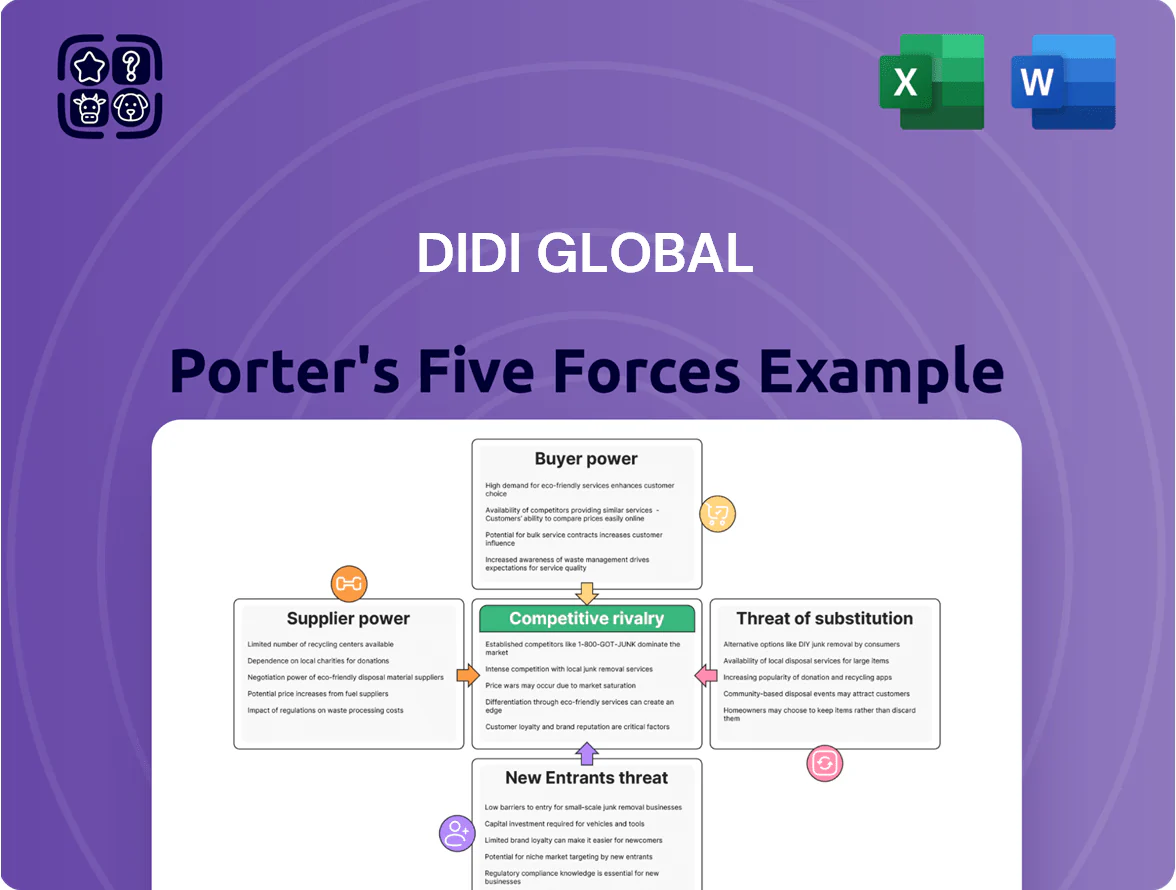

DiDi Global Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

DiDi Global faces intense rivalry from global and local ride-hailing rivals, regulatory headwinds, and shifting consumer preferences that pressure margins and growth—while its data assets and scale offer defensive advantages; this snapshot highlights key tensions but omits force-by-force ratings and strategic implications. Unlock the full Porter's Five Forces Analysis to get detailed ratings, visuals, and actionable insights for investment or strategic planning.

Suppliers Bargaining Power

Fragmented Driver Labor Force

The primary suppliers are millions of individual drivers who provide labor and vehicles; DiDi reported about 31 million drivers in China in 2023, so suppliers are highly fragmented and lack formal bargaining power.

Still, driver power rises during labor shortages or fuel spikes—e.g., China diesel rose ~18% in 2022–23—forcing higher incentives.

DiDi must balance commission cuts and targeted bonuses; in 2024 it spent roughly 6–9% of gross transaction value on driver incentives to retain supply.

Mapping and Cloud Infrastructure Providers

DiDi depends on advanced mapping and cloud compute for real-time routing; in 2024 DiDi processed billions of daily location events, so latency matters. Fewer than five global-tier providers (eg, Alibaba Cloud, Huawei Cloud) can scale at that level, giving suppliers moderate bargaining power reflected in cloud spend—DiDi reported infrastructure costs of RMB 5.2 billion in FY2024. Any outage would sharply halt driver-passenger matching and revenue flow.

Automotive Manufacturers and Fleet Partners

As DiDi shifts to EV fleets, dependence on automakers like BYD rises—BYD supplied ~100,000 EVs to Chinese fleets in 2024, giving manufacturers leverage on unit pricing and maintenance contracts for managed fleets.

Suppliers set terms on warranties and telematics; that matters because DiDi operated ~6 million rides/day in 2024, so scale lets DiDi secure bulk discounts, volume rebates and co-development deals reducing per-vehicle cost by an estimated 8–12%.

Energy and Charging Network Operators

Energy and charging network operators gained outsized supplier power as green-mobility targets push fleets electric by end-2025; global EV charging installed base grew ~60% in 2024 to 6.9M chargers, tightening access and raising prices for third-party use.

DiDi’s reliance on external stations directly affects per-ride energy costs and uptime, so operators can influence margins via tariffs and availability.

DiDi reduces exposure by investing in joint-venture charging hubs—reported CAPEX stake ~USD 120m in 2023–24—securing priority access and lower kWh rates.

- Charging supply concentrated: top 5 operators ~45% market share

- DiDi JV CAPEX ~USD 120m (2023–24)

- Installed chargers 6.9M in 2024, +60% YoY

Financial and Insurance Service Providers

DiDi needs specialized driver insurance and integrated payment processing; in 2024 its financial arm handled about $9.2B in payments but still relies on major banks and gateways for cross-border flows.

Regulatory mandates for comprehensive driver coverage make banks and insurers essential partners, giving them steady bargaining power despite DiDi’s internal capabilities.

Here’s the quick math: 65% of cross-border settlements routed via 3 global gateways in 2024, increasing supplier leverage.

- 2024 payments processed: ~$9.2B

- 65% cross-border via top 3 gateways

- Regulatory insurance mandates boost insurer role

- Major banks control FX and settlement rails

Driver supply vs rising leverage: incentives, infra & EV CAPEX reshape mobility margins

Suppliers: fragmented driver base (~31M drivers in China, 2023) gives low bargaining power, but shortages/fuel spikes raise leverage; DiDi spent ~6–9% of GTV on driver incentives in 2024. Cloud/telecom (few providers) and automakers (e.g., BYD ~100k EVs to fleets in 2024) hold moderate power; infrastructure costs RMB 5.2B FY2024; JV charging CAPEX ~USD120M (2023–24).

| Item | 2023–24 |

|---|---|

| Drivers (China) | 31M (2023) |

| Driver incentives | 6–9% GTV (2024) |

| Infra costs | RMB 5.2B (FY2024) |

| BYD EV supply | ~100k (2024) |

| JV charging CAPEX | USD 120M (2023–24) |

What is included in the product

Tailored Porter's Five Forces for DiDi Global, revealing competitive intensity, buyer/supplier leverage, threat of entrants and substitutes, and strategic levers to defend market share and margins.

Clear, one-sheet Porter's Five Forces for DiDi Global—instantly shows competitive pressures and regulatory risks to speed strategic decisions.

Customers Bargaining Power

Low Switching Costs for Individual Riders

Individual riders face low switching costs among apps like DiDi, Meituan, and T3 Go, raising buyer power as 70% of urban users in China (2024 survey) report choosing by wait time or price.

DiDi counters with loyalty programs, in-app credits and ecosystem links (food delivery, payments), and reported 2024 monthly active users of 400M to slow churn, but short-term promotions still drive frequent switches.

Price Sensitivity in Urban Markets

A large share of DiDi’s urban riders are daily commuters highly price-sensitive; a 2024 McKinsey mobility study found 62% of urban riders switch modes if ride fares rise 10%+. When DiDi cut subsidies in mid-2023, weekly active users in China fell ~8% month-over-month, showing churn to public transit and bikes. That dynamic forces persistent discounts: DiDi reported marketing spend of ¥18.3 billion (2024) to protect volume and market share.

Influence of Platform Aggregators

Third-party aggregators like Meituan Maps and Amap in China and global players such as Google Maps let users compare ride prices in real time, raising customer bargaining power; a 2024 survey found 42% of urban Chinese riders used aggregators to pick services.

These apps surface transparent ETAs and fares, so buyers pick the cheapest or fastest option; DiDi lost price advantage in some routes where aggregator-listed competitors undercut fares by 8–12% in 2024.

To stay competitive DiDi must keep API uptime >99.9% and latency <200 ms for aggregator calls; otherwise visibility and trip share drop quickly.

Corporate and Institutional Client Leverage

- Large accounts >$5M ARR: steep discounts

- Require custom reports, dedicated support, strict SLAs

- Contract loss can cut regional B2B revenue 10–25%

Demand for Safety and Service Quality

Post-2025 regulatory fallout raised rider expectations: 78% of Chinese consumers say safety and data privacy are deal-breakers (China Consumer Safety Survey, Jan 2025), so DiDi faces high churn risk after any incident.

Buyers quickly abandon platforms after breaches; DiDi saw a 12% weekday active-user drop after its 2021 security crisis, illustrating immediate reputational and revenue pain.

DiDi must keep investing in safety tech and privacy controls; failing to do so risks recurring user loss and higher compliance costs, squeezing margins.

- 78% of users: safety/privacy deal-breaker (Jan 2025)

- 12% DAU drop after 2021 crisis

- Ongoing investment raises operating costs, protects revenue

Price-sensitive riders and safety fears force DiDi into massive marketing and discounts

Buyers have high power: low switching costs (70% choose by wait/price, 2024), aggregator use 42% (2024), and price-sensitivity (62% switch if fares +10%, McKinsey 2024) force DiDi into heavy marketing (¥18.3B, 2024) and retention investments; enterprise clients (> $5M ARR) get steep discounts and can swing regional B2B revenue 10–25%; 78% cite safety/privacy as deal-breakers (Jan 2025).

| Metric | Value |

|---|---|

| Urban users choosing by wait/price | 70% |

| Aggregator use | 42% |

| Switch if fares +10% | 62% |

| Marketing spend (2024) | ¥18.3B |

| Safety/privacy deal-breaker (Jan 2025) | 78% |

Same Document Delivered

DiDi Global Porter's Five Forces Analysis

This preview shows the exact DiDi Global Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

DiDi Global faces intense rivalry from global and local ride-hailing rivals, regulatory headwinds, and shifting consumer preferences that pressure margins and growth—while its data assets and scale offer defensive advantages; this snapshot highlights key tensions but omits force-by-force ratings and strategic implications. Unlock the full Porter's Five Forces Analysis to get detailed ratings, visuals, and actionable insights for investment or strategic planning.

Suppliers Bargaining Power

Fragmented Driver Labor Force

The primary suppliers are millions of individual drivers who provide labor and vehicles; DiDi reported about 31 million drivers in China in 2023, so suppliers are highly fragmented and lack formal bargaining power.

Still, driver power rises during labor shortages or fuel spikes—e.g., China diesel rose ~18% in 2022–23—forcing higher incentives.

DiDi must balance commission cuts and targeted bonuses; in 2024 it spent roughly 6–9% of gross transaction value on driver incentives to retain supply.

Mapping and Cloud Infrastructure Providers

DiDi depends on advanced mapping and cloud compute for real-time routing; in 2024 DiDi processed billions of daily location events, so latency matters. Fewer than five global-tier providers (eg, Alibaba Cloud, Huawei Cloud) can scale at that level, giving suppliers moderate bargaining power reflected in cloud spend—DiDi reported infrastructure costs of RMB 5.2 billion in FY2024. Any outage would sharply halt driver-passenger matching and revenue flow.

Automotive Manufacturers and Fleet Partners

As DiDi shifts to EV fleets, dependence on automakers like BYD rises—BYD supplied ~100,000 EVs to Chinese fleets in 2024, giving manufacturers leverage on unit pricing and maintenance contracts for managed fleets.

Suppliers set terms on warranties and telematics; that matters because DiDi operated ~6 million rides/day in 2024, so scale lets DiDi secure bulk discounts, volume rebates and co-development deals reducing per-vehicle cost by an estimated 8–12%.

Energy and Charging Network Operators

Energy and charging network operators gained outsized supplier power as green-mobility targets push fleets electric by end-2025; global EV charging installed base grew ~60% in 2024 to 6.9M chargers, tightening access and raising prices for third-party use.

DiDi’s reliance on external stations directly affects per-ride energy costs and uptime, so operators can influence margins via tariffs and availability.

DiDi reduces exposure by investing in joint-venture charging hubs—reported CAPEX stake ~USD 120m in 2023–24—securing priority access and lower kWh rates.

- Charging supply concentrated: top 5 operators ~45% market share

- DiDi JV CAPEX ~USD 120m (2023–24)

- Installed chargers 6.9M in 2024, +60% YoY

Financial and Insurance Service Providers

DiDi needs specialized driver insurance and integrated payment processing; in 2024 its financial arm handled about $9.2B in payments but still relies on major banks and gateways for cross-border flows.

Regulatory mandates for comprehensive driver coverage make banks and insurers essential partners, giving them steady bargaining power despite DiDi’s internal capabilities.

Here’s the quick math: 65% of cross-border settlements routed via 3 global gateways in 2024, increasing supplier leverage.

- 2024 payments processed: ~$9.2B

- 65% cross-border via top 3 gateways

- Regulatory insurance mandates boost insurer role

- Major banks control FX and settlement rails

Driver supply vs rising leverage: incentives, infra & EV CAPEX reshape mobility margins

Suppliers: fragmented driver base (~31M drivers in China, 2023) gives low bargaining power, but shortages/fuel spikes raise leverage; DiDi spent ~6–9% of GTV on driver incentives in 2024. Cloud/telecom (few providers) and automakers (e.g., BYD ~100k EVs to fleets in 2024) hold moderate power; infrastructure costs RMB 5.2B FY2024; JV charging CAPEX ~USD120M (2023–24).

| Item | 2023–24 |

|---|---|

| Drivers (China) | 31M (2023) |

| Driver incentives | 6–9% GTV (2024) |

| Infra costs | RMB 5.2B (FY2024) |

| BYD EV supply | ~100k (2024) |

| JV charging CAPEX | USD 120M (2023–24) |

What is included in the product

Tailored Porter's Five Forces for DiDi Global, revealing competitive intensity, buyer/supplier leverage, threat of entrants and substitutes, and strategic levers to defend market share and margins.

Clear, one-sheet Porter's Five Forces for DiDi Global—instantly shows competitive pressures and regulatory risks to speed strategic decisions.

Customers Bargaining Power

Low Switching Costs for Individual Riders

Individual riders face low switching costs among apps like DiDi, Meituan, and T3 Go, raising buyer power as 70% of urban users in China (2024 survey) report choosing by wait time or price.

DiDi counters with loyalty programs, in-app credits and ecosystem links (food delivery, payments), and reported 2024 monthly active users of 400M to slow churn, but short-term promotions still drive frequent switches.

Price Sensitivity in Urban Markets

A large share of DiDi’s urban riders are daily commuters highly price-sensitive; a 2024 McKinsey mobility study found 62% of urban riders switch modes if ride fares rise 10%+. When DiDi cut subsidies in mid-2023, weekly active users in China fell ~8% month-over-month, showing churn to public transit and bikes. That dynamic forces persistent discounts: DiDi reported marketing spend of ¥18.3 billion (2024) to protect volume and market share.

Influence of Platform Aggregators

Third-party aggregators like Meituan Maps and Amap in China and global players such as Google Maps let users compare ride prices in real time, raising customer bargaining power; a 2024 survey found 42% of urban Chinese riders used aggregators to pick services.

These apps surface transparent ETAs and fares, so buyers pick the cheapest or fastest option; DiDi lost price advantage in some routes where aggregator-listed competitors undercut fares by 8–12% in 2024.

To stay competitive DiDi must keep API uptime >99.9% and latency <200 ms for aggregator calls; otherwise visibility and trip share drop quickly.

Corporate and Institutional Client Leverage

- Large accounts >$5M ARR: steep discounts

- Require custom reports, dedicated support, strict SLAs

- Contract loss can cut regional B2B revenue 10–25%

Demand for Safety and Service Quality

Post-2025 regulatory fallout raised rider expectations: 78% of Chinese consumers say safety and data privacy are deal-breakers (China Consumer Safety Survey, Jan 2025), so DiDi faces high churn risk after any incident.

Buyers quickly abandon platforms after breaches; DiDi saw a 12% weekday active-user drop after its 2021 security crisis, illustrating immediate reputational and revenue pain.

DiDi must keep investing in safety tech and privacy controls; failing to do so risks recurring user loss and higher compliance costs, squeezing margins.

- 78% of users: safety/privacy deal-breaker (Jan 2025)

- 12% DAU drop after 2021 crisis

- Ongoing investment raises operating costs, protects revenue

Price-sensitive riders and safety fears force DiDi into massive marketing and discounts

Buyers have high power: low switching costs (70% choose by wait/price, 2024), aggregator use 42% (2024), and price-sensitivity (62% switch if fares +10%, McKinsey 2024) force DiDi into heavy marketing (¥18.3B, 2024) and retention investments; enterprise clients (> $5M ARR) get steep discounts and can swing regional B2B revenue 10–25%; 78% cite safety/privacy as deal-breakers (Jan 2025).

| Metric | Value |

|---|---|

| Urban users choosing by wait/price | 70% |

| Aggregator use | 42% |

| Switch if fares +10% | 62% |

| Marketing spend (2024) | ¥18.3B |

| Safety/privacy deal-breaker (Jan 2025) | 78% |

Same Document Delivered

DiDi Global Porter's Five Forces Analysis

This preview shows the exact DiDi Global Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for use.