Dermapharm Holding Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

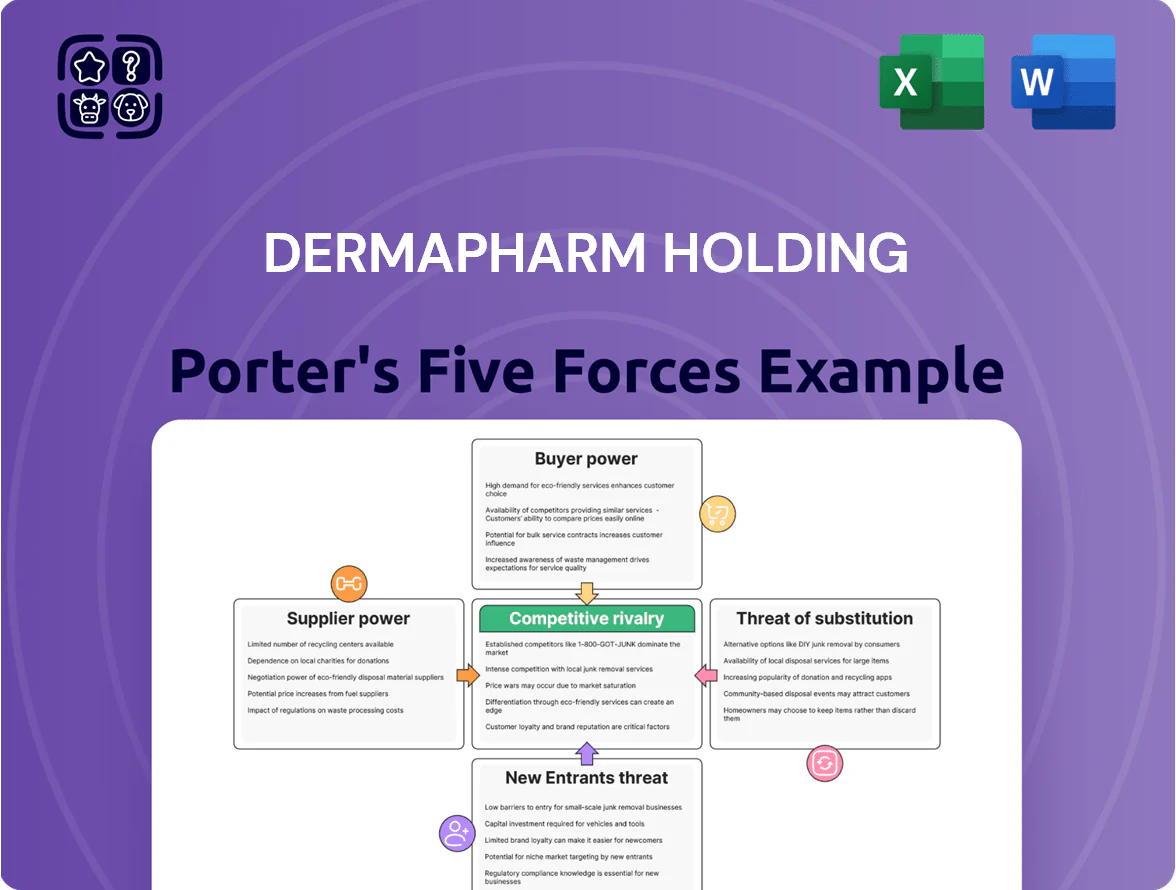

Dermapharm faces moderate buyer power and regulatory complexity, while brand strength and a diversified product mix mitigate supplier and substitute threats; competitive rivalry is elevated by private-label and specialty players.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Dermapharm Holding’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Active Pharmaceutical Ingredient Source Concentration

Dermapharm’s reliance on a handful of global suppliers for high-quality active pharmaceutical ingredients (APIs) creates moderate-to-high supplier power, as 70% of key APIs come from Asia and from fewer than 10 certified producers. Strict EU/GMP quality rules mean switching to unverified or cheaper suppliers risks regulatory fines and market recalls, limiting negotiating flexibility. By late 2025, the company had made supply-chain resilience a priority, targeting a 25% increase in dual-sourcing and buffer inventories to blunt price volatility and shipping delays. This concentration gives chemical and biological API suppliers clear leverage in contract talks, pushing Dermapharm toward longer-term contracts and joint risk-sharing agreements.

Energy and Utility Costs in European Manufacturing

Energy suppliers exert moderate-to-high bargaining power over Dermapharm due to the need for stable electricity and natural gas for sterile production; Germany industrial electricity prices averaged about 27 EUR/MWh in 2025, up ~8% year-on-year, raising COGS pressure.

The 2025 German push to renewable integration (renewables ~49% of power mix in 2024, grid updates ongoing) increases supplier complexity and short-term price volatility, letting providers influence Dermapharm’s production margins and capital expenditure planning.

Strict Regulatory Compliance for Packaging Materials

Suppliers of medical-grade packaging must meet EU safety and durability standards (e.g., EU GMP Annex 1), which narrows qualified vendors to a small pool—industry estimates show consolidation with top 5 suppliers holding ~60% of EU market in 2024.

High switching costs—quality audits, stability re-validation taking 6–12 months and €0.5–2.0m per SKU—give these vendors steady bargaining power.

As a result, packaging remains a stable, material manufacturing cost (~3–5% of COGS for Dermapharm in 2024) that limits procurement leverage.

Specialized Lab Equipment and Technology Providers

Specialized lab equipment and proprietary R&D software give suppliers strong leverage; many vendors lock customers into 5–10 year service contracts and consumables, pricing spare parts at 20–40% margins.

Dermapharm’s move into complex therapeutics by end‑2025 raised capex needs—company reported €65m R&D capex in 2024—making supplier switching costly and slow.

High technical skill and validation timelines (6–18 months) further cement supplier power and raise operational risk.

- Long service contracts: 5–10 years

- Supplier margins on parts: 20–40%

- Dermapharm R&D capex 2024: €65m

- Validation/switch time: 6–18 months

Logistics and Specialized Distribution Partners

Transporting sensitive pharma needs specialized logistics that preserve cold chains and GDP (Good Distribution Practice); only ~10–15 global providers meet strict GDP for EU/US markets, concentrating supplier power.

As Dermapharm expanded exports 28% in 2024, strategic logistics partners became critical; these firms can set fees and SLAs because they alone guarantee product integrity across regions.

- Few GDP-compliant firms (≈10–15)

- Dermapharm exports +28% in 2024

- Higher switching costs, premium fees

- Providers dictate SLAs to secure integrity

Supply Risks: 70% Asia API Concentration, High Validation Costs, Packagers Dominate

Suppliers hold moderate-to-high power: 70% of APIs from <10 Asian producers, dual-sourcing target +25% by end-2025; energy costs ~27 EUR/MWh (2025); top-5 EU packagers ≈60% market (2024); validation/switch 6–18 months costing €0.5–2.0m/SKU; R&D capex €65m (2024); GDP-compliant logistics ~10–15 firms; packaging = 3–5% COGS (2024).

| Metric | Value |

|---|---|

| APIs from Asia | 70% |

| Energy price (2025) | 27 EUR/MWh |

| Packagers market (top5, 2024) | 60% |

What is included in the product

Tailored exclusively for Dermapharm Holding, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats that shape its pricing, profitability, and strategic positioning.

A concise Porter's Five Forces snapshot for Dermapharm—quickly gauge competitive intensity, supplier and buyer power, threat of substitutes and new entrants to pinpoint strategic relief points.

Customers Bargaining Power

Influence of Statutory Health Insurance Funds

In Germany SHI funds (Gesetzliche Krankenversicherung) use rebate contracts to push prices down, awarding exclusivity to low-cost generics; in 2024 SHI covered ~88% of the population and saved an estimated €6.3bn via rebates. Dermapharm must win tenders to keep prescription products reimbursed, or risk losing market access to exclusive generic suppliers. This relentless bidding compresses margins in its branded-pharma segment, lowering average gross margins by several percentage points versus non-reimbursed OTC lines.

Consolidation of Pharmaceutical Wholesalers

The European pharma distribution market is concentrated: the top 5 wholesalers control roughly 65–70% of volumes, so they act as gatekeepers between manufacturers and retail pharmacies. These players leverage annual procurement volumes to extract better rebates and payment terms, forcing Dermapharm to accept lower gross margins to secure placement across ~20,000 pharmacy outlets. By late 2025 further M&A pushed their bargaining power higher, raising Dermapharm’s average trade discount by an estimated 150–250 basis points. As a result Dermapharm prioritizes portfolio breadth to retain distribution access and shelf share.

Price Sensitivity in the Over-The-Counter Market

For non-prescription meds and supplements, consumers choose across brands mainly on price and trust; EU OTC price transparency means 67% of German buyers compare prices online (Statista 2024), raising price sensitivity.

Online pharmacies and comparison tools cut switching costs, so Dermapharm must boost brand marketing and spend—its 2024 marketing capex rose 14% to €45m—to retain loyalty and defend premiums.

By end-2025, abundant wellness/skincare options increased churn risk; typical retention fell ~6pp in EU OTC categories in 2023–25, so Dermapharm faces higher retention costs.

Buying Groups and Pharmacy Cooperatives

Independent pharmacies join buying groups/cooperatives to pool demand; roughly 60% of German independents belonged to cooperatives in 2024, boosting negotiating leverage vs Dermapharm.

These groups create chain-like scale, pressing for deeper volume discounts and higher marketing subsidies, cutting Dermapharm’s margins if unmet.

Dermapharm must balance concession levels and targeted brand support to retain shelf space across Germany’s fragmented market.

- ~60% independents in cooperatives (2024)

- Higher discount/subsidy demands

- Risk: margin erosion vs market coverage

Governmental Healthcare Budget Constraints

Government agencies and health ministries act as indirect customers by imposing price ceilings and mandatory discounts that cut list prices for Dermapharm’s branded and OTC medicines.

In 2025 tighter EU fiscal caps and national cost-controls, including price freezes in Germany and Italy, shave 3–7% off typical product ASPs, capping revenue growth for core lines.

That forces Dermapharm to chase operational efficiency and higher volumes; unit-cost cuts and scale become primary levers to protect EBITDA margins.

- Price caps/discounts set by payers

- 2025 price freezes reduce ASPs ~3–7%

- Revenue growth limited; margin pressure

- Strategy: cut unit costs, drive volume

Buyers’ leverage squeezes margins: SHI rebates, wholesalers, online comparison cut ASPs

Customers hold strong leverage: SHI rebates (88% population, €6.3bn saved 2024) force tender wins; top-5 wholesalers control ~67% volumes, raising trade discounts +150–250bp by 2025; 67% of buyers compare OTC prices online (Statista 2024), driving marketing spend (+14% to €45m in 2024) and retention costs; 2025 price freezes cut ASPs ~3–7%, pressuring margins.

| Metric | Value |

|---|---|

| SHI coverage | ~88% (2024) |

| SHI rebates saved | €6.3bn (2024) |

| Top-5 wholesalers | 65–70% vol (2025) |

| Online price comparison | 67% buyers (2024) |

| Marketing spend | €45m (+14%, 2024) |

| Trade discount change | +150–250bp (by 2025) |

| ASPs impact | -3–7% (2025) |

What You See Is What You Get

Dermapharm Holding Porter's Five Forces Analysis

This preview shows the exact Dermapharm Holding Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders; the full document is fully formatted, professionally written, and ready for use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Dermapharm faces moderate buyer power and regulatory complexity, while brand strength and a diversified product mix mitigate supplier and substitute threats; competitive rivalry is elevated by private-label and specialty players.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Dermapharm Holding’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Active Pharmaceutical Ingredient Source Concentration

Dermapharm’s reliance on a handful of global suppliers for high-quality active pharmaceutical ingredients (APIs) creates moderate-to-high supplier power, as 70% of key APIs come from Asia and from fewer than 10 certified producers. Strict EU/GMP quality rules mean switching to unverified or cheaper suppliers risks regulatory fines and market recalls, limiting negotiating flexibility. By late 2025, the company had made supply-chain resilience a priority, targeting a 25% increase in dual-sourcing and buffer inventories to blunt price volatility and shipping delays. This concentration gives chemical and biological API suppliers clear leverage in contract talks, pushing Dermapharm toward longer-term contracts and joint risk-sharing agreements.

Energy and Utility Costs in European Manufacturing

Energy suppliers exert moderate-to-high bargaining power over Dermapharm due to the need for stable electricity and natural gas for sterile production; Germany industrial electricity prices averaged about 27 EUR/MWh in 2025, up ~8% year-on-year, raising COGS pressure.

The 2025 German push to renewable integration (renewables ~49% of power mix in 2024, grid updates ongoing) increases supplier complexity and short-term price volatility, letting providers influence Dermapharm’s production margins and capital expenditure planning.

Strict Regulatory Compliance for Packaging Materials

Suppliers of medical-grade packaging must meet EU safety and durability standards (e.g., EU GMP Annex 1), which narrows qualified vendors to a small pool—industry estimates show consolidation with top 5 suppliers holding ~60% of EU market in 2024.

High switching costs—quality audits, stability re-validation taking 6–12 months and €0.5–2.0m per SKU—give these vendors steady bargaining power.

As a result, packaging remains a stable, material manufacturing cost (~3–5% of COGS for Dermapharm in 2024) that limits procurement leverage.

Specialized Lab Equipment and Technology Providers

Specialized lab equipment and proprietary R&D software give suppliers strong leverage; many vendors lock customers into 5–10 year service contracts and consumables, pricing spare parts at 20–40% margins.

Dermapharm’s move into complex therapeutics by end‑2025 raised capex needs—company reported €65m R&D capex in 2024—making supplier switching costly and slow.

High technical skill and validation timelines (6–18 months) further cement supplier power and raise operational risk.

- Long service contracts: 5–10 years

- Supplier margins on parts: 20–40%

- Dermapharm R&D capex 2024: €65m

- Validation/switch time: 6–18 months

Logistics and Specialized Distribution Partners

Transporting sensitive pharma needs specialized logistics that preserve cold chains and GDP (Good Distribution Practice); only ~10–15 global providers meet strict GDP for EU/US markets, concentrating supplier power.

As Dermapharm expanded exports 28% in 2024, strategic logistics partners became critical; these firms can set fees and SLAs because they alone guarantee product integrity across regions.

- Few GDP-compliant firms (≈10–15)

- Dermapharm exports +28% in 2024

- Higher switching costs, premium fees

- Providers dictate SLAs to secure integrity

Supply Risks: 70% Asia API Concentration, High Validation Costs, Packagers Dominate

Suppliers hold moderate-to-high power: 70% of APIs from <10 Asian producers, dual-sourcing target +25% by end-2025; energy costs ~27 EUR/MWh (2025); top-5 EU packagers ≈60% market (2024); validation/switch 6–18 months costing €0.5–2.0m/SKU; R&D capex €65m (2024); GDP-compliant logistics ~10–15 firms; packaging = 3–5% COGS (2024).

| Metric | Value |

|---|---|

| APIs from Asia | 70% |

| Energy price (2025) | 27 EUR/MWh |

| Packagers market (top5, 2024) | 60% |

What is included in the product

Tailored exclusively for Dermapharm Holding, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats that shape its pricing, profitability, and strategic positioning.

A concise Porter's Five Forces snapshot for Dermapharm—quickly gauge competitive intensity, supplier and buyer power, threat of substitutes and new entrants to pinpoint strategic relief points.

Customers Bargaining Power

Influence of Statutory Health Insurance Funds

In Germany SHI funds (Gesetzliche Krankenversicherung) use rebate contracts to push prices down, awarding exclusivity to low-cost generics; in 2024 SHI covered ~88% of the population and saved an estimated €6.3bn via rebates. Dermapharm must win tenders to keep prescription products reimbursed, or risk losing market access to exclusive generic suppliers. This relentless bidding compresses margins in its branded-pharma segment, lowering average gross margins by several percentage points versus non-reimbursed OTC lines.

Consolidation of Pharmaceutical Wholesalers

The European pharma distribution market is concentrated: the top 5 wholesalers control roughly 65–70% of volumes, so they act as gatekeepers between manufacturers and retail pharmacies. These players leverage annual procurement volumes to extract better rebates and payment terms, forcing Dermapharm to accept lower gross margins to secure placement across ~20,000 pharmacy outlets. By late 2025 further M&A pushed their bargaining power higher, raising Dermapharm’s average trade discount by an estimated 150–250 basis points. As a result Dermapharm prioritizes portfolio breadth to retain distribution access and shelf share.

Price Sensitivity in the Over-The-Counter Market

For non-prescription meds and supplements, consumers choose across brands mainly on price and trust; EU OTC price transparency means 67% of German buyers compare prices online (Statista 2024), raising price sensitivity.

Online pharmacies and comparison tools cut switching costs, so Dermapharm must boost brand marketing and spend—its 2024 marketing capex rose 14% to €45m—to retain loyalty and defend premiums.

By end-2025, abundant wellness/skincare options increased churn risk; typical retention fell ~6pp in EU OTC categories in 2023–25, so Dermapharm faces higher retention costs.

Buying Groups and Pharmacy Cooperatives

Independent pharmacies join buying groups/cooperatives to pool demand; roughly 60% of German independents belonged to cooperatives in 2024, boosting negotiating leverage vs Dermapharm.

These groups create chain-like scale, pressing for deeper volume discounts and higher marketing subsidies, cutting Dermapharm’s margins if unmet.

Dermapharm must balance concession levels and targeted brand support to retain shelf space across Germany’s fragmented market.

- ~60% independents in cooperatives (2024)

- Higher discount/subsidy demands

- Risk: margin erosion vs market coverage

Governmental Healthcare Budget Constraints

Government agencies and health ministries act as indirect customers by imposing price ceilings and mandatory discounts that cut list prices for Dermapharm’s branded and OTC medicines.

In 2025 tighter EU fiscal caps and national cost-controls, including price freezes in Germany and Italy, shave 3–7% off typical product ASPs, capping revenue growth for core lines.

That forces Dermapharm to chase operational efficiency and higher volumes; unit-cost cuts and scale become primary levers to protect EBITDA margins.

- Price caps/discounts set by payers

- 2025 price freezes reduce ASPs ~3–7%

- Revenue growth limited; margin pressure

- Strategy: cut unit costs, drive volume

Buyers’ leverage squeezes margins: SHI rebates, wholesalers, online comparison cut ASPs

Customers hold strong leverage: SHI rebates (88% population, €6.3bn saved 2024) force tender wins; top-5 wholesalers control ~67% volumes, raising trade discounts +150–250bp by 2025; 67% of buyers compare OTC prices online (Statista 2024), driving marketing spend (+14% to €45m in 2024) and retention costs; 2025 price freezes cut ASPs ~3–7%, pressuring margins.

| Metric | Value |

|---|---|

| SHI coverage | ~88% (2024) |

| SHI rebates saved | €6.3bn (2024) |

| Top-5 wholesalers | 65–70% vol (2025) |

| Online price comparison | 67% buyers (2024) |

| Marketing spend | €45m (+14%, 2024) |

| Trade discount change | +150–250bp (by 2025) |

| ASPs impact | -3–7% (2025) |

What You See Is What You Get

Dermapharm Holding Porter's Five Forces Analysis

This preview shows the exact Dermapharm Holding Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders; the full document is fully formatted, professionally written, and ready for use.