Dime Community Bank Business Model Canvas

Dime Community Bank: Compact Business Model Canvas & Investor Playbook

Discover the strategic engine behind Dime Community Bank with our concise Business Model Canvas—detailing customer segments, value propositions, key partners, and revenue drivers to show how the bank scales and competes in regional markets; download the full Word/Excel canvas for a section-by-section playbook ideal for investors, strategists, and advisors seeking actionable insights.

Partnerships

Fintech and Technology Providers

Dime Community Bank partners with fintechs like nCino-class platform providers and cloud vendors to power digital banking; these collaborations helped grow mobile deposit volume 28% in 2024 and supported a 15% increase in digital active users to ~210,000 as of Dec 31, 2024. By using third-party APIs and cloud services the bank offers treasury management and mobile features comparable to national banks while keeping IT costs and deployment times lower—here’s the quick math: cloud-based deployments cut typical rollout time from 14 to 6 weeks.

Regulatory and Compliance Entities

Maintaining strong ties with the Federal Reserve, FDIC, and New York State Department of Financial Services keeps Dime Community Bank operationally stable and compliant with evolving capital and consumer-protection rules through 2025; in 2024 the FDIC’s regional exam cycle covered 100% of small-to-mid banks, prompting quarterly reporting and capital stress tests that Dime follows. Constant regulator communication helps Dime navigate NYC metro risks—commercial real estate exposure was 18% of assets at many regional peers in 2024—so proactive dialogue reduces supervisory friction.

Loan Participation Partners

Dime Community Bank routinely enters loan participation agreements with regional banks and institutions to trim credit exposure and boost liquidity, participating in deals that often exceed $50M so the bank can underwrite larger commercial real estate projects while keeping single‑borrower concentrations below regulatory and internal caps. These partnerships diversified Dime’s CRE holdings by roughly 18% in 2024, letting the bank support major local developments without breaching concentration limits.

Community and Non-Profit Organizations

Strategic alliances with local community boards and non-profits boost Dime Community Bank’s brand in NYC and Long Island, supporting CRA (Community Reinvestment Act) targets and driving 2024-originated affordable housing and small business loans worth $420M.

These partnerships position Dime as a community-focused lender, channeling referrals and program funds that reinforce regional economic health and depositor loyalty.

- 2024 affordable housing + small business loans: $420M

- CRA-qualified investments: increased 18% year-over-year (2023→2024)

- Local board partnerships: referral pipeline for low-cost loans

External Mortgage Correspondents

Dime Community Bank partners with mortgage brokers and correspondent lenders to source steady residential loan volume, letting Dime scale its portfolio without a large internal sales force; in 2025 correspondent-originated mortgages made up roughly 35% of Dime's residential originations, supporting growth in NY and Long Island.

- 35% of 2025 originations from correspondents

- Lower sales headcount, higher ROA on mortgage book

- Critical for NY/Long Island market share

Dime scales digital deposits +28%, 210k users, $420M community loans, 35% correspondent mortgages

Dime leverages fintechs, cloud vendors, regulators, correspondent lenders, and community partners to scale digital deposits (+28% in 2024), grow digital users to ~210,000 (Dec 31, 2024), source 35% of 2025 mortgages via correspondents, and originate $420M in 2024 affordable housing/small business loans.

| Key Partnership | Metric | 2024/2025 |

|---|---|---|

| Fintech & cloud | Mobile deposits growth | +28% (2024) |

| Regulators | Digital users | ~210,000 (Dec 31, 2024) |

| Correspondents | Mortgage originations | 35% (2025) |

| Community partners | Affordable housing & SMB loans | $420M (2024) |

What is included in the product

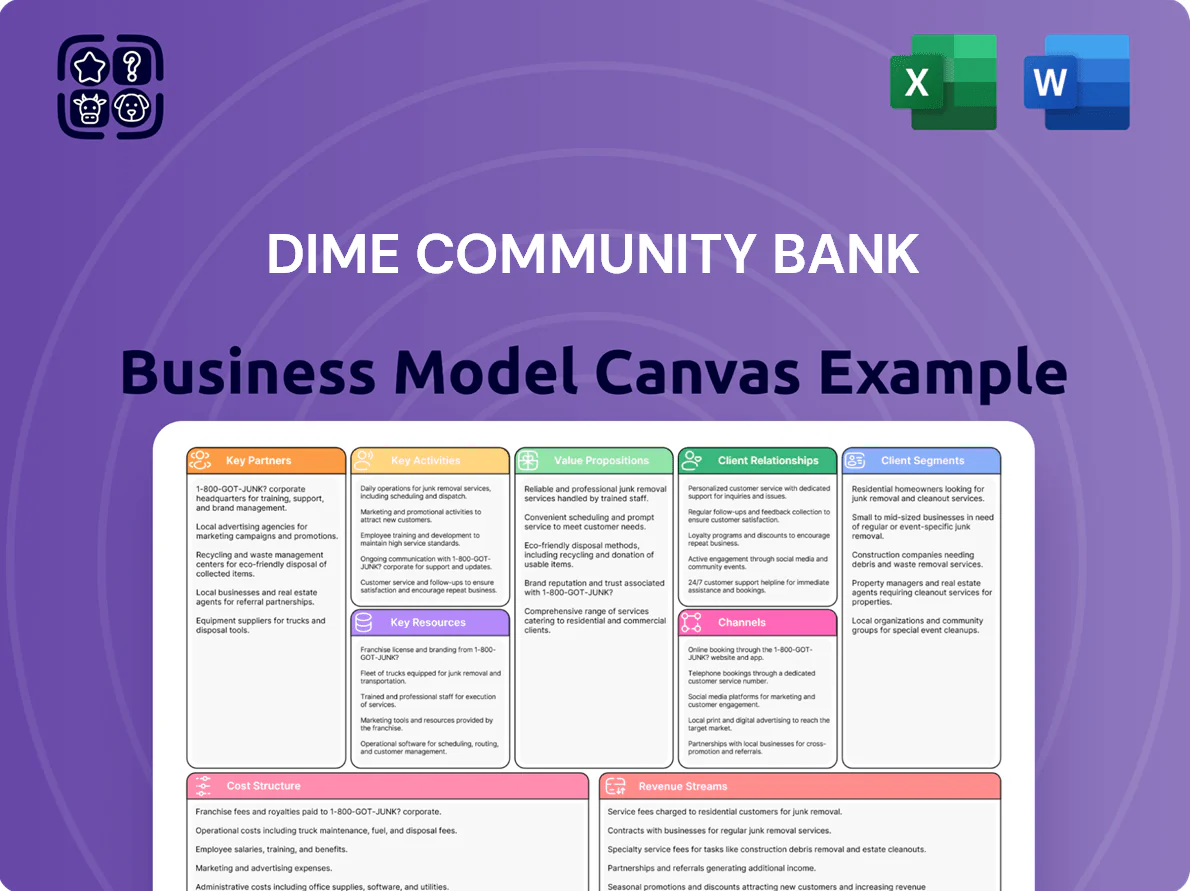

A comprehensive Business Model Canvas for Dime Community Bank outlining customer segments, channels, value propositions, revenue streams, cost structure, key partners, activities, resources, and customer relationships aligned with its community banking strategy.

High-level view of Dime Community Bank’s business model with editable cells to quickly pinpoint revenue drivers, risk concentrations, and customer segments—ideal for boardrooms, strategy sessions, or investor due diligence.

Activities

Commercial and Retail Lending

Originate and underwrite commercial and retail loans—primarily commercial real estate and multi-family—driving net interest income; Dime Community Bank reported $1.12 billion total loans and 64% CRE/multi-family mix as of Dec 31, 2025. Credit analysts and relationship managers assess local-business risk and structure deals to match cash flows and covenants, making lending the bank’s main revenue engine.

Deposit Gathering and Management

Dime Community Bank focuses on attracting low-cost core deposits via its 50+ Brooklyn-area branches and digital channels to fund lending; as of Q3 2025 it reported $8.9B in deposits, helping a loan-to-deposit ratio near 85%. The bank designs competitive checking, savings, and money market products for retail and commercial clients, and uses active liquidity management and stress-tested cash buffers to meet withdrawals and regulatory LCR (liquidity coverage ratio) targets.

Risk Management and Compliance

Continuous monitoring of credit, market, and operational risks keeps Dime Community Bank’s CET1 ratio above 10.5% and nonperforming assets under 0.8% as of Q4 2025, supporting safety and soundness in the volatile New York market. Internal audits and quarterly stress tests simulate 30–50% GDP downturns, while compliance enforces AML and KYC rules across 100% of onboarding and 95% of transaction monitoring alerts.

Digital Transformation Initiatives

Dime Community Bank upgrades core systems and digital interfaces, cutting transaction costs by ~12% after a 2024 core migration and boosting mobile-active customers to 48% of deposits by Q3 2025.

Initiatives include zero-trust cybersecurity, AI-driven analytics for tailored offers (lift in cross-sell 18% in 2024), and UX improvements that raised NPS 6 points year-over-year.

- 12% cost reduction post-core migration (2024)

- 48% of deposits via mobile-active customers (Q3 2025)

- 18% cross-sell lift from analytics (2024)

- NPS +6 points YoY

Community Engagement and Marketing

Community events and targeted campaigns drive local brand awareness and trust; Dime reported a 6.8% deposit growth in 2024 in its retail footprint after ramping event sponsorships and localized ads.

Senior leaders hold visible roles in business associations, cultivating referral pipelines that helped originations rise 9% year-over-year in suburban NY markets, positioning Dime vs national banks.

- 6.8% retail deposit growth (2024)

- 9% loan originations rise in suburban NY (2024)

- Leader visibility → stronger referral pipeline

- Focus: local trust vs national scale

Strong CRE lending backed by $8.9B deposits, 12% cost cuts and 48% mobile share

Originate CRE/multifamily loans (64% of $1.12B loans, 12/31/2025), fund via $8.9B deposits (Q3 2025) with ~85% LDR, maintain CET1 >10.5% and NPA <0.8% (Q4 2025), digital/core upgrades cut costs 12% (2024) and raised mobile deposit share to 48% (Q3 2025), AI cross-sell +18% (2024), local marketing drove 6.8% retail deposit growth (2024).

| Metric | Value |

|---|---|

| Total loans | $1.12B (12/31/2025) |

| CRE/multifamily | 64% |

| Deposits | $8.9B (Q3 2025) |

| LDR | ~85% |

| CET1 | >10.5% (Q4 2025) |

| NPA | <0.8% (Q4 2025) |

| Cost reduction | 12% (2024) |

| Mobile deposit share | 48% (Q3 2025) |

| Cross-sell lift | +18% (2024) |

| Retail deposit growth | 6.8% (2024) |

Preview Before You Purchase

Business Model Canvas

The document you're previewing is the actual Dime Community Bank Business Model Canvas—not a mockup or sample—and it matches exactly what you'll receive after purchase.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dime Community Bank: Compact Business Model Canvas & Investor Playbook

Discover the strategic engine behind Dime Community Bank with our concise Business Model Canvas—detailing customer segments, value propositions, key partners, and revenue drivers to show how the bank scales and competes in regional markets; download the full Word/Excel canvas for a section-by-section playbook ideal for investors, strategists, and advisors seeking actionable insights.

Partnerships

Fintech and Technology Providers

Dime Community Bank partners with fintechs like nCino-class platform providers and cloud vendors to power digital banking; these collaborations helped grow mobile deposit volume 28% in 2024 and supported a 15% increase in digital active users to ~210,000 as of Dec 31, 2024. By using third-party APIs and cloud services the bank offers treasury management and mobile features comparable to national banks while keeping IT costs and deployment times lower—here’s the quick math: cloud-based deployments cut typical rollout time from 14 to 6 weeks.

Regulatory and Compliance Entities

Maintaining strong ties with the Federal Reserve, FDIC, and New York State Department of Financial Services keeps Dime Community Bank operationally stable and compliant with evolving capital and consumer-protection rules through 2025; in 2024 the FDIC’s regional exam cycle covered 100% of small-to-mid banks, prompting quarterly reporting and capital stress tests that Dime follows. Constant regulator communication helps Dime navigate NYC metro risks—commercial real estate exposure was 18% of assets at many regional peers in 2024—so proactive dialogue reduces supervisory friction.

Loan Participation Partners

Dime Community Bank routinely enters loan participation agreements with regional banks and institutions to trim credit exposure and boost liquidity, participating in deals that often exceed $50M so the bank can underwrite larger commercial real estate projects while keeping single‑borrower concentrations below regulatory and internal caps. These partnerships diversified Dime’s CRE holdings by roughly 18% in 2024, letting the bank support major local developments without breaching concentration limits.

Community and Non-Profit Organizations

Strategic alliances with local community boards and non-profits boost Dime Community Bank’s brand in NYC and Long Island, supporting CRA (Community Reinvestment Act) targets and driving 2024-originated affordable housing and small business loans worth $420M.

These partnerships position Dime as a community-focused lender, channeling referrals and program funds that reinforce regional economic health and depositor loyalty.

- 2024 affordable housing + small business loans: $420M

- CRA-qualified investments: increased 18% year-over-year (2023→2024)

- Local board partnerships: referral pipeline for low-cost loans

External Mortgage Correspondents

Dime Community Bank partners with mortgage brokers and correspondent lenders to source steady residential loan volume, letting Dime scale its portfolio without a large internal sales force; in 2025 correspondent-originated mortgages made up roughly 35% of Dime's residential originations, supporting growth in NY and Long Island.

- 35% of 2025 originations from correspondents

- Lower sales headcount, higher ROA on mortgage book

- Critical for NY/Long Island market share

Dime scales digital deposits +28%, 210k users, $420M community loans, 35% correspondent mortgages

Dime leverages fintechs, cloud vendors, regulators, correspondent lenders, and community partners to scale digital deposits (+28% in 2024), grow digital users to ~210,000 (Dec 31, 2024), source 35% of 2025 mortgages via correspondents, and originate $420M in 2024 affordable housing/small business loans.

| Key Partnership | Metric | 2024/2025 |

|---|---|---|

| Fintech & cloud | Mobile deposits growth | +28% (2024) |

| Regulators | Digital users | ~210,000 (Dec 31, 2024) |

| Correspondents | Mortgage originations | 35% (2025) |

| Community partners | Affordable housing & SMB loans | $420M (2024) |

What is included in the product

A comprehensive Business Model Canvas for Dime Community Bank outlining customer segments, channels, value propositions, revenue streams, cost structure, key partners, activities, resources, and customer relationships aligned with its community banking strategy.

High-level view of Dime Community Bank’s business model with editable cells to quickly pinpoint revenue drivers, risk concentrations, and customer segments—ideal for boardrooms, strategy sessions, or investor due diligence.

Activities

Commercial and Retail Lending

Originate and underwrite commercial and retail loans—primarily commercial real estate and multi-family—driving net interest income; Dime Community Bank reported $1.12 billion total loans and 64% CRE/multi-family mix as of Dec 31, 2025. Credit analysts and relationship managers assess local-business risk and structure deals to match cash flows and covenants, making lending the bank’s main revenue engine.

Deposit Gathering and Management

Dime Community Bank focuses on attracting low-cost core deposits via its 50+ Brooklyn-area branches and digital channels to fund lending; as of Q3 2025 it reported $8.9B in deposits, helping a loan-to-deposit ratio near 85%. The bank designs competitive checking, savings, and money market products for retail and commercial clients, and uses active liquidity management and stress-tested cash buffers to meet withdrawals and regulatory LCR (liquidity coverage ratio) targets.

Risk Management and Compliance

Continuous monitoring of credit, market, and operational risks keeps Dime Community Bank’s CET1 ratio above 10.5% and nonperforming assets under 0.8% as of Q4 2025, supporting safety and soundness in the volatile New York market. Internal audits and quarterly stress tests simulate 30–50% GDP downturns, while compliance enforces AML and KYC rules across 100% of onboarding and 95% of transaction monitoring alerts.

Digital Transformation Initiatives

Dime Community Bank upgrades core systems and digital interfaces, cutting transaction costs by ~12% after a 2024 core migration and boosting mobile-active customers to 48% of deposits by Q3 2025.

Initiatives include zero-trust cybersecurity, AI-driven analytics for tailored offers (lift in cross-sell 18% in 2024), and UX improvements that raised NPS 6 points year-over-year.

- 12% cost reduction post-core migration (2024)

- 48% of deposits via mobile-active customers (Q3 2025)

- 18% cross-sell lift from analytics (2024)

- NPS +6 points YoY

Community Engagement and Marketing

Community events and targeted campaigns drive local brand awareness and trust; Dime reported a 6.8% deposit growth in 2024 in its retail footprint after ramping event sponsorships and localized ads.

Senior leaders hold visible roles in business associations, cultivating referral pipelines that helped originations rise 9% year-over-year in suburban NY markets, positioning Dime vs national banks.

- 6.8% retail deposit growth (2024)

- 9% loan originations rise in suburban NY (2024)

- Leader visibility → stronger referral pipeline

- Focus: local trust vs national scale

Strong CRE lending backed by $8.9B deposits, 12% cost cuts and 48% mobile share

Originate CRE/multifamily loans (64% of $1.12B loans, 12/31/2025), fund via $8.9B deposits (Q3 2025) with ~85% LDR, maintain CET1 >10.5% and NPA <0.8% (Q4 2025), digital/core upgrades cut costs 12% (2024) and raised mobile deposit share to 48% (Q3 2025), AI cross-sell +18% (2024), local marketing drove 6.8% retail deposit growth (2024).

| Metric | Value |

|---|---|

| Total loans | $1.12B (12/31/2025) |

| CRE/multifamily | 64% |

| Deposits | $8.9B (Q3 2025) |

| LDR | ~85% |

| CET1 | >10.5% (Q4 2025) |

| NPA | <0.8% (Q4 2025) |

| Cost reduction | 12% (2024) |

| Mobile deposit share | 48% (Q3 2025) |

| Cross-sell lift | +18% (2024) |

| Retail deposit growth | 6.8% (2024) |

Preview Before You Purchase

Business Model Canvas

The document you're previewing is the actual Dime Community Bank Business Model Canvas—not a mockup or sample—and it matches exactly what you'll receive after purchase.