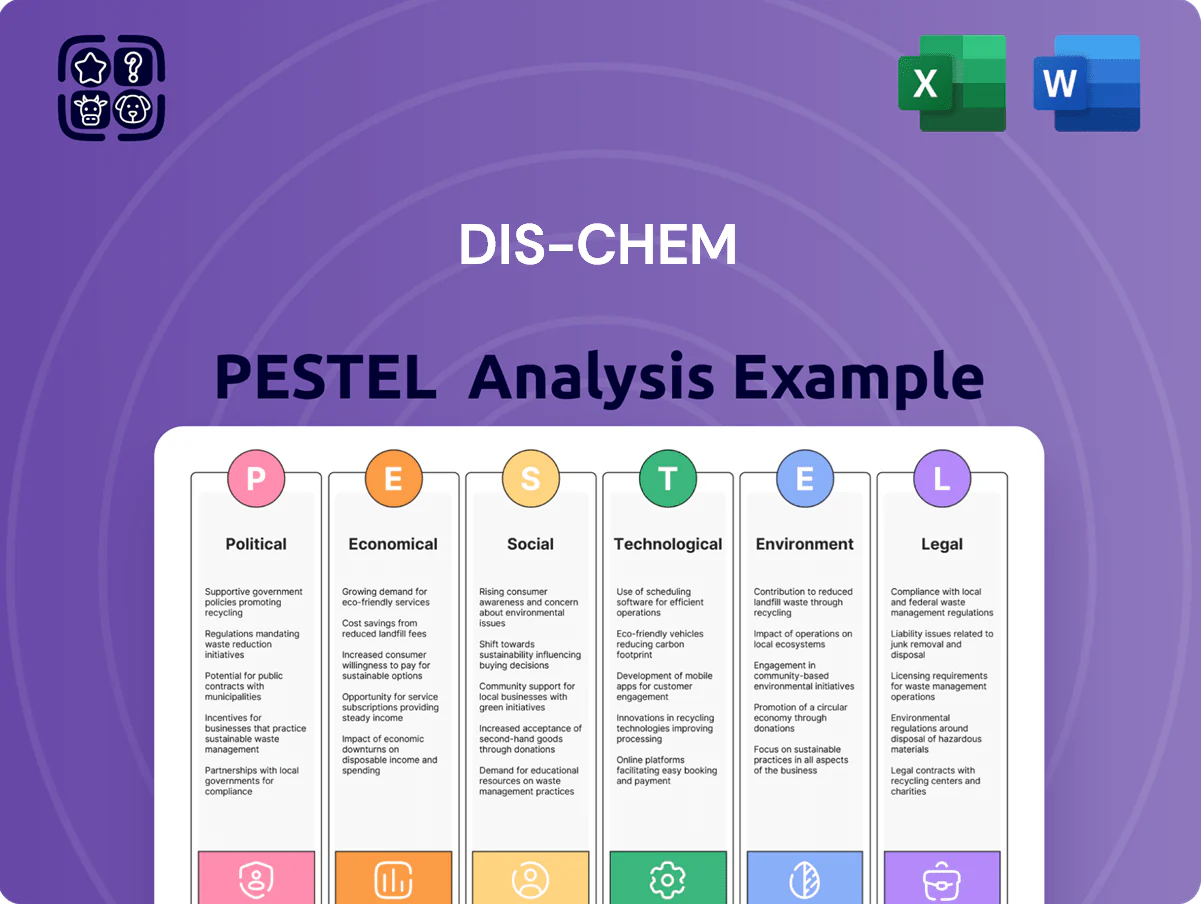

Dis-Chem PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, consumer health trends, and tech-driven retailing shape Dis-Chem’s future in our concise PESTLE snapshot—designed to inform investment and strategy decisions quickly. Buy the full PESTLE analysis for a detailed, actionable breakdown of regulatory risks, economic pressures, and environmental trends that could impact margins and growth. Download now to get ready-to-use insights for reports, pitches, or strategic planning.

Political factors

National Health Insurance implementation

The South African government's NHI progress creates uncertainty for private pharmacies; NHI pilot phases cover 10 of 52 health districts and the 2024 White Paper targets phased implementation by 2030, risking changes to dispensing rights and reimbursement for Dis-Chem.

Dis-Chem must prepare for centralized procurement—South Africa spent R218 billion on medicines in 2023—potentially compressing margins and altering supplier relationships.

Scaling its 400+ clinic network and positioning as a primary healthcare provider is essential for Dis-Chem to secure patient flow and revenue under a hybrid public-private model.

Political stability and governance

Ongoing political shifts and the Government of National Unity’s performance affect investor confidence; South Africa’s political risk premium rose to 2.1 percentage points in 2024, weighing on retail investment decisions. Legislative efficacy and policy rollout for trade and healthcare—key to pharmacy regulation—have slowed, with 2024 health budget growth at 3.8% vs. a 5-year average of 6.1%. Dis-Chem must model for policy volatility and possible ministerial reprioritisation impacting licensing and reimbursements.

B-BBEE compliance and transformation

B-BBEE remains a regulatory imperative in South Africa; Dis-Chem, which reported a 2024 empowerment scorecard showing level 4 compliance and 25% black ownership in its 2023 annual report, must sustain improvements to secure government tenders and retain its social license.

International trade and import policies

Political decisions on import duties and trade agreements directly affect Dis-Chem’s cost base for internationally sourced health and beauty products; for example, South Africa’s average applied tariff on cosmetics is 7.1% (WTO 2023), raising input costs if preferential access changes.

Escalating trade tensions can trigger supply-chain disruptions or higher tariffs on specialized supplements and luxury cosmetics, potentially widening gross margins by several percentage points if costs are passed on.

Maintaining a diversified supplier base across regions mitigates risks from shifting geopolitical alliances; Dis-Chem’s 2024 supplier diversification reduced single-country sourcing exposure to under 20%.

- Average cosmetics tariff SA 7.1% (WTO 2023)

- Trade shocks can move gross margins by multiple percentage points

- 2024: single-country supplier exposure <20%

Public health policy and vaccine mandates

Government vaccination drives position Dis-Chem as a frontline implementer; during 2024 the chain delivered over 1.2 million state-funded vaccines and vaccines/medications accounted for an estimated 8% of retail revenue.

Dis-Chem's role in distributing Department of Health-supplied medicines requires strict compliance to avoid fines and service interruptions; national mandates boosted in-store clinic visits by ~18% in 2023–24.

Alignment with health directives supports public wellness targets and preserves access to R1.4 billion in public procurement contracts awarded to major pharmacy chains in 2024.

- Delivered >1.2M state-funded vaccines (2024)

- Vaccines/meds ≈ 8% of retail revenue

- In-store clinic visits +18% (2023–24)

- Public procurement ~R1.4bn (2024)

Policy shake-up: NHI, centralized procurement and higher SA risk premium hit pharma

Political risks: NHI rollout (phased to 2030) threatens dispensing/reimbursement; R218bn medicine spend (2023) implies centralized procurement pressure; political/policy volatility raised SA risk premium to 2.1ppt (2024); B-BBEE level 4, 25% black ownership (2023) required for tenders; delivered >1.2M state vaccines (2024), public procurement ~R1.4bn.

| Metric | Value |

|---|---|

| Medicine spend 2023 | R218bn |

| Risk premium 2024 | 2.1 ppt |

| State vaccines 2024 | >1.2M |

| Public procurement 2024 | R1.4bn |

What is included in the product

Explores how macro-environmental factors uniquely affect Dis-Chem across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven subpoints and forward-looking insights tailored to the South African retail pharmacy context.

Condenses Dis-Chem's PESTLE into a sharp, shareable summary for meetings or presentations, visually segmented by category and written in plain language so teams can quickly align on external risks and market positioning.

Economic factors

Consumer disposable income pressure

Persistent inflation (CPI ~5.9% in 2025) and policy rates near 8.25% have eroded South African household real incomes, prompting tighter spending; Dis-Chem benefits from non-discretionary pharma sales but its luxury beauty and nutrition lines face demand risk. In FY2024 Dis-Chem reported gross margin pressure and increased promotional activity; the firm must balance premium assortments with growth in value-focused house brands to retain price-sensitive shoppers.

Currency volatility and exchange rates

Fluctuations of the rand—down ~6% vs USD in 2024 and volatility with average monthly FX swings of 3–4%—raise landing costs for Dis-Chem’s imported health products, squeezing gross margins when the ZAR depreciates. As a major importer of specialized pharmaceuticals and equipment, Dis-Chem saw imported cost inflation contribute to a 1.2–1.8ppt reduction in gross margin in parts of 2023–24. Hedging programs and increased local sourcing (targeting 15–20% more locally procured SKUs by 2025) are used to stabilize retail pricing and protect margins.

Unemployment and market growth

High structural unemployment in South Africa (32.9% Q4 2025 expanded definition) constrains the addressable market for private healthcare and retail pharmacy services, limiting Dis-Chem’s premium customer base.

Economic stagnation and subdued real GDP growth (0.6% 2024, IMF est. 0.8% 2025) hinder middle-class expansion, reducing demand for Dis-Chem’s high-margin wellness products.

To sustain volume and revenue, Dis-Chem may need to pursue lower-income segments via smaller-format stores and value ranges, mirroring competitors that target price-sensitive consumers.

Energy costs and load shedding

Operating large Dis-Chem stores and temperature-controlled warehouses drives high energy use; South African retail electricity tariff increases averaged about 12%–15% annually in 2023–2024, pressuring margins.

Backup generator fuel and maintenance raised operating costs—Dis-Chem noted energy and utilities exposure in 2024 financials, with energy-related expenses materially impacting store-level EBITDA.

Investment in on-site solar or efficiency reduced volatility risk but requires capex; efficient energy management is essential to preserve profitability amid load-shedding.

- 2024 tariffs +12%–15%

- Backup generator & fuel add significant variable costs

- On-site solar capex offsets long-term volatility

Single Exit Price (SEP) regulations

The South African Single Exit Price caps pharmacy margins on scheduled medicines, constraining Dis-Chem’s profitability from prescriptions; SEP rose about 3.4% in 2024 versus CPI of ~5.9%, squeezing retail pharmacy gross margins.

Consequently Dis-Chem emphasizes high-volume front-shop goods and clinic/optometry services—these non-SEP revenues made up over 45% of group sales in FY2024—to offset limited drug margin growth.

- SEP growth 2024 ~3.4% vs CPI ~5.9%

- Non-SEP sales >45% of FY2024 revenue

- Pharmacy margins pressured, reliant on volume and services

Cost pressures squeeze margins as weak growth, high rates and energy hikes bite

Inflation ~5.9% (2025), policy rate 8.25%, rand down ~6% vs USD (2024) squeeze margins; SEP +3.4% (2024) limits pharmacy margins so non-SEP sales >45% of FY2024 revenue; unemployment ~32.9% (Q4 2025) and GDP ~0.6% (2024) constrain premium demand; energy tariffs +12–15% (2023–24) and backup fuel raise operating costs, driving capex for solar.

| Metric | Value |

|---|---|

| Inflation (CPI) | ~5.9% (2025) |

| Policy rate | 8.25% |

| Rand vs USD | -6% (2024) |

| SEP increase | +3.4% (2024) |

| Non-SEP share | >45% FY2024 |

| Unemployment | 32.9% Q4 2025 |

| GDP growth | 0.6% (2024) |

| Energy tariffs | +12–15% (2023–24) |

Preview the Actual Deliverable

Dis-Chem PESTLE Analysis

The preview shown here is the exact Dis-Chem PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, consumer health trends, and tech-driven retailing shape Dis-Chem’s future in our concise PESTLE snapshot—designed to inform investment and strategy decisions quickly. Buy the full PESTLE analysis for a detailed, actionable breakdown of regulatory risks, economic pressures, and environmental trends that could impact margins and growth. Download now to get ready-to-use insights for reports, pitches, or strategic planning.

Political factors

National Health Insurance implementation

The South African government's NHI progress creates uncertainty for private pharmacies; NHI pilot phases cover 10 of 52 health districts and the 2024 White Paper targets phased implementation by 2030, risking changes to dispensing rights and reimbursement for Dis-Chem.

Dis-Chem must prepare for centralized procurement—South Africa spent R218 billion on medicines in 2023—potentially compressing margins and altering supplier relationships.

Scaling its 400+ clinic network and positioning as a primary healthcare provider is essential for Dis-Chem to secure patient flow and revenue under a hybrid public-private model.

Political stability and governance

Ongoing political shifts and the Government of National Unity’s performance affect investor confidence; South Africa’s political risk premium rose to 2.1 percentage points in 2024, weighing on retail investment decisions. Legislative efficacy and policy rollout for trade and healthcare—key to pharmacy regulation—have slowed, with 2024 health budget growth at 3.8% vs. a 5-year average of 6.1%. Dis-Chem must model for policy volatility and possible ministerial reprioritisation impacting licensing and reimbursements.

B-BBEE compliance and transformation

B-BBEE remains a regulatory imperative in South Africa; Dis-Chem, which reported a 2024 empowerment scorecard showing level 4 compliance and 25% black ownership in its 2023 annual report, must sustain improvements to secure government tenders and retain its social license.

International trade and import policies

Political decisions on import duties and trade agreements directly affect Dis-Chem’s cost base for internationally sourced health and beauty products; for example, South Africa’s average applied tariff on cosmetics is 7.1% (WTO 2023), raising input costs if preferential access changes.

Escalating trade tensions can trigger supply-chain disruptions or higher tariffs on specialized supplements and luxury cosmetics, potentially widening gross margins by several percentage points if costs are passed on.

Maintaining a diversified supplier base across regions mitigates risks from shifting geopolitical alliances; Dis-Chem’s 2024 supplier diversification reduced single-country sourcing exposure to under 20%.

- Average cosmetics tariff SA 7.1% (WTO 2023)

- Trade shocks can move gross margins by multiple percentage points

- 2024: single-country supplier exposure <20%

Public health policy and vaccine mandates

Government vaccination drives position Dis-Chem as a frontline implementer; during 2024 the chain delivered over 1.2 million state-funded vaccines and vaccines/medications accounted for an estimated 8% of retail revenue.

Dis-Chem's role in distributing Department of Health-supplied medicines requires strict compliance to avoid fines and service interruptions; national mandates boosted in-store clinic visits by ~18% in 2023–24.

Alignment with health directives supports public wellness targets and preserves access to R1.4 billion in public procurement contracts awarded to major pharmacy chains in 2024.

- Delivered >1.2M state-funded vaccines (2024)

- Vaccines/meds ≈ 8% of retail revenue

- In-store clinic visits +18% (2023–24)

- Public procurement ~R1.4bn (2024)

Policy shake-up: NHI, centralized procurement and higher SA risk premium hit pharma

Political risks: NHI rollout (phased to 2030) threatens dispensing/reimbursement; R218bn medicine spend (2023) implies centralized procurement pressure; political/policy volatility raised SA risk premium to 2.1ppt (2024); B-BBEE level 4, 25% black ownership (2023) required for tenders; delivered >1.2M state vaccines (2024), public procurement ~R1.4bn.

| Metric | Value |

|---|---|

| Medicine spend 2023 | R218bn |

| Risk premium 2024 | 2.1 ppt |

| State vaccines 2024 | >1.2M |

| Public procurement 2024 | R1.4bn |

What is included in the product

Explores how macro-environmental factors uniquely affect Dis-Chem across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven subpoints and forward-looking insights tailored to the South African retail pharmacy context.

Condenses Dis-Chem's PESTLE into a sharp, shareable summary for meetings or presentations, visually segmented by category and written in plain language so teams can quickly align on external risks and market positioning.

Economic factors

Consumer disposable income pressure

Persistent inflation (CPI ~5.9% in 2025) and policy rates near 8.25% have eroded South African household real incomes, prompting tighter spending; Dis-Chem benefits from non-discretionary pharma sales but its luxury beauty and nutrition lines face demand risk. In FY2024 Dis-Chem reported gross margin pressure and increased promotional activity; the firm must balance premium assortments with growth in value-focused house brands to retain price-sensitive shoppers.

Currency volatility and exchange rates

Fluctuations of the rand—down ~6% vs USD in 2024 and volatility with average monthly FX swings of 3–4%—raise landing costs for Dis-Chem’s imported health products, squeezing gross margins when the ZAR depreciates. As a major importer of specialized pharmaceuticals and equipment, Dis-Chem saw imported cost inflation contribute to a 1.2–1.8ppt reduction in gross margin in parts of 2023–24. Hedging programs and increased local sourcing (targeting 15–20% more locally procured SKUs by 2025) are used to stabilize retail pricing and protect margins.

Unemployment and market growth

High structural unemployment in South Africa (32.9% Q4 2025 expanded definition) constrains the addressable market for private healthcare and retail pharmacy services, limiting Dis-Chem’s premium customer base.

Economic stagnation and subdued real GDP growth (0.6% 2024, IMF est. 0.8% 2025) hinder middle-class expansion, reducing demand for Dis-Chem’s high-margin wellness products.

To sustain volume and revenue, Dis-Chem may need to pursue lower-income segments via smaller-format stores and value ranges, mirroring competitors that target price-sensitive consumers.

Energy costs and load shedding

Operating large Dis-Chem stores and temperature-controlled warehouses drives high energy use; South African retail electricity tariff increases averaged about 12%–15% annually in 2023–2024, pressuring margins.

Backup generator fuel and maintenance raised operating costs—Dis-Chem noted energy and utilities exposure in 2024 financials, with energy-related expenses materially impacting store-level EBITDA.

Investment in on-site solar or efficiency reduced volatility risk but requires capex; efficient energy management is essential to preserve profitability amid load-shedding.

- 2024 tariffs +12%–15%

- Backup generator & fuel add significant variable costs

- On-site solar capex offsets long-term volatility

Single Exit Price (SEP) regulations

The South African Single Exit Price caps pharmacy margins on scheduled medicines, constraining Dis-Chem’s profitability from prescriptions; SEP rose about 3.4% in 2024 versus CPI of ~5.9%, squeezing retail pharmacy gross margins.

Consequently Dis-Chem emphasizes high-volume front-shop goods and clinic/optometry services—these non-SEP revenues made up over 45% of group sales in FY2024—to offset limited drug margin growth.

- SEP growth 2024 ~3.4% vs CPI ~5.9%

- Non-SEP sales >45% of FY2024 revenue

- Pharmacy margins pressured, reliant on volume and services

Cost pressures squeeze margins as weak growth, high rates and energy hikes bite

Inflation ~5.9% (2025), policy rate 8.25%, rand down ~6% vs USD (2024) squeeze margins; SEP +3.4% (2024) limits pharmacy margins so non-SEP sales >45% of FY2024 revenue; unemployment ~32.9% (Q4 2025) and GDP ~0.6% (2024) constrain premium demand; energy tariffs +12–15% (2023–24) and backup fuel raise operating costs, driving capex for solar.

| Metric | Value |

|---|---|

| Inflation (CPI) | ~5.9% (2025) |

| Policy rate | 8.25% |

| Rand vs USD | -6% (2024) |

| SEP increase | +3.4% (2024) |

| Non-SEP share | >45% FY2024 |

| Unemployment | 32.9% Q4 2025 |

| GDP growth | 0.6% (2024) |

| Energy tariffs | +12–15% (2023–24) |

Preview the Actual Deliverable

Dis-Chem PESTLE Analysis

The preview shown here is the exact Dis-Chem PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.