Delta Electronics Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Delta Electronics faces moderate supplier power, intense rivalry from global power- and automation-equipment makers, growing buyer sophistication, and a rising threat from modular, low-cost substitutes—yet its scale and energy-efficiency IP provide defensive advantages.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Delta Electronics’s competitive dynamics, market pressures, and strategic advantages in detail.

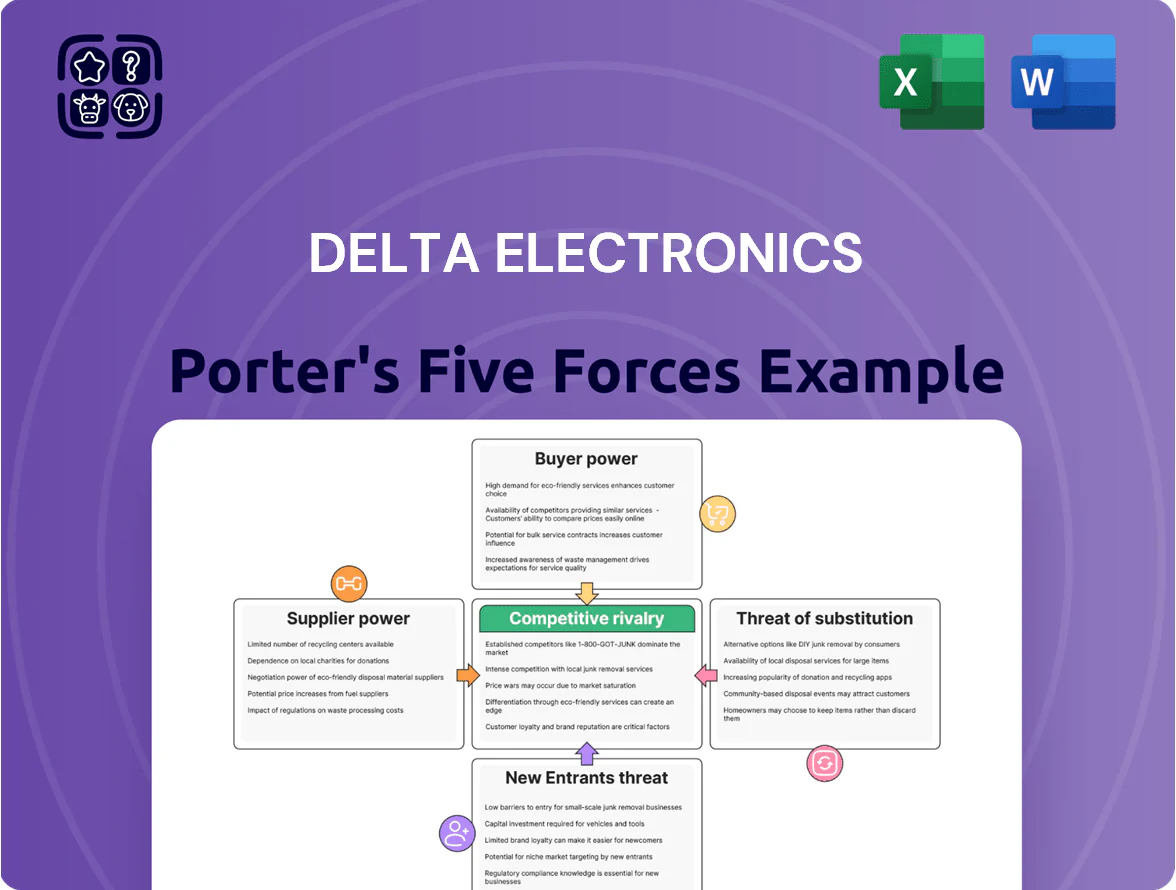

Suppliers Bargaining Power

Semiconductor dependency and supply chain leverage

Delta depends on specialized semiconductors for power supplies and EV chargers; in 2025 these chips account for roughly 18–22% of BOM value per unit, raising supplier influence.

Geopolitical tensions in the Asia-Pacific as of late 2025 keep lead foundries able to push 8–15% price premiums and 12–20 week lead-time variability, increasing supply risk.

To mitigate this, Delta holds strategic stockpiles covering 3–6 months of critical chips and signs multi-year agreements covering ~60% of chip needs to secure delivery and cap costs.

Raw material price volatility

Delta Electronics relies heavily on copper, aluminum and rare earths for thermal management and power modules; copper accounts for roughly 30–40% of conductive material costs in power products, so a 10% copper price rise (2022–2025 average volatility) can cut gross margins by ~1.5–2.0 percentage points.

Strategic multi-sourcing and regional diversification

Delta Electronics has cut supplier leverage by multi-sourcing across Southeast Asia, India, and the Americas, expanding its vendor count by ~38% from 2019–2024 and sourcing ~42% of components outside Taiwan as of FY2024; this lowers concentration risk so no single supplier or region can set prices, boosts resilience against events like 2021–2022 supply shocks, and helped trim component-cost volatility, improving gross-margin stability.

Vertical integration of critical components

Delta Electronics has increased internal production of critical sub-assemblies and proprietary components, cutting reliance on external suppliers for power modules and thermal solutions; in 2024 internal component sourcing rose to about 38% of COGS from 29% in 2021, improving supply control.

This vertical integration trims the pool of third-party manufacturers, lowers supplier bargaining power, and helped the company avoid ~6–9% input-cost spikes during 2021–2023 supply shocks.

- Internal sourcing up to 38% of COGS (2024)

- Supplier count for core modules down by ~22% since 2020

- Input-cost spike exposure cut ~6–9% in 2021–2023

Quality and sustainability compliance standards

Delta enforces strict ESG standards on suppliers to meet EU, US, and customer rules; by 2024 over 72% of its tier-one suppliers had third-party sustainability audits, cutting eligible vendors but raising compliance.

This narrows the vendor pool yet creates reciprocal dependence: suppliers need Delta's ~$9.6B 2024 electronics purchases to scale, so power balances via multi-year contracts and joint improvement programs.

Long-term collaboration reduces supplier bargaining power but ties partners to Delta through shared CapEx and volume guarantees.

- 72% suppliers audited (2024)

- $9.6B supplier spend (2024)

- Multi-year contracts >60% of spend

Moderate supplier power—critical chips/metals offset by multi‑sourcing, contracts, audits

Suppliers hold moderate power: critical semiconductors (18–22% BOM) and metals (copper 30–40% of conductive costs) raise dependence, but multi-sourcing (42% components outside Taiwan in FY2024), 60%+ multi-year chip contracts, 38% internal sourcing (2024) and $9.6B spend cut supplier leverage, while 72% audited suppliers tighten the vendor pool.

| Metric | Value |

|---|---|

| Semiconductor share of BOM | 18–22% |

| Copper share of conductive costs | 30–40% |

| Components sourced outside Taiwan (FY2024) | 42% |

| Internal sourcing of COGS (2024) | 38% |

| Multi-year contracts | ~60% of spend |

| Supplier audits (2024) | 72% |

| Supplier spend (2024) | $9.6B |

What is included in the product

Tailored exclusively for Delta Electronics, this Porter's Five Forces overview uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats that shape its pricing, profitability, and strategic positioning.

Concise Porter's Five Forces snapshot for Delta Electronics—quickly spot supplier, buyer, and competitive pressures to guide strategic moves.

Customers Bargaining Power

Concentration of hyperscale data center clients

Major cloud providers and hyperscale data center operators account for roughly 30–40% of Delta Electronics’ infrastructure revenue, so these buyers command strong bargaining power.

They demand highly efficient, customized thermal and power solutions at tight prices; Delta reported a 2024 gross margin of 23% in its Power Electronics segment, reflecting such pricing pressure.

Order volumes—often thousands of racks per contract—let buyers secure volume discounts, strict SLAs, and longer payment terms, compressing supplier bargaining leverage.

Low switching costs in commodity power products

For standard off-the-shelf power components, buyers face low switching costs and can source substitutes globally, boosting bargaining power for small industrial and consumer electronics clients; IDC reported in 2024 that >60% of component purchases for small OEMs were from open-market suppliers. Delta offsets this by selling integrated power systems and services—which made up ~35% of Delta’s FY2024 revenue—reducing customers’ ability to switch without major redesign costs.

High switching costs for integrated industrial systems

In industrial automation and EV infrastructure, Delta Electronics’ integrated hardware-software stacks create high switching costs: customers face reengineering, retraining, and downtime that can exceed 20–30% of project value per industry studies (2023), making swaps costly. Delta’s proprietary protocols and 24/7 support often tie clients to multi-year contracts; churn rates in comparable sectors fall below 5% annually. This technical lock-in reduces these customers’ bargaining power over the long term, preserving Delta’s pricing and margin leverage.

Regulatory demand for energy efficiency

Global carbon-neutrality mandates have increased demand for Delta Electronics’ high-efficiency power products; in 2024 Delta’s power solutions grew revenue ~8% year-on-year to roughly US$6.4 billion, reflecting buyers paying premiums for energy-saving equipment.

Corporate customers value capex that cuts opex and emissions—many target net-zero by 2050—so Delta’s specialized offerings shift bargaining power toward the supplier, letting it sustain higher margins.

- 2024 power revenue ≈ US$6.4B

- Y/Y growth ≈8% (2024)

- Buyers target net-zero by 2050

- Premiums for efficiency raise supplier leverage

Price sensitivity in the automotive EV sector

The EV market’s fierce price competition forces automakers to extract ~5–10% cost cuts from suppliers annually; as a key supplier of on-board chargers and charging stations, Delta Electronics faces heavy OEM pressure to cut unit prices, keeping customer bargaining power high compared with fragmented industrial buyers.

Hyperscalers squeeze margins; integrated systems & energy efficiency offer supplier leverage

Major cloud/hyperscalers drive strong buyer power (30–40% infra revenue); volume contracts force discounts and strict SLAs, while integrated systems (≈35% FY2024 revenue) and energy-efficiency premiums (2024 power revenue ≈US$6.4B, +8% y/y) create pockets of supplier leverage; EV OEMs push 5–10% annual cost cuts, keeping bargaining power high in that segment.

| Metric | 2024 |

|---|---|

| Power rev | US$6.4B |

| Power Y/Y | +8% |

| Infra buyer share | 30–40% |

| Integrated systems | ≈35% rev |

Full Version Awaits

Delta Electronics Porter's Five Forces Analysis

This preview shows the exact Delta Electronics Porter's Five Forces analysis you’ll receive—no placeholders or samples, fully formatted and ready for immediate download after purchase.

You're viewing the final, professionally written document; once you complete your purchase you’ll gain instant access to this same file for use in presentations, reports, or strategic planning.

No mockups—what’s shown is the deliverable, complete and ready to apply to your competitive and investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Delta Electronics faces moderate supplier power, intense rivalry from global power- and automation-equipment makers, growing buyer sophistication, and a rising threat from modular, low-cost substitutes—yet its scale and energy-efficiency IP provide defensive advantages.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Delta Electronics’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Semiconductor dependency and supply chain leverage

Delta depends on specialized semiconductors for power supplies and EV chargers; in 2025 these chips account for roughly 18–22% of BOM value per unit, raising supplier influence.

Geopolitical tensions in the Asia-Pacific as of late 2025 keep lead foundries able to push 8–15% price premiums and 12–20 week lead-time variability, increasing supply risk.

To mitigate this, Delta holds strategic stockpiles covering 3–6 months of critical chips and signs multi-year agreements covering ~60% of chip needs to secure delivery and cap costs.

Raw material price volatility

Delta Electronics relies heavily on copper, aluminum and rare earths for thermal management and power modules; copper accounts for roughly 30–40% of conductive material costs in power products, so a 10% copper price rise (2022–2025 average volatility) can cut gross margins by ~1.5–2.0 percentage points.

Strategic multi-sourcing and regional diversification

Delta Electronics has cut supplier leverage by multi-sourcing across Southeast Asia, India, and the Americas, expanding its vendor count by ~38% from 2019–2024 and sourcing ~42% of components outside Taiwan as of FY2024; this lowers concentration risk so no single supplier or region can set prices, boosts resilience against events like 2021–2022 supply shocks, and helped trim component-cost volatility, improving gross-margin stability.

Vertical integration of critical components

Delta Electronics has increased internal production of critical sub-assemblies and proprietary components, cutting reliance on external suppliers for power modules and thermal solutions; in 2024 internal component sourcing rose to about 38% of COGS from 29% in 2021, improving supply control.

This vertical integration trims the pool of third-party manufacturers, lowers supplier bargaining power, and helped the company avoid ~6–9% input-cost spikes during 2021–2023 supply shocks.

- Internal sourcing up to 38% of COGS (2024)

- Supplier count for core modules down by ~22% since 2020

- Input-cost spike exposure cut ~6–9% in 2021–2023

Quality and sustainability compliance standards

Delta enforces strict ESG standards on suppliers to meet EU, US, and customer rules; by 2024 over 72% of its tier-one suppliers had third-party sustainability audits, cutting eligible vendors but raising compliance.

This narrows the vendor pool yet creates reciprocal dependence: suppliers need Delta's ~$9.6B 2024 electronics purchases to scale, so power balances via multi-year contracts and joint improvement programs.

Long-term collaboration reduces supplier bargaining power but ties partners to Delta through shared CapEx and volume guarantees.

- 72% suppliers audited (2024)

- $9.6B supplier spend (2024)

- Multi-year contracts >60% of spend

Moderate supplier power—critical chips/metals offset by multi‑sourcing, contracts, audits

Suppliers hold moderate power: critical semiconductors (18–22% BOM) and metals (copper 30–40% of conductive costs) raise dependence, but multi-sourcing (42% components outside Taiwan in FY2024), 60%+ multi-year chip contracts, 38% internal sourcing (2024) and $9.6B spend cut supplier leverage, while 72% audited suppliers tighten the vendor pool.

| Metric | Value |

|---|---|

| Semiconductor share of BOM | 18–22% |

| Copper share of conductive costs | 30–40% |

| Components sourced outside Taiwan (FY2024) | 42% |

| Internal sourcing of COGS (2024) | 38% |

| Multi-year contracts | ~60% of spend |

| Supplier audits (2024) | 72% |

| Supplier spend (2024) | $9.6B |

What is included in the product

Tailored exclusively for Delta Electronics, this Porter's Five Forces overview uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats that shape its pricing, profitability, and strategic positioning.

Concise Porter's Five Forces snapshot for Delta Electronics—quickly spot supplier, buyer, and competitive pressures to guide strategic moves.

Customers Bargaining Power

Concentration of hyperscale data center clients

Major cloud providers and hyperscale data center operators account for roughly 30–40% of Delta Electronics’ infrastructure revenue, so these buyers command strong bargaining power.

They demand highly efficient, customized thermal and power solutions at tight prices; Delta reported a 2024 gross margin of 23% in its Power Electronics segment, reflecting such pricing pressure.

Order volumes—often thousands of racks per contract—let buyers secure volume discounts, strict SLAs, and longer payment terms, compressing supplier bargaining leverage.

Low switching costs in commodity power products

For standard off-the-shelf power components, buyers face low switching costs and can source substitutes globally, boosting bargaining power for small industrial and consumer electronics clients; IDC reported in 2024 that >60% of component purchases for small OEMs were from open-market suppliers. Delta offsets this by selling integrated power systems and services—which made up ~35% of Delta’s FY2024 revenue—reducing customers’ ability to switch without major redesign costs.

High switching costs for integrated industrial systems

In industrial automation and EV infrastructure, Delta Electronics’ integrated hardware-software stacks create high switching costs: customers face reengineering, retraining, and downtime that can exceed 20–30% of project value per industry studies (2023), making swaps costly. Delta’s proprietary protocols and 24/7 support often tie clients to multi-year contracts; churn rates in comparable sectors fall below 5% annually. This technical lock-in reduces these customers’ bargaining power over the long term, preserving Delta’s pricing and margin leverage.

Regulatory demand for energy efficiency

Global carbon-neutrality mandates have increased demand for Delta Electronics’ high-efficiency power products; in 2024 Delta’s power solutions grew revenue ~8% year-on-year to roughly US$6.4 billion, reflecting buyers paying premiums for energy-saving equipment.

Corporate customers value capex that cuts opex and emissions—many target net-zero by 2050—so Delta’s specialized offerings shift bargaining power toward the supplier, letting it sustain higher margins.

- 2024 power revenue ≈ US$6.4B

- Y/Y growth ≈8% (2024)

- Buyers target net-zero by 2050

- Premiums for efficiency raise supplier leverage

Price sensitivity in the automotive EV sector

The EV market’s fierce price competition forces automakers to extract ~5–10% cost cuts from suppliers annually; as a key supplier of on-board chargers and charging stations, Delta Electronics faces heavy OEM pressure to cut unit prices, keeping customer bargaining power high compared with fragmented industrial buyers.

Hyperscalers squeeze margins; integrated systems & energy efficiency offer supplier leverage

Major cloud/hyperscalers drive strong buyer power (30–40% infra revenue); volume contracts force discounts and strict SLAs, while integrated systems (≈35% FY2024 revenue) and energy-efficiency premiums (2024 power revenue ≈US$6.4B, +8% y/y) create pockets of supplier leverage; EV OEMs push 5–10% annual cost cuts, keeping bargaining power high in that segment.

| Metric | 2024 |

|---|---|

| Power rev | US$6.4B |

| Power Y/Y | +8% |

| Infra buyer share | 30–40% |

| Integrated systems | ≈35% rev |

Full Version Awaits

Delta Electronics Porter's Five Forces Analysis

This preview shows the exact Delta Electronics Porter's Five Forces analysis you’ll receive—no placeholders or samples, fully formatted and ready for immediate download after purchase.

You're viewing the final, professionally written document; once you complete your purchase you’ll gain instant access to this same file for use in presentations, reports, or strategic planning.

No mockups—what’s shown is the deliverable, complete and ready to apply to your competitive and investment decisions.