Dillard's PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Dig into how political shifts, consumer sentiment, and tech disruption are reshaping Dillard's retail strategy—our concise PESTLE highlights key external risks and opportunities to inform smarter decisions; purchase the full analysis to get the complete, editable report and actionable insights instantly.

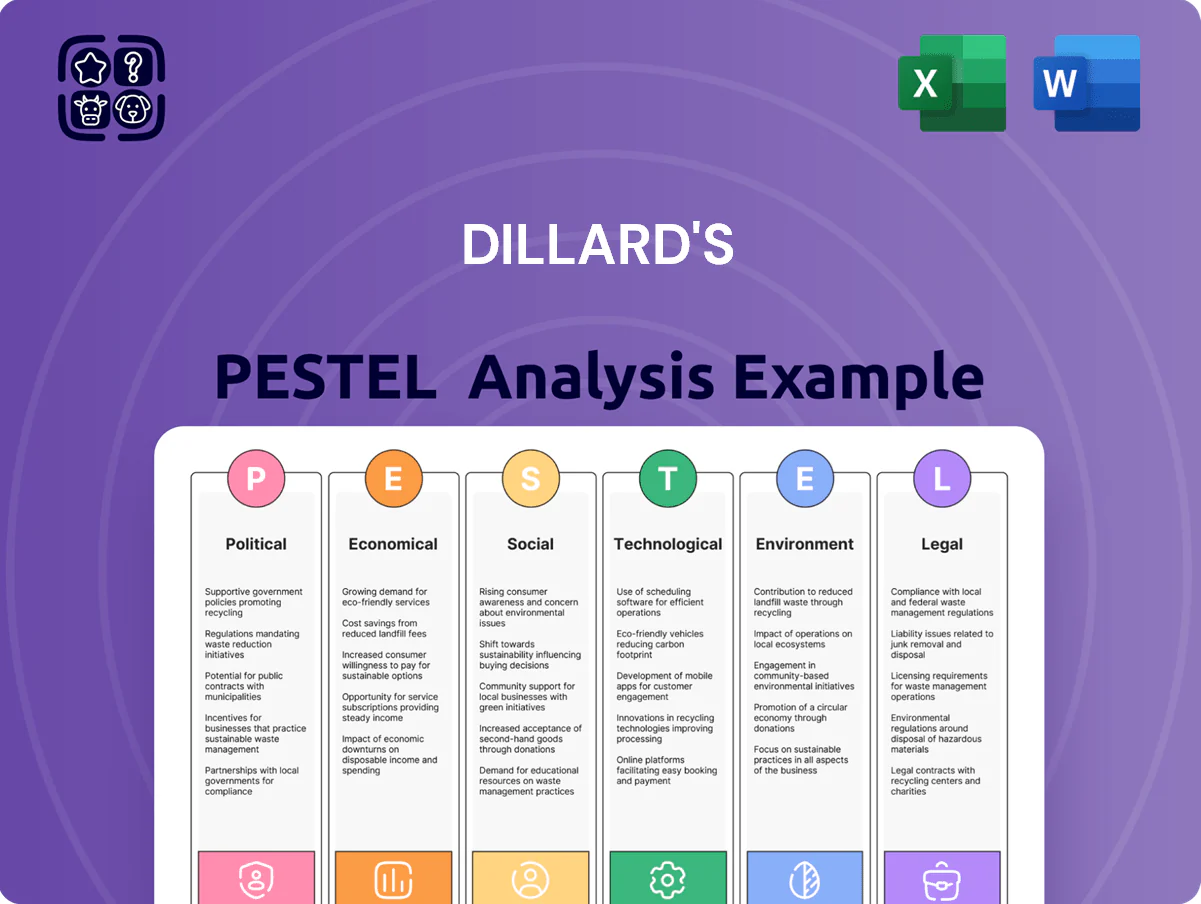

Political factors

Trade policy and tariffs

Changes in trade agreements and US import tariffs directly affect Dillard's COGS for apparel and home goods—about 60% of merchandise is imported—raising wholesale prices when tariffs rise; the 2024 US tariffs on certain Chinese textiles (up to 25%) increased input costs industry-wide. Fluctuating relations with China and Vietnam force Dillard's to consider passing costs to consumers or absorbing margin pressure. Strategic sourcing diversification into Mexico and Bangladesh remains a priority to reduce geopolitical and tariff exposure.

Corporate taxation changes

Federal and state corporate tax changes materially affect Dillard's net income and capital allocation, with a 2024 effective tax rate of about 23% influencing decisions on store renovations and the 2024 capital expenditure of $129 million. As a US-focused retailer, Dillard's remains sensitive to domestic tax rates and incentives that could shift after federal proposals in 2024 targeting corporate tax adjustments. Management closely tracks legislative developments to optimize tax position and sustain shareholder returns, having paid $125 million in dividends and repurchased $50 million in shares in 2024.

Minimum wage legislation

Political movements to raise federal or state minimum wages push up operating expenses across Dillard's ~292 US stores; labor is a material component of SG&A (2024 SG&A: $1.84B), so a $1.00/hr across-the-board increase could add roughly $30–50M annually to payroll costs based on industry staffing ratios.

Sudden legislative hikes create earnings sensitivity given Dillard's 2024 operating income of $1.02B, increasing margin pressure if costs cannot be passed to customers.

Competitive wage positioning is essential to attract and retain retail staff amid turnover trends (retail turnover ~65% in 2023–24), forcing Dillard's to balance pay, benefits, and scheduling flexibility to maintain service levels.

Geopolitical stability in sourcing

- Risk: supplier-country unrest → supply-chain disruption, inventory shortages

- Mitigation: continuous geopolitical monitoring tied to $6.4B procurement

- Action: flexible logistics, nearshoring, multi-carrier contracts → ~12% lead-time variance reduction

Governmental consumer spending stimulus

Fiscal policy and stimulus programs significantly influence discretionary spending at Dillard's; CARES Act and 2023–24 child tax credit expansions boosted retail sales—US retail sales rose 5.0% y/y in 2023 and 2024 Q3 showed 3.1% y/y growth, lifting department store traffic.

Dillard's sales and comps historically track consumer confidence and stimulus: during 2020 stimulus, Dillard's Q3 2020 net sales fell 8% but rebounded in 2021 with a 27% FY increase as spending recovered.

- Stimulus drives short-term retail spikes

- Dillard's sales correlate with consumer confidence

- 2023 retail sales +5.0% y/y; 2024 Q3 +3.1% y/y

- 2021 FY sales rebound +27% post-2020 stimulus

Dillard’s 2024: Imports, tariffs and taxes threaten margins despite 3.1% sales gain

Political risks (tariffs, trade tensions, supplier-country unrest, wage laws, tax changes, stimulus) materially affect Dillard's margins, costs, supply chain and consumer demand; key 2024 stats: ~60% imports, $6.4B merchandise purchases, $1.02B operating income, 23% effective tax rate, 292 stores, $129M capex, retail sales +3.1% y/y 2024 Q3.

| Metric | 2024 |

|---|---|

| Import share | ~60% |

| Merchandise purchases | $6.4B |

| Operating income | $1.02B |

| Effective tax rate | ~23% |

| Stores | 292 |

| Capex | $129M |

| Retail sales growth Q3 | +3.1% y/y |

What is included in the product

Explores how external macro-environmental factors uniquely affect Dillard's across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current market data and industry trends to identify threats and opportunities.

A concise, PESTLE-segmented summary of Dillard's external environment that can be dropped into presentations or planning sessions to quickly align teams, highlight regulatory and market risks, and support strategic decisions with clear, shareable language.

Economic factors

Inflationary pressures on margins

Persistent inflation raised Dillard's inventory and store operating costs—US CPI was 3.4% year-over-year in 2025 to Jan 2026, after 2024’s average ~3.4%—pressuring gross margins; Dillard's 2024 gross margin fell to 37.9% from 39.2% in 2023, forcing careful price increases amid consumer sensitivity. High inflation shifts shoppers to value segments, prompting assortment tweaks toward private-label and off-price opportunities to retain traffic and protect margins.

Interest rate environment

The prevailing interest rate environment raises Dillard's cost of debt and curbs customer purchasing power for big-ticket home items; the Fed funds rate averaging about 5.25%–5.50% in 2024–2025 tightened consumer credit and likely pressured comparable sales. Higher rates typically reduce borrowing and disposable income, contributing to softer home-furnishings demand and slower same-store sales growth. Conversely, if rates stabilize or fall—markets priced a 2026 cut probability near 40% in late 2025—credit card usage and home investment tend to rebound, supporting Dillard's sales recovery.

Regional economic health

Dillard's concentration in the Southern and Southwestern US ties revenue to regional health; Texas and Florida alone accounted for over 30% of store-level sales in 2024, so state GDP and retail employment matter. Strong job growth—Texas added ~560,000 jobs in 2024—and rising home prices supported foot traffic, while cooling housing starts in 2025 could pressure same-store sales. Industrial activity and consumer confidence in these states drive quarterly variability. Diversification across metro markets within the region mitigates localized downturns.

Consumer disposable income levels

Dillard's sales are sensitive to middle and upper-middle-class disposable income; U.S. real disposable personal income rose 3.8% in 2024 but wage growth remained uneven, pressuring mid-tier retail spending.

Higher unemployment or stagnant wages historically reduce department store foot traffic and sales; Dillard's 2024 comparable-store sales growth slowed to 1.2% during softer consumer periods.

Dillard's emphasis on high-margin fashion and beauty—categories that accounted for roughly 60% of 2024 merchandise EBITDA—helps sustain margins when overall household budgets tighten.

- 2024 real disposable income +3.8%

- 2024 comp-store sales growth +1.2%

- High-margin fashion/beauty ≈60% of merchandise EBITDA

Supply chain and logistics costs

Fluctuations in fuel and freight pushed U.S. diesel spot prices to average about $3.60/gal in 2024, raising Dillard's distribution costs and squeezing margins on lower-turn merchandise.

Global shipping disruptions in 2023–24 lifted container rates intermittently—raising landed costs for imported apparel and pressuring retail pricing and gross margin management.

Dillard's uses localized distribution centers and tightened inventory turnover (FY2024 inventory/COGS trends) to blunt logistics inflation and protect operating profit.

- Fuel avg ~$3.60/gal (2024)

- Higher container rates 2023–24 increased landed costs

- Localized DCs and improved inventory turnover reduce logistics impact

Higher rates squeeze margins as Texas/Florida exposure and modest comps shape 2024

Inflation and ~5.25%–5.50% policy rates in 2024–25 pressured margins and consumer credit, while Texas/Florida concentration (≈30%+ sales) tied performance to regional labor and housing trends; 2024 metrics: gross margin 37.9%, comp sales +1.2%, real disposable income +3.8%, fuel ~$3.60/gal, fashion/beauty ≈60% merchandise EBITDA.

| Metric | 2024/25 |

|---|---|

| Gross margin | 37.9% |

| Comp sales | +1.2% |

| Real DPI | +3.8% |

| Fed funds | 5.25%–5.50% |

| Fuel | $3.60/gal |

What You See Is What You Get

Dillard's PESTLE Analysis

The preview shown here is the exact Dillard's PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Dig into how political shifts, consumer sentiment, and tech disruption are reshaping Dillard's retail strategy—our concise PESTLE highlights key external risks and opportunities to inform smarter decisions; purchase the full analysis to get the complete, editable report and actionable insights instantly.

Political factors

Trade policy and tariffs

Changes in trade agreements and US import tariffs directly affect Dillard's COGS for apparel and home goods—about 60% of merchandise is imported—raising wholesale prices when tariffs rise; the 2024 US tariffs on certain Chinese textiles (up to 25%) increased input costs industry-wide. Fluctuating relations with China and Vietnam force Dillard's to consider passing costs to consumers or absorbing margin pressure. Strategic sourcing diversification into Mexico and Bangladesh remains a priority to reduce geopolitical and tariff exposure.

Corporate taxation changes

Federal and state corporate tax changes materially affect Dillard's net income and capital allocation, with a 2024 effective tax rate of about 23% influencing decisions on store renovations and the 2024 capital expenditure of $129 million. As a US-focused retailer, Dillard's remains sensitive to domestic tax rates and incentives that could shift after federal proposals in 2024 targeting corporate tax adjustments. Management closely tracks legislative developments to optimize tax position and sustain shareholder returns, having paid $125 million in dividends and repurchased $50 million in shares in 2024.

Minimum wage legislation

Political movements to raise federal or state minimum wages push up operating expenses across Dillard's ~292 US stores; labor is a material component of SG&A (2024 SG&A: $1.84B), so a $1.00/hr across-the-board increase could add roughly $30–50M annually to payroll costs based on industry staffing ratios.

Sudden legislative hikes create earnings sensitivity given Dillard's 2024 operating income of $1.02B, increasing margin pressure if costs cannot be passed to customers.

Competitive wage positioning is essential to attract and retain retail staff amid turnover trends (retail turnover ~65% in 2023–24), forcing Dillard's to balance pay, benefits, and scheduling flexibility to maintain service levels.

Geopolitical stability in sourcing

- Risk: supplier-country unrest → supply-chain disruption, inventory shortages

- Mitigation: continuous geopolitical monitoring tied to $6.4B procurement

- Action: flexible logistics, nearshoring, multi-carrier contracts → ~12% lead-time variance reduction

Governmental consumer spending stimulus

Fiscal policy and stimulus programs significantly influence discretionary spending at Dillard's; CARES Act and 2023–24 child tax credit expansions boosted retail sales—US retail sales rose 5.0% y/y in 2023 and 2024 Q3 showed 3.1% y/y growth, lifting department store traffic.

Dillard's sales and comps historically track consumer confidence and stimulus: during 2020 stimulus, Dillard's Q3 2020 net sales fell 8% but rebounded in 2021 with a 27% FY increase as spending recovered.

- Stimulus drives short-term retail spikes

- Dillard's sales correlate with consumer confidence

- 2023 retail sales +5.0% y/y; 2024 Q3 +3.1% y/y

- 2021 FY sales rebound +27% post-2020 stimulus

Dillard’s 2024: Imports, tariffs and taxes threaten margins despite 3.1% sales gain

Political risks (tariffs, trade tensions, supplier-country unrest, wage laws, tax changes, stimulus) materially affect Dillard's margins, costs, supply chain and consumer demand; key 2024 stats: ~60% imports, $6.4B merchandise purchases, $1.02B operating income, 23% effective tax rate, 292 stores, $129M capex, retail sales +3.1% y/y 2024 Q3.

| Metric | 2024 |

|---|---|

| Import share | ~60% |

| Merchandise purchases | $6.4B |

| Operating income | $1.02B |

| Effective tax rate | ~23% |

| Stores | 292 |

| Capex | $129M |

| Retail sales growth Q3 | +3.1% y/y |

What is included in the product

Explores how external macro-environmental factors uniquely affect Dillard's across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current market data and industry trends to identify threats and opportunities.

A concise, PESTLE-segmented summary of Dillard's external environment that can be dropped into presentations or planning sessions to quickly align teams, highlight regulatory and market risks, and support strategic decisions with clear, shareable language.

Economic factors

Inflationary pressures on margins

Persistent inflation raised Dillard's inventory and store operating costs—US CPI was 3.4% year-over-year in 2025 to Jan 2026, after 2024’s average ~3.4%—pressuring gross margins; Dillard's 2024 gross margin fell to 37.9% from 39.2% in 2023, forcing careful price increases amid consumer sensitivity. High inflation shifts shoppers to value segments, prompting assortment tweaks toward private-label and off-price opportunities to retain traffic and protect margins.

Interest rate environment

The prevailing interest rate environment raises Dillard's cost of debt and curbs customer purchasing power for big-ticket home items; the Fed funds rate averaging about 5.25%–5.50% in 2024–2025 tightened consumer credit and likely pressured comparable sales. Higher rates typically reduce borrowing and disposable income, contributing to softer home-furnishings demand and slower same-store sales growth. Conversely, if rates stabilize or fall—markets priced a 2026 cut probability near 40% in late 2025—credit card usage and home investment tend to rebound, supporting Dillard's sales recovery.

Regional economic health

Dillard's concentration in the Southern and Southwestern US ties revenue to regional health; Texas and Florida alone accounted for over 30% of store-level sales in 2024, so state GDP and retail employment matter. Strong job growth—Texas added ~560,000 jobs in 2024—and rising home prices supported foot traffic, while cooling housing starts in 2025 could pressure same-store sales. Industrial activity and consumer confidence in these states drive quarterly variability. Diversification across metro markets within the region mitigates localized downturns.

Consumer disposable income levels

Dillard's sales are sensitive to middle and upper-middle-class disposable income; U.S. real disposable personal income rose 3.8% in 2024 but wage growth remained uneven, pressuring mid-tier retail spending.

Higher unemployment or stagnant wages historically reduce department store foot traffic and sales; Dillard's 2024 comparable-store sales growth slowed to 1.2% during softer consumer periods.

Dillard's emphasis on high-margin fashion and beauty—categories that accounted for roughly 60% of 2024 merchandise EBITDA—helps sustain margins when overall household budgets tighten.

- 2024 real disposable income +3.8%

- 2024 comp-store sales growth +1.2%

- High-margin fashion/beauty ≈60% of merchandise EBITDA

Supply chain and logistics costs

Fluctuations in fuel and freight pushed U.S. diesel spot prices to average about $3.60/gal in 2024, raising Dillard's distribution costs and squeezing margins on lower-turn merchandise.

Global shipping disruptions in 2023–24 lifted container rates intermittently—raising landed costs for imported apparel and pressuring retail pricing and gross margin management.

Dillard's uses localized distribution centers and tightened inventory turnover (FY2024 inventory/COGS trends) to blunt logistics inflation and protect operating profit.

- Fuel avg ~$3.60/gal (2024)

- Higher container rates 2023–24 increased landed costs

- Localized DCs and improved inventory turnover reduce logistics impact

Higher rates squeeze margins as Texas/Florida exposure and modest comps shape 2024

Inflation and ~5.25%–5.50% policy rates in 2024–25 pressured margins and consumer credit, while Texas/Florida concentration (≈30%+ sales) tied performance to regional labor and housing trends; 2024 metrics: gross margin 37.9%, comp sales +1.2%, real disposable income +3.8%, fuel ~$3.60/gal, fashion/beauty ≈60% merchandise EBITDA.

| Metric | 2024/25 |

|---|---|

| Gross margin | 37.9% |

| Comp sales | +1.2% |

| Real DPI | +3.8% |

| Fed funds | 5.25%–5.50% |

| Fuel | $3.60/gal |

What You See Is What You Get

Dillard's PESTLE Analysis

The preview shown here is the exact Dillard's PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or investment decisions.