Delta Electronics Boston Consulting Group Matrix

Download Your Competitive Advantage

Delta Electronics’ BCG Matrix preview highlights its mix of high-growth power electronics and steady industrial automation segments, revealing likely Stars and Cash Cows amid slower legacy lines. This snapshot hints at where management should invest or harvest but stops short of quadrant-level granularity and tailored actions. Dive deeper into the full BCG Matrix to get detailed placements, data-driven recommendations, and a ready-to-use strategic roadmap. Purchase the complete report for Word and Excel deliverables that save you time and sharpen decision-making.

Stars

AI Data Center Power Solutions

Delta Electronics holds a top position in AI server power supplies, supplying high-efficiency units for high-density racks and capturing roughly 25% of the global AI PSU market by revenue as of Q4 2025.

Explosive generative AI build-outs drove a 38% year-over-year segment revenue rise in 2025, with data-center customers favoring Delta’s 96%+ efficiency platforms that command premium margins.

Maintaining advantage requires ongoing R and D spend—Delta increased R and D for power systems to 6.2% of segment sales in 2025—yet the unit economics stay strong as hyperscalers scale.

This AI data-center power segment remains Delta’s primary growth engine, contributing about 30% of company operating profit growth in 2025 while anchoring its role in the global AI hardware supply chain.

Electric Vehicle Powertrain Components

Delta Electronics has become a top-tier supplier of on-board chargers and DC-DC converters to global OEMs, with automotive revenue rising to NT$72.5 billion in 2024 (about US$2.2bn), up 18% year-on-year.

Even with EV sales swings, demand for high-voltage power electronics stays strong as legacy automakers shift platforms; global EV penetration hit 14% in 2024, supporting sustained order books.

Delta is spending heavily on capacity and R&D—capex for smart mobility rose to NT$15.3 billion in 2024—to keep an edge in this capital-intensive segment.

This powertrain unit sits as a BCG Stars: high-growth leader, projected to turn into a major profit center as margins improve with volume and chassis electrification through 2027.

Liquid Cooling and Thermal Management

With AI chips driving higher power densities, Delta Electronics’ liquid cooling and thermal management unit has captured ~18% global market share in data-center cooling as of 2025, replacing legacy air systems in high-density racks.

Cloud providers pushed demand, helping the unit grow revenue by ~28% YoY in 2024 to roughly $620M, reflecting Delta’s edge from decades in fan tech applied to liquid cooling modules.

Delta’s ongoing R&D — ~2.1% of 2024 revenue reinvested — aims to fend off newcomers and protect its premium position in this high-growth segment.

Energy Storage Systems

Delta Electronics positions Energy Storage Systems as a Star, offering scalable grid and industrial battery solutions that tapped a global storage market reaching ~$70bn in 2025 (BNEF) and >30% CAGR 2020–25 in deployments.

Its leading power-conversion market share—roughly 15% of global PCS shipments in 2024—gives tech and cost advantages; projects consume cash but drive recurring service and system revenues.

- Market size ~ $70bn (2025)

- CAGR >30% (2020–25)

- Delta PCS share ~15% (2024)

- High capex, rising O&M revenue

Smart Manufacturing and Robotics

The industrial automation segment has become a star as AI-driven robotics and automated lines raise factory productivity; global factory automation market hit USD 224.8 billion in 2024, growing ~8.6% CAGR to 2030.

Delta supplies key power, drives, and control software enabling Industry 4.0 migrations; its industrial automation revenue was NT$72.4 billion in 2024, up 12% year-over-year.

Rising labor costs and demand for precision push adoption—robot unit shipments grew 9% in 2024—and Delta’s strong Asia and Europe footprint keeps it a leader in this high-growth field.

- Market size 2024: USD 224.8B; CAGR ~8.6% to 2030

- Delta industrial automation revenue 2024: NT$72.4B (+12% YoY)

- Robot shipments growth 2024: +9%

- Strong presence: Asia, Europe — leading market share in power/drives

Delta’s powerhouses: AI PSU, EV, cooling, ESS & automation drive stellar market share growth

Delta’s AI server PSU, EV powertrain, liquid cooling, ESS, and industrial automation units are Stars—high market share in 2024–25 with strong growth: AI PSU ~25% global share (Q4 2025), AI segment +38% YoY (2025), EV revenue NT$72.5B (2024), cooling share ~18% (2025), ESS PCS ~15% (2024), automation revenue NT$72.4B (2024).

| Business | Key metric | Year |

|---|---|---|

| AI PSU | 25% global revenue share | Q4 2025 |

| AI segment | +38% YoY growth | 2025 |

| EV powertrain | NT$72.5B revenue | 2024 |

| Liquid cooling | ~18% market share | 2025 |

| ESS (PCS) | ~15% shipments share | 2024 |

| Industrial automation | NT$72.4B revenue | 2024 |

What is included in the product

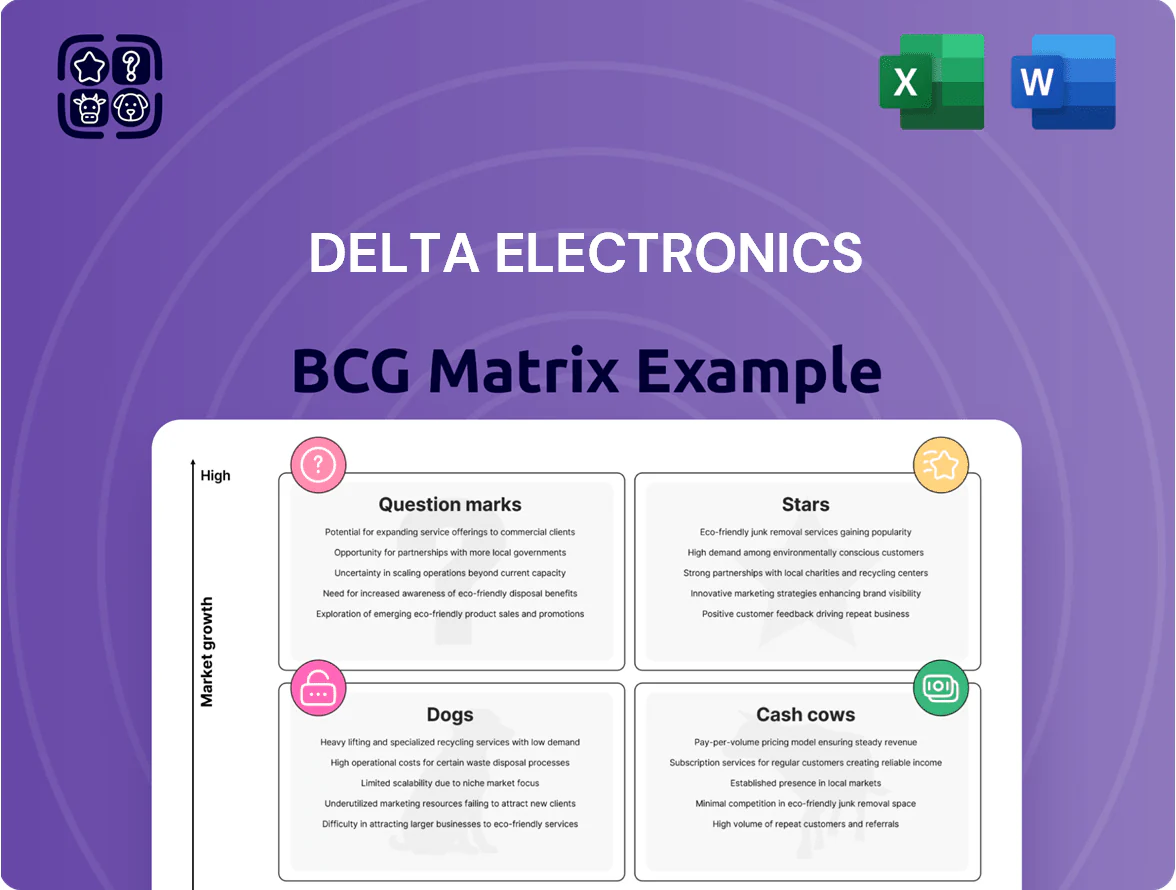

BCG Matrix mapping Delta Electronics’ units with strategic moves—invest in Stars, milk Cash Cows, evaluate Question Marks, divest Dogs.

One-page BCG matrix placing Delta Electronics’ business units in quadrants for quick strategic decisions and investor-ready sharing.

Cash Cows

Standard Switching Power Supplies

Delta Electronics standard switching power supplies are a cash cow, holding roughly 35–40% of the global PC/server PSU market and generating steady revenue—about US$1.2–1.4 billion annual segment sales in 2024—thanks to mature, low-growth demand.

Established tech means low incremental capex (single-digit percent of segment sales) to maintain leadership, producing predictable free cash flow used to fund higher-growth areas like EV powertrains and charging (Delta invested ~US$450M in EV-related R&D in 2024).

Industrial Inverters and PLCs

Delta Electronics dominates global frequency inverters and programmable logic controllers (PLCs), holding an estimated 18–22% market share in industrial drives as of 2024 and serving factories, HVAC, and renewables where reliability trumps rapid innovation.

These products sit in a slow-growth industrial segment (CAGR ~2–3% to 2028) and yield high gross margins (reported ~34% in Delta’s 2024 segment disclosure), with low incremental capex versus R&D-heavy units.

As a classic cash cow, the unit reliably funds corporate needs: in 2024 it contributed roughly 30% of operating cash flow, helping Delta pay down debt and sustain a 2024 dividend payout ratio near 40%.

Telecom Power Infrastructure

Delta Electronics’ Telecom Power Infrastructure unit supplies power systems for global telecom networks, including 5G base stations, and generated about US$1.1bn in FY2024 revenue (≈12% of group), driven by maintenance and upgrades after the initial 5G rollout slowed.

Operating in a mature market with few true global competitors, Delta’s long-term service contracts and multiyear OEM relationships kept segment gross margins near 22% in 2024, making it a stable cash cow and reliable liquidity source.

High Efficiency DC Fans

Delta Electronics leads global brushless DC (BLDC) fan production, supplying consumer electronics, appliances, and automotive cooling; in 2024 Delta reported cooling components revenue of about US$1.1 billion, with fans comprising a large share.

The BLDC fan market is mature—global CAGR ~2% (2024–2029)—but Delta’s scale and automated fabs keep gross margins above 30%, letting fans operate as high-efficiency cash cows.

These ubiquitous fans need minimal marketing or placement spend; steady cash flow funds R&D into advanced thermal management (liquid cooling, heat pipes), supporting new product lines and higher-margin solutions.

- 2024 cooling revenue ~US$1.1B

- Gross margins >30%

- Market CAGR ~2% (2024–2029)

- Funds R&D for advanced thermal systems

Networking Hardware and Switches

Networking Hardware and Switches: Delta Electronics' switches deliver steady revenue within its ICT segment, contributing roughly $450–520M annually (2024 est.) and holding mid-teens market share in APAC corporate/industrial markets, so they act as a cash cow—low growth but reliable cash flow versus AI hardware.

This unit benefits from enterprise digitalization with ~5–7% CAGR demand for standard switches (2023–2026 IDC), requires modest capex, and shows low margin volatility—operating margin ~8–10% in FY2024—supporting Delta's overall profitability.

- Annual revenue ~ $450–520M (2024 est.)

- Operating margin ~8–10% (FY2024)

- APAC mid-teens market share in corporate/industrial

- Demand CAGR ~5–7% (2023–2026, IDC)

Delta’s cash cows—$4.3–4.6B in mature units fuel $450M EV & charging R&D

Delta’s mature power supplies, industrial drives/PLCs, telecom power, BLDC fans, and standard switches acted as cash cows in 2024, generating ~US$4.3–4.6B combined revenue, high gross margins (fans ~30%; power supplies ~34%), low incremental capex (single-digit % of segment sales), and contributed ~30% of operating cash flow to fund EV and charging R&D (~US$450M in 2024).

| Unit | 2024 Rev | Gross Margin | Market CAGR |

|---|---|---|---|

| Power supplies | US$1.2–1.4B | ~34% | ~2–3% |

| Telecom power | US$1.1B | ~22% | ~2–3% |

| BLDC fans | US$1.1B | >30% | ~2% |

| Switches | US$0.45–0.52B | ~8–10% op | 5–7% |

What You’re Viewing Is Included

Delta Electronics BCG Matrix

The preview you're viewing is the exact Delta Electronics BCG Matrix report you'll receive after purchase—no watermarks, no demo placeholders—just a fully formatted, analysis-ready document designed for strategic clarity and professional presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Delta Electronics’ BCG Matrix preview highlights its mix of high-growth power electronics and steady industrial automation segments, revealing likely Stars and Cash Cows amid slower legacy lines. This snapshot hints at where management should invest or harvest but stops short of quadrant-level granularity and tailored actions. Dive deeper into the full BCG Matrix to get detailed placements, data-driven recommendations, and a ready-to-use strategic roadmap. Purchase the complete report for Word and Excel deliverables that save you time and sharpen decision-making.

Stars

AI Data Center Power Solutions

Delta Electronics holds a top position in AI server power supplies, supplying high-efficiency units for high-density racks and capturing roughly 25% of the global AI PSU market by revenue as of Q4 2025.

Explosive generative AI build-outs drove a 38% year-over-year segment revenue rise in 2025, with data-center customers favoring Delta’s 96%+ efficiency platforms that command premium margins.

Maintaining advantage requires ongoing R and D spend—Delta increased R and D for power systems to 6.2% of segment sales in 2025—yet the unit economics stay strong as hyperscalers scale.

This AI data-center power segment remains Delta’s primary growth engine, contributing about 30% of company operating profit growth in 2025 while anchoring its role in the global AI hardware supply chain.

Electric Vehicle Powertrain Components

Delta Electronics has become a top-tier supplier of on-board chargers and DC-DC converters to global OEMs, with automotive revenue rising to NT$72.5 billion in 2024 (about US$2.2bn), up 18% year-on-year.

Even with EV sales swings, demand for high-voltage power electronics stays strong as legacy automakers shift platforms; global EV penetration hit 14% in 2024, supporting sustained order books.

Delta is spending heavily on capacity and R&D—capex for smart mobility rose to NT$15.3 billion in 2024—to keep an edge in this capital-intensive segment.

This powertrain unit sits as a BCG Stars: high-growth leader, projected to turn into a major profit center as margins improve with volume and chassis electrification through 2027.

Liquid Cooling and Thermal Management

With AI chips driving higher power densities, Delta Electronics’ liquid cooling and thermal management unit has captured ~18% global market share in data-center cooling as of 2025, replacing legacy air systems in high-density racks.

Cloud providers pushed demand, helping the unit grow revenue by ~28% YoY in 2024 to roughly $620M, reflecting Delta’s edge from decades in fan tech applied to liquid cooling modules.

Delta’s ongoing R&D — ~2.1% of 2024 revenue reinvested — aims to fend off newcomers and protect its premium position in this high-growth segment.

Energy Storage Systems

Delta Electronics positions Energy Storage Systems as a Star, offering scalable grid and industrial battery solutions that tapped a global storage market reaching ~$70bn in 2025 (BNEF) and >30% CAGR 2020–25 in deployments.

Its leading power-conversion market share—roughly 15% of global PCS shipments in 2024—gives tech and cost advantages; projects consume cash but drive recurring service and system revenues.

- Market size ~ $70bn (2025)

- CAGR >30% (2020–25)

- Delta PCS share ~15% (2024)

- High capex, rising O&M revenue

Smart Manufacturing and Robotics

The industrial automation segment has become a star as AI-driven robotics and automated lines raise factory productivity; global factory automation market hit USD 224.8 billion in 2024, growing ~8.6% CAGR to 2030.

Delta supplies key power, drives, and control software enabling Industry 4.0 migrations; its industrial automation revenue was NT$72.4 billion in 2024, up 12% year-over-year.

Rising labor costs and demand for precision push adoption—robot unit shipments grew 9% in 2024—and Delta’s strong Asia and Europe footprint keeps it a leader in this high-growth field.

- Market size 2024: USD 224.8B; CAGR ~8.6% to 2030

- Delta industrial automation revenue 2024: NT$72.4B (+12% YoY)

- Robot shipments growth 2024: +9%

- Strong presence: Asia, Europe — leading market share in power/drives

Delta’s powerhouses: AI PSU, EV, cooling, ESS & automation drive stellar market share growth

Delta’s AI server PSU, EV powertrain, liquid cooling, ESS, and industrial automation units are Stars—high market share in 2024–25 with strong growth: AI PSU ~25% global share (Q4 2025), AI segment +38% YoY (2025), EV revenue NT$72.5B (2024), cooling share ~18% (2025), ESS PCS ~15% (2024), automation revenue NT$72.4B (2024).

| Business | Key metric | Year |

|---|---|---|

| AI PSU | 25% global revenue share | Q4 2025 |

| AI segment | +38% YoY growth | 2025 |

| EV powertrain | NT$72.5B revenue | 2024 |

| Liquid cooling | ~18% market share | 2025 |

| ESS (PCS) | ~15% shipments share | 2024 |

| Industrial automation | NT$72.4B revenue | 2024 |

What is included in the product

BCG Matrix mapping Delta Electronics’ units with strategic moves—invest in Stars, milk Cash Cows, evaluate Question Marks, divest Dogs.

One-page BCG matrix placing Delta Electronics’ business units in quadrants for quick strategic decisions and investor-ready sharing.

Cash Cows

Standard Switching Power Supplies

Delta Electronics standard switching power supplies are a cash cow, holding roughly 35–40% of the global PC/server PSU market and generating steady revenue—about US$1.2–1.4 billion annual segment sales in 2024—thanks to mature, low-growth demand.

Established tech means low incremental capex (single-digit percent of segment sales) to maintain leadership, producing predictable free cash flow used to fund higher-growth areas like EV powertrains and charging (Delta invested ~US$450M in EV-related R&D in 2024).

Industrial Inverters and PLCs

Delta Electronics dominates global frequency inverters and programmable logic controllers (PLCs), holding an estimated 18–22% market share in industrial drives as of 2024 and serving factories, HVAC, and renewables where reliability trumps rapid innovation.

These products sit in a slow-growth industrial segment (CAGR ~2–3% to 2028) and yield high gross margins (reported ~34% in Delta’s 2024 segment disclosure), with low incremental capex versus R&D-heavy units.

As a classic cash cow, the unit reliably funds corporate needs: in 2024 it contributed roughly 30% of operating cash flow, helping Delta pay down debt and sustain a 2024 dividend payout ratio near 40%.

Telecom Power Infrastructure

Delta Electronics’ Telecom Power Infrastructure unit supplies power systems for global telecom networks, including 5G base stations, and generated about US$1.1bn in FY2024 revenue (≈12% of group), driven by maintenance and upgrades after the initial 5G rollout slowed.

Operating in a mature market with few true global competitors, Delta’s long-term service contracts and multiyear OEM relationships kept segment gross margins near 22% in 2024, making it a stable cash cow and reliable liquidity source.

High Efficiency DC Fans

Delta Electronics leads global brushless DC (BLDC) fan production, supplying consumer electronics, appliances, and automotive cooling; in 2024 Delta reported cooling components revenue of about US$1.1 billion, with fans comprising a large share.

The BLDC fan market is mature—global CAGR ~2% (2024–2029)—but Delta’s scale and automated fabs keep gross margins above 30%, letting fans operate as high-efficiency cash cows.

These ubiquitous fans need minimal marketing or placement spend; steady cash flow funds R&D into advanced thermal management (liquid cooling, heat pipes), supporting new product lines and higher-margin solutions.

- 2024 cooling revenue ~US$1.1B

- Gross margins >30%

- Market CAGR ~2% (2024–2029)

- Funds R&D for advanced thermal systems

Networking Hardware and Switches

Networking Hardware and Switches: Delta Electronics' switches deliver steady revenue within its ICT segment, contributing roughly $450–520M annually (2024 est.) and holding mid-teens market share in APAC corporate/industrial markets, so they act as a cash cow—low growth but reliable cash flow versus AI hardware.

This unit benefits from enterprise digitalization with ~5–7% CAGR demand for standard switches (2023–2026 IDC), requires modest capex, and shows low margin volatility—operating margin ~8–10% in FY2024—supporting Delta's overall profitability.

- Annual revenue ~ $450–520M (2024 est.)

- Operating margin ~8–10% (FY2024)

- APAC mid-teens market share in corporate/industrial

- Demand CAGR ~5–7% (2023–2026, IDC)

Delta’s cash cows—$4.3–4.6B in mature units fuel $450M EV & charging R&D

Delta’s mature power supplies, industrial drives/PLCs, telecom power, BLDC fans, and standard switches acted as cash cows in 2024, generating ~US$4.3–4.6B combined revenue, high gross margins (fans ~30%; power supplies ~34%), low incremental capex (single-digit % of segment sales), and contributed ~30% of operating cash flow to fund EV and charging R&D (~US$450M in 2024).

| Unit | 2024 Rev | Gross Margin | Market CAGR |

|---|---|---|---|

| Power supplies | US$1.2–1.4B | ~34% | ~2–3% |

| Telecom power | US$1.1B | ~22% | ~2–3% |

| BLDC fans | US$1.1B | >30% | ~2% |

| Switches | US$0.45–0.52B | ~8–10% op | 5–7% |

What You’re Viewing Is Included

Delta Electronics BCG Matrix

The preview you're viewing is the exact Delta Electronics BCG Matrix report you'll receive after purchase—no watermarks, no demo placeholders—just a fully formatted, analysis-ready document designed for strategic clarity and professional presentation.