DFS Furniture PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic pressures, and technological trends are reshaping DFS Furniture’s market position—our concise PESTLE highlights the key external forces you need to know. Ideal for investors and strategists, the full report delivers actionable insights and ready-to-use charts to inform decisions. Purchase the complete PESTLE now for a deep, editable analysis you can apply immediately.

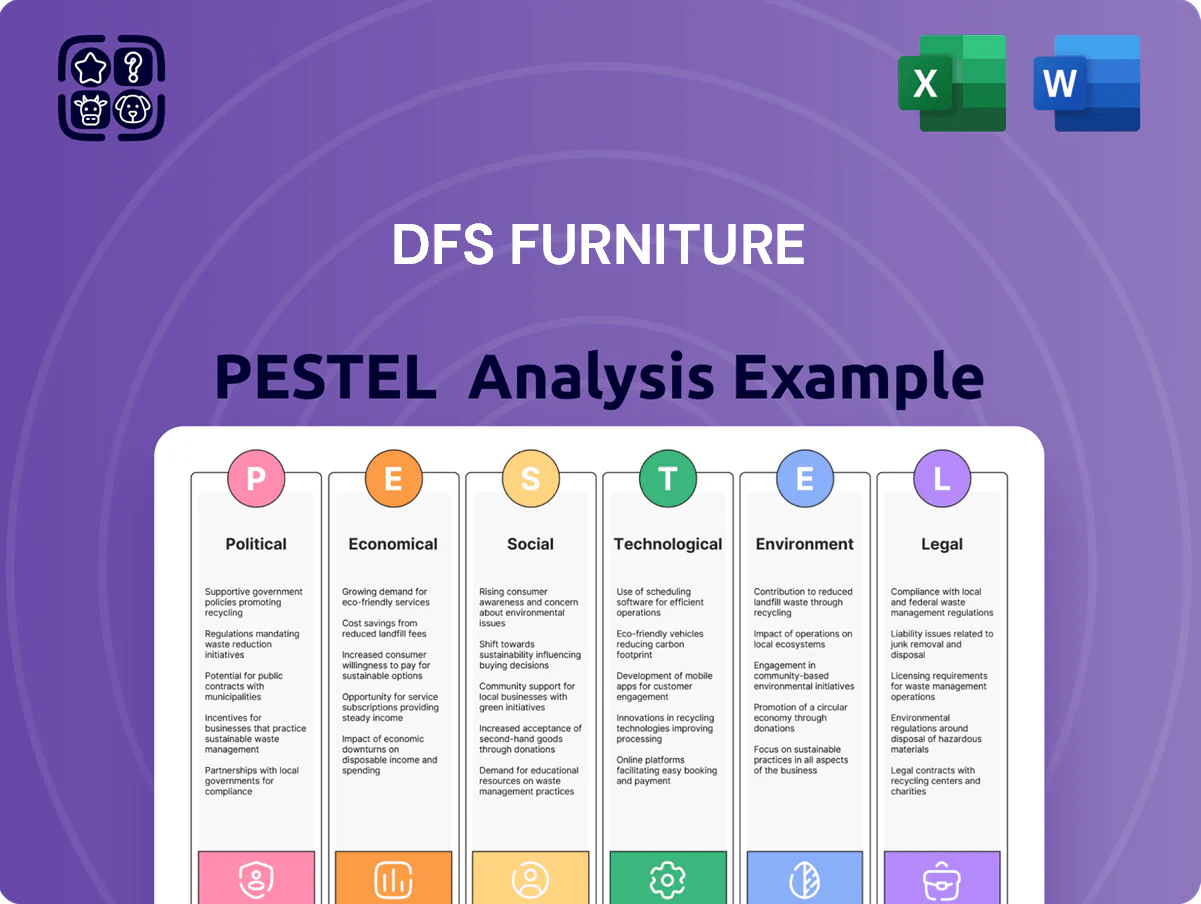

Political factors

Trade Agreement Stability

UK-EU trade relations remain pivotal for DFS, which in 2024 sourced roughly 28% of components from EU suppliers; any regulatory divergence could raise cross-border costs by an estimated 4–7% and add administrative delays. Continued alignment through late 2025 would help stabilise average UK-to-Spain/Netherlands lead times—currently ~12–18 days—reducing variability and inventory carrying costs.

Housing Market Policies

Government housing incentives shape sofa demand: UK first-time buyer schemes and Help to Buy-style grants can boost moves and correlate with higher upholstery orders—ONS data show UK housing transactions rose 8.7% in 2024 vs 2023 after stimulus; new-build completions reached ~210,000 in 2024, up 5%, signaling inventory needs. DFS should track planning reform outcomes and monthly HM Land Registry transactions to align marketing and stock with projected completions.

International Relations

Geopolitical tensions—notably Red Sea disruptions and South China Sea frictions—have pushed global shipping rates up 18% year-on-year in 2024, raising landed costs for DFS by an estimated 2–3% of COGS. Political instability in manufacturing hubs like Vietnam and Sri Lanka has caused freight surges and delays, with container dwell times up 22% in hotspots. Maintaining a diversified supplier base across SE Asia and Eastern Europe is essential to limit exposure to sudden spikes through 2026.

Customs and Border Regulations

Import tariffs on timber and specialized fabrics from non-EU regions—averaging 3–7% for timber and up to 12% for some upholstery textiles in 2024—can erode DFS’s margin and price competitiveness on UK sales.

With trade policy shifts through 2025 and occasional protectionist proposals, production costs could rise by an estimated 1–3% annually if tariffs or compliance costs increase.

Active lobbying and membership in bodies like the British Furniture Manufacturers Association and UK Trade & Investment enable DFS to forecast changes and potentially secure tariff relief or preferential terms.

- 2024 tariffs: timber 3–7%, textiles up to 12%

- Potential cost impact 2024–25: +1–3% production costs

- Mitigation: lobbying, trade body engagement

Tax and Fiscal Policy

Local political stability in the Netherlands and Spain shapes DFS Furniture’s international operations; the Netherlands ranked 8th and Spain 25th on the 2024 Global Peace Index, influencing supply-chain predictability and expansion costs.

Divergent regional rules on retail hours and business taxes—municipal levies up to 3% in parts of Spain versus Dutch local surcharges—require tailored management and pricing.

Monitoring local elections and policy shifts (e.g., 2024 municipal cycles) keeps DFS compliant and competitive.

- Netherlands GPI rank 8 (2024)

- Spain GPI rank 25 (2024)

- Local business levies up to 3% in regions of Spain

- 2024 municipal elections heighten policy risk

Trade, tariffs and shipping squeeze margins amid housing-led furniture demand surge

Political factors: UK-EU trade stability affects ~28% EU-sourced components, potential 4–7% cross-border cost uplift; 2024 housing stimulus lifted transactions +8.7% supporting sofa demand; 2024 shipping/political disruptions raised landed costs ~2–3% COGS; tariffs timber 3–7%, textiles up to 12% (2024) — lobbying and supplier diversification mitigate risks.

| Metric | 2024 Value |

|---|---|

| EU sourcing | 28% |

| Housing txns change | +8.7% |

| Shipping cost rise | +18% |

| Tariffs (timber/textiles) | 3–7% / up to 12% |

What is included in the product

Explores how macro-environmental forces uniquely impact DFS Furniture across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to reveal threats and opportunities.

A concise PESTLE snapshot that clarifies external risks and opportunities for DFS Furniture, ideal for dropping into presentations or sharing across teams to speed strategic alignment and support planning discussions.

Economic factors

Interest Rate Fluctuations

High interest rates in the mid-2020s, with UK base rate peaking at 5.25% in 2023-24 and average household borrowing costs near 6% in 2024, suppressed demand for big-ticket credit purchases like sofas.

If Bank of England guidance leads to easing toward ~4% by late 2025, consumer appetite for interest-free credit is likely to recover, potentially lifting DFS sales volumes.

DFS’s capacity to subsidise or securitise attractive financing—interest-free plans accounted for ~30% of transactions in 2023—remains central to maintaining its middle-market value proposition.

Disposable Income Levels

Real wage growth remained modest at about 1.2% in 2025 UK CPI-adjusted terms, constraining disposable income and reducing frequency of discretionary home-improvement purchases.

Inflation fell to 3.4% by Dec 2025 from a 2022 peak, but cumulative real-income erosion means many households postpone major furniture replacements.

DFS leverages tiered pricing—entry sofas from ~£299 to premium ranges >£2,000—to capture budget-conscious buyers and higher-margin premium seekers.

Raw Material Inflation

Raw material inflation for DFS remains acute as timber, polyurethane foam and upholstery fabrics rose 14-22% globally in 2024, pressuring gross margins that were 32.1% in FY2024; passing costs risks ceding share to discount chains. Volatility in commodity indexes (timber +18% YoY to end-2024) forces DFS to pursue lean manufacturing, yield improvements and multi-year supplier contracts—over 60% of key inputs now hedged—to protect EBITDA.

Currency Exchange Volatility

Currency volatility between GBP, EUR and USD influences DFS through import costs and FX translation; a 10% fall in the Pound versus the Dollar in 2023 raised UK retail import costs by an estimated 6–8% for comparable furniture components.

With global sourcing, a weaker Pound can lift cost of sales materially unless hedged; DFS reported using forwards and options covering roughly 60–80% of near-term exposures in 2024.

These hedging programs help stabilize consumer pricing and protect reported international earnings—FX translation swung DFS adjusted pre-tax profit by circa 4–5% in 2022–24.

- 10% GBP decline → ~6–8% higher import costs

- 60–80% of short-term FX exposure hedged (2024)

- FX translation affected pre-tax profit by ~4–5% (2022–24)

Labor Market Costs

Labor market tightness across the UK and EU raised average manufacturing wage costs by ~6% YoY in 2024, squeezing margins and slowing delivery times as driver and warehouse vacancies stayed ~15% above pre‑pandemic levels.

Rising minimum wages (UK National Living Wage up 9.7% since 2022 to £11.44 in 2024) and premium pay for skilled upholsterers increase DFS’s recruitment and retention spend, with sector pay premiums of 10–25% reported in 2024.

DFS must offset higher labour expenses through productivity gains—automation, route optimisation and training—to preserve EBIT margins; a 3–5% productivity uplift could materially counter a 6% wage rise.

- UK wage inflation ~6% (2024)

- National Living Wage £11.44 (2024)

- Driver/warehouse vacancies ~15% above pre‑pandemic (2024)

- Skilled upholsterer pay premium 10–25% (2024)

- Required productivity uplift ~3–5% to offset wage rises

Higher rates, cost inflation and FX swings squeeze margins despite hedging

Higher borrowing costs (BoE peak 5.25% 2023; avg household rates ~6% 2024) and muted real wages (~1.2% 2025) depressed big-ticket demand; raw-material inflation (+14–22% 2024) and 6% wage inflation squeezed margins (gross margin 32.1% FY2024). FX moves (10% GBP fall → ~6–8% import cost rise) and hedging (60–80% cover) partly stabilized earnings (FX swung pre-tax ~4–5%).

| Metric | Value |

|---|---|

| BoE peak | 5.25% (2023) |

| Household borrowing | ~6% (2024) |

| Wage inflation | ~6% (2024) |

| Raw material rise | 14–22% (2024) |

| Gross margin | 32.1% (FY2024) |

| FX hedged | 60–80% (2024) |

Full Version Awaits

DFS Furniture PESTLE Analysis

The preview shown here is the exact DFS Furniture PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use, with no placeholders or teasers.

The layout, content, and structure visible in this preview are identical to the downloadable file you’ll get immediately after checkout, professionally structured for immediate application.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic pressures, and technological trends are reshaping DFS Furniture’s market position—our concise PESTLE highlights the key external forces you need to know. Ideal for investors and strategists, the full report delivers actionable insights and ready-to-use charts to inform decisions. Purchase the complete PESTLE now for a deep, editable analysis you can apply immediately.

Political factors

Trade Agreement Stability

UK-EU trade relations remain pivotal for DFS, which in 2024 sourced roughly 28% of components from EU suppliers; any regulatory divergence could raise cross-border costs by an estimated 4–7% and add administrative delays. Continued alignment through late 2025 would help stabilise average UK-to-Spain/Netherlands lead times—currently ~12–18 days—reducing variability and inventory carrying costs.

Housing Market Policies

Government housing incentives shape sofa demand: UK first-time buyer schemes and Help to Buy-style grants can boost moves and correlate with higher upholstery orders—ONS data show UK housing transactions rose 8.7% in 2024 vs 2023 after stimulus; new-build completions reached ~210,000 in 2024, up 5%, signaling inventory needs. DFS should track planning reform outcomes and monthly HM Land Registry transactions to align marketing and stock with projected completions.

International Relations

Geopolitical tensions—notably Red Sea disruptions and South China Sea frictions—have pushed global shipping rates up 18% year-on-year in 2024, raising landed costs for DFS by an estimated 2–3% of COGS. Political instability in manufacturing hubs like Vietnam and Sri Lanka has caused freight surges and delays, with container dwell times up 22% in hotspots. Maintaining a diversified supplier base across SE Asia and Eastern Europe is essential to limit exposure to sudden spikes through 2026.

Customs and Border Regulations

Import tariffs on timber and specialized fabrics from non-EU regions—averaging 3–7% for timber and up to 12% for some upholstery textiles in 2024—can erode DFS’s margin and price competitiveness on UK sales.

With trade policy shifts through 2025 and occasional protectionist proposals, production costs could rise by an estimated 1–3% annually if tariffs or compliance costs increase.

Active lobbying and membership in bodies like the British Furniture Manufacturers Association and UK Trade & Investment enable DFS to forecast changes and potentially secure tariff relief or preferential terms.

- 2024 tariffs: timber 3–7%, textiles up to 12%

- Potential cost impact 2024–25: +1–3% production costs

- Mitigation: lobbying, trade body engagement

Tax and Fiscal Policy

Local political stability in the Netherlands and Spain shapes DFS Furniture’s international operations; the Netherlands ranked 8th and Spain 25th on the 2024 Global Peace Index, influencing supply-chain predictability and expansion costs.

Divergent regional rules on retail hours and business taxes—municipal levies up to 3% in parts of Spain versus Dutch local surcharges—require tailored management and pricing.

Monitoring local elections and policy shifts (e.g., 2024 municipal cycles) keeps DFS compliant and competitive.

- Netherlands GPI rank 8 (2024)

- Spain GPI rank 25 (2024)

- Local business levies up to 3% in regions of Spain

- 2024 municipal elections heighten policy risk

Trade, tariffs and shipping squeeze margins amid housing-led furniture demand surge

Political factors: UK-EU trade stability affects ~28% EU-sourced components, potential 4–7% cross-border cost uplift; 2024 housing stimulus lifted transactions +8.7% supporting sofa demand; 2024 shipping/political disruptions raised landed costs ~2–3% COGS; tariffs timber 3–7%, textiles up to 12% (2024) — lobbying and supplier diversification mitigate risks.

| Metric | 2024 Value |

|---|---|

| EU sourcing | 28% |

| Housing txns change | +8.7% |

| Shipping cost rise | +18% |

| Tariffs (timber/textiles) | 3–7% / up to 12% |

What is included in the product

Explores how macro-environmental forces uniquely impact DFS Furniture across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to reveal threats and opportunities.

A concise PESTLE snapshot that clarifies external risks and opportunities for DFS Furniture, ideal for dropping into presentations or sharing across teams to speed strategic alignment and support planning discussions.

Economic factors

Interest Rate Fluctuations

High interest rates in the mid-2020s, with UK base rate peaking at 5.25% in 2023-24 and average household borrowing costs near 6% in 2024, suppressed demand for big-ticket credit purchases like sofas.

If Bank of England guidance leads to easing toward ~4% by late 2025, consumer appetite for interest-free credit is likely to recover, potentially lifting DFS sales volumes.

DFS’s capacity to subsidise or securitise attractive financing—interest-free plans accounted for ~30% of transactions in 2023—remains central to maintaining its middle-market value proposition.

Disposable Income Levels

Real wage growth remained modest at about 1.2% in 2025 UK CPI-adjusted terms, constraining disposable income and reducing frequency of discretionary home-improvement purchases.

Inflation fell to 3.4% by Dec 2025 from a 2022 peak, but cumulative real-income erosion means many households postpone major furniture replacements.

DFS leverages tiered pricing—entry sofas from ~£299 to premium ranges >£2,000—to capture budget-conscious buyers and higher-margin premium seekers.

Raw Material Inflation

Raw material inflation for DFS remains acute as timber, polyurethane foam and upholstery fabrics rose 14-22% globally in 2024, pressuring gross margins that were 32.1% in FY2024; passing costs risks ceding share to discount chains. Volatility in commodity indexes (timber +18% YoY to end-2024) forces DFS to pursue lean manufacturing, yield improvements and multi-year supplier contracts—over 60% of key inputs now hedged—to protect EBITDA.

Currency Exchange Volatility

Currency volatility between GBP, EUR and USD influences DFS through import costs and FX translation; a 10% fall in the Pound versus the Dollar in 2023 raised UK retail import costs by an estimated 6–8% for comparable furniture components.

With global sourcing, a weaker Pound can lift cost of sales materially unless hedged; DFS reported using forwards and options covering roughly 60–80% of near-term exposures in 2024.

These hedging programs help stabilize consumer pricing and protect reported international earnings—FX translation swung DFS adjusted pre-tax profit by circa 4–5% in 2022–24.

- 10% GBP decline → ~6–8% higher import costs

- 60–80% of short-term FX exposure hedged (2024)

- FX translation affected pre-tax profit by ~4–5% (2022–24)

Labor Market Costs

Labor market tightness across the UK and EU raised average manufacturing wage costs by ~6% YoY in 2024, squeezing margins and slowing delivery times as driver and warehouse vacancies stayed ~15% above pre‑pandemic levels.

Rising minimum wages (UK National Living Wage up 9.7% since 2022 to £11.44 in 2024) and premium pay for skilled upholsterers increase DFS’s recruitment and retention spend, with sector pay premiums of 10–25% reported in 2024.

DFS must offset higher labour expenses through productivity gains—automation, route optimisation and training—to preserve EBIT margins; a 3–5% productivity uplift could materially counter a 6% wage rise.

- UK wage inflation ~6% (2024)

- National Living Wage £11.44 (2024)

- Driver/warehouse vacancies ~15% above pre‑pandemic (2024)

- Skilled upholsterer pay premium 10–25% (2024)

- Required productivity uplift ~3–5% to offset wage rises

Higher rates, cost inflation and FX swings squeeze margins despite hedging

Higher borrowing costs (BoE peak 5.25% 2023; avg household rates ~6% 2024) and muted real wages (~1.2% 2025) depressed big-ticket demand; raw-material inflation (+14–22% 2024) and 6% wage inflation squeezed margins (gross margin 32.1% FY2024). FX moves (10% GBP fall → ~6–8% import cost rise) and hedging (60–80% cover) partly stabilized earnings (FX swung pre-tax ~4–5%).

| Metric | Value |

|---|---|

| BoE peak | 5.25% (2023) |

| Household borrowing | ~6% (2024) |

| Wage inflation | ~6% (2024) |

| Raw material rise | 14–22% (2024) |

| Gross margin | 32.1% (FY2024) |

| FX hedged | 60–80% (2024) |

Full Version Awaits

DFS Furniture PESTLE Analysis

The preview shown here is the exact DFS Furniture PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use, with no placeholders or teasers.

The layout, content, and structure visible in this preview are identical to the downloadable file you’ll get immediately after checkout, professionally structured for immediate application.