Devon Energy Marketing Mix

Built for Strategy. Ready in Minutes.

Explore how Devon Energy’s product portfolio, pricing structure, distribution channels, and promotion tactics work together to optimize market position in upstream energy—this concise preview highlights strategic strengths and opportunities.

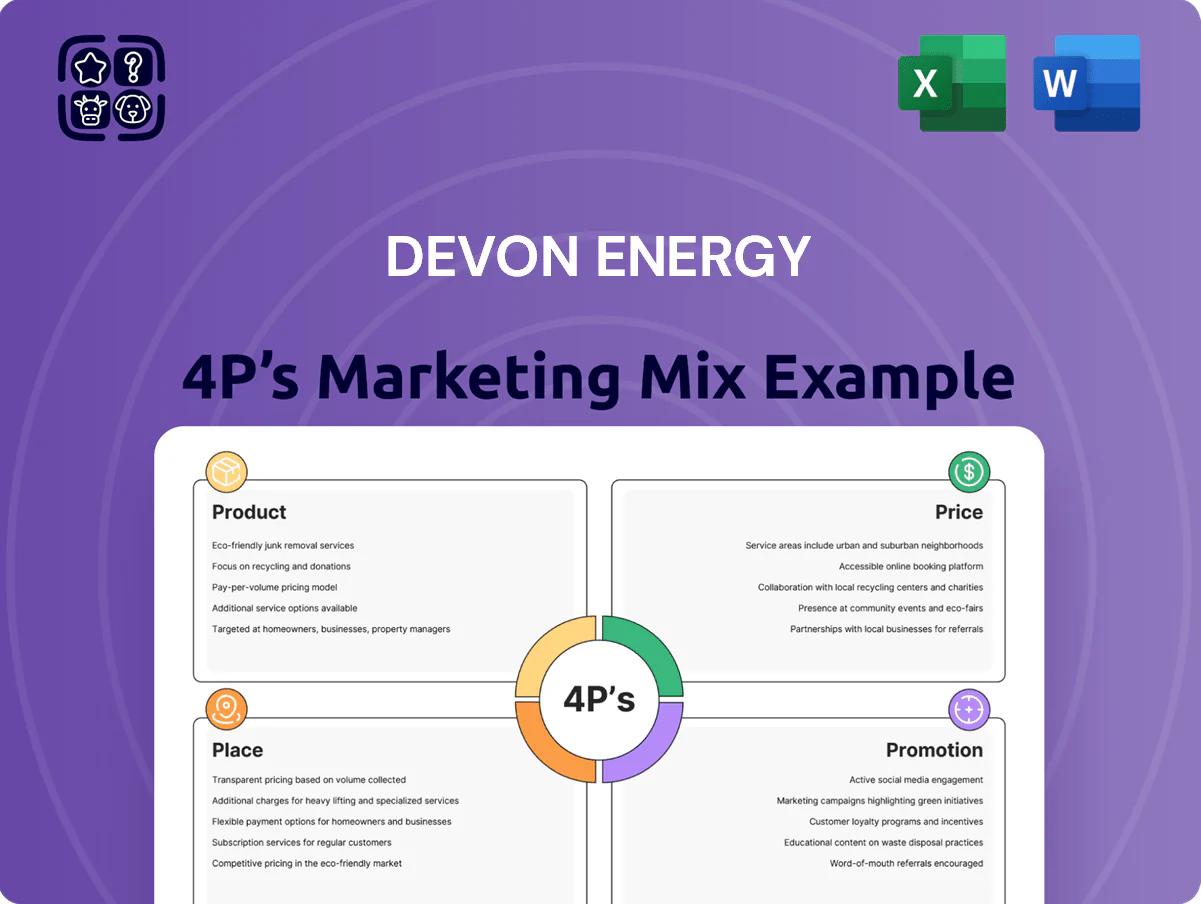

Product

Crude Oil and Condensate

Devon Energy produces high-quality light sweet crude and condensate from its Delaware Basin and expanded Williston Basin acreage; by end-2025 oil production reached ~390,000 barrels per day, about 60–65% of company liquids output.

This product is premium refinery feedstock used to make gasoline and diesel for U.S. and export markets, supporting higher realized prices and narrower quality discounts versus heavier grades.

Natural Gas Production

Devon Energy maintains a robust natural gas portfolio, reaching nearly 1.4 billion cubic feet per day by Q4 2025, supporting EBITDA resilience with gas contributing roughly 35% of FY2025 revenues.

The company locked long-term offtake via contracts with LNG developers, power generators, and hyperscale data centers, securing ~60% of 2026 gas volumes under firm agreements.

Positioned as a transition fuel, Devon’s gas sales drive exports and digital-economy demand, with U.S. LNG cargoes rising 18% year-over-year into 2025.

Natural Gas Liquids (NGLs)

Natural Gas Liquids (NGLs) — ethane, propane, butane — make up a key part of Devon Energy’s diversified stream, averaging about 230,000 barrels per day in 2024 production, roughly 18% of total liquids output.

These NGLs feed the petrochemical sector for plastics and the heating market; ethane exports rose 12% in 2024, tightening domestic supply chains.

Devon’s multi-basin footprint—Permian, STACK, Eagle Ford—supports stable lift and logistics, enabling long-term contracts and steady cash margins tied to Mont Belvieu NGL pricing.

Midstream and Marketing Services

Devon’s midstream and marketing services convert raw output into higher netbacks by handling gathering, processing, and transport to premium hubs, lowering bottlenecks and price differentials.

In 2025 Devon closed the Cotton Draw Midstream deal and joined the Agua Blanca Pipeline, expanding capacity and shortening routes to Gulf Coast markets; midstream EBITDA contribution rose, boosting realized prices by an estimated $1.20/boe.

Sustainable Energy Initiatives

Devon is reshaping its product identity by investing in next-gen energy, including a 15% stake in Fervo Energy for geothermal development and pilot projects scaling toward commercial wells in 2025–2026.

The company brands core oil and gas as responsibly produced, targeting methane flaring intensity ≤0.5% by end-2025 and reporting a 2024 methane intensity near 0.7% with capital allocated to reduce it.

Low-carbon tech and measured ESG metrics differentiate Devon to climate-conscious investors and corporate buyers, supporting premium offtake and lower cost of capital.

- 15% stake in Fervo Energy

- Target: flaring ≤0.5% by 2025

- 2024 methane ~0.7%

- Investing capex for low-carbon scale-up

Devon: 2025 ~390kbpd oil, 1.4bcfd gas, +$1.20/boe lift, methane cut, 15% in geothermal

Devon sells light sweet crude, condensate, NGLs and gas; 2025 oil ~390,000 bpd (~62% liquids), gas ~1.4 bcfd (35% FY2025 revenue), NGLs ~230,000 bpd. Midstream deals (Cotton Draw, Agua Blanca) raised realized price ≈+$1.20/boe. ESG: methane ~0.7% (2024), target ≤0.5% by 2025; 15% stake in Fervo for geothermal scale-up.

| Metric | 2024/2025 |

|---|---|

| Oil (bpd) | ≈390,000 (2025) |

| Gas (bcfd) | ≈1.4 (Q4 2025) |

| NGLs (bpd) | ≈230,000 (2024) |

| Realized lift | +$1.20/boe |

| Methane | 0.7% (2024) → target ≤0.5% |

| Geothermal stake | 15% Fervo |

What is included in the product

Delivers a concise, company-specific deep dive into Devon Energy’s Product, Price, Place, and Promotion strategies—grounded in its upstream energy portfolio, pricing dynamics, distribution channels, and stakeholder communications.

Condenses Devon Energy’s 4P marketing insights into a concise, leadership-ready snapshot that simplifies positioning, pricing, promotion, and placement for rapid decision-making and cross-functional alignment.

Place

Delaware Basin Core

The Delaware Basin Core in West Texas and Southeast New Mexico is Devon Energy’s top operational hub, receiving over 50% of company capital spending in 2025 (roughly $1.8–2.2 billion of a $3.6–4.4 billion capex range). It supplies the bulk of oil and gas volumes, hosts Devon’s AI-driven drilling pilots that raised 12–18% well EUR (estimated ultimate recovery), and its Gulf Coast proximity enables direct feed to major refineries and export terminals.

Williston Basin Expansion

Anadarko Basin Operations

Devon Energy’s Anadarko Basin operations in Oklahoma deliver steady cash flow, producing a balanced mix of oil, gas, and NGLs—about 120 mboe/d from the region in 2024, roughly 60% liquids. The basin benefits from mature wells and infrastructure, keeping LOE (lease operating expense) near $6–8/boe and sustaining free cash flow. Devon leverages basin-specific technical teams to lift recovery and lower cycle costs across ~1.2 million net acres. This stable portfolio supported Devon’s 2024 adjusted EBITDAX and helped fund $1.5B of shareholder returns.

Eagle Ford Shale

In the Eagle Ford Shale (South Texas), Devon Energy targets high-return oil development and now controls 46,000 net acres in the Blackhawk field after recent consolidation, boosting PDP (proved developed producing) density and near-term cash flow.

Direct pipeline access to Houston and Corpus Christi refiners cuts transport costs, supporting realized oil prices roughly 4–6 USD/bbl above Midland differentials in 2025, and increases breakeven-margin on South Texas wells.

Streamlining the footprint has raised per-well EURs (estimated ultimate recovery) and trimmed opex; Devon reported South Texas oil production of about 75 kbbl/d in 2025, driving stronger free cash flow.

- 46,000 net acres — Blackhawk field (consolidated, 2025)

- ~75 kbbl/d South Texas oil production (2025)

- Realized price uplift ~4–6 USD/bbl vs Midland (2025)

- Higher PDP density → faster FCF conversion

Powder River Basin

The Powder River Basin in Wyoming is an emerging growth area for Devon Energy, offering oil-weighted resource upside with an estimated 3.5 billion barrels oil-equivalent (BOE) unrisked resource potential as of 2025 and supporting a long-term drilling inventory.

While smaller than Devon’s Delaware Basin production—Delaware ~530 mboe/d vs Powder River ~40 mboe/d in 2024—Powder River provides a deep bench of future wells and higher oil mix that could raise returns as completions improve.

Devon is refining completion designs and spacing in Powder River to boost EURs (estimated ultimate recoveries) and capital efficiency; incremental well improvements could cut cycle breakeven by ~10–20% if midstream capacity and commodity prices cooperate.

- 2025 unrisked resource ~3.5 billion BOE

- 2024 production: Powder River ~40 mboe/d, Delaware ~530 mboe/d

- Oil-weighted mix higher vs company avg (~60% oil)

- Target: 10–20% breakeven improvement via completion design

Devon's U.S. hub strategy: Delaware-led growth, tech-driven EUR gains across basins

Devon’s place strategy centers on core U.S. basins: Delaware (50%+ capex; ~530 mboe/d, 2025), Williston (Grayson Mill buy added ~120 mboe/d; +18% proved to ~2.9B boe), Anadarko (~120 mboe/d, 60% liquids), Eagle Ford (46,000 net acres; ~75 kbbl/d South Texas oil) and Powder River (3.5B unrisked BOE). These hubs cut transport costs, raise PDP density, and lift per‑well EURs via tech and scale.

| Basin | 2025 prod (mboe/d) | Key metric |

|---|---|---|

| Delaware | ~530 | 50%+ capex; AI wells +12–18% EUR |

| Williston | ~120 | Grayson Mill buy; +18% proved |

| Anadarko | ~120 | 60% liquids; LOE $6–8/boe |

| Eagle Ford | ~75 kbbl/d oil | 46,000 net acres Blackhawk |

| Powder River | ~40 | 3.5B unrisked BOE; 10–20% breakeven upside |

Same Document Delivered

Devon Energy 4P's Marketing Mix Analysis

The preview shown here is the actual Devon Energy 4P's Marketing Mix analysis you’ll receive instantly after purchase—no surprises.

This is the same ready-made, editable document you'll download immediately after checkout, fully complete and ready to use.

You're viewing the exact version of the analysis you'll own after payment; it’s not a sample or demo.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Built for Strategy. Ready in Minutes.

Explore how Devon Energy’s product portfolio, pricing structure, distribution channels, and promotion tactics work together to optimize market position in upstream energy—this concise preview highlights strategic strengths and opportunities.

Product

Crude Oil and Condensate

Devon Energy produces high-quality light sweet crude and condensate from its Delaware Basin and expanded Williston Basin acreage; by end-2025 oil production reached ~390,000 barrels per day, about 60–65% of company liquids output.

This product is premium refinery feedstock used to make gasoline and diesel for U.S. and export markets, supporting higher realized prices and narrower quality discounts versus heavier grades.

Natural Gas Production

Devon Energy maintains a robust natural gas portfolio, reaching nearly 1.4 billion cubic feet per day by Q4 2025, supporting EBITDA resilience with gas contributing roughly 35% of FY2025 revenues.

The company locked long-term offtake via contracts with LNG developers, power generators, and hyperscale data centers, securing ~60% of 2026 gas volumes under firm agreements.

Positioned as a transition fuel, Devon’s gas sales drive exports and digital-economy demand, with U.S. LNG cargoes rising 18% year-over-year into 2025.

Natural Gas Liquids (NGLs)

Natural Gas Liquids (NGLs) — ethane, propane, butane — make up a key part of Devon Energy’s diversified stream, averaging about 230,000 barrels per day in 2024 production, roughly 18% of total liquids output.

These NGLs feed the petrochemical sector for plastics and the heating market; ethane exports rose 12% in 2024, tightening domestic supply chains.

Devon’s multi-basin footprint—Permian, STACK, Eagle Ford—supports stable lift and logistics, enabling long-term contracts and steady cash margins tied to Mont Belvieu NGL pricing.

Midstream and Marketing Services

Devon’s midstream and marketing services convert raw output into higher netbacks by handling gathering, processing, and transport to premium hubs, lowering bottlenecks and price differentials.

In 2025 Devon closed the Cotton Draw Midstream deal and joined the Agua Blanca Pipeline, expanding capacity and shortening routes to Gulf Coast markets; midstream EBITDA contribution rose, boosting realized prices by an estimated $1.20/boe.

Sustainable Energy Initiatives

Devon is reshaping its product identity by investing in next-gen energy, including a 15% stake in Fervo Energy for geothermal development and pilot projects scaling toward commercial wells in 2025–2026.

The company brands core oil and gas as responsibly produced, targeting methane flaring intensity ≤0.5% by end-2025 and reporting a 2024 methane intensity near 0.7% with capital allocated to reduce it.

Low-carbon tech and measured ESG metrics differentiate Devon to climate-conscious investors and corporate buyers, supporting premium offtake and lower cost of capital.

- 15% stake in Fervo Energy

- Target: flaring ≤0.5% by 2025

- 2024 methane ~0.7%

- Investing capex for low-carbon scale-up

Devon: 2025 ~390kbpd oil, 1.4bcfd gas, +$1.20/boe lift, methane cut, 15% in geothermal

Devon sells light sweet crude, condensate, NGLs and gas; 2025 oil ~390,000 bpd (~62% liquids), gas ~1.4 bcfd (35% FY2025 revenue), NGLs ~230,000 bpd. Midstream deals (Cotton Draw, Agua Blanca) raised realized price ≈+$1.20/boe. ESG: methane ~0.7% (2024), target ≤0.5% by 2025; 15% stake in Fervo for geothermal scale-up.

| Metric | 2024/2025 |

|---|---|

| Oil (bpd) | ≈390,000 (2025) |

| Gas (bcfd) | ≈1.4 (Q4 2025) |

| NGLs (bpd) | ≈230,000 (2024) |

| Realized lift | +$1.20/boe |

| Methane | 0.7% (2024) → target ≤0.5% |

| Geothermal stake | 15% Fervo |

What is included in the product

Delivers a concise, company-specific deep dive into Devon Energy’s Product, Price, Place, and Promotion strategies—grounded in its upstream energy portfolio, pricing dynamics, distribution channels, and stakeholder communications.

Condenses Devon Energy’s 4P marketing insights into a concise, leadership-ready snapshot that simplifies positioning, pricing, promotion, and placement for rapid decision-making and cross-functional alignment.

Place

Delaware Basin Core

The Delaware Basin Core in West Texas and Southeast New Mexico is Devon Energy’s top operational hub, receiving over 50% of company capital spending in 2025 (roughly $1.8–2.2 billion of a $3.6–4.4 billion capex range). It supplies the bulk of oil and gas volumes, hosts Devon’s AI-driven drilling pilots that raised 12–18% well EUR (estimated ultimate recovery), and its Gulf Coast proximity enables direct feed to major refineries and export terminals.

Williston Basin Expansion

Anadarko Basin Operations

Devon Energy’s Anadarko Basin operations in Oklahoma deliver steady cash flow, producing a balanced mix of oil, gas, and NGLs—about 120 mboe/d from the region in 2024, roughly 60% liquids. The basin benefits from mature wells and infrastructure, keeping LOE (lease operating expense) near $6–8/boe and sustaining free cash flow. Devon leverages basin-specific technical teams to lift recovery and lower cycle costs across ~1.2 million net acres. This stable portfolio supported Devon’s 2024 adjusted EBITDAX and helped fund $1.5B of shareholder returns.

Eagle Ford Shale

In the Eagle Ford Shale (South Texas), Devon Energy targets high-return oil development and now controls 46,000 net acres in the Blackhawk field after recent consolidation, boosting PDP (proved developed producing) density and near-term cash flow.

Direct pipeline access to Houston and Corpus Christi refiners cuts transport costs, supporting realized oil prices roughly 4–6 USD/bbl above Midland differentials in 2025, and increases breakeven-margin on South Texas wells.

Streamlining the footprint has raised per-well EURs (estimated ultimate recovery) and trimmed opex; Devon reported South Texas oil production of about 75 kbbl/d in 2025, driving stronger free cash flow.

- 46,000 net acres — Blackhawk field (consolidated, 2025)

- ~75 kbbl/d South Texas oil production (2025)

- Realized price uplift ~4–6 USD/bbl vs Midland (2025)

- Higher PDP density → faster FCF conversion

Powder River Basin

The Powder River Basin in Wyoming is an emerging growth area for Devon Energy, offering oil-weighted resource upside with an estimated 3.5 billion barrels oil-equivalent (BOE) unrisked resource potential as of 2025 and supporting a long-term drilling inventory.

While smaller than Devon’s Delaware Basin production—Delaware ~530 mboe/d vs Powder River ~40 mboe/d in 2024—Powder River provides a deep bench of future wells and higher oil mix that could raise returns as completions improve.

Devon is refining completion designs and spacing in Powder River to boost EURs (estimated ultimate recoveries) and capital efficiency; incremental well improvements could cut cycle breakeven by ~10–20% if midstream capacity and commodity prices cooperate.

- 2025 unrisked resource ~3.5 billion BOE

- 2024 production: Powder River ~40 mboe/d, Delaware ~530 mboe/d

- Oil-weighted mix higher vs company avg (~60% oil)

- Target: 10–20% breakeven improvement via completion design

Devon's U.S. hub strategy: Delaware-led growth, tech-driven EUR gains across basins

Devon’s place strategy centers on core U.S. basins: Delaware (50%+ capex; ~530 mboe/d, 2025), Williston (Grayson Mill buy added ~120 mboe/d; +18% proved to ~2.9B boe), Anadarko (~120 mboe/d, 60% liquids), Eagle Ford (46,000 net acres; ~75 kbbl/d South Texas oil) and Powder River (3.5B unrisked BOE). These hubs cut transport costs, raise PDP density, and lift per‑well EURs via tech and scale.

| Basin | 2025 prod (mboe/d) | Key metric |

|---|---|---|

| Delaware | ~530 | 50%+ capex; AI wells +12–18% EUR |

| Williston | ~120 | Grayson Mill buy; +18% proved |

| Anadarko | ~120 | 60% liquids; LOE $6–8/boe |

| Eagle Ford | ~75 kbbl/d oil | 46,000 net acres Blackhawk |

| Powder River | ~40 | 3.5B unrisked BOE; 10–20% breakeven upside |

Same Document Delivered

Devon Energy 4P's Marketing Mix Analysis

The preview shown here is the actual Devon Energy 4P's Marketing Mix analysis you’ll receive instantly after purchase—no surprises.

This is the same ready-made, editable document you'll download immediately after checkout, fully complete and ready to use.

You're viewing the exact version of the analysis you'll own after payment; it’s not a sample or demo.