Domino's Pizza Boston Consulting Group Matrix

Download Your Competitive Advantage

Domino’s Pizza sits at an inflection point—its global delivery tech and strong brand suggest “Stars” in digital-forward markets, while legacy operations and regional competitors create pockets of “Question Marks” and occasional “Dogs.” This preview highlights high-level quadrant cues and strategic tensions; purchase the full BCG Matrix for a complete quadrant mapping, data-driven recommendations, and actionable capital-allocation guidance to sharpen your market moves.

Stars

Digital Ordering Ecosystem

As of late 2025, digital channels drive over 85% of Domino's U.S. retail sales, marking a high-growth, dominant-market-share segment in the BCG Matrix.

Domino's keeps investing in its proprietary app and AI ordering platform—R&D and tech capex rose ~12% in 2024–25—to sustain its digital lead over competitors.

The digital-first strategy boosts average ticket size (roughly +6–8%) and repeat rates, making digital the primary engine of modern revenue and loyalty.

China Market Operations

Domino's China master franchisee DPC Dash had opened over 1,300 stores by end-2025 and guided ~350 new stores for 2026, driving rapid unit growth and heavy capital spend that fits a BCG Star profile.

Same-store sales in China rose for 30+ consecutive quarters through 2025, signaling rising market share and strong demand; these gains plus annual store-level investments (capex per new store ≈ $250–350k) mark high-growth, high-share status.

Indian Market Presence

With over 1,500 stores in India, Domino's is a Stars-category market, showing rapid growth and high delivery adoption; same-store sales rose double digits in 2025, driven by a digital mix that now accounts for ~70% of orders.

Carryout Acceleration Strategy

Carryout has become a Star in Domino’s BCG matrix after fortressing—adding dense stores to cut pickup time—driving late 2025 carryout same-store sales up 8.4% year-over-year via targeted digital promos and the Best Deal Ever platform; the segment is winning share from dine-in rivals but needs continued capex for store densification (Domino’s reported ~\$220m incremental carryout store investment in 2025).

- Same-store carryout sales +8.4% (late 2025)

- ~\$220m capex for densification (2025)

- Share gains vs dine-in: market share +1.6 pts (2025)

- Lift from Best Deal Ever: digital order growth +12% (Q4 2025)

Domino's Rewards Program

The revamped Domino's Rewards Program reached over 35 million active members by end-2025, driving a double-digit lift in repeat orders and aiding retention amid slowing same-store sales.

Personalized offers and app-driven engagement made it an industry digital leader, increasing average order frequency by ~12% and contribution margin per-member by roughly $4 annually.

It needs steady marketing spend—roughly $150–200M yearly—to defend share versus delivery aggregators and sustain growth.

- 35M active members (2025)

- ~12% higher order frequency

- +$4 contribution margin/member/year

- $150–200M annual marketing support

Digital Dominance, Rapid China/India Expansion & Strong Carryout Growth (2025 Highlights)

Stars: Digital, China, India, and Carryout show high growth and high share—digital >85% U.S. sales, 35M rewards members (2025), China 1,300+ stores (end-2025) guiding 350 in 2026, India 1,500+ stores with double-digit SSS growth (2025), carryout SSS +8.4% (late 2025), $220M 2025 densification capex, $150–200M annual marketing.

| Metric | Value (2025) |

|---|---|

| Digital U.S. sales | >85% |

| Rewards members | 35M |

| China stores | 1,300+ |

| India stores | 1,500+ |

| Carryout SSS | +8.4% |

| Densification capex | $220M |

| Marketing spend | $150–200M |

What is included in the product

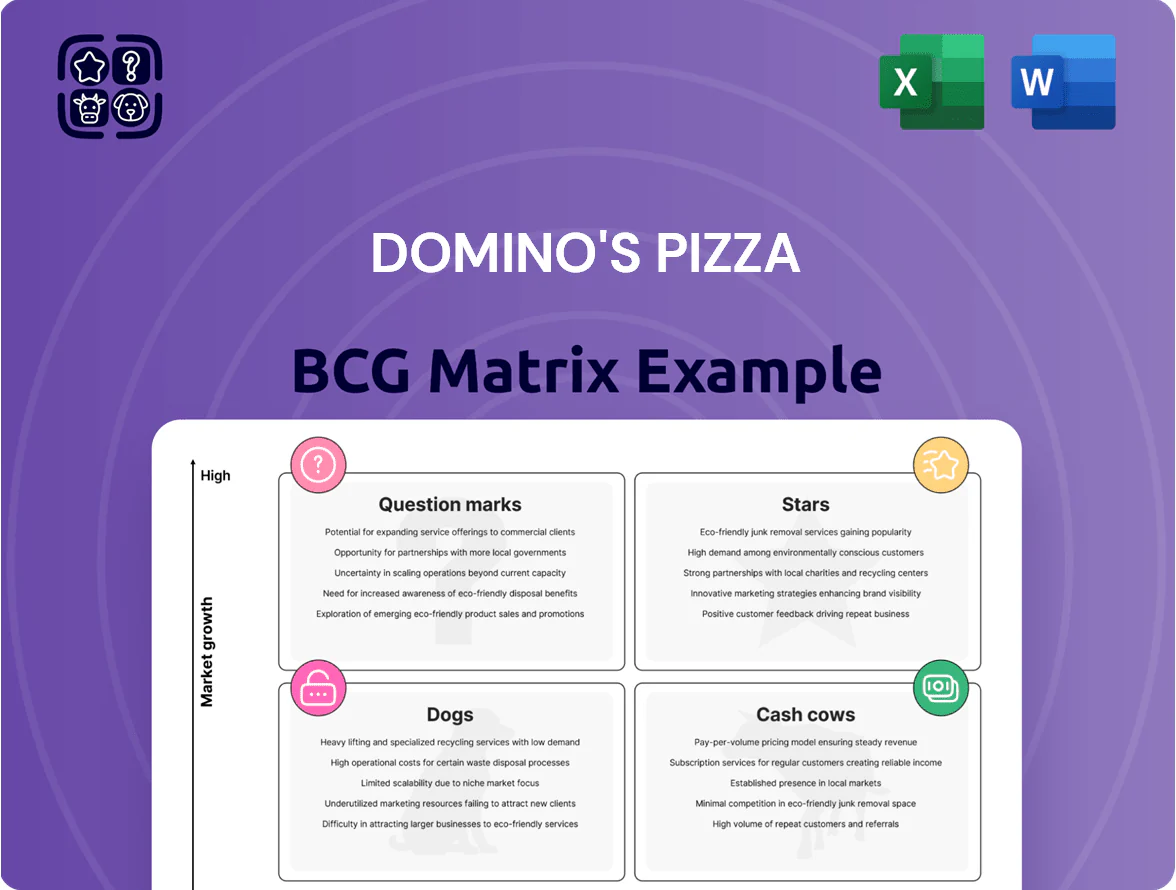

BCG Matrix review of Domino’s: identifies Stars, Cash Cows, Question Marks, Dogs with investment, hold, divest guidance and trend impacts.

One-page Domino's BCG Matrix placing each unit in a quadrant for fast strategic review and presentation-ready sharing.

Cash Cows

U.S. Franchise Royalties

Domino’s U.S. franchise royalties are a cash cow: mature, high-share, high-margin, recurring income with minimal capital needs, yielding steady operating margin uplift and free cash flow.

By late 2025 about 99% of Domino’s ~20,000 global stores were franchised, producing roughly $1.2B in global royalties and fees in FY2024, per company filings.

Those royalties fund R&D, cover interest on $3.5B net debt (2024), and bankroll expansion into Star markets such as India and Brazil.

Global Supply Chain Services

Domino's Global Supply Chain Services generates over 60% of Domino's 2024 consolidated revenue, supplying ingredients and equipment to 18,000+ stores and converting large-scale procurement into steady gross margins near 28% and operating cash conversion above 85% in 2024.

Core Pizza Menu Items

Standard offerings like Hand-Tossed and Thin Crust account for roughly 60–65% of Domino’s U.S. pizza sales (2024 company data), holding dominant share in the mature pizza market and needing minimal promo spend versus new SKUs.

Standardized prep yields high margins—corporate reports show systemwide food cost ~35% and core pizzas delivering most of the EBITDA that funds R&D and limited-time tests.

Mature European Markets

Mature European Markets like the UK and Ireland hold dominant share in Domino’s portfolio, operating in low-growth but stable conditions and delivering predictable retail sales and royalty income.

By end-2025 Domino’s targets ~1,600 stores in these markets, generating steady cash flow—UK system sales reached £1.7bn in 2024 and franchise royalties contributed ~£120m—funds often redeployed to higher-growth Asian initiatives.

- Stable, low growth; high market share

- ~1,600 stores target by 31-Dec-2025

- UK system sales ~£1.7bn (2024)

- Franchise royalties ~£120m (2024)

- Cash funds Asian expansion

Brand Licensing and Fees

Brand licensing and master-franchise fees generate high-margin, low-overhead cash for Domino’s, with 2024 franchising revenue ~ $1.1 billion and royalty-related margins above 80%—leveraging global brand equity in saturated mature markets like the US and UK.

This passive income supports dividend capacity; Domino’s paid $1.44 per share in dividends in 2024, funded in part by steady royalty inflows and minimal incremental cost.

- 2024 franchising revenue: ~$1.1B

- Royalty margins: ~80%+

- Key markets: US, UK, Australia

- Supports dividends: $1.44/share in 2024

Domino’s cash engines: $1.2B royalties + high‑margin supply chain fuel growth & payouts

Domino’s cash cows: franchised royalties and Global Supply Chain deliver high-margin, recurring cash—~$1.2B royalties/fees (FY2024), 99% franchised by late-2025, supply-chain ~60% revenue with ~28% gross margin (2024), funds debt service ($3.5B net debt, 2024), R&D, dividends ($1.44/share, 2024) and Asian expansion.

| Metric | 2024 |

|---|---|

| Royalties/fees | $1.2B |

| Franchised stores | ~99% of 20,000 |

| Supply-chain rev% | ~60% |

| Net debt | $3.5B |

What You See Is What You Get

Domino's Pizza BCG Matrix

The file you're previewing is the exact Domino's Pizza BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just a fully formatted, strategy-ready document designed for clear portfolio analysis. This preview mirrors the final deliverable, complete with market-backed positioning, growth-share plotting, and concise strategic recommendations. Once purchased, the full file is immediately downloadable and editable for presentations, planning, or client use—no surprises, no further edits required.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Domino’s Pizza sits at an inflection point—its global delivery tech and strong brand suggest “Stars” in digital-forward markets, while legacy operations and regional competitors create pockets of “Question Marks” and occasional “Dogs.” This preview highlights high-level quadrant cues and strategic tensions; purchase the full BCG Matrix for a complete quadrant mapping, data-driven recommendations, and actionable capital-allocation guidance to sharpen your market moves.

Stars

Digital Ordering Ecosystem

As of late 2025, digital channels drive over 85% of Domino's U.S. retail sales, marking a high-growth, dominant-market-share segment in the BCG Matrix.

Domino's keeps investing in its proprietary app and AI ordering platform—R&D and tech capex rose ~12% in 2024–25—to sustain its digital lead over competitors.

The digital-first strategy boosts average ticket size (roughly +6–8%) and repeat rates, making digital the primary engine of modern revenue and loyalty.

China Market Operations

Domino's China master franchisee DPC Dash had opened over 1,300 stores by end-2025 and guided ~350 new stores for 2026, driving rapid unit growth and heavy capital spend that fits a BCG Star profile.

Same-store sales in China rose for 30+ consecutive quarters through 2025, signaling rising market share and strong demand; these gains plus annual store-level investments (capex per new store ≈ $250–350k) mark high-growth, high-share status.

Indian Market Presence

With over 1,500 stores in India, Domino's is a Stars-category market, showing rapid growth and high delivery adoption; same-store sales rose double digits in 2025, driven by a digital mix that now accounts for ~70% of orders.

Carryout Acceleration Strategy

Carryout has become a Star in Domino’s BCG matrix after fortressing—adding dense stores to cut pickup time—driving late 2025 carryout same-store sales up 8.4% year-over-year via targeted digital promos and the Best Deal Ever platform; the segment is winning share from dine-in rivals but needs continued capex for store densification (Domino’s reported ~\$220m incremental carryout store investment in 2025).

- Same-store carryout sales +8.4% (late 2025)

- ~\$220m capex for densification (2025)

- Share gains vs dine-in: market share +1.6 pts (2025)

- Lift from Best Deal Ever: digital order growth +12% (Q4 2025)

Domino's Rewards Program

The revamped Domino's Rewards Program reached over 35 million active members by end-2025, driving a double-digit lift in repeat orders and aiding retention amid slowing same-store sales.

Personalized offers and app-driven engagement made it an industry digital leader, increasing average order frequency by ~12% and contribution margin per-member by roughly $4 annually.

It needs steady marketing spend—roughly $150–200M yearly—to defend share versus delivery aggregators and sustain growth.

- 35M active members (2025)

- ~12% higher order frequency

- +$4 contribution margin/member/year

- $150–200M annual marketing support

Digital Dominance, Rapid China/India Expansion & Strong Carryout Growth (2025 Highlights)

Stars: Digital, China, India, and Carryout show high growth and high share—digital >85% U.S. sales, 35M rewards members (2025), China 1,300+ stores (end-2025) guiding 350 in 2026, India 1,500+ stores with double-digit SSS growth (2025), carryout SSS +8.4% (late 2025), $220M 2025 densification capex, $150–200M annual marketing.

| Metric | Value (2025) |

|---|---|

| Digital U.S. sales | >85% |

| Rewards members | 35M |

| China stores | 1,300+ |

| India stores | 1,500+ |

| Carryout SSS | +8.4% |

| Densification capex | $220M |

| Marketing spend | $150–200M |

What is included in the product

BCG Matrix review of Domino’s: identifies Stars, Cash Cows, Question Marks, Dogs with investment, hold, divest guidance and trend impacts.

One-page Domino's BCG Matrix placing each unit in a quadrant for fast strategic review and presentation-ready sharing.

Cash Cows

U.S. Franchise Royalties

Domino’s U.S. franchise royalties are a cash cow: mature, high-share, high-margin, recurring income with minimal capital needs, yielding steady operating margin uplift and free cash flow.

By late 2025 about 99% of Domino’s ~20,000 global stores were franchised, producing roughly $1.2B in global royalties and fees in FY2024, per company filings.

Those royalties fund R&D, cover interest on $3.5B net debt (2024), and bankroll expansion into Star markets such as India and Brazil.

Global Supply Chain Services

Domino's Global Supply Chain Services generates over 60% of Domino's 2024 consolidated revenue, supplying ingredients and equipment to 18,000+ stores and converting large-scale procurement into steady gross margins near 28% and operating cash conversion above 85% in 2024.

Core Pizza Menu Items

Standard offerings like Hand-Tossed and Thin Crust account for roughly 60–65% of Domino’s U.S. pizza sales (2024 company data), holding dominant share in the mature pizza market and needing minimal promo spend versus new SKUs.

Standardized prep yields high margins—corporate reports show systemwide food cost ~35% and core pizzas delivering most of the EBITDA that funds R&D and limited-time tests.

Mature European Markets

Mature European Markets like the UK and Ireland hold dominant share in Domino’s portfolio, operating in low-growth but stable conditions and delivering predictable retail sales and royalty income.

By end-2025 Domino’s targets ~1,600 stores in these markets, generating steady cash flow—UK system sales reached £1.7bn in 2024 and franchise royalties contributed ~£120m—funds often redeployed to higher-growth Asian initiatives.

- Stable, low growth; high market share

- ~1,600 stores target by 31-Dec-2025

- UK system sales ~£1.7bn (2024)

- Franchise royalties ~£120m (2024)

- Cash funds Asian expansion

Brand Licensing and Fees

Brand licensing and master-franchise fees generate high-margin, low-overhead cash for Domino’s, with 2024 franchising revenue ~ $1.1 billion and royalty-related margins above 80%—leveraging global brand equity in saturated mature markets like the US and UK.

This passive income supports dividend capacity; Domino’s paid $1.44 per share in dividends in 2024, funded in part by steady royalty inflows and minimal incremental cost.

- 2024 franchising revenue: ~$1.1B

- Royalty margins: ~80%+

- Key markets: US, UK, Australia

- Supports dividends: $1.44/share in 2024

Domino’s cash engines: $1.2B royalties + high‑margin supply chain fuel growth & payouts

Domino’s cash cows: franchised royalties and Global Supply Chain deliver high-margin, recurring cash—~$1.2B royalties/fees (FY2024), 99% franchised by late-2025, supply-chain ~60% revenue with ~28% gross margin (2024), funds debt service ($3.5B net debt, 2024), R&D, dividends ($1.44/share, 2024) and Asian expansion.

| Metric | 2024 |

|---|---|

| Royalties/fees | $1.2B |

| Franchised stores | ~99% of 20,000 |

| Supply-chain rev% | ~60% |

| Net debt | $3.5B |

What You See Is What You Get

Domino's Pizza BCG Matrix

The file you're previewing is the exact Domino's Pizza BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just a fully formatted, strategy-ready document designed for clear portfolio analysis. This preview mirrors the final deliverable, complete with market-backed positioning, growth-share plotting, and concise strategic recommendations. Once purchased, the full file is immediately downloadable and editable for presentations, planning, or client use—no surprises, no further edits required.