discoverIE Group Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

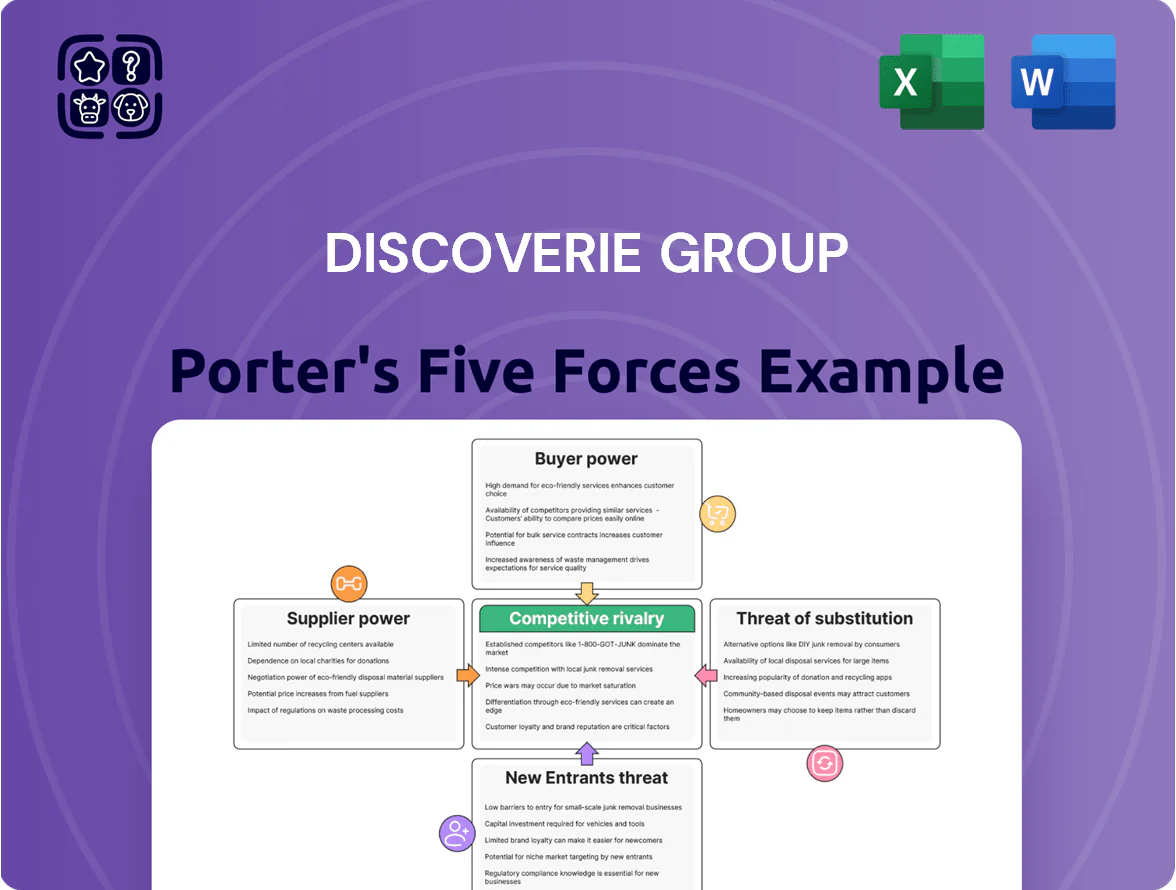

discoverIE Group operates in a fragmented, technology-driven components market where supplier specialization and moderate buyer bargaining shape margins, while product differentiation and regulatory standards raise barriers for new entrants.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore discoverIE Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized component dependency

discoverIE Group depends on specialized semiconductor and precision-metal suppliers for its custom electronics; in 2024 about 62% of material spend was on high-spec components, raising supply risk.

Limited qualified sources meeting tight engineering tolerances mean few substitutes, so supplier switching costs and lead times often exceed 20 weeks for key parts.

That scarcity gives suppliers pricing leverage—raw-material cost inflation added ~8% to COGS in 2023—so suppliers can push higher prices and stretch delivery schedules during demand spikes.

Raw material price volatility

Input costs for copper, silver and engineering plastics swing with global commodity markets—copper rose ~40% from Jan 2023 to Dec 2024, squeezing margins on discoverIE’s electronic components unless recovered.

discoverIE often passes costs to customers, but contract repricing lags of 3–6 months raise temporary supplier power and margin volatility.

The firm’s exposure hinges on long-term supply ties; suppliers concentrated in Asia and Europe give some negotiating leverage, yet spot-buy spikes in 2024 forced short-term premium purchases of ~5–8% of COGS.

Geographic concentration of supply chains

A large share of electronic components is still made in East Asia—about 70% of global semiconductor assembly and 60% of passive component capacity in 2024—so discoverIE faces dependency on regional stability and shipping corridors.

Supply disruptions let vendors with stock push prices and lead times up; during H1 2023 shortages raised component prices by ~15% in the sector.

discoverIE has regionalized sourcing—roughly 30% more local inventory held since 2022—but key tech parts remain from a few suppliers, keeping supplier leverage high.

Switching costs for technical inputs

Changing suppliers for discoverIE Group’s critical, customized components requires lengthy re-qualification and testing to meet industrial safety standards, often taking 6–18 months per part and costing hundreds of thousands of pounds in validation and downtime.

These high switching costs lock suppliers into designs, giving them stronger bargaining power across product life cycles and limiting discoverIE’s ability to switch vendors quickly to chase lower input prices.

- 6–18 months typical re-qualification

- £100k+ validation cost per part

- Supplier stays tied to design → higher leverage

- Limits rapid vendor switching to cut input costs

Supplier consolidation trends

Supplier consolidation in semiconductors cut global supplier count by ~15% from 2019–2024, concentrating revenue—top 10 vendors now hold ~58% of market share (2024, IDC), boosting supplier leverage versus mid-sized manufacturers like discoverIE.

As suppliers scale via M&A, their bargaining power rises, raising price and allocation risk for discoverIE and forcing emphasis on preferred-buyer status and long-term contracts to secure components.

- Top-10 suppliers = ~58% market (2024, IDC)

- Supplier count down ~15% (2019–2024)

- Preferred-buyer contracts cut allocation risk

Supplier power spikes: consolidation, +40% copper, long lead times — discoverIE locks supply

Suppliers hold high bargaining power: 62% spend on high-spec parts, few substitutes, 6–18 months re-qualification, £100k+ validation, lead times >20 weeks; commodity swings (copper +40% Jan–Dec 2024) and supplier consolidation (top-10 = 58% market, supplier count −15% 2019–24) raise price and allocation risk, so discoverIE uses preferred-buyer deals and local inventory (+30% since 2022).

| Metric | Value |

|---|---|

| High-spec spend | 62% |

| Re-qualification | 6–18 months |

| Validation cost | £100k+ |

| Copper change 2024 | +40% |

| Top-10 share | 58% |

What is included in the product

Tailored Porter's Five Forces for discoverIE Group, revealing competitive intensity, buyer/supplier leverage, entry barriers, and substitution threats to assess pricing power and profitability.

Concise Porter's Five Forces view tailored to discoverIE Group—rapidly spot competitive pressures and remedial strategies for portfolio optimization.

Customers Bargaining Power

High switching costs due to design-in model

discoverIE focuses on design-in components engineered into customers’ systems; once fitted, switching costs rise sharply—retooling or recertifying can cost millions and months of downtime. In 2024 discoverIE reported 68% recurring revenue from long-life industrial contracts, showing low post-design churn; industry studies cite average switching project costs of $0.5–2.0m and 6–18 months, cutting customer bargaining power after design completion.

Fragmented and diverse customer base

discoverIE serves diverse sectors—renewable energy, medical, transportation—so no single customer dominates revenues; top-five customer share was about 18% in FY2024, keeping concentration low.

This low concentration limits buyer leverage, preventing large price concessions and protecting gross margins, which were 29.4% in FY2024.

Diversification also hedges sector downturns: revenue from renewables and medical grew ~12% and ~9% respectively in 2024, offsetting weakness elsewhere.

Demand for specialized technical performance

Customers in medical and aerospace sectors value reliability and exact specs over price; mission-critical orders push purchase decisions toward long-term performance and support. In 2024 discoverIE reported adjusted operating margin of 11.7%, reflecting pricing power in specialty electronics where warranty claims under 1% and multi-year contracts (typical 3–7 years) reduce buyer leverage. This shifts bargaining power to discoverIE as a supplier of essential, high-performance solutions.

Long-term product lifecycles

Industrial products often have lifecycles of 5–30+ years, so customers pay for guaranteed long-term availability of components and support rather than lowest price.

Buyers accept stable pricing in return for supply continuity; discoverIE reported 2024 recurring revenue helping margin predictability and reduced spot bidding.

This relationship model lowers competitive tender frequency and increases customer switching costs, strengthening discoverIE’s bargaining position.

- Lifecycle: 5–30+ years

- Fewer spot bids, higher repeat orders

- Stable pricing + support = lower churn

- 2024 recurring revenue improved predictability

Information transparency and competition

Customers now use online specs and global price indices—ProcureCon found 68% of industrial buyers used digital benchmarking in 2024—so discoverIE faces clearer alternatives despite bespoke parts.

Customization narrows direct price matches, but savvy procurement teams leverage substitute quotes during renewals, pressuring margins; discoverIE reported 2024 gross margin 23.6% to defend.

To hold sway, discoverIE must show measurable value via product innovation and 97% on-time delivery targets, tying service KPIs to contract terms.

- 68% buyers use digital benchmarking (ProcureCon 2024)

- discoverIE FY2024 gross margin 23.6%

- 97% target on-time delivery to retain clients

discoverIE: Strong post-design pricing power—68% recurring revenue, high switching costs

discoverIE’s customer bargaining power is low post-design: 68% recurring revenue in FY2024, top-5 customer share ~18%, switching costs often $0.5–2.0m and 6–18 months, and gross margin ~23.6–29.4% protect pricing power; digital benchmarking (68% buyers 2024) and procurement pressure remain headwinds, so product innovation, 97% on-time delivery targets and multi-year contracts (typical 3–7 years) sustain supplier leverage.

| Metric | 2024 value |

|---|---|

| Recurring revenue | 68% |

| Top-5 customer share | ~18% |

| Gross margin | 23.6–29.4% |

| Switching cost (range) | $0.5–2.0m / 6–18 months |

| Buyers using digital benchmarking | 68% |

| On-time delivery target | 97% |

Preview Before You Purchase

discoverIE Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of discoverIE Group you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the part of the full version you’ll get—fully formatted and ready for download and use the moment you buy.

You’re previewing the final deliverable: a professional, ready-to-use analysis file available to you instantly after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

discoverIE Group operates in a fragmented, technology-driven components market where supplier specialization and moderate buyer bargaining shape margins, while product differentiation and regulatory standards raise barriers for new entrants.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore discoverIE Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized component dependency

discoverIE Group depends on specialized semiconductor and precision-metal suppliers for its custom electronics; in 2024 about 62% of material spend was on high-spec components, raising supply risk.

Limited qualified sources meeting tight engineering tolerances mean few substitutes, so supplier switching costs and lead times often exceed 20 weeks for key parts.

That scarcity gives suppliers pricing leverage—raw-material cost inflation added ~8% to COGS in 2023—so suppliers can push higher prices and stretch delivery schedules during demand spikes.

Raw material price volatility

Input costs for copper, silver and engineering plastics swing with global commodity markets—copper rose ~40% from Jan 2023 to Dec 2024, squeezing margins on discoverIE’s electronic components unless recovered.

discoverIE often passes costs to customers, but contract repricing lags of 3–6 months raise temporary supplier power and margin volatility.

The firm’s exposure hinges on long-term supply ties; suppliers concentrated in Asia and Europe give some negotiating leverage, yet spot-buy spikes in 2024 forced short-term premium purchases of ~5–8% of COGS.

Geographic concentration of supply chains

A large share of electronic components is still made in East Asia—about 70% of global semiconductor assembly and 60% of passive component capacity in 2024—so discoverIE faces dependency on regional stability and shipping corridors.

Supply disruptions let vendors with stock push prices and lead times up; during H1 2023 shortages raised component prices by ~15% in the sector.

discoverIE has regionalized sourcing—roughly 30% more local inventory held since 2022—but key tech parts remain from a few suppliers, keeping supplier leverage high.

Switching costs for technical inputs

Changing suppliers for discoverIE Group’s critical, customized components requires lengthy re-qualification and testing to meet industrial safety standards, often taking 6–18 months per part and costing hundreds of thousands of pounds in validation and downtime.

These high switching costs lock suppliers into designs, giving them stronger bargaining power across product life cycles and limiting discoverIE’s ability to switch vendors quickly to chase lower input prices.

- 6–18 months typical re-qualification

- £100k+ validation cost per part

- Supplier stays tied to design → higher leverage

- Limits rapid vendor switching to cut input costs

Supplier consolidation trends

Supplier consolidation in semiconductors cut global supplier count by ~15% from 2019–2024, concentrating revenue—top 10 vendors now hold ~58% of market share (2024, IDC), boosting supplier leverage versus mid-sized manufacturers like discoverIE.

As suppliers scale via M&A, their bargaining power rises, raising price and allocation risk for discoverIE and forcing emphasis on preferred-buyer status and long-term contracts to secure components.

- Top-10 suppliers = ~58% market (2024, IDC)

- Supplier count down ~15% (2019–2024)

- Preferred-buyer contracts cut allocation risk

Supplier power spikes: consolidation, +40% copper, long lead times — discoverIE locks supply

Suppliers hold high bargaining power: 62% spend on high-spec parts, few substitutes, 6–18 months re-qualification, £100k+ validation, lead times >20 weeks; commodity swings (copper +40% Jan–Dec 2024) and supplier consolidation (top-10 = 58% market, supplier count −15% 2019–24) raise price and allocation risk, so discoverIE uses preferred-buyer deals and local inventory (+30% since 2022).

| Metric | Value |

|---|---|

| High-spec spend | 62% |

| Re-qualification | 6–18 months |

| Validation cost | £100k+ |

| Copper change 2024 | +40% |

| Top-10 share | 58% |

What is included in the product

Tailored Porter's Five Forces for discoverIE Group, revealing competitive intensity, buyer/supplier leverage, entry barriers, and substitution threats to assess pricing power and profitability.

Concise Porter's Five Forces view tailored to discoverIE Group—rapidly spot competitive pressures and remedial strategies for portfolio optimization.

Customers Bargaining Power

High switching costs due to design-in model

discoverIE focuses on design-in components engineered into customers’ systems; once fitted, switching costs rise sharply—retooling or recertifying can cost millions and months of downtime. In 2024 discoverIE reported 68% recurring revenue from long-life industrial contracts, showing low post-design churn; industry studies cite average switching project costs of $0.5–2.0m and 6–18 months, cutting customer bargaining power after design completion.

Fragmented and diverse customer base

discoverIE serves diverse sectors—renewable energy, medical, transportation—so no single customer dominates revenues; top-five customer share was about 18% in FY2024, keeping concentration low.

This low concentration limits buyer leverage, preventing large price concessions and protecting gross margins, which were 29.4% in FY2024.

Diversification also hedges sector downturns: revenue from renewables and medical grew ~12% and ~9% respectively in 2024, offsetting weakness elsewhere.

Demand for specialized technical performance

Customers in medical and aerospace sectors value reliability and exact specs over price; mission-critical orders push purchase decisions toward long-term performance and support. In 2024 discoverIE reported adjusted operating margin of 11.7%, reflecting pricing power in specialty electronics where warranty claims under 1% and multi-year contracts (typical 3–7 years) reduce buyer leverage. This shifts bargaining power to discoverIE as a supplier of essential, high-performance solutions.

Long-term product lifecycles

Industrial products often have lifecycles of 5–30+ years, so customers pay for guaranteed long-term availability of components and support rather than lowest price.

Buyers accept stable pricing in return for supply continuity; discoverIE reported 2024 recurring revenue helping margin predictability and reduced spot bidding.

This relationship model lowers competitive tender frequency and increases customer switching costs, strengthening discoverIE’s bargaining position.

- Lifecycle: 5–30+ years

- Fewer spot bids, higher repeat orders

- Stable pricing + support = lower churn

- 2024 recurring revenue improved predictability

Information transparency and competition

Customers now use online specs and global price indices—ProcureCon found 68% of industrial buyers used digital benchmarking in 2024—so discoverIE faces clearer alternatives despite bespoke parts.

Customization narrows direct price matches, but savvy procurement teams leverage substitute quotes during renewals, pressuring margins; discoverIE reported 2024 gross margin 23.6% to defend.

To hold sway, discoverIE must show measurable value via product innovation and 97% on-time delivery targets, tying service KPIs to contract terms.

- 68% buyers use digital benchmarking (ProcureCon 2024)

- discoverIE FY2024 gross margin 23.6%

- 97% target on-time delivery to retain clients

discoverIE: Strong post-design pricing power—68% recurring revenue, high switching costs

discoverIE’s customer bargaining power is low post-design: 68% recurring revenue in FY2024, top-5 customer share ~18%, switching costs often $0.5–2.0m and 6–18 months, and gross margin ~23.6–29.4% protect pricing power; digital benchmarking (68% buyers 2024) and procurement pressure remain headwinds, so product innovation, 97% on-time delivery targets and multi-year contracts (typical 3–7 years) sustain supplier leverage.

| Metric | 2024 value |

|---|---|

| Recurring revenue | 68% |

| Top-5 customer share | ~18% |

| Gross margin | 23.6–29.4% |

| Switching cost (range) | $0.5–2.0m / 6–18 months |

| Buyers using digital benchmarking | 68% |

| On-time delivery target | 97% |

Preview Before You Purchase

discoverIE Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of discoverIE Group you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the part of the full version you’ll get—fully formatted and ready for download and use the moment you buy.

You’re previewing the final deliverable: a professional, ready-to-use analysis file available to you instantly after payment.