DL E&C Porter's Five Forces Analysis

Don't Miss the Bigger Picture

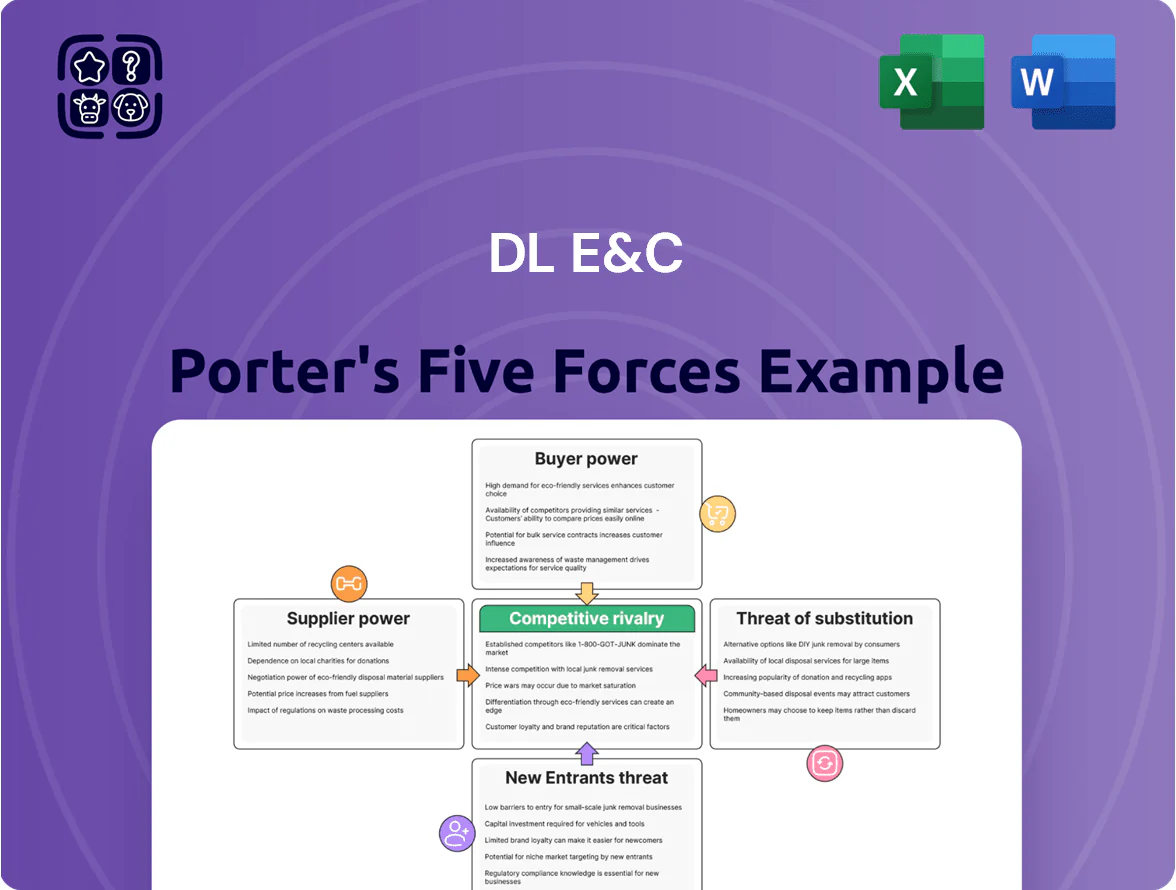

DL E&C faces moderate rivalry and significant supplier concentration, while new entrants and substitutes pose variable threats depending on project type and technology adoption; buyers wield strong bargaining power on large contracts—together shaping slim margins and strategic urgency.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore DL E&C’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of Essential Raw Material Costs

Steel, cement and ready-mix concrete account for roughly 35–45% of DL E&C project costs; global steel prices rose ~28% in 2021–2022 and inflation kept cement up ~12% in 2023, boosting supplier leverage during supply disruptions. Suppliers gain bargaining power in high-inflation or constrained-supply periods, so DL E&C uses multi-year supply contracts and a diversified vendor base—cutting single-supplier exposure to below 20%—to limit cost volatility.

Specialized Engineering and Technical Subcontractors

DL E&C relies on a small pool of specialist subcontractors for complex plant and civil works, giving suppliers bargaining power to push fees up—industry data show premium rates 15–30% above general contractors in 2024.

To counter this, DL E&C has built multi-year strategic partnerships and, since 2022, increased internal technical training >40% to cut external dependency and negotiate better terms.

Labor Market Constraints and Rising Wages

The shrinking skilled labor pool in South Korea and globally, with South Korea’s construction employment down ~6% since 2019 and average construction wages up ~18% from 2020–2024, raises supplier (labor) bargaining power and cost pressure on DL E&C.

Unions and trade groups wield leverage—strikes and negotiations delayed projects in 2023–24—hitting margins; labor disputes raised project delays by an estimated 3–7% in the sector.

DL E&C counters by automating sites and using modular construction; modular adoption rose to ~12% of projects in 2024, helping cut on-site labor hours by ~25% and protect EBITDA margins.

Energy and Logistics Provider Influence

- Electricity +12% (2024 Korea)

- Diesel ~$1.12/L (2024 avg)

- Transport premium 15–25%

- Target logistics cut 3–5%

Strategic Procurement of Green Technologies

As DL E&C expands into carbon capture and hydrogen plants, a small pool of advanced-environmental-tech suppliers (top 5 vendors control ~60% of IP) gives suppliers strong bargaining power during the early green transition, raising licensing and capex premiums by an estimated 15–25% in 2024–25.

DL E&C offsets this by scaling internal R&D—2025 budget target KRW 40bn—to develop proprietary capture membranes and electrolyzers, aiming to cut licensing costs by ~30% over five years.

- Top 5 tech suppliers ~60% IP share

- Supplier price premium +15–25% (2024–25)

- DL E&C 2025 R&D target KRW 40bn

- Goal: licensing cost cut ~30% in 5 years

Suppliers’ rising power squeezes DL E&C — materials, labor and specialist costs bite; mitigation via contracts, modulars, R&D

Suppliers hold moderate-to-high bargaining power for DL E&C: key materials (steel/cement ~35–45% costs) and specialist subcontractors push prices up (steel +28% 2021–22; cement +12% 2023; specialist premium 15–30% in 2024). Labor and energy cost rises (wages +18% 2020–24; electricity +12% 2024; diesel $1.12/L) increase leverage; DL E&C uses multi-year contracts, vendor diversification, modular build (~12% projects 2024) and KRW 40bn R&D (2025 target) to limit exposure.

| Metric | Value |

|---|---|

| Materials share | 35–45% |

| Steel change | +28% (2021–22) |

| Cement change | +12% (2023) |

| Specialist premium | 15–30% (2024) |

| Wage change | +18% (2020–24) |

| Electricity | +12% Korea (2024) |

| Diesel | $1.12/L (2024) |

| Modular share | ~12% (2024) |

| R&D target | KRW 40bn (2025) |

What is included in the product

Provides a concise Porter's Five Forces assessment tailored to DL E&C, highlighting competitive rivalry, buyer/supplier leverage, entry barriers, substitute threats, and strategic implications for pricing, margins, and market positioning.

DL E&C Porter's Five Forces condensed into one actionable sheet—quickly identify competitive hotspots and relief strategies for suppliers, buyers, entrants, substitutes, and rivalry to streamline boardroom decisions.

Customers Bargaining Power

Concentration of Government Infrastructure Projects

Public sector agencies account for roughly 60–75% of South Korea’s large civil contracts, giving government clients strong bargaining power over DL E&C by defining bidding terms, safety rules, and environmental standards.

These buyers demand high creditworthiness and safety: DL E&C maintains an A-/A3 credit band and zero-fatality site targets to qualify for tenders often worth KRW 200–1,000 billion.

Price Sensitivity in the Residential Housing Market

Individual buyers and developers show high price sensitivity to interest rates and cycles; Korean mortgage rates climbed from ~2.5% in 2021 to ~4.5% by end-2024, cutting housing demand and boosting buyer leverage against DL E&C residential brands like e-Pyeonhansesang.

When mortgage costs rise, buyers press for better amenities or discounts; DL E&C defends margins via premiumization and higher build quality, citing a 2024 ASP (avg. selling price) premium near 10% vs. mid-tier rivals to retain pricing power.

Corporate Client Leverage in EPC Contracts

Large petrochemical and power clients consolidate EPC spend—top 10 buyers account for ~40% of regional project awards in 2024—pressuring margins through volume pricing and long payment terms.

These buyers run strict audits and demand full cost transparency; 78% of major EPC contracts in 2023 included milestone-based audits and KPIs tied to 10–15% of final payment.

DL E&C leverages a 120+ project track record and digital tools (BIM, cloud PM) to demonstrate 7–12% efficiency gains, defending pricing and win rates.

Demand for Sustainable and ESG Compliant Buildings

Institutional investors and corporates now demand ESG and LEED-certified buildings; 2024 data show green-certified assets attracted 28% higher investment inflows globally, boosting buyer leverage over specs and materials.

Customers can dictate construction methods and materials, pressuring margins if suppliers don’t comply; DL E&C reduces this risk by embedding sustainable practices and energy-efficient designs into its core offerings.

- 2024: green asset inflows +28%

- DL E&C: core offerings include energy-efficient systems

- Customer leverage rises with stricter ESG/LEED rules

Availability of Alternative Construction Firms

The presence of multiple high-tier construction firms in South Korea and the Middle East lets clients switch if DL E&C misses milestones or quality targets, increasing customer bargaining power; global data shows 28% of large infrastructure clients invoked liquidated damages in 2023.

Clients use this leverage to demand strict performance guarantees and LD clauses; DL E&C counters by emphasizing execution excellence and CRM, keeping reported retention above 82% in 2024.

DL E&C: Public contracts, BIM gains & 82% retention counter buyer and green pressure

Public agencies (60–75% of large contracts) and top 10 EPC buyers (≈40% of awards) give clients strong leverage; DL E&C defends with A-/A3 credit, 120+ projects, BIM efficiencies (7–12%) and 82% retention. Mortgage rate rise to ~4.5% end-2024 cut housing demand, boosting buyer price pressure; green specs raised buyer leverage as green assets drew +28% inflows in 2024.

| Metric | Value (2024) |

|---|---|

| Public share | 60–75% |

| Top10 buyer share | ≈40% |

| Mortgage rate | ≈4.5% |

| Green inflows | +28% |

| BIM efficiency | 7–12% |

| Retention | 82% |

What You See Is What You Get

DL E&C Porter's Five Forces Analysis

This preview shows the exact DL E&C Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready to use with no placeholders or mockups.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

DL E&C faces moderate rivalry and significant supplier concentration, while new entrants and substitutes pose variable threats depending on project type and technology adoption; buyers wield strong bargaining power on large contracts—together shaping slim margins and strategic urgency.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore DL E&C’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of Essential Raw Material Costs

Steel, cement and ready-mix concrete account for roughly 35–45% of DL E&C project costs; global steel prices rose ~28% in 2021–2022 and inflation kept cement up ~12% in 2023, boosting supplier leverage during supply disruptions. Suppliers gain bargaining power in high-inflation or constrained-supply periods, so DL E&C uses multi-year supply contracts and a diversified vendor base—cutting single-supplier exposure to below 20%—to limit cost volatility.

Specialized Engineering and Technical Subcontractors

DL E&C relies on a small pool of specialist subcontractors for complex plant and civil works, giving suppliers bargaining power to push fees up—industry data show premium rates 15–30% above general contractors in 2024.

To counter this, DL E&C has built multi-year strategic partnerships and, since 2022, increased internal technical training >40% to cut external dependency and negotiate better terms.

Labor Market Constraints and Rising Wages

The shrinking skilled labor pool in South Korea and globally, with South Korea’s construction employment down ~6% since 2019 and average construction wages up ~18% from 2020–2024, raises supplier (labor) bargaining power and cost pressure on DL E&C.

Unions and trade groups wield leverage—strikes and negotiations delayed projects in 2023–24—hitting margins; labor disputes raised project delays by an estimated 3–7% in the sector.

DL E&C counters by automating sites and using modular construction; modular adoption rose to ~12% of projects in 2024, helping cut on-site labor hours by ~25% and protect EBITDA margins.

Energy and Logistics Provider Influence

- Electricity +12% (2024 Korea)

- Diesel ~$1.12/L (2024 avg)

- Transport premium 15–25%

- Target logistics cut 3–5%

Strategic Procurement of Green Technologies

As DL E&C expands into carbon capture and hydrogen plants, a small pool of advanced-environmental-tech suppliers (top 5 vendors control ~60% of IP) gives suppliers strong bargaining power during the early green transition, raising licensing and capex premiums by an estimated 15–25% in 2024–25.

DL E&C offsets this by scaling internal R&D—2025 budget target KRW 40bn—to develop proprietary capture membranes and electrolyzers, aiming to cut licensing costs by ~30% over five years.

- Top 5 tech suppliers ~60% IP share

- Supplier price premium +15–25% (2024–25)

- DL E&C 2025 R&D target KRW 40bn

- Goal: licensing cost cut ~30% in 5 years

Suppliers’ rising power squeezes DL E&C — materials, labor and specialist costs bite; mitigation via contracts, modulars, R&D

Suppliers hold moderate-to-high bargaining power for DL E&C: key materials (steel/cement ~35–45% costs) and specialist subcontractors push prices up (steel +28% 2021–22; cement +12% 2023; specialist premium 15–30% in 2024). Labor and energy cost rises (wages +18% 2020–24; electricity +12% 2024; diesel $1.12/L) increase leverage; DL E&C uses multi-year contracts, vendor diversification, modular build (~12% projects 2024) and KRW 40bn R&D (2025 target) to limit exposure.

| Metric | Value |

|---|---|

| Materials share | 35–45% |

| Steel change | +28% (2021–22) |

| Cement change | +12% (2023) |

| Specialist premium | 15–30% (2024) |

| Wage change | +18% (2020–24) |

| Electricity | +12% Korea (2024) |

| Diesel | $1.12/L (2024) |

| Modular share | ~12% (2024) |

| R&D target | KRW 40bn (2025) |

What is included in the product

Provides a concise Porter's Five Forces assessment tailored to DL E&C, highlighting competitive rivalry, buyer/supplier leverage, entry barriers, substitute threats, and strategic implications for pricing, margins, and market positioning.

DL E&C Porter's Five Forces condensed into one actionable sheet—quickly identify competitive hotspots and relief strategies for suppliers, buyers, entrants, substitutes, and rivalry to streamline boardroom decisions.

Customers Bargaining Power

Concentration of Government Infrastructure Projects

Public sector agencies account for roughly 60–75% of South Korea’s large civil contracts, giving government clients strong bargaining power over DL E&C by defining bidding terms, safety rules, and environmental standards.

These buyers demand high creditworthiness and safety: DL E&C maintains an A-/A3 credit band and zero-fatality site targets to qualify for tenders often worth KRW 200–1,000 billion.

Price Sensitivity in the Residential Housing Market

Individual buyers and developers show high price sensitivity to interest rates and cycles; Korean mortgage rates climbed from ~2.5% in 2021 to ~4.5% by end-2024, cutting housing demand and boosting buyer leverage against DL E&C residential brands like e-Pyeonhansesang.

When mortgage costs rise, buyers press for better amenities or discounts; DL E&C defends margins via premiumization and higher build quality, citing a 2024 ASP (avg. selling price) premium near 10% vs. mid-tier rivals to retain pricing power.

Corporate Client Leverage in EPC Contracts

Large petrochemical and power clients consolidate EPC spend—top 10 buyers account for ~40% of regional project awards in 2024—pressuring margins through volume pricing and long payment terms.

These buyers run strict audits and demand full cost transparency; 78% of major EPC contracts in 2023 included milestone-based audits and KPIs tied to 10–15% of final payment.

DL E&C leverages a 120+ project track record and digital tools (BIM, cloud PM) to demonstrate 7–12% efficiency gains, defending pricing and win rates.

Demand for Sustainable and ESG Compliant Buildings

Institutional investors and corporates now demand ESG and LEED-certified buildings; 2024 data show green-certified assets attracted 28% higher investment inflows globally, boosting buyer leverage over specs and materials.

Customers can dictate construction methods and materials, pressuring margins if suppliers don’t comply; DL E&C reduces this risk by embedding sustainable practices and energy-efficient designs into its core offerings.

- 2024: green asset inflows +28%

- DL E&C: core offerings include energy-efficient systems

- Customer leverage rises with stricter ESG/LEED rules

Availability of Alternative Construction Firms

The presence of multiple high-tier construction firms in South Korea and the Middle East lets clients switch if DL E&C misses milestones or quality targets, increasing customer bargaining power; global data shows 28% of large infrastructure clients invoked liquidated damages in 2023.

Clients use this leverage to demand strict performance guarantees and LD clauses; DL E&C counters by emphasizing execution excellence and CRM, keeping reported retention above 82% in 2024.

DL E&C: Public contracts, BIM gains & 82% retention counter buyer and green pressure

Public agencies (60–75% of large contracts) and top 10 EPC buyers (≈40% of awards) give clients strong leverage; DL E&C defends with A-/A3 credit, 120+ projects, BIM efficiencies (7–12%) and 82% retention. Mortgage rate rise to ~4.5% end-2024 cut housing demand, boosting buyer price pressure; green specs raised buyer leverage as green assets drew +28% inflows in 2024.

| Metric | Value (2024) |

|---|---|

| Public share | 60–75% |

| Top10 buyer share | ≈40% |

| Mortgage rate | ≈4.5% |

| Green inflows | +28% |

| BIM efficiency | 7–12% |

| Retention | 82% |

What You See Is What You Get

DL E&C Porter's Five Forces Analysis

This preview shows the exact DL E&C Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready to use with no placeholders or mockups.