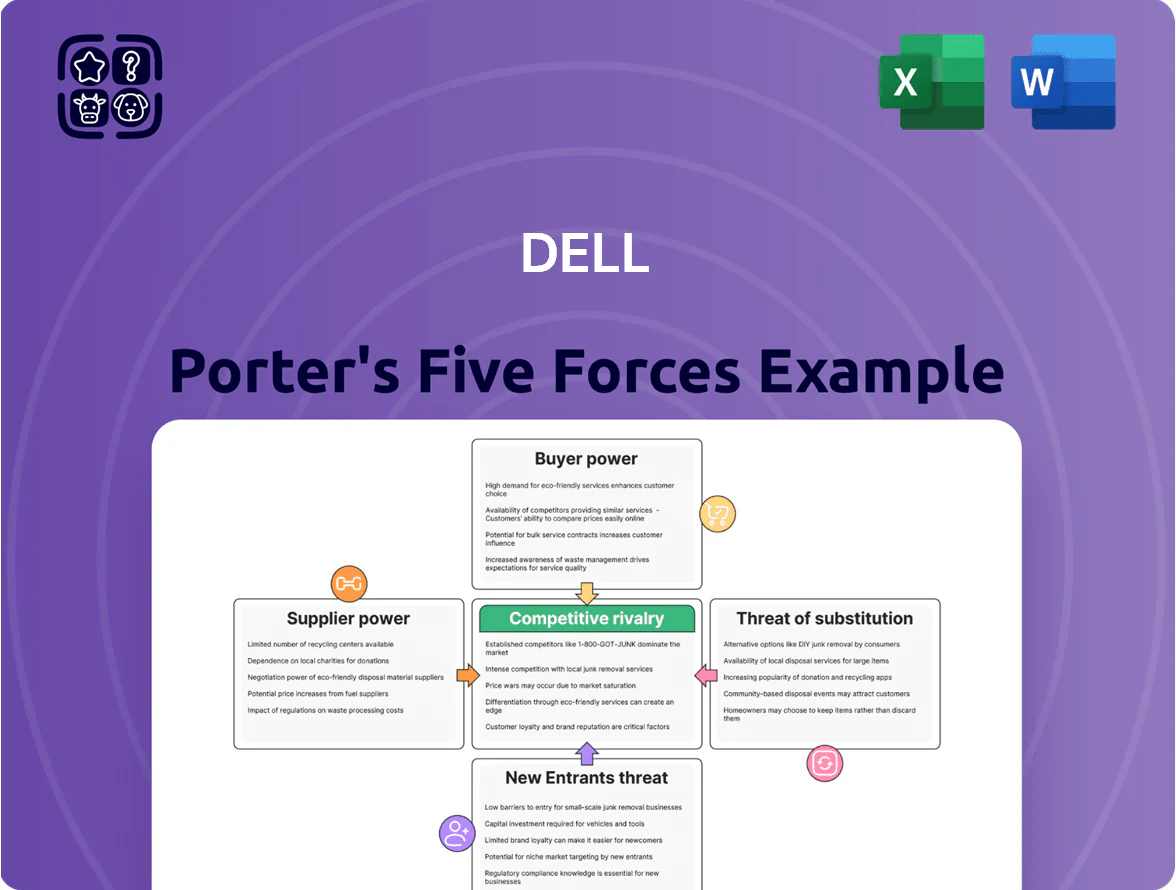

Dell faces intense rivalry from PC and server makers, evolving buyer power, and supplier dynamics that shape margins; emerging cloud and substitute services also pressure long-term growth—this snapshot highlights key tensions and strategic levers.

Suppliers Bargaining Power

Dependency on Semiconductor Giants

Dell depends on a few chipmakers—Intel, AMD, Nvidia—for CPUs/GPUs; in 2024 Intel/AMD/Nvidia held ~70% of server/PC CPU and >80% of discrete GPU market, concentrating supplier power.

That concentration raised supplier leverage during the 2023–24 AI hardware rush, when GPU prices spiked ~30% and allocation cutbacks forced OEM shipment delays.

These chips are highly specialized, so Dell faces multi-quarter redesigns and certification costs if switching vendors, increasing supplier switching costs and strategic dependence.

Geopolitics and Supply Chain Vulnerability

Dominance of AI Hardware Providers

Commodity Volatility in Memory and Storage

Suppliers like Samsung and Micron dominate DRAM and NAND markets, which swung 40–60% in spot prices during 2023–2024; Dell’s scale dampens but doesn’t eliminate exposure, so Dell often becomes a price taker in upcycles.

The lack of close substitutes for high-speed memory/storage gives suppliers moderate-to-high influence on Dell’s COGS; memory costs can move gross margin by 100–300 basis points in tight markets.

- Major suppliers: Samsung, Micron, SK Hynix

- Spot volatility: ~40–60% (2023–24)

- Margin impact: 100–300 bps swing

- Dell’s hedge: scale buys but limited substitute

Software and Operating System Integration

Microsoft supplies Windows to roughly 75% of global PC OS market share as of 2025, giving it strong supplier power over Dell’s large PC and laptop mix; Dell depends on Windows for baseline compatibility and enterprise sales.

Deep integration of Windows and enterprise tools (Active Directory, Azure AD, Intune) is vital for functionality and buyer acceptance, so Dell follows Microsoft patch and feature timetables to avoid enterprise disruption.

Few viable OS alternatives exist for business customers, forcing Dell to accept Microsoft licensing, revenue-share terms, and update cadence to stay competitive; in 2024 Microsoft generated $86.9B from its More Personal Computing segment, underscoring its leverage.

- ~75% Windows PC market share (2025)

- Microsoft More Personal Computing revenue $86.9B (FY2024)

- Dell must align to Windows update/license schedules

Concentrated Chip Power: Suppliers, Taiwan Foundries & Volatile GPU/Memory Markets

Supplier power is high: Intel/AMD/Nvidia ~70% CPU & >80% discrete GPU share (2024); Taiwan holds ~63% advanced foundry capacity (2024); Nvidia AI chip scarcity drove H100/Blackwell allocation limits and ~30% price spikes (2023–24); memory spot swings ~40–60% moved Dell gross margin 100–300 bps; Microsoft Windows ~75% PC OS share (2025), giving license/control leverage.

| Metric | Value |

|---|---|

| CPU/GPU concentration | ~70% / >80% (2024) |

| Taiwan foundry share | ~63% (2024) |

| GPU price spike | ~30% (2023–24) |

| Memory volatility | 40–60% (2023–24) |

| Windows PC share | ~75% (2025) |

What is included in the product

Tailored exclusively for Dell, this Porter's Five Forces analysis uncovers competitive dynamics, supplier and buyer power, entry barriers, substitutes, and emerging disruptions that shape Dell’s pricing, profitability, and strategic positioning.

Concise Porter's Five Forces summary tailored for Dell—quickly pinpoint supplier, buyer, rivalry, entrant, and substitute pressures to guide strategic decisions.

Customers Bargaining Power

Enterprise Volume Influence

Large corporates and government buyers account for roughly 45% of Dell Technologies’ FY2024 revenue (ended Jan 2024), so their order volume gives them strong bargaining power.

They routinely demand double-digit discounts and bespoke service-level agreements (SLA), forcing Dell to offer price concessions and tailored support during RFPs.

Dell balances slim gross margins—22.8% in FY2024—against the need to win multi-year contracts worth hundreds of millions by using volume pricing, bundling, and cost-efficiency measures.

Low Switching Costs for Individual Consumers

Expansion of Infrastructure as a Service

The rise of Dell APEX and consumption pricing shifted buyer power toward subscriptions: by FY2024 Dell reported APEX orders growing 23% year-over-year, pushing customers to demand pay-as-you-go flexibility and monthly billing.

Customers can scale capacity up or down by usage, transferring efficiency risk to Dell and forcing tighter SLAs and lower unit costs—APEX targets rental-like margins, so buyers press for continual price/performance gains.

Because buyers avoid sunk hardware buys, they insist on ongoing innovation and feature updates; in 2024 49% of enterprise cloud buyers cited service agility as their top purchase driver, strengthening customer negotiating leverage.

Public Sector Bidding Processes

Educational institutions and government agencies use strict competitive bidding that boosts buyer power; in US federal procurement in FY2024, 23% of IT contracts were awarded to lowest-price technically acceptable offers, pressuring margins.

Dell must meet cost and compliance specs (e.g., FIPS, FedRAMP) and invest in specialized public-sector sales and compliance teams; Dell’s public-sector revenue was about $13.4B in FY2024, so procurement wins materially affect top-line.

- Bidding favors lowest compliant bid

- Compliance standards: FIPS, FedRAMP, GSA schedules

- Dell public-sector revenue approx $13.4B (FY2024)

- Specialized sales/compliance raises bid costs

Availability of Information and Market Transparency

The digital age gives buyers wide access to pricing, benchmarks, and reviews, cutting Dell’s ability to hold premium prices unless it shows clear tech or support advantages; Gartner reported 72% of enterprise buyers used third-party reviews in 2024 when selecting vendors.

Information symmetry strengthens negotiation power—buyers demand features tied to AI, edge, and security trends, and IDC noted 61% of procurement teams negotiated price or SLA in 2024.

High-volume buyers & public bids squeeze prices as APEX growth demands flexible SLAs

Large buyers (≈45% of FY2024 revenue) and public-sector procurement (≈$13.4B) give customers high bargaining power via volume discounts, strict SLAs, and lowest-price bidding; consumer shoppers (68% price-driven) and review transparency (72% use third‑party reviews) force promotional pricing; APEX subscription growth (23% YoY) raises demands for pay-as-you-go flexibility and tighter SLAs.

| Metric | Value |

|---|---|

| Large-buyer share | ≈45% FY2024 |

| Public-sector rev | $13.4B FY2024 |

| APEX growth | 23% YoY |

| Price-driven consumers | 68% (2024) |

| Third-party reviews | 72% (Gartner 2024) |

Full Version Awaits

Dell Porter's Five Forces Analysis

This preview shows the exact Dell Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the full, professionally formatted analysis, ready for download and use the moment you buy. You're looking at the actual deliverable; once your purchase is complete, you'll get instant access to this same file. No mockups or samples—what you see is what you get.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Dell faces intense rivalry from PC and server makers, evolving buyer power, and supplier dynamics that shape margins; emerging cloud and substitute services also pressure long-term growth—this snapshot highlights key tensions and strategic levers.

Suppliers Bargaining Power

Dependency on Semiconductor Giants

Dell depends on a few chipmakers—Intel, AMD, Nvidia—for CPUs/GPUs; in 2024 Intel/AMD/Nvidia held ~70% of server/PC CPU and >80% of discrete GPU market, concentrating supplier power.

That concentration raised supplier leverage during the 2023–24 AI hardware rush, when GPU prices spiked ~30% and allocation cutbacks forced OEM shipment delays.

These chips are highly specialized, so Dell faces multi-quarter redesigns and certification costs if switching vendors, increasing supplier switching costs and strategic dependence.

Geopolitics and Supply Chain Vulnerability

Dominance of AI Hardware Providers

Commodity Volatility in Memory and Storage

Suppliers like Samsung and Micron dominate DRAM and NAND markets, which swung 40–60% in spot prices during 2023–2024; Dell’s scale dampens but doesn’t eliminate exposure, so Dell often becomes a price taker in upcycles.

The lack of close substitutes for high-speed memory/storage gives suppliers moderate-to-high influence on Dell’s COGS; memory costs can move gross margin by 100–300 basis points in tight markets.

- Major suppliers: Samsung, Micron, SK Hynix

- Spot volatility: ~40–60% (2023–24)

- Margin impact: 100–300 bps swing

- Dell’s hedge: scale buys but limited substitute

Software and Operating System Integration

Microsoft supplies Windows to roughly 75% of global PC OS market share as of 2025, giving it strong supplier power over Dell’s large PC and laptop mix; Dell depends on Windows for baseline compatibility and enterprise sales.

Deep integration of Windows and enterprise tools (Active Directory, Azure AD, Intune) is vital for functionality and buyer acceptance, so Dell follows Microsoft patch and feature timetables to avoid enterprise disruption.

Few viable OS alternatives exist for business customers, forcing Dell to accept Microsoft licensing, revenue-share terms, and update cadence to stay competitive; in 2024 Microsoft generated $86.9B from its More Personal Computing segment, underscoring its leverage.

- ~75% Windows PC market share (2025)

- Microsoft More Personal Computing revenue $86.9B (FY2024)

- Dell must align to Windows update/license schedules

Concentrated Chip Power: Suppliers, Taiwan Foundries & Volatile GPU/Memory Markets

Supplier power is high: Intel/AMD/Nvidia ~70% CPU & >80% discrete GPU share (2024); Taiwan holds ~63% advanced foundry capacity (2024); Nvidia AI chip scarcity drove H100/Blackwell allocation limits and ~30% price spikes (2023–24); memory spot swings ~40–60% moved Dell gross margin 100–300 bps; Microsoft Windows ~75% PC OS share (2025), giving license/control leverage.

| Metric | Value |

|---|---|

| CPU/GPU concentration | ~70% / >80% (2024) |

| Taiwan foundry share | ~63% (2024) |

| GPU price spike | ~30% (2023–24) |

| Memory volatility | 40–60% (2023–24) |

| Windows PC share | ~75% (2025) |

What is included in the product

Tailored exclusively for Dell, this Porter's Five Forces analysis uncovers competitive dynamics, supplier and buyer power, entry barriers, substitutes, and emerging disruptions that shape Dell’s pricing, profitability, and strategic positioning.

Concise Porter's Five Forces summary tailored for Dell—quickly pinpoint supplier, buyer, rivalry, entrant, and substitute pressures to guide strategic decisions.

Customers Bargaining Power

Enterprise Volume Influence

Large corporates and government buyers account for roughly 45% of Dell Technologies’ FY2024 revenue (ended Jan 2024), so their order volume gives them strong bargaining power.

They routinely demand double-digit discounts and bespoke service-level agreements (SLA), forcing Dell to offer price concessions and tailored support during RFPs.

Dell balances slim gross margins—22.8% in FY2024—against the need to win multi-year contracts worth hundreds of millions by using volume pricing, bundling, and cost-efficiency measures.

Low Switching Costs for Individual Consumers

Expansion of Infrastructure as a Service

The rise of Dell APEX and consumption pricing shifted buyer power toward subscriptions: by FY2024 Dell reported APEX orders growing 23% year-over-year, pushing customers to demand pay-as-you-go flexibility and monthly billing.

Customers can scale capacity up or down by usage, transferring efficiency risk to Dell and forcing tighter SLAs and lower unit costs—APEX targets rental-like margins, so buyers press for continual price/performance gains.

Because buyers avoid sunk hardware buys, they insist on ongoing innovation and feature updates; in 2024 49% of enterprise cloud buyers cited service agility as their top purchase driver, strengthening customer negotiating leverage.

Public Sector Bidding Processes

Educational institutions and government agencies use strict competitive bidding that boosts buyer power; in US federal procurement in FY2024, 23% of IT contracts were awarded to lowest-price technically acceptable offers, pressuring margins.

Dell must meet cost and compliance specs (e.g., FIPS, FedRAMP) and invest in specialized public-sector sales and compliance teams; Dell’s public-sector revenue was about $13.4B in FY2024, so procurement wins materially affect top-line.

- Bidding favors lowest compliant bid

- Compliance standards: FIPS, FedRAMP, GSA schedules

- Dell public-sector revenue approx $13.4B (FY2024)

- Specialized sales/compliance raises bid costs

Availability of Information and Market Transparency

The digital age gives buyers wide access to pricing, benchmarks, and reviews, cutting Dell’s ability to hold premium prices unless it shows clear tech or support advantages; Gartner reported 72% of enterprise buyers used third-party reviews in 2024 when selecting vendors.

Information symmetry strengthens negotiation power—buyers demand features tied to AI, edge, and security trends, and IDC noted 61% of procurement teams negotiated price or SLA in 2024.

High-volume buyers & public bids squeeze prices as APEX growth demands flexible SLAs

Large buyers (≈45% of FY2024 revenue) and public-sector procurement (≈$13.4B) give customers high bargaining power via volume discounts, strict SLAs, and lowest-price bidding; consumer shoppers (68% price-driven) and review transparency (72% use third‑party reviews) force promotional pricing; APEX subscription growth (23% YoY) raises demands for pay-as-you-go flexibility and tighter SLAs.

| Metric | Value |

|---|---|

| Large-buyer share | ≈45% FY2024 |

| Public-sector rev | $13.4B FY2024 |

| APEX growth | 23% YoY |

| Price-driven consumers | 68% (2024) |

| Third-party reviews | 72% (Gartner 2024) |

Full Version Awaits

Dell Porter's Five Forces Analysis

This preview shows the exact Dell Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the full, professionally formatted analysis, ready for download and use the moment you buy. You're looking at the actual deliverable; once your purchase is complete, you'll get instant access to this same file. No mockups or samples—what you see is what you get.