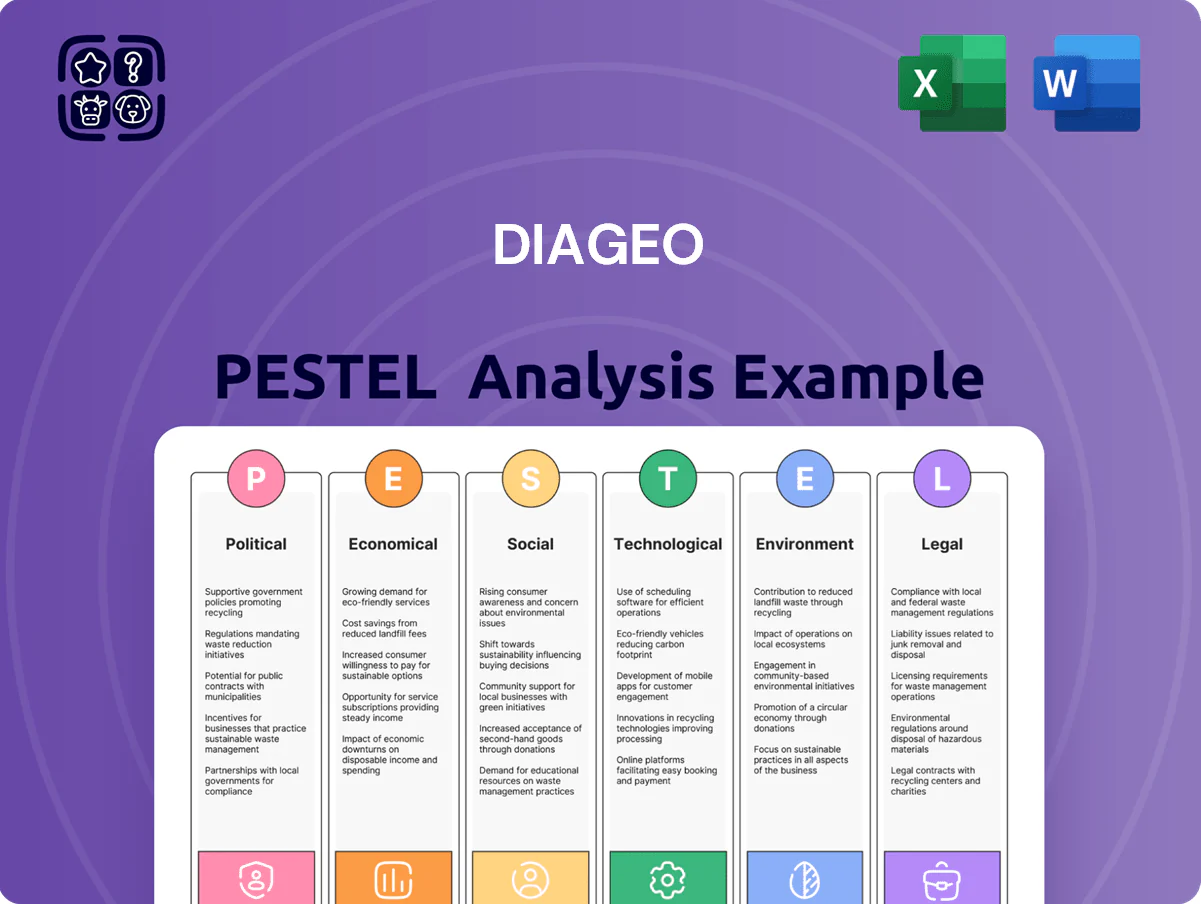

Diageo PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and evolving consumer tastes are shaping Diageo’s strategic outlook—our PESTLE distills these forces into clear implications for growth and risk. Ideal for investors and strategists who need fast, actionable context. Purchase the full PESTLE to unlock detailed trends, regulatory analysis, and ready-to-use insights for decision-making.

Political factors

Global Trade Relations and Tariffs

Diageo faces material risk from trade disputes—2019–2023 retaliatory US tariffs on EU spirits and 2020–2024 Chinese tariffs raised costs on Scotch and Bourbon, pressuring gross margins by up to 150–300 basis points in affected markets.

Shifts in UK–US–China policy alter landed prices and competitiveness of premium labels; China accounted for about 6% of Diageo’s FY2024 net sales, amplifying sensitivity to tariff moves.

Management must actively use pricing, hedging and supply-chain re‑routing to defend market share and EBITDA, noting a 2024 operating margin of roughly 25% that could be eroded if tariff escalation recurs.

Post-Brexit Regulatory Alignment

As a UK-headquartered firm, Diageo faces ongoing regulatory divergence post-Brexit, with 2024 trade frictions raising compliance costs; Scotch whisky exports were £4.3bn in 2023, making favorable UK-EU terms essential to competitiveness.

Negotiating preferential rules of origin and tariff-free access for spirits remains a priority to protect margins and market share across the EU.

UK government shifts on export subsidies and manufacturing support—including a £500m distillery investment fund proposed in 2024—shape Diageo’s domestic CAPEX and supply-chain planning.

Emerging Market Political Stability

Diageo’s heavy exposure in Africa, Asia and Latin America—markets that generated about 48% of net sales in FY2024—subjects it to political volatility where civil unrest or leadership changes can disrupt supply chains and production. In 2023–24, regional disruptions contributed to a 2.1% hit to organic net sales in select markets, prompting tighter risk controls. The company increases monitoring and contingency spending to safeguard growth in high-potential developing economies.

Alcohol Taxation Policies

Governments use excise taxes on alcohol for revenue and public health; in 2024 global alcohol excise receipts exceeded $200bn, with spirits taxes rising sharply in several markets (eg UK increased spirits duty in 2023 by 13.4%).

Sudden spirits tax hikes can cut demand—price elasticity for spirits often −0.7—forcing Diageo (2024 net sales £14.1bn) to absorb margin or cede volume to cheaper brands.

Diageo actively lobbies for predictable tax regimes via trade associations; its 2024 public affairs spend and industry advocacy helped influence policy consultations in 15+ markets.

- Excise taxes: >$200bn global receipts (2024)

- UK spirits duty +13.4% (2023)

- Spirits price elasticity ≈ −0.7

- Diageo 2024 net sales £14.1bn; advocacy across 15+ markets

International Trade Agreements

Ongoing UK-India free trade talks could cut India's 150%+ effective tariff on Scotch; Diageo estimates India could become a top-three market by volume if tariffs fall, tapping ~300m middle-class consumers and supporting long-term premium whisky growth after India already accounted for ~8% of global Scotch exports by value in 2023.

- Potential tariff cut from 150%+ could boost Scotch affordability

- ~300m Indian middle-class consumers represent large premium demand

- India ~8% of Scotch export value in 2023; favorable deals drive volume growth

Political taxes and tariffs threaten 150–300bp margin hit for Diageo’s £14.1bn sales

Political risks—tariffs, excise taxes, trade deals and regional instability—can shave 150–300bp off gross margins in affected markets; China (6% FY2024 sales) and India (~8% of Scotch export value 2023) are key exposures. Government excise receipts topped $200bn in 2024; UK spirits duty +13.4% (2023) and price elasticity ≈ −0.7 amplify volume risk for £14.1bn sales (FY2024). Diageo’s advocacy spans 15+ markets to defend margins and market access.

| Metric | Value |

|---|---|

| FY2024 net sales | £14.1bn |

| China share | ~6% |

| Scotch export value (India share 2023) | ~8% |

| Global excise receipts (2024) | >$200bn |

| UK spirits duty change (2023) | +13.4% |

What is included in the product

Explores how macro-environmental forces shape Diageo across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and regional regulatory context to identify threats and opportunities for executives and investors.

A concise, visually segmented Diageo PESTLE summary that surfaces key external risks and opportunities for quick inclusion in presentations, easily editable for region- or product-specific notes and shareable across teams to streamline strategic planning and stakeholder alignment.

Economic factors

Currency Fluctuations and Hedging

As a GBP reporter with ~60% revenue in USD and other currencies, Diageo is highly sensitive to exchange rate moves; a 10% GBP appreciation vs USD would cut reported revenues materially and reduced FY2024 adjusted operating profit by ~£200m in sensitivity scenarios. The group uses derivatives and natural hedges—Diageo held £9.8bn net cash and reported active hedging balances in 2024—to limit short-term volatility, but persistent structural FX shifts threaten long-term earnings and dividend capacity.

Premiumization Trends Amid Inflation

Despite global inflation averaging around 6% in 2024–25 in key markets, Diageo leverages the drink-less but better trend to achieve value growth: in FY25 premium and super-premium skews grew faster, contributing roughly 55% of net sales growth. High-net-worth consumers remained resilient—global ultra-wealthy wealth rose ~8% in 2024—supporting margin retention in top-tier brands. Prolonged inflation, however, risks down-trading with price-sensitive consumers shifting to lower-priced labels within Diageo’s portfolio.

Global Supply Chain Costs

Rising raw-materials, energy and logistics costs materially affect Diageo’s COGS and margins; in 2024 packaging and input inflation contributed to a 4.5% increase in COGS year-over-year, pressuring gross margin despite 6% organic net sales growth.

Volatility in glass, grain and agave prices—with global glass container index up ~12% in 2023–24 and Mexican agave futures spiking 30% in 2024—has driven Diageo to expand strategic procurement, hedging and supplier consolidation programs.

Efficiency initiatives, including supply-chain automation and energy-efficiency projects targeting a 3–5% reduction in input costs, are critical to preserving Diageo’s industry-leading operating margin (~24% reported in FY2024) that investors expect.

Interest Rate Impacts on Capital

Higher global interest rates raised Diageo’s weighted average cost of debt to about 3.6% in 2024, increasing financing costs for M&A and capex and potentially delaying large-scale projects.

Diageo’s disciplined balance sheet—with net debt/EBITDA around 1.1x in FY24—helps ensure debt serviceability while sustaining dividends and buybacks.

Shifts in central bank policy alter discount rates used by analysts, contributing to valuation sensitivity and share price volatility.

- WACC/discount rates rose with global hikes

- Net debt/EBITDA ~1.1x (FY24)

- Cost of debt ~3.6% (2024)

Disposable Income in Emerging Markets

The expanding middle class in Southeast Asia and Africa—forecasted to add over 1 billion people by 2030—boosts disposable income, directly improving demand for branded spirits; Diageo reported 2024 organic net sales growth of 8% in Africa & North America regions, reflecting this trend.

Rising GDP per capita in Vietnam (+3.2% real GDP 2024) and Nigeria (estimated 2.5% 2024) shifts consumption from informal alcohol to regulated brands, increasing Diageo’s addressable market and pricing power.

Diageo’s exposure ties revenues to emerging-market FX and GDP volatility: ~30% of 2024 net sales came from Africa & Asia, so macro slowdowns pose material risk.

- Middle-class growth → larger branded-spirit demand

- 2024: Diageo organic sales +8% in key regions

- Vietnam GDP +3.2% and Nigeria ~2.5% in 2024 support consumption shifts

- ~30% of net sales from Africa & Asia — exposure to GDP/FX risk

Diageo margins squeezed by FX, inflation and rates despite £9.8bn cash and premiumisation

FX swings, higher input/energy costs and rising rates compressed margins in FY24—GBP strength could cut reported revenue materially; Diageo used hedges and held £9.8bn net cash with net debt/EBITDA ~1.1x. Premiumisation drove ~55% of net sales growth; Africa & Asia (~30% sales) grew ~8% organically. Cost inflation raised COGS ~4.5% and WACC pushed cost of debt ~3.6% in 2024.

| Metric | 2024 |

|---|---|

| Net cash | £9.8bn |

| Net debt/EBITDA | ~1.1x |

| COGS ↑ | 4.5% |

| Cost of debt | ~3.6% |

What You See Is What You Get

Diageo PESTLE Analysis

The Diageo PESTLE analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and evolving consumer tastes are shaping Diageo’s strategic outlook—our PESTLE distills these forces into clear implications for growth and risk. Ideal for investors and strategists who need fast, actionable context. Purchase the full PESTLE to unlock detailed trends, regulatory analysis, and ready-to-use insights for decision-making.

Political factors

Global Trade Relations and Tariffs

Diageo faces material risk from trade disputes—2019–2023 retaliatory US tariffs on EU spirits and 2020–2024 Chinese tariffs raised costs on Scotch and Bourbon, pressuring gross margins by up to 150–300 basis points in affected markets.

Shifts in UK–US–China policy alter landed prices and competitiveness of premium labels; China accounted for about 6% of Diageo’s FY2024 net sales, amplifying sensitivity to tariff moves.

Management must actively use pricing, hedging and supply-chain re‑routing to defend market share and EBITDA, noting a 2024 operating margin of roughly 25% that could be eroded if tariff escalation recurs.

Post-Brexit Regulatory Alignment

As a UK-headquartered firm, Diageo faces ongoing regulatory divergence post-Brexit, with 2024 trade frictions raising compliance costs; Scotch whisky exports were £4.3bn in 2023, making favorable UK-EU terms essential to competitiveness.

Negotiating preferential rules of origin and tariff-free access for spirits remains a priority to protect margins and market share across the EU.

UK government shifts on export subsidies and manufacturing support—including a £500m distillery investment fund proposed in 2024—shape Diageo’s domestic CAPEX and supply-chain planning.

Emerging Market Political Stability

Diageo’s heavy exposure in Africa, Asia and Latin America—markets that generated about 48% of net sales in FY2024—subjects it to political volatility where civil unrest or leadership changes can disrupt supply chains and production. In 2023–24, regional disruptions contributed to a 2.1% hit to organic net sales in select markets, prompting tighter risk controls. The company increases monitoring and contingency spending to safeguard growth in high-potential developing economies.

Alcohol Taxation Policies

Governments use excise taxes on alcohol for revenue and public health; in 2024 global alcohol excise receipts exceeded $200bn, with spirits taxes rising sharply in several markets (eg UK increased spirits duty in 2023 by 13.4%).

Sudden spirits tax hikes can cut demand—price elasticity for spirits often −0.7—forcing Diageo (2024 net sales £14.1bn) to absorb margin or cede volume to cheaper brands.

Diageo actively lobbies for predictable tax regimes via trade associations; its 2024 public affairs spend and industry advocacy helped influence policy consultations in 15+ markets.

- Excise taxes: >$200bn global receipts (2024)

- UK spirits duty +13.4% (2023)

- Spirits price elasticity ≈ −0.7

- Diageo 2024 net sales £14.1bn; advocacy across 15+ markets

International Trade Agreements

Ongoing UK-India free trade talks could cut India's 150%+ effective tariff on Scotch; Diageo estimates India could become a top-three market by volume if tariffs fall, tapping ~300m middle-class consumers and supporting long-term premium whisky growth after India already accounted for ~8% of global Scotch exports by value in 2023.

- Potential tariff cut from 150%+ could boost Scotch affordability

- ~300m Indian middle-class consumers represent large premium demand

- India ~8% of Scotch export value in 2023; favorable deals drive volume growth

Political taxes and tariffs threaten 150–300bp margin hit for Diageo’s £14.1bn sales

Political risks—tariffs, excise taxes, trade deals and regional instability—can shave 150–300bp off gross margins in affected markets; China (6% FY2024 sales) and India (~8% of Scotch export value 2023) are key exposures. Government excise receipts topped $200bn in 2024; UK spirits duty +13.4% (2023) and price elasticity ≈ −0.7 amplify volume risk for £14.1bn sales (FY2024). Diageo’s advocacy spans 15+ markets to defend margins and market access.

| Metric | Value |

|---|---|

| FY2024 net sales | £14.1bn |

| China share | ~6% |

| Scotch export value (India share 2023) | ~8% |

| Global excise receipts (2024) | >$200bn |

| UK spirits duty change (2023) | +13.4% |

What is included in the product

Explores how macro-environmental forces shape Diageo across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and regional regulatory context to identify threats and opportunities for executives and investors.

A concise, visually segmented Diageo PESTLE summary that surfaces key external risks and opportunities for quick inclusion in presentations, easily editable for region- or product-specific notes and shareable across teams to streamline strategic planning and stakeholder alignment.

Economic factors

Currency Fluctuations and Hedging

As a GBP reporter with ~60% revenue in USD and other currencies, Diageo is highly sensitive to exchange rate moves; a 10% GBP appreciation vs USD would cut reported revenues materially and reduced FY2024 adjusted operating profit by ~£200m in sensitivity scenarios. The group uses derivatives and natural hedges—Diageo held £9.8bn net cash and reported active hedging balances in 2024—to limit short-term volatility, but persistent structural FX shifts threaten long-term earnings and dividend capacity.

Premiumization Trends Amid Inflation

Despite global inflation averaging around 6% in 2024–25 in key markets, Diageo leverages the drink-less but better trend to achieve value growth: in FY25 premium and super-premium skews grew faster, contributing roughly 55% of net sales growth. High-net-worth consumers remained resilient—global ultra-wealthy wealth rose ~8% in 2024—supporting margin retention in top-tier brands. Prolonged inflation, however, risks down-trading with price-sensitive consumers shifting to lower-priced labels within Diageo’s portfolio.

Global Supply Chain Costs

Rising raw-materials, energy and logistics costs materially affect Diageo’s COGS and margins; in 2024 packaging and input inflation contributed to a 4.5% increase in COGS year-over-year, pressuring gross margin despite 6% organic net sales growth.

Volatility in glass, grain and agave prices—with global glass container index up ~12% in 2023–24 and Mexican agave futures spiking 30% in 2024—has driven Diageo to expand strategic procurement, hedging and supplier consolidation programs.

Efficiency initiatives, including supply-chain automation and energy-efficiency projects targeting a 3–5% reduction in input costs, are critical to preserving Diageo’s industry-leading operating margin (~24% reported in FY2024) that investors expect.

Interest Rate Impacts on Capital

Higher global interest rates raised Diageo’s weighted average cost of debt to about 3.6% in 2024, increasing financing costs for M&A and capex and potentially delaying large-scale projects.

Diageo’s disciplined balance sheet—with net debt/EBITDA around 1.1x in FY24—helps ensure debt serviceability while sustaining dividends and buybacks.

Shifts in central bank policy alter discount rates used by analysts, contributing to valuation sensitivity and share price volatility.

- WACC/discount rates rose with global hikes

- Net debt/EBITDA ~1.1x (FY24)

- Cost of debt ~3.6% (2024)

Disposable Income in Emerging Markets

The expanding middle class in Southeast Asia and Africa—forecasted to add over 1 billion people by 2030—boosts disposable income, directly improving demand for branded spirits; Diageo reported 2024 organic net sales growth of 8% in Africa & North America regions, reflecting this trend.

Rising GDP per capita in Vietnam (+3.2% real GDP 2024) and Nigeria (estimated 2.5% 2024) shifts consumption from informal alcohol to regulated brands, increasing Diageo’s addressable market and pricing power.

Diageo’s exposure ties revenues to emerging-market FX and GDP volatility: ~30% of 2024 net sales came from Africa & Asia, so macro slowdowns pose material risk.

- Middle-class growth → larger branded-spirit demand

- 2024: Diageo organic sales +8% in key regions

- Vietnam GDP +3.2% and Nigeria ~2.5% in 2024 support consumption shifts

- ~30% of net sales from Africa & Asia — exposure to GDP/FX risk

Diageo margins squeezed by FX, inflation and rates despite £9.8bn cash and premiumisation

FX swings, higher input/energy costs and rising rates compressed margins in FY24—GBP strength could cut reported revenue materially; Diageo used hedges and held £9.8bn net cash with net debt/EBITDA ~1.1x. Premiumisation drove ~55% of net sales growth; Africa & Asia (~30% sales) grew ~8% organically. Cost inflation raised COGS ~4.5% and WACC pushed cost of debt ~3.6% in 2024.

| Metric | 2024 |

|---|---|

| Net cash | £9.8bn |

| Net debt/EBITDA | ~1.1x |

| COGS ↑ | 4.5% |

| Cost of debt | ~3.6% |

What You See Is What You Get

Diageo PESTLE Analysis

The Diageo PESTLE analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.