D'Ieteren Porter's Five Forces Analysis

Don't Miss the Bigger Picture

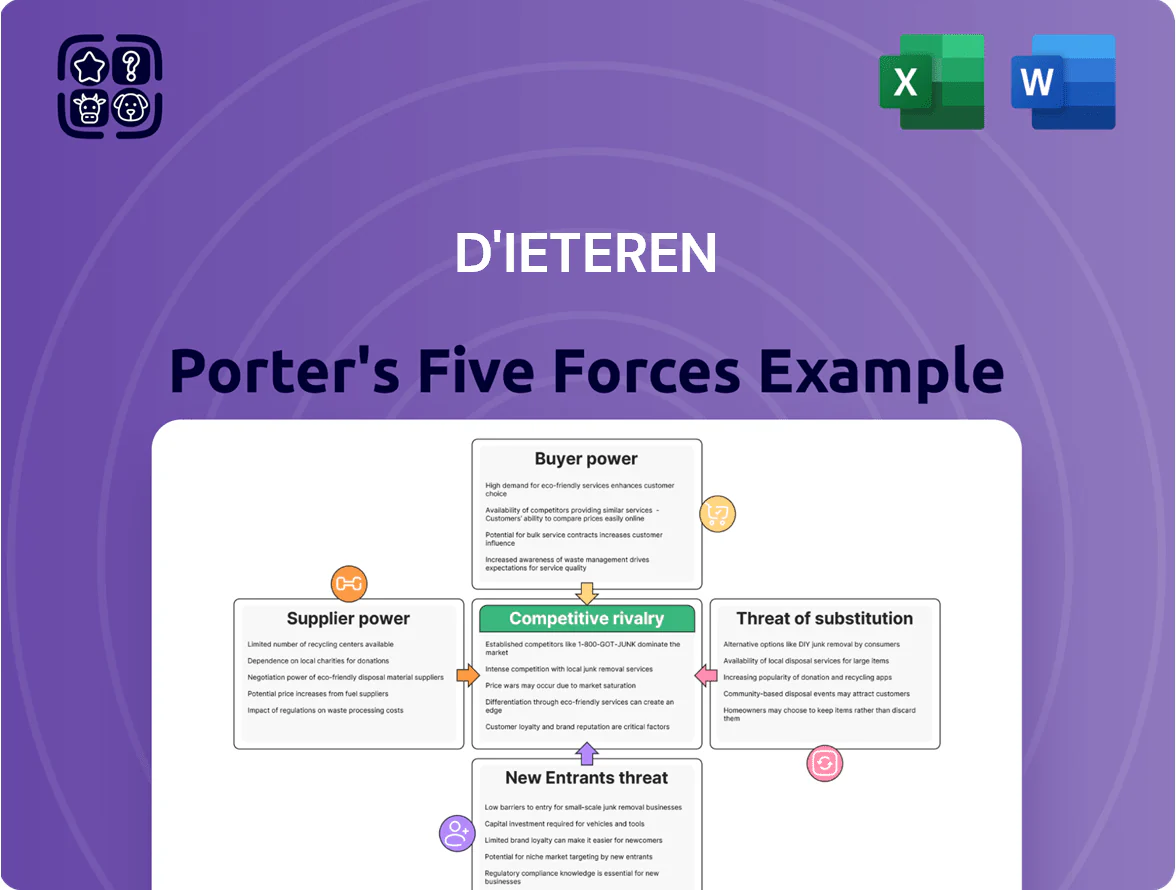

D'Ieteren faces a mix of supplier leverage, moderate buyer power, and evolving substitute threats tied to mobility shifts; competitive rivalry is shaped by scale advantages and after-sales networks while entry barriers remain niche-specific. This snapshot highlights strategic pressure points and growth levers for the group. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals and actionable implications for investment or strategy.

Suppliers Bargaining Power

Concentration of Volkswagen Group as a key principal

The automotive division depends on an exclusive Volkswagen Group (VW AG) distribution deal for Audi, Porsche and VW in Belgium, creating supplier leverage over SKU mix, pricing and inventory flows; VW Group reported €279.2bn revenue in 2024, signalling strong upstream bargaining power.

Supplier control extends to EV transition timing: VW committed €88bn to electrification through 2026, so D'Ieteren’s EV stock cadence mirrors VW’s rollout and allocation choices.

By late 2025 VW’s move to agency models (already piloted across EU markets) shifts margins and direct customer data to the manufacturer, reducing distributor gross margin and pricing autonomy for D'Ieteren.

Technological complexity of ADAS glass components

The growing complexity of ADAS (advanced driver assistance systems) glass means only a few global suppliers—led by AGC, Saint-Gobain, and Nippon Sheet Glass—can produce sensor-integrated panes at scale, giving them pricing power over Belron’s safety-recalibration services. In 2024 certified ADAS-capable glass accounted for an estimated 30–40% of new-vehicle glass value, boosting higher-margin repair revenue for Belron. Limited alternative sourcing and long qualification cycles (6–12 months) raise supplier leverage and input-cost risk.

Consolidation of industrial spare parts manufacturers

Supplier consolidation in industrial spare parts is rising: top 5 global component makers grew market share to ~48% by 2024, reducing vendor choices for TVH Parts within D'Ieteren and pressuring niche mechanical part prices.

D'Ieteren offsets this by using its ~€2.1bn 2024 distribution volume and global reach to remain a preferred partner, securing long‑term supply agreements and volume discounts to limit procurement cost increases.

Sourcing of sustainable raw materials for Moleskine

Moleskine faces rising supplier pressure as European environmental rules tightening by 2025 raise costs for FSC-certified paper and premium sustainable materials, with only about 30 high-quality, ethically compliant paper mills in Europe giving suppliers pricing power.

Suppliers can pass on higher energy and compliance costs—European paper producers saw a 12–18% rise in production costs in 2023–24—squeezing Moleskine margins unless it absorbs costs or raises prices.

Maintaining Moleskine’s premium positioning requires steady access to these specific materials, so any mill shutdowns or export constraints make the brand vulnerable to supply interruptions and stock shortages.

- ~30 compliant mills in Europe; 12–18% cost rise 2023–24

- Suppliers hold pricing power; margin pressure if costs passed on

- Supply disruptions risk premium inventory shortages

Energy and logistics providers for distribution networks

D'Ieteren’s large logistics for vehicles and spare parts are exposed to energy and shipping price moves; EU carbon tax hikes by 2025 raised carrier fuel and compliance costs, pushing freight rates up ~8–12% in 2024–25.

Because D'Ieteren depends on third-party fleets for timely global delivery, these providers hold indirect bargaining power that can compress margins and force higher working-capital needs.

- Freight rate rise: ~8–12% (2024–25)

- EU carbon levy effective 2025

- Higher carrier pricing → margin pressure

- Third-party reliance → limited switchability

Supplier power bites margins: VW scale, ADAS glass oligopoly & paper cost squeeze

Suppliers wield significant leverage: VW Group’s €279.2bn revenue (2024) and €88bn electrification spend to 2026 tie D'Ieteren to OEM pricing, rollout and agency-model margin shifts; ADAS glass oligopoly (AGC, Saint‑Gobain, NSG) makes 30–40% of new-glass value ADAS-capable (2024), raising Belron costs; ~30 EU FSC mills and 12–18% paper cost rise (2023–24) squeeze Moleskine margins.

| Metric | Value |

|---|---|

| VW revenue (2024) | €279.2bn |

| VW electrification spend | €88bn to 2026 |

| ADAS glass share (value) | 30–40% |

| EU FSC mills | ~30 |

| Paper cost rise | 12–18% |

What is included in the product

Tailored Porter's Five Forces analysis for D'Ieteren that uncovers competitive intensity, supplier and buyer power, threats from substitutes and new entrants, and identifies disruptive trends and strategic levers to protect margins and market share.

A concise Porter’s Five Forces snapshot for D'Ieteren—quickly highlights supplier, buyer, entrant, substitute, and rivalry pressures to speed strategic decisions.

Customers Bargaining Power

Influence of major insurance and fleet companies

A substantial share of Belron’s revenue comes from large insurers and fleet managers demanding standardized global pricing; these clients account for roughly 40–50% of group sales in 2024, giving them strong bargaining power. They steer high volumes to preferred providers via cost and SLA terms, forcing price concessions. By end-2025 many use digital platforms to compare repair quotes in real time, squeezing margins and pressuring Belron to digitize pricing and reduce unit costs.

Shift toward consumer agency models in automotive sales

Individual Belgian buyers gain transparency from online configurators and direct-to-consumer EV sales (Tesla, 12% BE EV market 2024), shrinking D'Ieteren Automotive’s ability to hold traditional dealership margins as customers demand price parity across regions.

Extensive online reviews and comparison platforms increase buyer leverage, while third-party financing (captive finance share down to ~35% in 2024) decouples purchase from service, raising price sensitivity and reducing upsell opportunities.

B2B demand for uptime and reliability in industrial parts

Customers of TVH Parts—repair shops and industrial fleet operators—value uptime and same-day/next-day availability more than lowest price, with 68% of industrial buyers in Europe (2024 Eurostat buyer survey) citing delivery speed as primary procurement criterion; fragmented numbers reduce collective bargaining but raise churn risk if stockouts occur.

Brand loyalty versus price sensitivity in luxury stationery

Moleskine buyers show lower price sensitivity thanks to lifestyle positioning; the brand commands ~15–25% price premiums vs mass notebooks and repeat purchase rates near 40% in premium segments (2024 data), but customers wield strong influence over brand perception via social media.

High-quality digital note apps (Notion, Apple Notes, GoodNotes) and smart notebooks raise switching risk: if Moleskine misses product innovation or premium feel, migration is easy.

By 2025 customers expect seamless omnichannel buying; studies show 68% abandon purchase after friction, giving them leverage to choose rival lifestyle brands.

- Low price sensitivity: ~15–25% premium

- High brand power: strong social-media influence

- Switch risk: rising digital alternatives

- Omnichannel demand: 68% abandonment vs friction

Government and public sector procurement for green mobility

Government and public-sector procurement and large corporates with ESG targets are high-volume buyers for D'Ieteren's green mobility services, often driving contracts worth tens to hundreds of millions—EU public procurement of EV fleets rose 28% in 2024.

These buyers use competitive tenders with strict emissions and price criteria, forcing D'Ieteren to redesign offerings, meet ISO 14001-like standards, and compress margins to secure 5–10 year institutional contracts.

- High-volume demand: municipal and corporate fleets

- Tenders: strict ESG + price thresholds

- Margin impact: longer contracts, tighter pricing

- 2024 stat: EU public EV procurement +28%

Buyers reshape margins: insurers, EVs, uptime and premium brands squeeze pricing

Large insurers/fleets drive 40–50% of Belron sales (2024), forcing price/SLA cuts; digital quoting by 2025 compresses margins. Retail auto buyers (Tesla 12% BE EV 2024) and online tools erode dealership margins. TVH customers prioritize uptime—68% cite delivery speed (2024). Moleskine holds 15–25% price premium and ~40% repeat rate (2024) but faces digital note app churn.

| Buyer | Key stat |

|---|---|

| Insurers/Fleets | 40–50% sales (2024) |

| Tesla BE | 12% EV market (2024) |

| TVH buyers | 68% delivery priority (2024) |

| Moleskine | 15–25% premium; ~40% repeat (2024) |

What You See Is What You Get

D'Ieteren Porter's Five Forces Analysis

This preview shows the exact D'Ieteren Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—fully formatted, downloadable, and ready for use the moment you buy.

You're looking at the actual, final analysis file; once you complete payment, you’ll get instant access to this identical document for immediate application.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

D'Ieteren faces a mix of supplier leverage, moderate buyer power, and evolving substitute threats tied to mobility shifts; competitive rivalry is shaped by scale advantages and after-sales networks while entry barriers remain niche-specific. This snapshot highlights strategic pressure points and growth levers for the group. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals and actionable implications for investment or strategy.

Suppliers Bargaining Power

Concentration of Volkswagen Group as a key principal

The automotive division depends on an exclusive Volkswagen Group (VW AG) distribution deal for Audi, Porsche and VW in Belgium, creating supplier leverage over SKU mix, pricing and inventory flows; VW Group reported €279.2bn revenue in 2024, signalling strong upstream bargaining power.

Supplier control extends to EV transition timing: VW committed €88bn to electrification through 2026, so D'Ieteren’s EV stock cadence mirrors VW’s rollout and allocation choices.

By late 2025 VW’s move to agency models (already piloted across EU markets) shifts margins and direct customer data to the manufacturer, reducing distributor gross margin and pricing autonomy for D'Ieteren.

Technological complexity of ADAS glass components

The growing complexity of ADAS (advanced driver assistance systems) glass means only a few global suppliers—led by AGC, Saint-Gobain, and Nippon Sheet Glass—can produce sensor-integrated panes at scale, giving them pricing power over Belron’s safety-recalibration services. In 2024 certified ADAS-capable glass accounted for an estimated 30–40% of new-vehicle glass value, boosting higher-margin repair revenue for Belron. Limited alternative sourcing and long qualification cycles (6–12 months) raise supplier leverage and input-cost risk.

Consolidation of industrial spare parts manufacturers

Supplier consolidation in industrial spare parts is rising: top 5 global component makers grew market share to ~48% by 2024, reducing vendor choices for TVH Parts within D'Ieteren and pressuring niche mechanical part prices.

D'Ieteren offsets this by using its ~€2.1bn 2024 distribution volume and global reach to remain a preferred partner, securing long‑term supply agreements and volume discounts to limit procurement cost increases.

Sourcing of sustainable raw materials for Moleskine

Moleskine faces rising supplier pressure as European environmental rules tightening by 2025 raise costs for FSC-certified paper and premium sustainable materials, with only about 30 high-quality, ethically compliant paper mills in Europe giving suppliers pricing power.

Suppliers can pass on higher energy and compliance costs—European paper producers saw a 12–18% rise in production costs in 2023–24—squeezing Moleskine margins unless it absorbs costs or raises prices.

Maintaining Moleskine’s premium positioning requires steady access to these specific materials, so any mill shutdowns or export constraints make the brand vulnerable to supply interruptions and stock shortages.

- ~30 compliant mills in Europe; 12–18% cost rise 2023–24

- Suppliers hold pricing power; margin pressure if costs passed on

- Supply disruptions risk premium inventory shortages

Energy and logistics providers for distribution networks

D'Ieteren’s large logistics for vehicles and spare parts are exposed to energy and shipping price moves; EU carbon tax hikes by 2025 raised carrier fuel and compliance costs, pushing freight rates up ~8–12% in 2024–25.

Because D'Ieteren depends on third-party fleets for timely global delivery, these providers hold indirect bargaining power that can compress margins and force higher working-capital needs.

- Freight rate rise: ~8–12% (2024–25)

- EU carbon levy effective 2025

- Higher carrier pricing → margin pressure

- Third-party reliance → limited switchability

Supplier power bites margins: VW scale, ADAS glass oligopoly & paper cost squeeze

Suppliers wield significant leverage: VW Group’s €279.2bn revenue (2024) and €88bn electrification spend to 2026 tie D'Ieteren to OEM pricing, rollout and agency-model margin shifts; ADAS glass oligopoly (AGC, Saint‑Gobain, NSG) makes 30–40% of new-glass value ADAS-capable (2024), raising Belron costs; ~30 EU FSC mills and 12–18% paper cost rise (2023–24) squeeze Moleskine margins.

| Metric | Value |

|---|---|

| VW revenue (2024) | €279.2bn |

| VW electrification spend | €88bn to 2026 |

| ADAS glass share (value) | 30–40% |

| EU FSC mills | ~30 |

| Paper cost rise | 12–18% |

What is included in the product

Tailored Porter's Five Forces analysis for D'Ieteren that uncovers competitive intensity, supplier and buyer power, threats from substitutes and new entrants, and identifies disruptive trends and strategic levers to protect margins and market share.

A concise Porter’s Five Forces snapshot for D'Ieteren—quickly highlights supplier, buyer, entrant, substitute, and rivalry pressures to speed strategic decisions.

Customers Bargaining Power

Influence of major insurance and fleet companies

A substantial share of Belron’s revenue comes from large insurers and fleet managers demanding standardized global pricing; these clients account for roughly 40–50% of group sales in 2024, giving them strong bargaining power. They steer high volumes to preferred providers via cost and SLA terms, forcing price concessions. By end-2025 many use digital platforms to compare repair quotes in real time, squeezing margins and pressuring Belron to digitize pricing and reduce unit costs.

Shift toward consumer agency models in automotive sales

Individual Belgian buyers gain transparency from online configurators and direct-to-consumer EV sales (Tesla, 12% BE EV market 2024), shrinking D'Ieteren Automotive’s ability to hold traditional dealership margins as customers demand price parity across regions.

Extensive online reviews and comparison platforms increase buyer leverage, while third-party financing (captive finance share down to ~35% in 2024) decouples purchase from service, raising price sensitivity and reducing upsell opportunities.

B2B demand for uptime and reliability in industrial parts

Customers of TVH Parts—repair shops and industrial fleet operators—value uptime and same-day/next-day availability more than lowest price, with 68% of industrial buyers in Europe (2024 Eurostat buyer survey) citing delivery speed as primary procurement criterion; fragmented numbers reduce collective bargaining but raise churn risk if stockouts occur.

Brand loyalty versus price sensitivity in luxury stationery

Moleskine buyers show lower price sensitivity thanks to lifestyle positioning; the brand commands ~15–25% price premiums vs mass notebooks and repeat purchase rates near 40% in premium segments (2024 data), but customers wield strong influence over brand perception via social media.

High-quality digital note apps (Notion, Apple Notes, GoodNotes) and smart notebooks raise switching risk: if Moleskine misses product innovation or premium feel, migration is easy.

By 2025 customers expect seamless omnichannel buying; studies show 68% abandon purchase after friction, giving them leverage to choose rival lifestyle brands.

- Low price sensitivity: ~15–25% premium

- High brand power: strong social-media influence

- Switch risk: rising digital alternatives

- Omnichannel demand: 68% abandonment vs friction

Government and public sector procurement for green mobility

Government and public-sector procurement and large corporates with ESG targets are high-volume buyers for D'Ieteren's green mobility services, often driving contracts worth tens to hundreds of millions—EU public procurement of EV fleets rose 28% in 2024.

These buyers use competitive tenders with strict emissions and price criteria, forcing D'Ieteren to redesign offerings, meet ISO 14001-like standards, and compress margins to secure 5–10 year institutional contracts.

- High-volume demand: municipal and corporate fleets

- Tenders: strict ESG + price thresholds

- Margin impact: longer contracts, tighter pricing

- 2024 stat: EU public EV procurement +28%

Buyers reshape margins: insurers, EVs, uptime and premium brands squeeze pricing

Large insurers/fleets drive 40–50% of Belron sales (2024), forcing price/SLA cuts; digital quoting by 2025 compresses margins. Retail auto buyers (Tesla 12% BE EV 2024) and online tools erode dealership margins. TVH customers prioritize uptime—68% cite delivery speed (2024). Moleskine holds 15–25% price premium and ~40% repeat rate (2024) but faces digital note app churn.

| Buyer | Key stat |

|---|---|

| Insurers/Fleets | 40–50% sales (2024) |

| Tesla BE | 12% EV market (2024) |

| TVH buyers | 68% delivery priority (2024) |

| Moleskine | 15–25% premium; ~40% repeat (2024) |

What You See Is What You Get

D'Ieteren Porter's Five Forces Analysis

This preview shows the exact D'Ieteren Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—fully formatted, downloadable, and ready for use the moment you buy.

You're looking at the actual, final analysis file; once you complete payment, you’ll get instant access to this identical document for immediate application.