DiaSorin PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, regulatory pressures, and rapid diagnostic-tech advances are reshaping DiaSorin’s prospects—our concise PESTLE snapshot highlights the external forces that matter for investors and strategists; purchase the full analysis to access detailed, actionable insights and ready-to-use slides for decision-making.

Political factors

Global Healthcare Policy Shifts

Governments are prioritizing diagnostic accuracy to cut long-term costs, with value-based care policies adopted by over 40 countries by late 2025, shifting procurement toward outcomes-linked diagnostics and boosting demand for DiaSorin’s specialized kits.

Reimbursement reforms have tied payments to clinical value—immunodiagnostics and molecular tests saw a 12–18% average reimbursement adjustment in key EU markets in 2024–25—pressuring pricing and product positioning.

Maintaining strong ties with national health authorities is essential: in 2025 DiaSorin must secure coverage decisions and HTA endorsements to protect market access and revenue streams in major markets representing ~55% of its diagnostics sales.

Geopolitical Stability and Trade Relations

DiaSorin’s global supply chain, spanning over 20 manufacturing sites and sales in 90+ countries, is highly exposed to trade tensions between the EU, US and China; 2024 revenues of €1.6bn underscore sensitivity to cross-border disruptions. Political instability or new tariffs can delay critical reagents and analyzers, risking production slowdowns that could cut sales growth already slowing to mid-single digits in 2024. The firm must adapt through dual sourcing, local assembly and compliance with country-specific manufacturing rules to limit interruption risks in volatile markets.

Government Funding for Pandemic Preparedness

In response to COVID-19, many countries sustained dedicated budgets for infectious disease surveillance, with OECD reporting a 12% median increase in public health capital spending 2021–2023; DiaSorin gains as labs upgrade analyzers and procure molecular assays. Major EU recovery packages allocated over €20 billion to health resilience by 2024, supporting demand for high-throughput diagnostics where DiaSorin competes. Political focus on biosecurity and rapid response keeps government procurement cycles favorable, driving recurring orders for platforms and reagents.

Regulatory Harmonization Initiatives

Political efforts to harmonize medical device regulations, such as the EU-US Medical Device Single Audit Program and ICH-like talks, can lower DiaSorin's market-entry costs by reducing duplicate clinical trials and expediting approvals across ~50+ jurisdictions, supporting its 2024 revenues of €1.05bn in IVDs.

However, rising local protectionism in markets like India (import tariffs up to 15% and recent Buy Global procurement preferences) may force DiaSorin to invest in domestic manufacturing, increasing capex and potentially raising breakeven timelines.

Navigating these divergent political landscapes is critical for sustaining DiaSorin's global competitive edge in the IVD segment, where regulatory delays can shift market share and affect margins.

- Harmonization reduces repeat trials and speeds approvals across 50+ jurisdictions

- 2024 IVD revenue: ~€1.05bn

- Local protectionism (e.g., India tariffs ~15%) may necessitate domestic capex

- Regulatory strategy impacts market share and margins

Impact of Healthcare Privatization

Privatization in Europe and Asia shifts purchasing toward private labs; private providers now account for about 25–40% of diagnostic volumes in key markets like Italy and India, affecting DiaSorin’s revenue mix and pricing power.

Private chains prioritize efficiency and cost-per-test, pressuring margins and favoring high-throughput, lower-cost assays over premium niche tests.

DiaSorin must reallocate policy engagement and commercial resources to influence private procurement practices and tender frameworks as private providers grow.

- Private diagnostics share ~25–40% in target markets

- Focus on cost-per-test reduces average selling price

- Requires shifted gov’t relations toward private-sector stakeholders

Policy shocks reshape DiaSorin: pricing cuts, value procurement & forced localisation

Political shifts—value-based procurement in 40+ countries by 2025, reimbursement cuts of 12–18% in key EU markets (2024–25), and increased health resilience funding (+12% median public health spend 2021–23)—reshape DiaSorin’s access, pricing and capex needs; protectionism (India tariffs ~15%) and private lab growth (25–40% volumes) force localisation and commercial pivoting.

| Metric | Value |

|---|---|

| 2024 revenues (total) | €1.6bn |

| 2024 IVD revenue | €1.05bn |

| Reimbursement change (EU 2024–25) | −12–18% |

| Countries with value-based procurement by 2025 | 40+ |

| Public health spend increase (2021–23) | +12% median |

| India import tariff example | ~15% |

| Private diagnostics share (key markets) | 25–40% |

What is included in the product

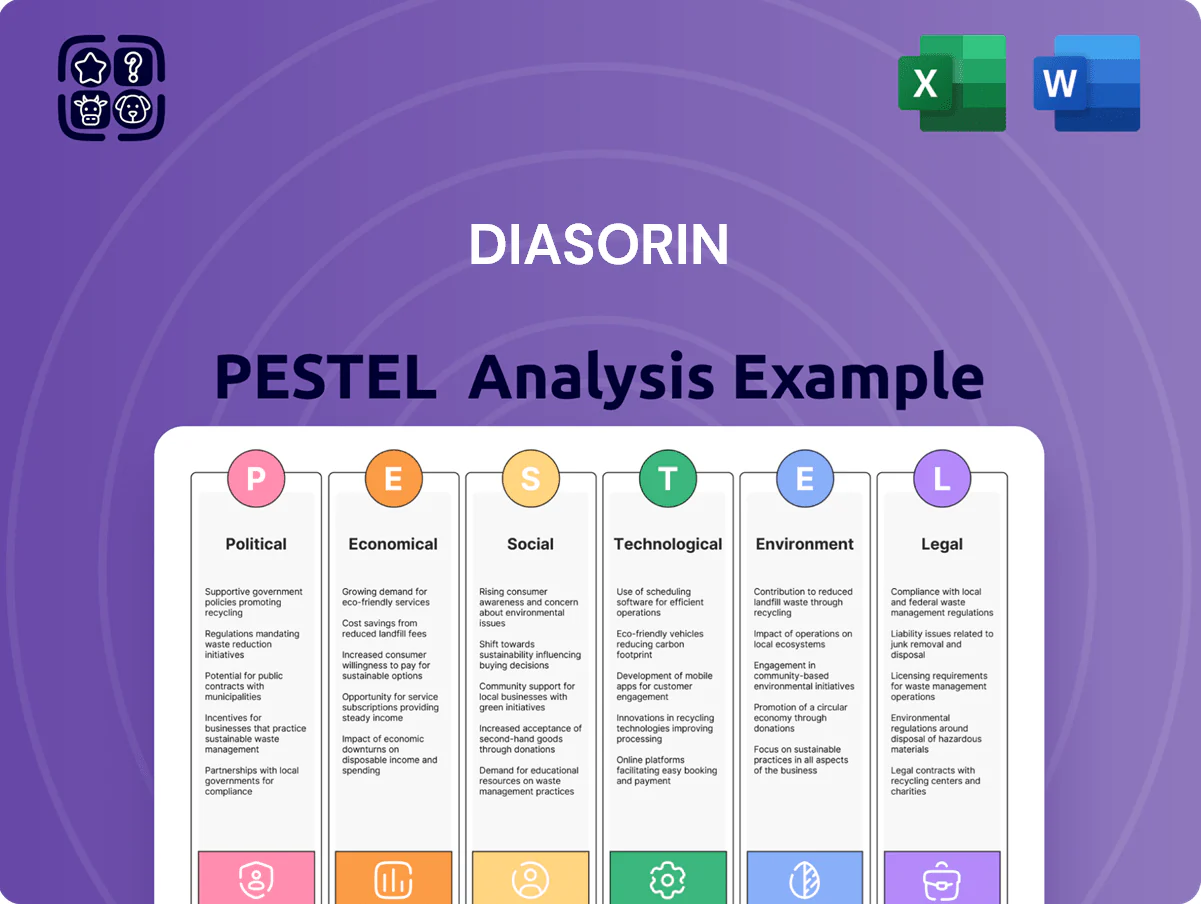

Explores how external macro-environmental factors uniquely affect DiaSorin across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify risks and opportunities.

Provides a concise, shareable DiaSorin PESTLE summary that’s visually segmented by category for quick interpretation during meetings or strategy sessions.

Economic factors

Inflationary Pressures on Operational Costs

Persistent global inflation through 2025 pushed raw material, energy and specialized labor costs up ~6–9% year-on-year, squeezing DiaSorin’s margins as reagent kit ASPs rose only modestly; managing input inflation while keeping instruments and consumables price-competitive is critical. Automation and process efficiencies—where DiaSorin reported a target to cut manufacturing costs by ~4–6% in 2024–25—are essential to protect EBITDA against sustained cost pressure.

Currency Exchange Rate Volatility

As an Italian company with a large global footprint, DiaSorin faces material exposure to EUR/USD and other major currency swings; in 2024 roughly 45% of revenue was generated in North America, so a stronger euro can materially compress reported EUR results when translating USD sales.

In 2024 the euro appreciated about 4% vs the dollar year‑on‑year, which would have reduced translated North American revenue by a similar magnitude absent mitigation.

DiaSorin employs strategic hedging—forward contracts covering a portion of expected cash flows—and increasingly localized manufacturing in the US and Brazil to reduce transactional and translation risk and stabilize margins.

Public Healthcare Budget Constraints

Many national health systems face fiscal pressure, with OECD public health spending growth slowing to 1.1% in 2023, tightening budgets for diagnostics and lab equipment and forcing DiaSorin to prove cost-effectiveness versus cheaper assays; studies show diagnostic cost-per-positive impact can sway procurement decisions by up to 20%. Economic contractions in Italy and Brazil in 2023–24 reduced hospital CAPEX by an estimated 8–12%, delaying automated-analyzer placements.

Growth in Emerging Market Economies

The expanding middle class in emerging markets—projected to reach 3.3 billion people by 2030—boosts per-capita healthcare spend; WHO reports health expenditure growth in low- and middle-income countries averaged ~4.1% annually (2020–2023), creating demand for diagnostics. DiaSorin is prioritizing Latin America, Asia and MENA to offset flat growth in Europe/North America, but faces currency swings and GDP volatility (IMF 2024: EM growth 4.1%). Scalable, cost-effective assays and local partnerships are critical to win under-resourced systems.

- EM middle class → higher per-capita health spend; 3.3B by 2030

- WHO: LMIC health spending +4.1% annually (2020–2023)

- IMF 2024 EM growth ~4.1%; currency/GDP volatility risk

- Need scalable, low-cost assays and local distribution/partnerships

Interest Rate Impact on Lab Investments

Rising global interest rates—US Fed funds ~5.25–5.50% and ECB deposit ~3.75% in 2025—raise financing costs for private labs, shifting purchases toward leasing or reagent-rental models and compressing capital expenditure by an estimated 10–15% in smaller labs.

DiaSorin reports expanding flexible financing and reagent-rental offerings, stabilizing recurring revenue and smoothing cash flow despite higher borrowing costs.

- Higher rates push leasing/rental adoption

- Smaller labs cut CAPEX ~10–15%

- DiaSorin expands financing/reagent-rental

- Recurring revenue cushions cash-flow volatility

DiaSorin braces for cost cuts and FX risk as EM demand offsets slow OECD spending

Inflation (2024–25) raised input costs ~6–9% y/y while ASPs rose modestly; DiaSorin targets 4–6% manufacturing cost cuts to protect EBITDA. FX risk is material—~45% revenue from North America in 2024; EUR appreciated ~4% vs USD in 2024, hedging and local production mitigate translation impact. OECD health spending growth slowed to 1.1% (2023); EM growth ~4.1% (IMF 2024) and LMIC health spend +4.1% (WHO 2020–23) support EM expansion. Higher rates (Fed ~5.25–5.50%, ECB ~3.75% in 2025) push leasing/reagent-rental uptake; smaller labs cut CAPEX ~10–15%.

| Metric | Value |

|---|---|

| Input cost inflation | ~6–9% y/y (2024–25) |

| Manufacturing cost target | ~4–6% reduction (2024–25) |

| North America revenue | ~45% (2024) |

| EUR vs USD (2024) | EUR +4% y/y |

| OECD health spend growth | 1.1% (2023) |

| EM growth (IMF) | ~4.1% (2024) |

| LMIC health spend | +4.1% annually (2020–23) |

| Fed funds rate | ~5.25–5.50% (2025) |

| ECB deposit rate | ~3.75% (2025) |

| Smaller labs CAPEX cut | ~10–15% |

Preview Before You Purchase

DiaSorin PESTLE Analysis

The preview shown here is the exact DiaSorin PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, regulatory pressures, and rapid diagnostic-tech advances are reshaping DiaSorin’s prospects—our concise PESTLE snapshot highlights the external forces that matter for investors and strategists; purchase the full analysis to access detailed, actionable insights and ready-to-use slides for decision-making.

Political factors

Global Healthcare Policy Shifts

Governments are prioritizing diagnostic accuracy to cut long-term costs, with value-based care policies adopted by over 40 countries by late 2025, shifting procurement toward outcomes-linked diagnostics and boosting demand for DiaSorin’s specialized kits.

Reimbursement reforms have tied payments to clinical value—immunodiagnostics and molecular tests saw a 12–18% average reimbursement adjustment in key EU markets in 2024–25—pressuring pricing and product positioning.

Maintaining strong ties with national health authorities is essential: in 2025 DiaSorin must secure coverage decisions and HTA endorsements to protect market access and revenue streams in major markets representing ~55% of its diagnostics sales.

Geopolitical Stability and Trade Relations

DiaSorin’s global supply chain, spanning over 20 manufacturing sites and sales in 90+ countries, is highly exposed to trade tensions between the EU, US and China; 2024 revenues of €1.6bn underscore sensitivity to cross-border disruptions. Political instability or new tariffs can delay critical reagents and analyzers, risking production slowdowns that could cut sales growth already slowing to mid-single digits in 2024. The firm must adapt through dual sourcing, local assembly and compliance with country-specific manufacturing rules to limit interruption risks in volatile markets.

Government Funding for Pandemic Preparedness

In response to COVID-19, many countries sustained dedicated budgets for infectious disease surveillance, with OECD reporting a 12% median increase in public health capital spending 2021–2023; DiaSorin gains as labs upgrade analyzers and procure molecular assays. Major EU recovery packages allocated over €20 billion to health resilience by 2024, supporting demand for high-throughput diagnostics where DiaSorin competes. Political focus on biosecurity and rapid response keeps government procurement cycles favorable, driving recurring orders for platforms and reagents.

Regulatory Harmonization Initiatives

Political efforts to harmonize medical device regulations, such as the EU-US Medical Device Single Audit Program and ICH-like talks, can lower DiaSorin's market-entry costs by reducing duplicate clinical trials and expediting approvals across ~50+ jurisdictions, supporting its 2024 revenues of €1.05bn in IVDs.

However, rising local protectionism in markets like India (import tariffs up to 15% and recent Buy Global procurement preferences) may force DiaSorin to invest in domestic manufacturing, increasing capex and potentially raising breakeven timelines.

Navigating these divergent political landscapes is critical for sustaining DiaSorin's global competitive edge in the IVD segment, where regulatory delays can shift market share and affect margins.

- Harmonization reduces repeat trials and speeds approvals across 50+ jurisdictions

- 2024 IVD revenue: ~€1.05bn

- Local protectionism (e.g., India tariffs ~15%) may necessitate domestic capex

- Regulatory strategy impacts market share and margins

Impact of Healthcare Privatization

Privatization in Europe and Asia shifts purchasing toward private labs; private providers now account for about 25–40% of diagnostic volumes in key markets like Italy and India, affecting DiaSorin’s revenue mix and pricing power.

Private chains prioritize efficiency and cost-per-test, pressuring margins and favoring high-throughput, lower-cost assays over premium niche tests.

DiaSorin must reallocate policy engagement and commercial resources to influence private procurement practices and tender frameworks as private providers grow.

- Private diagnostics share ~25–40% in target markets

- Focus on cost-per-test reduces average selling price

- Requires shifted gov’t relations toward private-sector stakeholders

Policy shocks reshape DiaSorin: pricing cuts, value procurement & forced localisation

Political shifts—value-based procurement in 40+ countries by 2025, reimbursement cuts of 12–18% in key EU markets (2024–25), and increased health resilience funding (+12% median public health spend 2021–23)—reshape DiaSorin’s access, pricing and capex needs; protectionism (India tariffs ~15%) and private lab growth (25–40% volumes) force localisation and commercial pivoting.

| Metric | Value |

|---|---|

| 2024 revenues (total) | €1.6bn |

| 2024 IVD revenue | €1.05bn |

| Reimbursement change (EU 2024–25) | −12–18% |

| Countries with value-based procurement by 2025 | 40+ |

| Public health spend increase (2021–23) | +12% median |

| India import tariff example | ~15% |

| Private diagnostics share (key markets) | 25–40% |

What is included in the product

Explores how external macro-environmental factors uniquely affect DiaSorin across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify risks and opportunities.

Provides a concise, shareable DiaSorin PESTLE summary that’s visually segmented by category for quick interpretation during meetings or strategy sessions.

Economic factors

Inflationary Pressures on Operational Costs

Persistent global inflation through 2025 pushed raw material, energy and specialized labor costs up ~6–9% year-on-year, squeezing DiaSorin’s margins as reagent kit ASPs rose only modestly; managing input inflation while keeping instruments and consumables price-competitive is critical. Automation and process efficiencies—where DiaSorin reported a target to cut manufacturing costs by ~4–6% in 2024–25—are essential to protect EBITDA against sustained cost pressure.

Currency Exchange Rate Volatility

As an Italian company with a large global footprint, DiaSorin faces material exposure to EUR/USD and other major currency swings; in 2024 roughly 45% of revenue was generated in North America, so a stronger euro can materially compress reported EUR results when translating USD sales.

In 2024 the euro appreciated about 4% vs the dollar year‑on‑year, which would have reduced translated North American revenue by a similar magnitude absent mitigation.

DiaSorin employs strategic hedging—forward contracts covering a portion of expected cash flows—and increasingly localized manufacturing in the US and Brazil to reduce transactional and translation risk and stabilize margins.

Public Healthcare Budget Constraints

Many national health systems face fiscal pressure, with OECD public health spending growth slowing to 1.1% in 2023, tightening budgets for diagnostics and lab equipment and forcing DiaSorin to prove cost-effectiveness versus cheaper assays; studies show diagnostic cost-per-positive impact can sway procurement decisions by up to 20%. Economic contractions in Italy and Brazil in 2023–24 reduced hospital CAPEX by an estimated 8–12%, delaying automated-analyzer placements.

Growth in Emerging Market Economies

The expanding middle class in emerging markets—projected to reach 3.3 billion people by 2030—boosts per-capita healthcare spend; WHO reports health expenditure growth in low- and middle-income countries averaged ~4.1% annually (2020–2023), creating demand for diagnostics. DiaSorin is prioritizing Latin America, Asia and MENA to offset flat growth in Europe/North America, but faces currency swings and GDP volatility (IMF 2024: EM growth 4.1%). Scalable, cost-effective assays and local partnerships are critical to win under-resourced systems.

- EM middle class → higher per-capita health spend; 3.3B by 2030

- WHO: LMIC health spending +4.1% annually (2020–2023)

- IMF 2024 EM growth ~4.1%; currency/GDP volatility risk

- Need scalable, low-cost assays and local distribution/partnerships

Interest Rate Impact on Lab Investments

Rising global interest rates—US Fed funds ~5.25–5.50% and ECB deposit ~3.75% in 2025—raise financing costs for private labs, shifting purchases toward leasing or reagent-rental models and compressing capital expenditure by an estimated 10–15% in smaller labs.

DiaSorin reports expanding flexible financing and reagent-rental offerings, stabilizing recurring revenue and smoothing cash flow despite higher borrowing costs.

- Higher rates push leasing/rental adoption

- Smaller labs cut CAPEX ~10–15%

- DiaSorin expands financing/reagent-rental

- Recurring revenue cushions cash-flow volatility

DiaSorin braces for cost cuts and FX risk as EM demand offsets slow OECD spending

Inflation (2024–25) raised input costs ~6–9% y/y while ASPs rose modestly; DiaSorin targets 4–6% manufacturing cost cuts to protect EBITDA. FX risk is material—~45% revenue from North America in 2024; EUR appreciated ~4% vs USD in 2024, hedging and local production mitigate translation impact. OECD health spending growth slowed to 1.1% (2023); EM growth ~4.1% (IMF 2024) and LMIC health spend +4.1% (WHO 2020–23) support EM expansion. Higher rates (Fed ~5.25–5.50%, ECB ~3.75% in 2025) push leasing/reagent-rental uptake; smaller labs cut CAPEX ~10–15%.

| Metric | Value |

|---|---|

| Input cost inflation | ~6–9% y/y (2024–25) |

| Manufacturing cost target | ~4–6% reduction (2024–25) |

| North America revenue | ~45% (2024) |

| EUR vs USD (2024) | EUR +4% y/y |

| OECD health spend growth | 1.1% (2023) |

| EM growth (IMF) | ~4.1% (2024) |

| LMIC health spend | +4.1% annually (2020–23) |

| Fed funds rate | ~5.25–5.50% (2025) |

| ECB deposit rate | ~3.75% (2025) |

| Smaller labs CAPEX cut | ~10–15% |

Preview Before You Purchase

DiaSorin PESTLE Analysis

The preview shown here is the exact DiaSorin PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.