DNB Bank PESTLE Analysis

Your Competitive Advantage Starts with This Report

Understand how political, economic, and technological forces are reshaping DNB Bank’s strategic landscape—our concise PESTLE highlights risks like regulatory shifts and climate mandates, plus opportunities in digital finance and Nordic growth. Ready-made for investors and strategists, the full PESTLE delivers actionable, editable insights to inform decisions and forecasts. Purchase now to access the complete analysis and start leveraging external trends immediately.

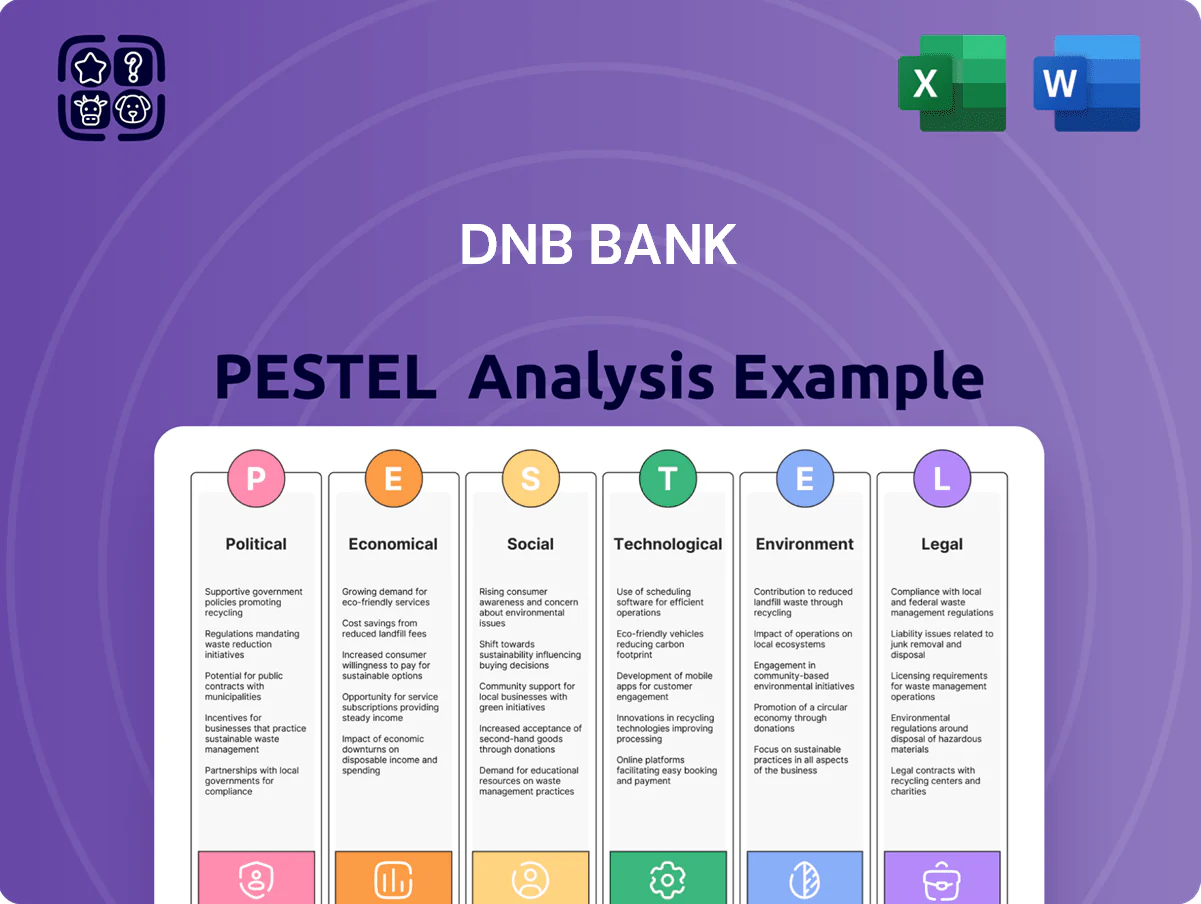

Political factors

State Ownership and Stability

The Norwegian state, via the Ministry of Trade, Industry and Fisheries, holds about 34 percent of DNB, giving the bank exceptional institutional stability and alignment with Norway’s fiscal priorities; this stake supported DNB during 2023–2025 volatility as CET1 remained around 16% and return on equity near 12% in 2024.

Geopolitical Influence on Energy and Shipping

DNB's leading position in energy and shipping finance makes it highly exposed to geopolitical tensions: disruptions like Red Sea transit risks increased VLCC freight rates by over 40% in 2024, pressuring client cashflows and collateral values.

By end-2025, shifting alliances and sanctions—EU/US measures affecting Russian and Iranian energy flows—require DNB to use enhanced country limits and scenario stress tests covering >30% of its international corporate portfolio.

Political instability in key maritime corridors raises non-performing loan risk for sector borrowers; DNB reported sector-weighted impairment coverage ratios rising to ~2.8% in 2024, signaling tightened credit appetite.

EEA Integration and Regulatory Alignment

Norway’s EEA membership forces DNB to implement EU financial packages and Banking Union standards despite non-EU status, requiring alignment with EU rules that covered roughly €38.5 trillion in EU banking assets in 2024; this drives ongoing coordination with Brussels and Oslo to maintain regulatory equivalence and cross-border market access. DNB’s regulatory capital ratio of 19.1% (end-2024) reflects buffers maintained amid evolving EU directives and stress-test expectations.

National Green Transition Policies

The Norwegian government’s target of carbon neutrality by 2050 and interim 2030 emissions cuts increase political pressure on DNB to finance renewables; Norway pledged a 50–55% reduction from 1990 levels by 2030 and green investments rose to NOK 120 bn in 2024.

Political mandates channel capital to Nordic sustainable infrastructure, with EU green taxonomy alignment affecting lending standards and DNB’s sustainability-linked loans totaling over NOK 80 bn by 2025.

DNB must reconcile rapid decarbonization expectations with revenue exposure to oil and gas—Norwegian oil & gas accounted for ~14% of GDP and DNB’s corporate loan book had notable fossil fuel clients through 2024.

- Norway: carbon neutrality by 2050; 50–55% GHG cut by 2030

- NOK 120 bn in green investments (2024)

- DNB sustainability-linked loans >NOK 80 bn (2025)

- Oil & gas ≈14% of Norwegian GDP; significant exposure in DNB loan book (2024)

Trade Relations and Export Finance

DNB underwrites roughly NOK 200–250bn in export-related exposures and is exposed to shifts in trade agreements and protectionism that could hinder Norwegian seafood and maritime exports.

Political moves in the US, China or EU affect demand; a 10% tariff or stricter quotas on seafood could materially stress clients in fisheries and shipping that represent a sizable share of DNB’s corporate loan book.

- Exposure: NOK ~200–250bn export finance

- Key sectors: seafood, maritime—significant loan concentration

- Risk: tariffs/quotas in US/China can reduce export volumes

- Action: recalibrate lending, increase geopolitical stress testing

DNB: 34% state backing, CET1 ~16%, ROE ~12% — strong capital, green push

State 34% ownership gives DNB institutional stability; CET1 ~16% (2024) and ROE ~12% (2024). Geopolitical risks (Red Sea, sanctions) raised VLCC rates +40% (2024) and drove sector impairments to ~2.8% (2024). Norway: carbon neutrality 2050, −50–55% by 2030; green invest NOK120bn (2024); DNB sustainability loans >NOK80bn (2025). Export exposure NOK200–250bn; regulatory capital 19.1% (end‑2024).

| Metric | Value |

|---|---|

| State stake | 34% |

| CET1 (2024) | ~16% |

| ROE (2024) | ~12% |

| Impairments (sector) | ~2.8% |

| Green invest (Norway 2024) | NOK120bn |

| DNB green loans (2025) | >NOK80bn |

| Export exposure | NOK200–250bn |

| Regulatory capital (end‑2024) | 19.1% |

What is included in the product

Explores how macro-environmental factors uniquely affect DNB Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and trends to identify risks and opportunities for strategy and scenario planning.

Provides a concise, visually segmented PESTLE summary of DNB Bank that’s easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Interest Rate Environment and Net Interest Margin

Norges Bank’s 2025 monetary policy, keeping the policy rate near 4.5% (vs ~0% in the 2010s), materially supported DNB’s net interest margin, lifting group net interest income by roughly 18% year-on-year through H1 2025 to NOK ~34 billion.

Higher rates improved earnings on loans and deposits but raised expected credit losses; DNB reported Stage 3 loans edging up to ~1.9% of gross loans, reflecting elevated default risk among leveraged households and corporates.

Volatility in Energy and Seafood Markets

DNB’s heavy exposure to energy and seafood makes earnings cyclical and tied to commodity swings; Norwegian oil & gas investment fell 18% in 2023 vs 2022, pressuring corporate lending and fees.

Oil prices swung ~40% between 2022–2024, altering clients’ repayment capacity in the North Sea and driving higher impairment charges for DNB.

Seafood exports (~NOK 110bn in 2024) face demand and biological risks (e.g., sea lice), directly impacting credit quality in DNB’s corporate loan book.

Norwegian Household Debt Levels

Norwegian household debt reached about 264% of disposable income in 2024, driven largely by mortgage exposure, posing systemic risk to DNB if unemployment spikes or house prices fall sharply.

DNB reports mortgage loans constituting roughly 40% of its loan book, so a severe property downturn could materially raise impairment losses despite the bank's stringent lending criteria.

Analysts remain wary: even with loan-to-value limits and stress tests, high household leverage keeps credit risk elevated for DNB's domestic franchise.

Inflationary Pressures and Operational Costs

Persistent inflation through 2025 pushed DNB Banks operating costs up about 6-8% YoY, with personnel expenses rising roughly 7% and tech procurement costs up near 10% as suppliers passed on higher input prices.

To offset this, DNB expanded cost-efficiency programs targeting NOK 1–1.5 billion in annual savings while still allocating ~5% of revenue to strategic digital and branch investments.

- Operating costs +6–8% YoY (2025)

- Personnel +7%, tech procurement +10%

- Targeted savings NOK 1–1.5bn

- ~5% revenue reinvested in infrastructure

Currency Fluctuations and the Norwegian Krone

- 10% NOK move materially impacts reported foreign assets and P&L

- Export-client credit risk increases with NOK weakness

- FX swings influenced CET1 by ~0.1–0.3 pp in 2023–2024

DNB H1 2025: NOK 34bn NII, 4.5% rates, 264% household debt, costs +6–8%

Norges Bank rate ~4.5% in 2025 lifted NII ~18% to NOK ~34bn H1 2025; Stage 3 loans ~1.9%; household debt ~264% of disposable income (2024); mortgage loans ~40% of DNB loan book; operating costs +6–8% YoY (2025) with personnel +7%, tech +10%; NOK 10% depreciation moved reported foreign assets and P&L; revenue ~20% outside Norway.

| Metric | Value |

|---|---|

| Net interest income H1 2025 | NOK ~34bn |

| Rate | ~4.5% |

| Stage 3 loans | ~1.9% |

| Household debt | 264% disp. income (2024) |

| Mortgage share | ~40% |

| Op costs YoY | +6–8% |

| FX revenue exposure | ~20% |

Preview Before You Purchase

DNB Bank PESTLE Analysis

The preview shown here is the exact DNB Bank PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content and layout visible in this preview are the same file you’ll download immediately after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Understand how political, economic, and technological forces are reshaping DNB Bank’s strategic landscape—our concise PESTLE highlights risks like regulatory shifts and climate mandates, plus opportunities in digital finance and Nordic growth. Ready-made for investors and strategists, the full PESTLE delivers actionable, editable insights to inform decisions and forecasts. Purchase now to access the complete analysis and start leveraging external trends immediately.

Political factors

State Ownership and Stability

The Norwegian state, via the Ministry of Trade, Industry and Fisheries, holds about 34 percent of DNB, giving the bank exceptional institutional stability and alignment with Norway’s fiscal priorities; this stake supported DNB during 2023–2025 volatility as CET1 remained around 16% and return on equity near 12% in 2024.

Geopolitical Influence on Energy and Shipping

DNB's leading position in energy and shipping finance makes it highly exposed to geopolitical tensions: disruptions like Red Sea transit risks increased VLCC freight rates by over 40% in 2024, pressuring client cashflows and collateral values.

By end-2025, shifting alliances and sanctions—EU/US measures affecting Russian and Iranian energy flows—require DNB to use enhanced country limits and scenario stress tests covering >30% of its international corporate portfolio.

Political instability in key maritime corridors raises non-performing loan risk for sector borrowers; DNB reported sector-weighted impairment coverage ratios rising to ~2.8% in 2024, signaling tightened credit appetite.

EEA Integration and Regulatory Alignment

Norway’s EEA membership forces DNB to implement EU financial packages and Banking Union standards despite non-EU status, requiring alignment with EU rules that covered roughly €38.5 trillion in EU banking assets in 2024; this drives ongoing coordination with Brussels and Oslo to maintain regulatory equivalence and cross-border market access. DNB’s regulatory capital ratio of 19.1% (end-2024) reflects buffers maintained amid evolving EU directives and stress-test expectations.

National Green Transition Policies

The Norwegian government’s target of carbon neutrality by 2050 and interim 2030 emissions cuts increase political pressure on DNB to finance renewables; Norway pledged a 50–55% reduction from 1990 levels by 2030 and green investments rose to NOK 120 bn in 2024.

Political mandates channel capital to Nordic sustainable infrastructure, with EU green taxonomy alignment affecting lending standards and DNB’s sustainability-linked loans totaling over NOK 80 bn by 2025.

DNB must reconcile rapid decarbonization expectations with revenue exposure to oil and gas—Norwegian oil & gas accounted for ~14% of GDP and DNB’s corporate loan book had notable fossil fuel clients through 2024.

- Norway: carbon neutrality by 2050; 50–55% GHG cut by 2030

- NOK 120 bn in green investments (2024)

- DNB sustainability-linked loans >NOK 80 bn (2025)

- Oil & gas ≈14% of Norwegian GDP; significant exposure in DNB loan book (2024)

Trade Relations and Export Finance

DNB underwrites roughly NOK 200–250bn in export-related exposures and is exposed to shifts in trade agreements and protectionism that could hinder Norwegian seafood and maritime exports.

Political moves in the US, China or EU affect demand; a 10% tariff or stricter quotas on seafood could materially stress clients in fisheries and shipping that represent a sizable share of DNB’s corporate loan book.

- Exposure: NOK ~200–250bn export finance

- Key sectors: seafood, maritime—significant loan concentration

- Risk: tariffs/quotas in US/China can reduce export volumes

- Action: recalibrate lending, increase geopolitical stress testing

DNB: 34% state backing, CET1 ~16%, ROE ~12% — strong capital, green push

State 34% ownership gives DNB institutional stability; CET1 ~16% (2024) and ROE ~12% (2024). Geopolitical risks (Red Sea, sanctions) raised VLCC rates +40% (2024) and drove sector impairments to ~2.8% (2024). Norway: carbon neutrality 2050, −50–55% by 2030; green invest NOK120bn (2024); DNB sustainability loans >NOK80bn (2025). Export exposure NOK200–250bn; regulatory capital 19.1% (end‑2024).

| Metric | Value |

|---|---|

| State stake | 34% |

| CET1 (2024) | ~16% |

| ROE (2024) | ~12% |

| Impairments (sector) | ~2.8% |

| Green invest (Norway 2024) | NOK120bn |

| DNB green loans (2025) | >NOK80bn |

| Export exposure | NOK200–250bn |

| Regulatory capital (end‑2024) | 19.1% |

What is included in the product

Explores how macro-environmental factors uniquely affect DNB Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and trends to identify risks and opportunities for strategy and scenario planning.

Provides a concise, visually segmented PESTLE summary of DNB Bank that’s easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Interest Rate Environment and Net Interest Margin

Norges Bank’s 2025 monetary policy, keeping the policy rate near 4.5% (vs ~0% in the 2010s), materially supported DNB’s net interest margin, lifting group net interest income by roughly 18% year-on-year through H1 2025 to NOK ~34 billion.

Higher rates improved earnings on loans and deposits but raised expected credit losses; DNB reported Stage 3 loans edging up to ~1.9% of gross loans, reflecting elevated default risk among leveraged households and corporates.

Volatility in Energy and Seafood Markets

DNB’s heavy exposure to energy and seafood makes earnings cyclical and tied to commodity swings; Norwegian oil & gas investment fell 18% in 2023 vs 2022, pressuring corporate lending and fees.

Oil prices swung ~40% between 2022–2024, altering clients’ repayment capacity in the North Sea and driving higher impairment charges for DNB.

Seafood exports (~NOK 110bn in 2024) face demand and biological risks (e.g., sea lice), directly impacting credit quality in DNB’s corporate loan book.

Norwegian Household Debt Levels

Norwegian household debt reached about 264% of disposable income in 2024, driven largely by mortgage exposure, posing systemic risk to DNB if unemployment spikes or house prices fall sharply.

DNB reports mortgage loans constituting roughly 40% of its loan book, so a severe property downturn could materially raise impairment losses despite the bank's stringent lending criteria.

Analysts remain wary: even with loan-to-value limits and stress tests, high household leverage keeps credit risk elevated for DNB's domestic franchise.

Inflationary Pressures and Operational Costs

Persistent inflation through 2025 pushed DNB Banks operating costs up about 6-8% YoY, with personnel expenses rising roughly 7% and tech procurement costs up near 10% as suppliers passed on higher input prices.

To offset this, DNB expanded cost-efficiency programs targeting NOK 1–1.5 billion in annual savings while still allocating ~5% of revenue to strategic digital and branch investments.

- Operating costs +6–8% YoY (2025)

- Personnel +7%, tech procurement +10%

- Targeted savings NOK 1–1.5bn

- ~5% revenue reinvested in infrastructure

Currency Fluctuations and the Norwegian Krone

- 10% NOK move materially impacts reported foreign assets and P&L

- Export-client credit risk increases with NOK weakness

- FX swings influenced CET1 by ~0.1–0.3 pp in 2023–2024

DNB H1 2025: NOK 34bn NII, 4.5% rates, 264% household debt, costs +6–8%

Norges Bank rate ~4.5% in 2025 lifted NII ~18% to NOK ~34bn H1 2025; Stage 3 loans ~1.9%; household debt ~264% of disposable income (2024); mortgage loans ~40% of DNB loan book; operating costs +6–8% YoY (2025) with personnel +7%, tech +10%; NOK 10% depreciation moved reported foreign assets and P&L; revenue ~20% outside Norway.

| Metric | Value |

|---|---|

| Net interest income H1 2025 | NOK ~34bn |

| Rate | ~4.5% |

| Stage 3 loans | ~1.9% |

| Household debt | 264% disp. income (2024) |

| Mortgage share | ~40% |

| Op costs YoY | +6–8% |

| FX revenue exposure | ~20% |

Preview Before You Purchase

DNB Bank PESTLE Analysis

The preview shown here is the exact DNB Bank PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content and layout visible in this preview are the same file you’ll download immediately after payment.