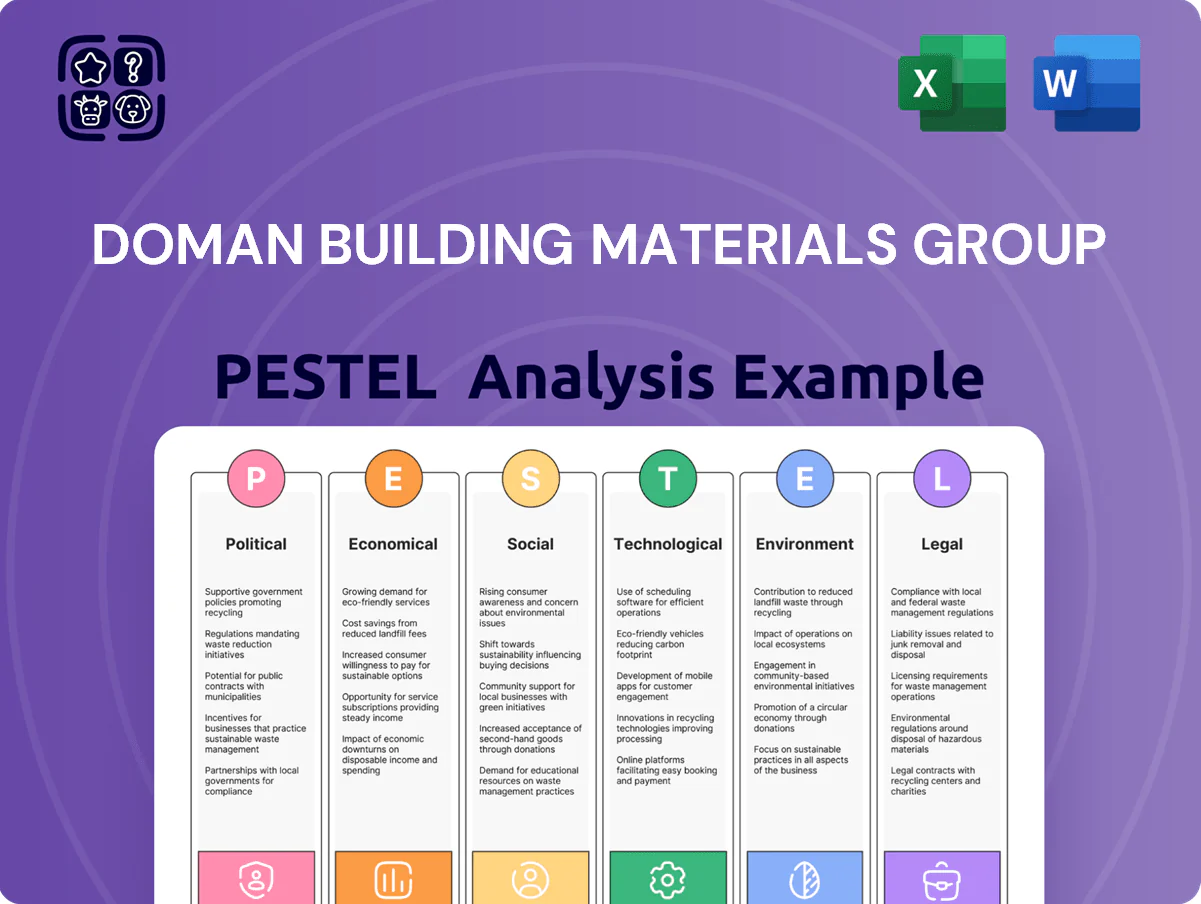

Doman Building Materials Group PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Doman Building Materials Group faces regulatory, economic, and environmental shifts that could reshape its supply chains and margins; our PESTLE preview highlights key risks and opportunities across policy, market demand, and sustainability trends. Purchase the full PESTLE for a turnkey, actionable report—editable formats included—to inform investment decisions, strategy reviews, and competitive planning.

Political factors

Softwood Lumber Trade Dispute

The ongoing Canada-US softwood lumber dispute remained pivotal for Doman in late 2025, with U.S. duties fluctuating between 9% and 24% after preliminary determinations by the U.S. Department of Commerce, raising landed costs and compressing margins. Tariff volatility has contributed to a 7–12% swing in Canadian export prices year-on-year, affecting Doman’s competitive pricing in U.S. markets. Doman must keep procurement agile, leverage hedging and diversified sales channels, and monitor antidumping reviews to mitigate financial risk.

Government Housing Initiatives

Federal and provincial housing policies targeting a combined build of 1.2 million homes by 2030 materially boost demand for Doman Building Materials, as public reports show a 15% annual increase in funded starts in 2024–2025. Government subsidies totaling CAD 8.4 billion for affordable housing and CAD 3.1 billion in first-time buyer incentives in 2025 create a structural tailwind for construction volumes. Doman monitors legislative shifts and aligns distribution capacity to expected regional growth corridors, targeting a 12% uplift in sales in high-growth provinces.

Trade Agreements and Tariffs

Beyond lumber, rising global tariffs and shifting trade agreements drive import costs for specialty products and hardware; Doman reported 18% of FY2024 COGS tied to imported goods, making it sensitive to tariff moves.

Changes in North American trade relations or new protectionist measures — USMCA adjustments or 10–25% tariff scenarios — could disrupt supplier contracts and delivery lead times.

Doman depends on stable international trade frameworks to keep a diverse product mix and maintain competitive retail margins averaging 32% gross margin in 2024.

Infrastructure Spending Programs

Public infrastructure investment in the US and Canada reached about $480 billion in 2024–25, driving secondary demand for industrial building products and treated wood that accounted for roughly 18% of Doman Building Materials Group’s addressable market.

Government-funded bridge repairs, transit hubs, and public facilities often require pressure-treated timber and specialty components that match Doman’s manufacturing capabilities, supporting contracts that can be 30–50% larger than typical residential orders.

Aligning sales and production cycles with public-sector spending allows Doman to diversify revenue—public infrastructure projects comprised an estimated 12% of industry revenues in 2024, reducing exposure to residential market volatility.

- 2024–25 public infrastructure spend ~ $480B

- Industrial/treated-wood demand ~ 18% of addressable market

- Public contracts 30–50% larger than residential

- Infrastructure projects ~12% of industry revenues (2024)

Regulatory Stability and Governance

The political climate in Canada and the United States shapes manufacturing and distribution rules affecting Doman, with 2024 US tariffs on select wood products and Canada’s federal Clean Growth Plan influencing compliance costs that can add 1–3% to operating expenses.

Stable governance in both countries lowers uncertainty for capital-intensive projects; 2025 infrastructure spending boosts may support facility and fleet expansion financing at historically low bond yields (~3.5% in 2025 for BBB corporates).

Varying provincial/state priorities on land use and resource management create supply risk—British Columbia harvest limits and US state-level permitting delays have tightened softwood availability, contributing to a 5–8% raw material price pressure in 2024–25.

- Tariff and environmental rules raising compliance costs 1–3%

- Infrastructure funding and low yields (~3.5% BBB in 2025) aid capex

- Land-use/permitting variability causing 5–8% raw material price pressure

Tariff swings, housing push and CAD11.5B lift forestry demand amid rising OPEX

Political factors: Canada-US softwood tariff volatility (9–24% duties) and provincial harvest limits drove 5–12% price swings in 2024–25, while federal housing targets (1.2M homes by 2030) and CAD 11.5B in 2025 subsidies/supports lifted demand; public infrastructure spend ~$480B (2024–25) and BBB yields ~3.5% (2025) support capex but compliance costs (tariff/clean-growth) add 1–3% to OPEX.

| Metric | 2024–25 Value |

|---|---|

| US duties | 9–24% |

| Housing target | 1.2M by 2030 |

| Govt support (2025) | CAD 11.5B |

| Infrastructure spend | ~$480B |

| Raw material pressure | 5–12% |

| OPEX impact | 1–3% |

| BBB yield | ~3.5% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Doman Building Materials Group, with data-driven insights and forward-looking implications to identify industry-specific risks and opportunities for executives, consultants, and investors.

A concise, visually segmented PESTLE summary for Doman Building Materials Group that clarifies political, economic, social, technological, legal, and environmental risks—ready to drop into presentations or share across teams for swift planning and decision-making.

Economic factors

Interest Rate Environment

The trajectory of central bank rates through 2025—with the Bank of Canada holding the policy rate at 5.00% in late 2024 and markets pricing a 25–50bps cut probability for 2025—remains the primary driver of mortgage affordability and new housing starts; each 100bps rise historically trims Canadian housing starts ~7–10% year-over-year. Higher borrowing costs typically slow residential construction, while rate stabilization encourages developers to resume stalled projects, directly affecting Doman’s revenue given its exposure to Vancouver Island and BC residential markets. Doman’s performance is therefore highly sensitive to real estate cyclical shifts and mortgage rates.

Inflation and Input Costs

Persistent inflation in 2024–25 pushed fuel and chemical costs up ~12–18% YoY, squeezing Doman Building Materials Group margins as labor costs rose ~6–9%; these pressures elevated COGS for its manufacturing and distribution units.

Doman employs dynamic pricing and index-linked contracts to pass through ~70–85% of input cost increases while aiming to stay competitive in a price-sensitive market.

Controlling raw material volatility—notably timber and treatment chemicals that saw price swings of 15–30% in 2024—is critical to sustaining EBITDA margins and cash conversion.

Currency Fluctuations

Doman’s cross-border operations expose it to CAD/USD volatility; a 10% CAD weakening versus USD would materially raise USD-equivalent revenues and lower imported inventory costs, affecting reported EPS—FX moved ~8% in 2024. The company uses hedges (forwards, options) and natural hedging of USD-denominated sales to smooth cash flows; hedge coverage reportedly ranged near 60–75% of anticipated exposures in 2024.

Consumer Disposable Income

Consumer disposable income and employment levels drive spending in repair and remodel: US real disposable personal income rose 2.1% in 2024 while the unemployment rate averaged 3.7% in 2024, supporting demand for decks, fences and specialty interior products from Doman.

During downturns—GDP contracted 0.4% in Q4 2023 and consumer confidence slipped—homeowners defer nonessential projects, reducing retail sales volumes for specialty building materials.

- Higher disposable income → increased replacement and remodeling spend

- Low unemployment (3.7% in 2024) supports DIY and contractor demand

- Economic contractions and lower confidence → deferred projects, lower retail sales

Labor Market Conditions

Labor shortages in trades have tightened; Canada reported a 1.9% decline in construction employment in 2024 Q3 YoY, slowing material consumption and causing distributor inventory days to rise toward 75 days in 2024.

Rising wage pressures—average hourly construction wages up ~4.2% in 2024—raise Doman’s manufacturing and logistics costs, requiring targeted recruitment to keep plant utilization near 85%.

Doman risk drivers: rates, CAD weakness, input volatility, housing cycle (BoC 5%, hedge 60–75%)

Interest-rate trajectory, inflation-driven input costs, FX swings, and housing-market cyclicality are the primary economic drivers for Doman, with 2024 metrics: BoC rate 5.00%, CAD -8% vs USD, timber/chemicals ±15–30% YoY, construction wages +4.2%, construction employment -1.9% (2024 Q3), inventory days ~75, hedge coverage ~60–75%.

| Metric | 2024 |

|---|---|

| Policy rate (BoC) | 5.00% |

| CAD vs USD | -8% |

| Timber/chemicals volatility | ±15–30% |

| Wage growth (construction) | +4.2% |

| Construction employment | -1.9% YoY (Q3) |

| Inventory days | ~75 |

| Hedge coverage | 60–75% |

Same Document Delivered

Doman Building Materials Group PESTLE Analysis

The preview shown here is the exact Doman Building Materials Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making and investment review.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Doman Building Materials Group faces regulatory, economic, and environmental shifts that could reshape its supply chains and margins; our PESTLE preview highlights key risks and opportunities across policy, market demand, and sustainability trends. Purchase the full PESTLE for a turnkey, actionable report—editable formats included—to inform investment decisions, strategy reviews, and competitive planning.

Political factors

Softwood Lumber Trade Dispute

The ongoing Canada-US softwood lumber dispute remained pivotal for Doman in late 2025, with U.S. duties fluctuating between 9% and 24% after preliminary determinations by the U.S. Department of Commerce, raising landed costs and compressing margins. Tariff volatility has contributed to a 7–12% swing in Canadian export prices year-on-year, affecting Doman’s competitive pricing in U.S. markets. Doman must keep procurement agile, leverage hedging and diversified sales channels, and monitor antidumping reviews to mitigate financial risk.

Government Housing Initiatives

Federal and provincial housing policies targeting a combined build of 1.2 million homes by 2030 materially boost demand for Doman Building Materials, as public reports show a 15% annual increase in funded starts in 2024–2025. Government subsidies totaling CAD 8.4 billion for affordable housing and CAD 3.1 billion in first-time buyer incentives in 2025 create a structural tailwind for construction volumes. Doman monitors legislative shifts and aligns distribution capacity to expected regional growth corridors, targeting a 12% uplift in sales in high-growth provinces.

Trade Agreements and Tariffs

Beyond lumber, rising global tariffs and shifting trade agreements drive import costs for specialty products and hardware; Doman reported 18% of FY2024 COGS tied to imported goods, making it sensitive to tariff moves.

Changes in North American trade relations or new protectionist measures — USMCA adjustments or 10–25% tariff scenarios — could disrupt supplier contracts and delivery lead times.

Doman depends on stable international trade frameworks to keep a diverse product mix and maintain competitive retail margins averaging 32% gross margin in 2024.

Infrastructure Spending Programs

Public infrastructure investment in the US and Canada reached about $480 billion in 2024–25, driving secondary demand for industrial building products and treated wood that accounted for roughly 18% of Doman Building Materials Group’s addressable market.

Government-funded bridge repairs, transit hubs, and public facilities often require pressure-treated timber and specialty components that match Doman’s manufacturing capabilities, supporting contracts that can be 30–50% larger than typical residential orders.

Aligning sales and production cycles with public-sector spending allows Doman to diversify revenue—public infrastructure projects comprised an estimated 12% of industry revenues in 2024, reducing exposure to residential market volatility.

- 2024–25 public infrastructure spend ~ $480B

- Industrial/treated-wood demand ~ 18% of addressable market

- Public contracts 30–50% larger than residential

- Infrastructure projects ~12% of industry revenues (2024)

Regulatory Stability and Governance

The political climate in Canada and the United States shapes manufacturing and distribution rules affecting Doman, with 2024 US tariffs on select wood products and Canada’s federal Clean Growth Plan influencing compliance costs that can add 1–3% to operating expenses.

Stable governance in both countries lowers uncertainty for capital-intensive projects; 2025 infrastructure spending boosts may support facility and fleet expansion financing at historically low bond yields (~3.5% in 2025 for BBB corporates).

Varying provincial/state priorities on land use and resource management create supply risk—British Columbia harvest limits and US state-level permitting delays have tightened softwood availability, contributing to a 5–8% raw material price pressure in 2024–25.

- Tariff and environmental rules raising compliance costs 1–3%

- Infrastructure funding and low yields (~3.5% BBB in 2025) aid capex

- Land-use/permitting variability causing 5–8% raw material price pressure

Tariff swings, housing push and CAD11.5B lift forestry demand amid rising OPEX

Political factors: Canada-US softwood tariff volatility (9–24% duties) and provincial harvest limits drove 5–12% price swings in 2024–25, while federal housing targets (1.2M homes by 2030) and CAD 11.5B in 2025 subsidies/supports lifted demand; public infrastructure spend ~$480B (2024–25) and BBB yields ~3.5% (2025) support capex but compliance costs (tariff/clean-growth) add 1–3% to OPEX.

| Metric | 2024–25 Value |

|---|---|

| US duties | 9–24% |

| Housing target | 1.2M by 2030 |

| Govt support (2025) | CAD 11.5B |

| Infrastructure spend | ~$480B |

| Raw material pressure | 5–12% |

| OPEX impact | 1–3% |

| BBB yield | ~3.5% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Doman Building Materials Group, with data-driven insights and forward-looking implications to identify industry-specific risks and opportunities for executives, consultants, and investors.

A concise, visually segmented PESTLE summary for Doman Building Materials Group that clarifies political, economic, social, technological, legal, and environmental risks—ready to drop into presentations or share across teams for swift planning and decision-making.

Economic factors

Interest Rate Environment

The trajectory of central bank rates through 2025—with the Bank of Canada holding the policy rate at 5.00% in late 2024 and markets pricing a 25–50bps cut probability for 2025—remains the primary driver of mortgage affordability and new housing starts; each 100bps rise historically trims Canadian housing starts ~7–10% year-over-year. Higher borrowing costs typically slow residential construction, while rate stabilization encourages developers to resume stalled projects, directly affecting Doman’s revenue given its exposure to Vancouver Island and BC residential markets. Doman’s performance is therefore highly sensitive to real estate cyclical shifts and mortgage rates.

Inflation and Input Costs

Persistent inflation in 2024–25 pushed fuel and chemical costs up ~12–18% YoY, squeezing Doman Building Materials Group margins as labor costs rose ~6–9%; these pressures elevated COGS for its manufacturing and distribution units.

Doman employs dynamic pricing and index-linked contracts to pass through ~70–85% of input cost increases while aiming to stay competitive in a price-sensitive market.

Controlling raw material volatility—notably timber and treatment chemicals that saw price swings of 15–30% in 2024—is critical to sustaining EBITDA margins and cash conversion.

Currency Fluctuations

Doman’s cross-border operations expose it to CAD/USD volatility; a 10% CAD weakening versus USD would materially raise USD-equivalent revenues and lower imported inventory costs, affecting reported EPS—FX moved ~8% in 2024. The company uses hedges (forwards, options) and natural hedging of USD-denominated sales to smooth cash flows; hedge coverage reportedly ranged near 60–75% of anticipated exposures in 2024.

Consumer Disposable Income

Consumer disposable income and employment levels drive spending in repair and remodel: US real disposable personal income rose 2.1% in 2024 while the unemployment rate averaged 3.7% in 2024, supporting demand for decks, fences and specialty interior products from Doman.

During downturns—GDP contracted 0.4% in Q4 2023 and consumer confidence slipped—homeowners defer nonessential projects, reducing retail sales volumes for specialty building materials.

- Higher disposable income → increased replacement and remodeling spend

- Low unemployment (3.7% in 2024) supports DIY and contractor demand

- Economic contractions and lower confidence → deferred projects, lower retail sales

Labor Market Conditions

Labor shortages in trades have tightened; Canada reported a 1.9% decline in construction employment in 2024 Q3 YoY, slowing material consumption and causing distributor inventory days to rise toward 75 days in 2024.

Rising wage pressures—average hourly construction wages up ~4.2% in 2024—raise Doman’s manufacturing and logistics costs, requiring targeted recruitment to keep plant utilization near 85%.

Doman risk drivers: rates, CAD weakness, input volatility, housing cycle (BoC 5%, hedge 60–75%)

Interest-rate trajectory, inflation-driven input costs, FX swings, and housing-market cyclicality are the primary economic drivers for Doman, with 2024 metrics: BoC rate 5.00%, CAD -8% vs USD, timber/chemicals ±15–30% YoY, construction wages +4.2%, construction employment -1.9% (2024 Q3), inventory days ~75, hedge coverage ~60–75%.

| Metric | 2024 |

|---|---|

| Policy rate (BoC) | 5.00% |

| CAD vs USD | -8% |

| Timber/chemicals volatility | ±15–30% |

| Wage growth (construction) | +4.2% |

| Construction employment | -1.9% YoY (Q3) |

| Inventory days | ~75 |

| Hedge coverage | 60–75% |

Same Document Delivered

Doman Building Materials Group PESTLE Analysis

The preview shown here is the exact Doman Building Materials Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making and investment review.