DNB Bank Boston Consulting Group Matrix

Actionable Strategy Starts Here

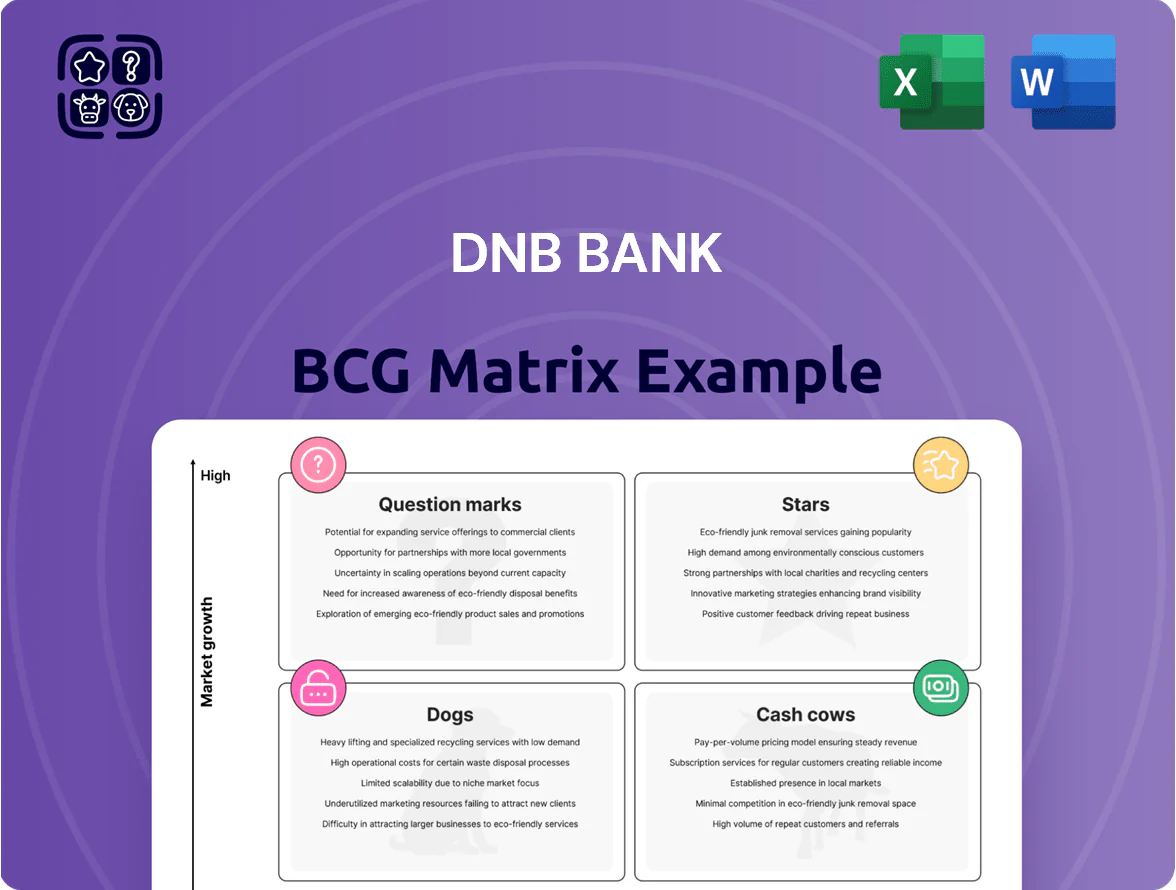

DNB Bank’s BCG Matrix snapshot highlights which business units drive growth and which consume cash amid shifting Nordic markets; our preview teases Stars, Cash Cows, Dogs, and Question Marks but stops short of the quadrant-level strategy you need. Purchase the full BCG Matrix to get a complete, data-driven breakdown of each segment, quadrant-by-quadrant recommendations, and ready-to-use Word and Excel deliverables that accelerate your investment and capital-allocation decisions.

Stars

Renewable Energy Financing

DNB has a leading share in renewable energy financing, notably offshore wind and solar, backing projects totaling ~€18.5bn in commitments through 2025; specialized teams drive deal win rates above 35% in Europe.

Sustainable Bond Issuance

As primary underwriter for ESG-linked debt in the Nordics, DNB captured about 38% market share in 2024, underwriting NOK 72 billion of green/social bonds, so this is a Stars quadrant asset. Investors’ demand pushed IB revenue growth ~22% YoY in 2024, lifting fee income and deal flow. High transaction volumes require ongoing spend—DNB reported NOK 210 million in 2024 on ESG verification and hired 60 specialists to scale capacity.

Digital Wealth Management

DNB Banks digital wealth-management platforms lead Norway’s tech-savvy retail market, with a 2024 market share of about 34% in robo-advice and automated funds flows, handling NOK 120 billion in client assets under management (AUM) as of Dec 31, 2024.

Growth stays robust: retail allocations to digital equity and fund products rose 22% YoY in 2024 as traditional savings moved away from cash and deposits.

DNB invested NOK 850 million in 2023–24 on UI upgrades and algorithmic advisory models, keeping product rollout cadence high to repel fintech disruptors and sustain customer acquisition.

Nordic Corporate M&A Advisory

DNB Markets dominates Nordic M&A in energy and seafood, advising on roughly 40% of regional deals in 2024 and generating about NOK 1.2bn in fees that year.

Deal flow is rising as post-transition consolidation pushes companies to scale; Nordic energy and seafood deal value grew 18% y/y to NOK 120bn in 2024.

High revenue comes with heavy costs: top-tier bankers, global roadshows, and compliance pushed unit operating spend to ~NOK 650m in 2024.

- Market share ~40% (2024)

- Fees ~NOK 1.2bn (2024)

- Deal value NOK 120bn, +18% y/y (2024)

- Operating spend ~NOK 650m (2024)

Integrated Payment Solutions

DNB’s Integrated Payment Solutions sit as Stars: DNB processes ~45% of Norway’s digital transactions via Vipps and bank channels, benefiting from a 2024 cashless trend where card and mobile payments rose 6.8% YoY; revenue from payments grew ~12% in 2024, but sustaining growth needs ongoing investment in fraud detection and SEPA/PSD2-compliant cross-border rails.

- ~45% market share in domestic digital transactions

- Card/mobile payments +6.8% YoY (2024)

- Payments revenue +12% (2024)

- Key needs: fraud AI, cross-border SEPA/PSD2 integration

DNB: Nordic renewable finance leader—€18.5bn commitments, digital & ESG market dominance

DNB’s Stars: leading renewable finance (~€18.5bn commitments to 2025), Nordic ESG bond underwriter (38% share; NOK 72bn, 2024), digital wealth AUM NOK 120bn (34% robo market, 2024), payments ~45% domestic digital transactions; high revenue growth balanced by NOK 650m operating spend and NOK 210m ESG costs (2024).

| Metric | Value (2024) |

|---|---|

| Renewable commitments | €18.5bn to 2025 |

| ESG bonds underwritten | NOK 72bn (38%) |

| Digital wealth AUM | NOK 120bn (34%) |

| Payments market share | ~45% |

| Operating spend | NOK 650m |

| ESG verification cost | NOK 210m |

What is included in the product

Comprehensive BCG Matrix review of DNB Bank’s units with strategic guidance on Stars, Cash Cows, Question Marks, and Dogs.

One-page BCG Matrix mapping DNB business units for quick strategic clarity and executive decision-making.

Cash Cows

Norwegian Residential Mortgages

Norwegian residential mortgages form DNB Bank’s stability core, with about 30% market share and NOK 1,000+ billion in mortgage loans by end-2024 in a mature domestic market growing ~1% annually.

High net interest margins (~1.5% on mortgages in 2024) and low per-loan costs produce significant excess cash, funding dividends (pay-out ratio ~60% in 2024) and NOK 4–6 billion annual digital transformation spend.

Personal Savings and Deposits

DNB remains the primary deposit bank for roughly 50% of Norwegian households, giving the group a low-cost funding base that supported NOK 1,250bn in customer deposits at year-end 2025. Market growth is limited by high penetration—retail deposit penetration in Norway exceeds 85%—so personal savings sit in the BCG Cash Cows quadrant. The segment needs minimal marketing spend and delivers steady net interest income, contributing about 35% of group funding benefits annually. Predictable deposits lower funding volatility and reduce wholesale refinancing needs.

Traditional Shipping Finance

DNB’s Traditional Shipping Finance remains a cash cow: Norway’s leading maritime lender held ~15% of global export ship finance as of 2024 and booked NOK 3.4bn in shipping net interest income in 2024, while global seaborne trade growth is ~2–3% CAGR and highly cyclical. The unit leverages DNB’s top-tier reputation to select low-default, large clients with low origination cost, funding greener ventures and R&D from stable cashflows.

Life Insurance and Pensions

DNB Liv (DNB Livsforsikring) holds about 30% of Norway’s institutional pension market and ~22% of retail pensions as of 2025, making it a market leader; the sector is mature and tightly regulated, so revenue growth runs ~2–4% annually but operating margins stay high.

High scale and cost-efficiency let Life Insurance and Pensions generate strong cash returns, funding roughly NOK 18–22 billion to group central reserves in 2024–25, supporting capital ratios and dividend capacity.

- Market shares: ~30% institutional, ~22% retail (2025)

- Growth: stable 2–4% p.a.

- Cash contribution: ~NOK 18–22bn (2024–25)

- Role: steady cash cow; supports CET1 and dividends

Domestic SME Lending

Domestic SME lending is a cash cow for DNB Bank, holding roughly 35% market share in Norway’s SME loans (€18bn outstanding at YE 2025) and delivering stable NIMs near 2.1% while loan-loss rates stay low at 0.4% due to rich behavioral data and conservative underwriting.

Economic maturity caps volume growth to ~2–3% CAGR, but high fee income and limited capex needs keep RoTE steady around 12% and generate predictable earnings for the corporate portfolio.

- €18bn outstanding (YE 2025)

- 35% market share in Norway

- NIM ~2.1%, loan-loss 0.4%

- Projected growth 2–3% CAGR

- RoTE ~12%, low incremental capex

DNB’s cash cows: High-margin mortgages, SME, shipping & DNB Liv fuelling steady cash

DNB’s cash cows—Norwegian mortgages, SME lending, shipping finance, and DNB Liv—deliver steady cash (NOK 18–22bn from Life, ~NOK 10–14bn from mortgages/SME/shipping combined in 2024–25), high margins (mortgage NIM ~1.5%, SME NIM ~2.1%), large shares (mortgages ~30%, SME ~35%, DNB Liv institutional ~30%) and low growth (1–4% CAGR), funding dividends and digital spend.

| Segment | Market share | Key metric | Cash (2024–25) |

|---|---|---|---|

| Mortgages | ~30% | NIM ~1.5%, NOK 1,000bn+ | NOK 4–6bn |

| SME lending | ~35% | €18bn, NIM ~2.1% | NOK 2–4bn |

| Shipping finance | ~15% global export finance | cyclical, NOK 3.4bn NII | NOK 1–2bn |

| DNB Liv | ~30% institutional | 30% inst., 22% retail | NOK 18–22bn |

What You’re Viewing Is Included

DNB Bank BCG Matrix

The file you're previewing on this page is the exact DNB Bank BCG Matrix report you'll receive after purchase—no watermarks, no demo pages—just a fully formatted, analysis-ready document designed for strategic clarity and professional presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

DNB Bank’s BCG Matrix snapshot highlights which business units drive growth and which consume cash amid shifting Nordic markets; our preview teases Stars, Cash Cows, Dogs, and Question Marks but stops short of the quadrant-level strategy you need. Purchase the full BCG Matrix to get a complete, data-driven breakdown of each segment, quadrant-by-quadrant recommendations, and ready-to-use Word and Excel deliverables that accelerate your investment and capital-allocation decisions.

Stars

Renewable Energy Financing

DNB has a leading share in renewable energy financing, notably offshore wind and solar, backing projects totaling ~€18.5bn in commitments through 2025; specialized teams drive deal win rates above 35% in Europe.

Sustainable Bond Issuance

As primary underwriter for ESG-linked debt in the Nordics, DNB captured about 38% market share in 2024, underwriting NOK 72 billion of green/social bonds, so this is a Stars quadrant asset. Investors’ demand pushed IB revenue growth ~22% YoY in 2024, lifting fee income and deal flow. High transaction volumes require ongoing spend—DNB reported NOK 210 million in 2024 on ESG verification and hired 60 specialists to scale capacity.

Digital Wealth Management

DNB Banks digital wealth-management platforms lead Norway’s tech-savvy retail market, with a 2024 market share of about 34% in robo-advice and automated funds flows, handling NOK 120 billion in client assets under management (AUM) as of Dec 31, 2024.

Growth stays robust: retail allocations to digital equity and fund products rose 22% YoY in 2024 as traditional savings moved away from cash and deposits.

DNB invested NOK 850 million in 2023–24 on UI upgrades and algorithmic advisory models, keeping product rollout cadence high to repel fintech disruptors and sustain customer acquisition.

Nordic Corporate M&A Advisory

DNB Markets dominates Nordic M&A in energy and seafood, advising on roughly 40% of regional deals in 2024 and generating about NOK 1.2bn in fees that year.

Deal flow is rising as post-transition consolidation pushes companies to scale; Nordic energy and seafood deal value grew 18% y/y to NOK 120bn in 2024.

High revenue comes with heavy costs: top-tier bankers, global roadshows, and compliance pushed unit operating spend to ~NOK 650m in 2024.

- Market share ~40% (2024)

- Fees ~NOK 1.2bn (2024)

- Deal value NOK 120bn, +18% y/y (2024)

- Operating spend ~NOK 650m (2024)

Integrated Payment Solutions

DNB’s Integrated Payment Solutions sit as Stars: DNB processes ~45% of Norway’s digital transactions via Vipps and bank channels, benefiting from a 2024 cashless trend where card and mobile payments rose 6.8% YoY; revenue from payments grew ~12% in 2024, but sustaining growth needs ongoing investment in fraud detection and SEPA/PSD2-compliant cross-border rails.

- ~45% market share in domestic digital transactions

- Card/mobile payments +6.8% YoY (2024)

- Payments revenue +12% (2024)

- Key needs: fraud AI, cross-border SEPA/PSD2 integration

DNB: Nordic renewable finance leader—€18.5bn commitments, digital & ESG market dominance

DNB’s Stars: leading renewable finance (~€18.5bn commitments to 2025), Nordic ESG bond underwriter (38% share; NOK 72bn, 2024), digital wealth AUM NOK 120bn (34% robo market, 2024), payments ~45% domestic digital transactions; high revenue growth balanced by NOK 650m operating spend and NOK 210m ESG costs (2024).

| Metric | Value (2024) |

|---|---|

| Renewable commitments | €18.5bn to 2025 |

| ESG bonds underwritten | NOK 72bn (38%) |

| Digital wealth AUM | NOK 120bn (34%) |

| Payments market share | ~45% |

| Operating spend | NOK 650m |

| ESG verification cost | NOK 210m |

What is included in the product

Comprehensive BCG Matrix review of DNB Bank’s units with strategic guidance on Stars, Cash Cows, Question Marks, and Dogs.

One-page BCG Matrix mapping DNB business units for quick strategic clarity and executive decision-making.

Cash Cows

Norwegian Residential Mortgages

Norwegian residential mortgages form DNB Bank’s stability core, with about 30% market share and NOK 1,000+ billion in mortgage loans by end-2024 in a mature domestic market growing ~1% annually.

High net interest margins (~1.5% on mortgages in 2024) and low per-loan costs produce significant excess cash, funding dividends (pay-out ratio ~60% in 2024) and NOK 4–6 billion annual digital transformation spend.

Personal Savings and Deposits

DNB remains the primary deposit bank for roughly 50% of Norwegian households, giving the group a low-cost funding base that supported NOK 1,250bn in customer deposits at year-end 2025. Market growth is limited by high penetration—retail deposit penetration in Norway exceeds 85%—so personal savings sit in the BCG Cash Cows quadrant. The segment needs minimal marketing spend and delivers steady net interest income, contributing about 35% of group funding benefits annually. Predictable deposits lower funding volatility and reduce wholesale refinancing needs.

Traditional Shipping Finance

DNB’s Traditional Shipping Finance remains a cash cow: Norway’s leading maritime lender held ~15% of global export ship finance as of 2024 and booked NOK 3.4bn in shipping net interest income in 2024, while global seaborne trade growth is ~2–3% CAGR and highly cyclical. The unit leverages DNB’s top-tier reputation to select low-default, large clients with low origination cost, funding greener ventures and R&D from stable cashflows.

Life Insurance and Pensions

DNB Liv (DNB Livsforsikring) holds about 30% of Norway’s institutional pension market and ~22% of retail pensions as of 2025, making it a market leader; the sector is mature and tightly regulated, so revenue growth runs ~2–4% annually but operating margins stay high.

High scale and cost-efficiency let Life Insurance and Pensions generate strong cash returns, funding roughly NOK 18–22 billion to group central reserves in 2024–25, supporting capital ratios and dividend capacity.

- Market shares: ~30% institutional, ~22% retail (2025)

- Growth: stable 2–4% p.a.

- Cash contribution: ~NOK 18–22bn (2024–25)

- Role: steady cash cow; supports CET1 and dividends

Domestic SME Lending

Domestic SME lending is a cash cow for DNB Bank, holding roughly 35% market share in Norway’s SME loans (€18bn outstanding at YE 2025) and delivering stable NIMs near 2.1% while loan-loss rates stay low at 0.4% due to rich behavioral data and conservative underwriting.

Economic maturity caps volume growth to ~2–3% CAGR, but high fee income and limited capex needs keep RoTE steady around 12% and generate predictable earnings for the corporate portfolio.

- €18bn outstanding (YE 2025)

- 35% market share in Norway

- NIM ~2.1%, loan-loss 0.4%

- Projected growth 2–3% CAGR

- RoTE ~12%, low incremental capex

DNB’s cash cows: High-margin mortgages, SME, shipping & DNB Liv fuelling steady cash

DNB’s cash cows—Norwegian mortgages, SME lending, shipping finance, and DNB Liv—deliver steady cash (NOK 18–22bn from Life, ~NOK 10–14bn from mortgages/SME/shipping combined in 2024–25), high margins (mortgage NIM ~1.5%, SME NIM ~2.1%), large shares (mortgages ~30%, SME ~35%, DNB Liv institutional ~30%) and low growth (1–4% CAGR), funding dividends and digital spend.

| Segment | Market share | Key metric | Cash (2024–25) |

|---|---|---|---|

| Mortgages | ~30% | NIM ~1.5%, NOK 1,000bn+ | NOK 4–6bn |

| SME lending | ~35% | €18bn, NIM ~2.1% | NOK 2–4bn |

| Shipping finance | ~15% global export finance | cyclical, NOK 3.4bn NII | NOK 1–2bn |

| DNB Liv | ~30% institutional | 30% inst., 22% retail | NOK 18–22bn |

What You’re Viewing Is Included

DNB Bank BCG Matrix

The file you're previewing on this page is the exact DNB Bank BCG Matrix report you'll receive after purchase—no watermarks, no demo pages—just a fully formatted, analysis-ready document designed for strategic clarity and professional presentation.