DGF Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

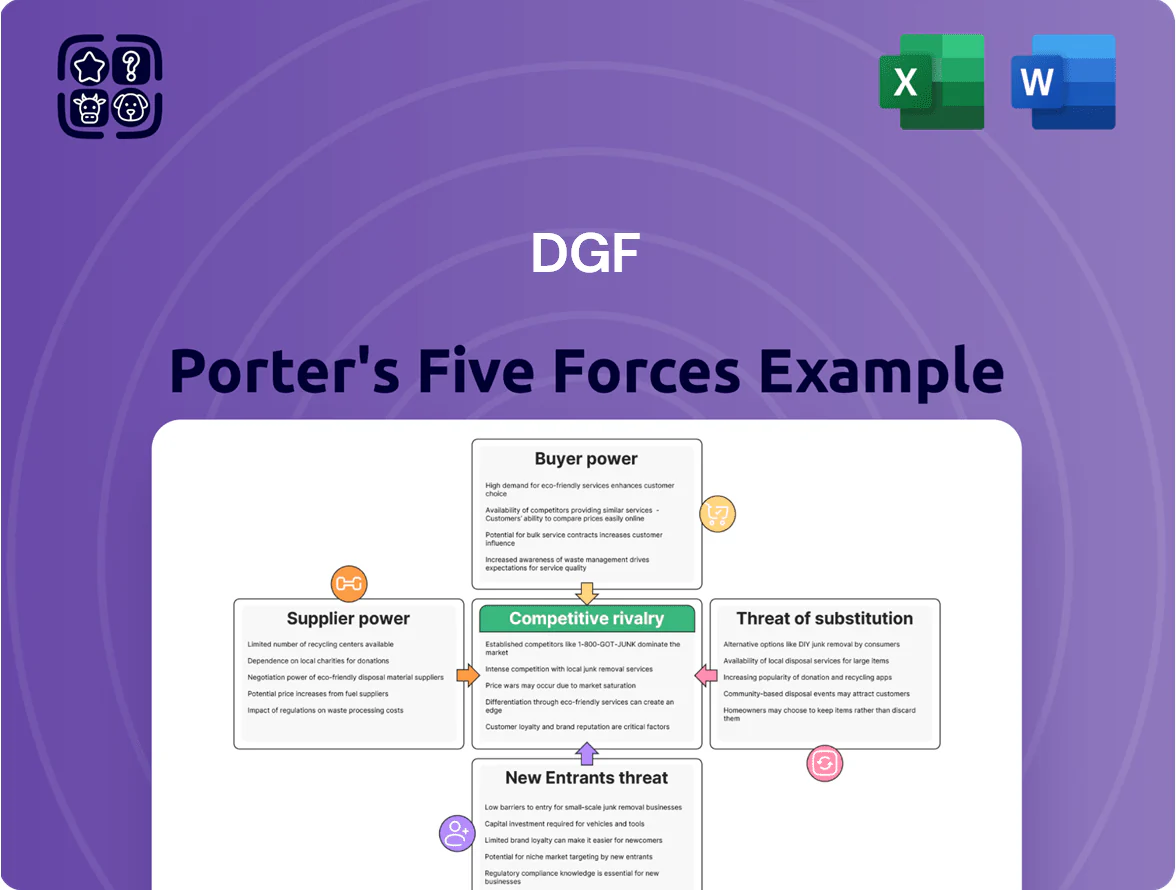

DGF’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, threat of entrants, and substitute pressures—revealing where strategic focus can create advantage. This brief only scratches the surface; unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable implications tailored to DGF to inform investment or strategy decisions.

Suppliers Bargaining Power

Fragmented raw material supply base

The global markets for flour, sugar, and dairy are highly fragmented—over 5,000 regional mills and processors in 2024—so no single supplier holds sway, keeping supplier power low for DGF.

DGF’s annual ingredient purchases of ~USD 120m let it secure 3–6% price rebates and switch suppliers quickly if costs or quality slip.

Still, premium pastry cocoa and couverture chocolate come from ~30 certified high-quality mills, raising supplier leverage slightly in those niches.

Commodity price volatility and supply chain risks

Suppliers of cocoa, nuts, and fats face climate shocks and geopolitics that caused 2023–25 price spikes—cocoa rose ~40% in 2023 and global edible oil prices were up ~22% by mid‑2024—pressures suppliers pass to buyers. DGF’s large procurement volumes give negotiating leverage, but it still absorbs macro shocks when spot prices jump. By end‑2025 tighter environmental rules increased supplier compliance costs, adding estimated 5–8% to input prices. This keeps supplier bargaining power elevated despite DGF’s scale.

Dependency on specialized equipment manufacturers

DGF depends on a small set of high-end bakery and chocolate machinery makers, whose proprietary tech and spare parts give them strong leverage; industry data shows 60–70% of industrial chocolate lines use vendor-specific components, raising switching costs and spare-parts margins. Keeping exclusive or preferred partnerships (DGF reported 18% equipment revenue growth in 2024 after securing two OEM agreements) is vital to protect service levels and pricing power.

Logistics and energy cost fluctuations

Rising energy prices and the shift to sustainable packaging raised suppliers’ leverage; global oil-related freight costs jumped ~40% in 2021–24 and biodegradable packaging premiums run 10–30% higher (2025 market data).

DGF’s reliance on temperature-controlled transport makes it captive to specialized logistics rates: cold-chain freight can cost 20–50% more than dry freight, directly lifting COGS and squeezing margins.

- Energy-driven freight +40% (2021–24)

- Sustainable packaging premium 10–30% (2025)

- Cold-chain cost premium 20–50%

- Secondary supplier layer increases COGS and margin pressure

Increasing importance of sustainability certifications

Suppliers with certified organic, fair-trade, or carbon-neutral labels gain bargaining power as 68% of global consumers say sustainability influences purchases (NielsenIQ, 2024), letting premium suppliers charge 10–25% higher prices.

DGF must secure certified inputs to meet pro clients’ marketing claims and avoid losing RFPs; lack of certification raises churn risk and can push contract terms to favor suppliers.

- 68% of consumers influenced by sustainability (NielsenIQ 2024)

- Premium price premium: 10–25%

- Certification needed to win RFPs from professional clients

Suppliers exert limited but rising pressure—commodity spikes, freight & packaging squeeze margins

Suppliers hold overall low-to-moderate power: DGF’s ~USD120m annual buys and fragmented flour/sugar/dairy markets limit leverage, but niche cocoa, specialized machinery, cold-chain logistics, and sustainability-certified inputs raise supplier bargaining power—price shocks (cocoa +40% in 2023), energy-driven freight +40% (2021–24), and 10–30% packaging premiums force DGF to absorb or hedge costs.

| Metric | Value |

|---|---|

| Annual procurement | USD120m |

| Cocoa spike | +40% (2023) |

| Freight rise | +40% (2021–24) |

| Packaging premium | 10–30% (2025) |

What is included in the product

Tailored Porter's Five Forces analysis for DGF that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats to inform strategic positioning and investor materials.

A concise Porter's Five Forces one-sheet for DGF—instantly highlights competitive pressures and strategic levers to speed boardroom decisions and scenario planning.

Customers Bargaining Power

Fragmented artisan customer base

High volume industrial buyer leverage

Large-scale industrial food producers and retail chains buy massive volumes and often secure discounts—top 20 retail chains accounted for ~40% of US grocery sales in 2024, so their bargaining clout is high.

These buyers run competitive bids across distributors to cut costs; a 2023 ProcureTech survey found 68% of manufacturers use multi-supplier tenders for ingredients.

DGF must match with superior technical support and integrated logistics; retaining a single high-volume account can represent 5–15% of distributor revenues, so service wins volume.

Low switching costs for commodity ingredients

For basic ingredients like sugar or butter, customers face low switching costs and will defect to cheaper distributors when price dominates—commodity buyers drove a 7% average margin compression in global wholesale food distribution in 2024. There is little brand loyalty for raw commodities, so this segment is highly price-sensitive and volatile.

DGF reduces that risk by bundling commodities with specialized ingredients and value-added training programs; in 2024 bundled contracts represented about 28% of DGF’s sales, lifting blended gross margins by ~210 basis points versus standalone commodity sales.

Value-added services as a retention tool

DGF’s expert technical support and training create psychological and professional switching costs—bakers relying on DGF for recipe development and staff training become dependent, lowering willingness to switch for small price cuts. In 2024 DGF reported training >3,200 chefs and a 12% higher retention rate among trained accounts, which reduces customer bargaining power by embedding recipe know-how and operational workflows.

- Training >3,200 chefs (2024)

- Trained accounts: +12% retention (2024)

- Recipe development ties procurement to DGF

- Increases switching cost despite price pressure

Access to digital procurement platforms

By late 2025, B2B e-commerce growth — global B2B digital sales reached about $22 trillion in 2024 — gave customers real-time price and supplier transparency, letting buyers compare DGF’s freight and logistics rates with international rivals instantly.

That visibility forces DGF to match competitive pricing and faster delivery; customers increasingly demand sub-2% price variances and 24–72 hour quote turnarounds, shifting bargaining power slightly toward buyers.

- Global B2B digital sales ~ $22T (2024)

- Buyers demand <2% price variance

- Typical quote turnaround 24–72 hrs

- Power shifted slightly to buyers by 2025

Mixed buyer power: artisans loyal but retailers dominate as B2B e-commerce shifts leverage

Customers’ bargaining power is mixed: fragmented artisan clients (42% of 2024 revenue, €86m) have low price leverage but value service; large retailers and industrial buyers hold high clout and drive discounts; commodities buyers are highly price-sensitive; DGF offsets pressure via training (3,200+ chefs, +12% retention) and 28% bundled sales, but 2024 B2B e-commerce transparency (~$22T market) nudges power toward buyers.

| Metric | 2024 |

|---|---|

| Artisan revenue share | 42% (€86m) |

| Bundled sales | 28% |

| Chefs trained | 3,200+ |

| Retention lift | +12% |

| Global B2B digital sales | $22T |

Preview Before You Purchase

DGF Porter's Five Forces Analysis

This preview shows the exact DGF Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or mockups.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

DGF’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, threat of entrants, and substitute pressures—revealing where strategic focus can create advantage. This brief only scratches the surface; unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable implications tailored to DGF to inform investment or strategy decisions.

Suppliers Bargaining Power

Fragmented raw material supply base

The global markets for flour, sugar, and dairy are highly fragmented—over 5,000 regional mills and processors in 2024—so no single supplier holds sway, keeping supplier power low for DGF.

DGF’s annual ingredient purchases of ~USD 120m let it secure 3–6% price rebates and switch suppliers quickly if costs or quality slip.

Still, premium pastry cocoa and couverture chocolate come from ~30 certified high-quality mills, raising supplier leverage slightly in those niches.

Commodity price volatility and supply chain risks

Suppliers of cocoa, nuts, and fats face climate shocks and geopolitics that caused 2023–25 price spikes—cocoa rose ~40% in 2023 and global edible oil prices were up ~22% by mid‑2024—pressures suppliers pass to buyers. DGF’s large procurement volumes give negotiating leverage, but it still absorbs macro shocks when spot prices jump. By end‑2025 tighter environmental rules increased supplier compliance costs, adding estimated 5–8% to input prices. This keeps supplier bargaining power elevated despite DGF’s scale.

Dependency on specialized equipment manufacturers

DGF depends on a small set of high-end bakery and chocolate machinery makers, whose proprietary tech and spare parts give them strong leverage; industry data shows 60–70% of industrial chocolate lines use vendor-specific components, raising switching costs and spare-parts margins. Keeping exclusive or preferred partnerships (DGF reported 18% equipment revenue growth in 2024 after securing two OEM agreements) is vital to protect service levels and pricing power.

Logistics and energy cost fluctuations

Rising energy prices and the shift to sustainable packaging raised suppliers’ leverage; global oil-related freight costs jumped ~40% in 2021–24 and biodegradable packaging premiums run 10–30% higher (2025 market data).

DGF’s reliance on temperature-controlled transport makes it captive to specialized logistics rates: cold-chain freight can cost 20–50% more than dry freight, directly lifting COGS and squeezing margins.

- Energy-driven freight +40% (2021–24)

- Sustainable packaging premium 10–30% (2025)

- Cold-chain cost premium 20–50%

- Secondary supplier layer increases COGS and margin pressure

Increasing importance of sustainability certifications

Suppliers with certified organic, fair-trade, or carbon-neutral labels gain bargaining power as 68% of global consumers say sustainability influences purchases (NielsenIQ, 2024), letting premium suppliers charge 10–25% higher prices.

DGF must secure certified inputs to meet pro clients’ marketing claims and avoid losing RFPs; lack of certification raises churn risk and can push contract terms to favor suppliers.

- 68% of consumers influenced by sustainability (NielsenIQ 2024)

- Premium price premium: 10–25%

- Certification needed to win RFPs from professional clients

Suppliers exert limited but rising pressure—commodity spikes, freight & packaging squeeze margins

Suppliers hold overall low-to-moderate power: DGF’s ~USD120m annual buys and fragmented flour/sugar/dairy markets limit leverage, but niche cocoa, specialized machinery, cold-chain logistics, and sustainability-certified inputs raise supplier bargaining power—price shocks (cocoa +40% in 2023), energy-driven freight +40% (2021–24), and 10–30% packaging premiums force DGF to absorb or hedge costs.

| Metric | Value |

|---|---|

| Annual procurement | USD120m |

| Cocoa spike | +40% (2023) |

| Freight rise | +40% (2021–24) |

| Packaging premium | 10–30% (2025) |

What is included in the product

Tailored Porter's Five Forces analysis for DGF that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats to inform strategic positioning and investor materials.

A concise Porter's Five Forces one-sheet for DGF—instantly highlights competitive pressures and strategic levers to speed boardroom decisions and scenario planning.

Customers Bargaining Power

Fragmented artisan customer base

High volume industrial buyer leverage

Large-scale industrial food producers and retail chains buy massive volumes and often secure discounts—top 20 retail chains accounted for ~40% of US grocery sales in 2024, so their bargaining clout is high.

These buyers run competitive bids across distributors to cut costs; a 2023 ProcureTech survey found 68% of manufacturers use multi-supplier tenders for ingredients.

DGF must match with superior technical support and integrated logistics; retaining a single high-volume account can represent 5–15% of distributor revenues, so service wins volume.

Low switching costs for commodity ingredients

For basic ingredients like sugar or butter, customers face low switching costs and will defect to cheaper distributors when price dominates—commodity buyers drove a 7% average margin compression in global wholesale food distribution in 2024. There is little brand loyalty for raw commodities, so this segment is highly price-sensitive and volatile.

DGF reduces that risk by bundling commodities with specialized ingredients and value-added training programs; in 2024 bundled contracts represented about 28% of DGF’s sales, lifting blended gross margins by ~210 basis points versus standalone commodity sales.

Value-added services as a retention tool

DGF’s expert technical support and training create psychological and professional switching costs—bakers relying on DGF for recipe development and staff training become dependent, lowering willingness to switch for small price cuts. In 2024 DGF reported training >3,200 chefs and a 12% higher retention rate among trained accounts, which reduces customer bargaining power by embedding recipe know-how and operational workflows.

- Training >3,200 chefs (2024)

- Trained accounts: +12% retention (2024)

- Recipe development ties procurement to DGF

- Increases switching cost despite price pressure

Access to digital procurement platforms

By late 2025, B2B e-commerce growth — global B2B digital sales reached about $22 trillion in 2024 — gave customers real-time price and supplier transparency, letting buyers compare DGF’s freight and logistics rates with international rivals instantly.

That visibility forces DGF to match competitive pricing and faster delivery; customers increasingly demand sub-2% price variances and 24–72 hour quote turnarounds, shifting bargaining power slightly toward buyers.

- Global B2B digital sales ~ $22T (2024)

- Buyers demand <2% price variance

- Typical quote turnaround 24–72 hrs

- Power shifted slightly to buyers by 2025

Mixed buyer power: artisans loyal but retailers dominate as B2B e-commerce shifts leverage

Customers’ bargaining power is mixed: fragmented artisan clients (42% of 2024 revenue, €86m) have low price leverage but value service; large retailers and industrial buyers hold high clout and drive discounts; commodities buyers are highly price-sensitive; DGF offsets pressure via training (3,200+ chefs, +12% retention) and 28% bundled sales, but 2024 B2B e-commerce transparency (~$22T market) nudges power toward buyers.

| Metric | 2024 |

|---|---|

| Artisan revenue share | 42% (€86m) |

| Bundled sales | 28% |

| Chefs trained | 3,200+ |

| Retention lift | +12% |

| Global B2B digital sales | $22T |

Preview Before You Purchase

DGF Porter's Five Forces Analysis

This preview shows the exact DGF Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or mockups.